This report examines the common economic factors that continue to drive conflict in Iraq, Libya, Syria and Yemen. It also makes specific recommendations to Western policymakers addressing these types of sub-economies in detail.

Chatham House report

Published 25 June 2019

Updated 18 October 2023

ISBN: 978 1 78413 332 0

This report examines the common economic factors that continue to drive conflict in Iraq, Libya, Syria and Yemen. It also makes specific recommendations to Western policymakers addressing these types of sub-economies in detail.

In order to examine the development of conflict sub-economies in Iraq, Libya, Syria and Yemen, one must first understand the national context: most notably the evolution and current status of each conflict, as well as the economic systems that pre-dated armed conflict and have evolved as a result of it. Here, it is worth noting that all four countries have legacies of long-term dictatorial rule going back to the 1960s. These legacies have played an important part in shaping current political and economic struggles.

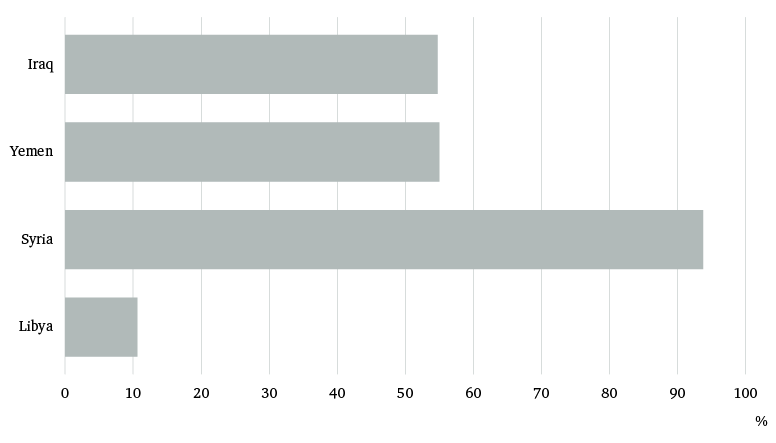

There are significant differences in population size between Iraq (38.27 million in 2017), Libya (6.38 million in 2017), Syria (18.27 million in 2017 – down from 21.96 million in 2011) and Yemen (28.25 million in 2017).39 The extent to which the local population in each country has been directly affected by violent conflict differs markedly. According to 2016 World Bank calculations, more than 90 per cent of Syrians had been directly affected by conflict. In Yemen and Iraq, that number falls to around 55 per cent, while in Libya it is 10 per cent.40

As of April 2019, the development of conflict in each of the four countries was at different stages. This report does not seek to analyse the current status of each conflict, but it is necessary nonetheless to outline the salient aspects of the conflicts and describe the principal actors in order to provide a grounding for the discussion of conflict sub-economies that follows.

Despite celebrating the end of ISIS’s territorial rule in their country in 2017, Iraqis continue to share concerns over how peace will be ensured. Iraq’s recent history reveals a poor track record of converting military victories into longer-term political solutions. A nationalist and populist protest movement has arisen throughout the country, reframing a conflict hitherto debated most often in terms of ethno-sectarianism into a class-based narrative of ‘citizens versus elites’.41

Despite celebrating the end of ISIS’s territorial rule in their country in 2017, Iraqis continue to share concerns over how peace will be ensured

Multiple armed actors, loyal to political parties rather than to state institutions, fought together to achieve the victory against ISIS. They now compete to fill the vacuum left by ISIS’s territorial losses, their rivalry occurring along and around the main economic routes once used by ISIS. The competing actors in northern Iraq and the recently liberated areas include Kurdish Peshmerga armed groups, affiliated to either the Kurdistan Democratic Party (KDP) or the Patriotic Union of Kurdistan (PUK); the Popular Mobilization Units (PMU, or al-Hashd al-Shaabi); and armed groups linked to local tribes. At the same time, despite its territorial losses, ISIS continues to operate underground in several provinces,42 while the weak state conditions that had allowed ISIS to flourish remain unaddressed. Since 2003, neither the central government nor local representatives have been able to provide stability or basic services. This has allowed groups such as ISIS at times to exploit governance vacuums in the pursuit of legitimacy, resources and power.

Following the 2011 overthrow of the regime headed by Muammar Gaddafi, Libya’s slide back into conflict in 2014 resulted in the emergence of rival governance structures, a split that remains unresolved. The Libyan Political Agreement, brokered under the auspices of the UN in December 2015, led to the creation of the Government of National Accord (GNA) under the leadership of a nine-member Presidency Council. Yet the GNA has failed to become the unity government envisaged. Members representing the east of the country soon boycotted the Presidency Council, and the internationally recognized parliament failed to ratify the Libyan Political Agreement, meaning that the GNA has no grounding in Libyan law. Consequently, it nominally owes its continuing existence to support from Western actors – though in reality the GNA has little power to influence events on the ground. Armed groups remain active and beyond its control. The most powerful military actor, Khalifa Haftar, leads a coalition of tribal forces and regular army units under the banner of the Libyan Arab Armed Forces (but still commonly referred to as the Libyan National Army or LNA).43 Haftar was notably excluded from the Libyan Political Agreement, but has since been elevated to the rank of field marshal and appointed commander of the Libyan Armed Forces by the House of Representatives, the eastern-based parliament recognized by the international community.44

The blurred line between state and non-state armed groups further complicates the situation. Armed groups technically affiliated with state entities often operate autonomously, while competing with other quasi-state actors for control of territory, revenue-generating opportunities and influence. International efforts to chart a route out of Libya’s governance crisis continue to flounder. Within this context, a low-intensity conflict rumbles on, characterized by continued competitive violence as rival groups seek control of infrastructure, transit areas and state bodies. LNA forces have undertaken lengthy military operations in Benghazi and Derna, causing thousands of casualties and displacing thousands more. At the time of writing, the LNA was in the midst of an offensive on the capital, Tripoli, in what amounts to the third outbreak of civil war since 2010.

As of the spring of 2019, Syria remained divided into four distinct zones, three of which were controlled by combinations of local and international actors. In the most populated and urbanized western part of the country, the regime of President Assad is back in charge. This has been made possible through the active backing of Russia and Iran, which continue to play important security, political and economic roles. North of Aleppo, rebel opposition groups funded and armed by Turkey control a second area, which is being increasingly integrated into the Turkish economy. Meanwhile, the northeast is controlled by the Kurdish-dominated Syrian Democratic Forces, with the support of the US. A fourth region, in the northwest, broadly corresponding to the Idlib governorate, is under the control of Hayat Tahrir al-Sham (HTS), a Salafi-jihadi organization.45 This is the only part of Syria that is devoid of any significant foreign presence.

An internationally sponsored peace process led by the UN has sought to promote a political solution, but it has been gradually eclipsed by the Astana process, a tripartite forum grouping Turkey, Russia and Iran that has the more modest ambition of finding a short-term security arrangement. While the Assad regime’s successes in the past couple of years have ended calls for his departure, victory on the ground has not yet resulted in full acceptance of his rule by the West and the Arab world. Western sanctions also continue to isolate the Syrian regime. The scale of violence in the country has declined, although at the time of writing the regime was engaged in a new offensive in Idlib. A lasting political solution remains distant.

The Houthis have become adept at coercing businesses, government institutions and other economic actors into cooperating with the de facto authorities in Sanaa

Yemen’s civil war has divided the country into multiple, rival zones of control, each with its own system – and in some cases multiple systems – of governance, security and economic management. Northwest Yemen is controlled by Houthi rebels who entered Sanaa in September 2014 and then spread east, west and south in a quest to control the entire country, in alliance with loyalists of ex-president Ali Abdullah Saleh. The Houthis killed Saleh amidst rising internal tensions in December 2017, and have since moved to control all aspects of life in Yemen’s highlands and along its west coast. They have become adept at coercing businesses, government institutions and other economic actors into cooperating with the de facto authorities in Sanaa.

To the east of Sanaa, a network of military and tribal players from the al-Jawf, Mareb and northern Hadramawt governorates has emerged as the most important grouping in this region. Members of this network share common ties to Islah, Yemen’s main Sunni Islamist party.

In the south of Yemen, rival factions vie for power and legitimacy. These include the technocrats and security forces affiliated with the internationally recognized government of Abd Rabbu Mansour Hadi. They also include a web of political and security forces linked to the Southern Transitional Council – a self-styled government-in-waiting that is closely linked to the United Arab Emirates (UAE) – as well as multiple UAE-backed armed Salafist-led groups. Members of the latter include secessionists, Salafists and indeed Salafist-secessionists, many of which defy classification. The UAE-backed southern networks and Islah harbour deep animosity towards one another: in Taiz, a front-line city in central Yemen, UAE-backed forces and allies of Islah clash regularly, making it all but impossible to govern the city. While a fragile UN-brokered agreement to freeze the fighting and demilitarize the key western port of Hodeida still holds, fighting continues in other areas of the country.

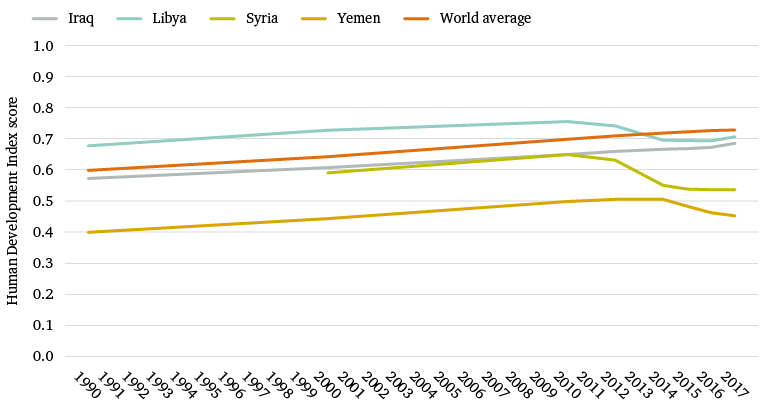

In undertaking a comparative analysis of the conflict economies of Iraq, Libya, Syria and Yemen, we began by acknowledging the significant differences in their conflict histories. There are also major differences between the four countries in terms of development indicators and economic structure. On the UN’s Human Development Index, a summary measure of average achievement in key dimensions of human development (a long and healthy life, knowledge and education, and a decent standard of living), Libya ranked 108th out of 189 countries in 2017, while Iraq ranked 120th, Syria 155th and Yemen 178th.46

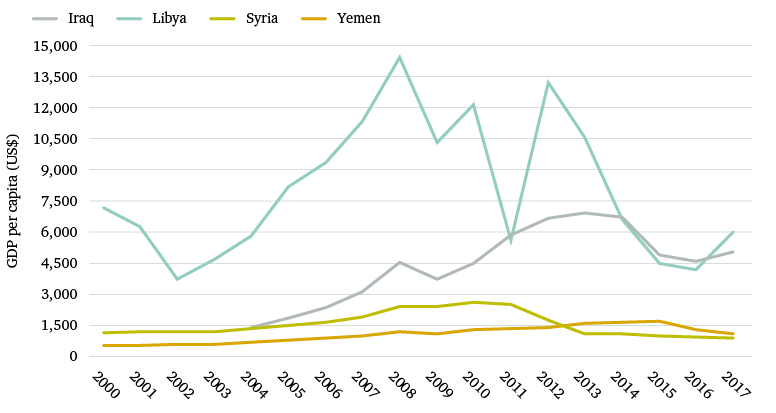

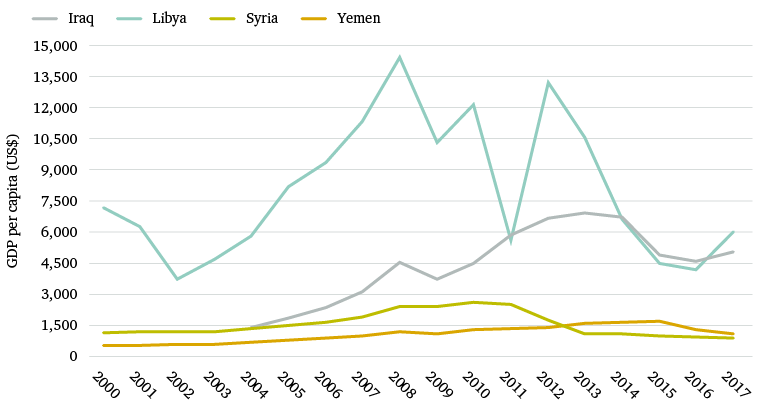

While official GDP statistics have limitations,47 they do offer a useful entry point for comparison of the economies in question and allow a relatively consistent basis for that comparison. GDP per capita in oil-rich Libya was $5,978 in 2017, while in Iraq it was $5,017. Syria and Yemen do not have natural resources on the same scale. GDP per capita was only $910 in Syria and $1,106 in Yemen in 2017 (see Figure 3).48 These differences have had a significant impact on the nature of the conflict economies to have developed. Oil revenues are the dominant source of rents in Iraq and Libya. In Syria and Yemen, shortfalls in funding have forced rival groups to adopt a range of coping strategies and seek alternative forms of revenue, most notably from external actors.

Iraq is the most oil-dependent state on earth. In 2015, the oil and gas sector accounted for 58 per cent of Iraqi GDP, 99 per cent of the country’s exports and over 90 per cent of central government revenue.49 At the same time, Iraq has not had an economy free from conflict in four decades. The Iran–Iraq war (1980–88), the first Gulf war (1990–91), international sanctions and intermittent airstrikes (1990s), the US-led invasion and subsequent occupation (2003–05), the first civil war (2006–08), and the emergence of ISIS (2013–18) have all conditioned the development of Iraq’s conflict economy. Despite the recapture of ISIS-held territory, the economic situation is deteriorating: gross national income (GNI) per capita has fallen from $6,900 in 2013 to $4,700 in 2017.50

Control of the Iraqi state is key to accessing oil revenues, allowing leaders to sustain patronage networks and remove opponents. Since the ousting of Saddam Hussein in 2003, political and military elites have competed for control of the state and its institutions in order to access resources. The decision-making autonomy of political and security officials allows them to award contracts to preferred business partners and benefit from a culture of kickbacks. These networks of officials have captured parts of the informal economy. Political leaders also maintain relationships with state-sanctioned armed groups, which extract rents and taxes from smugglers and informal businesspeople. Mainstream political parties (divided along Shia, Sunni and Kurdish identity lines) use their access to state-recognized (and therefore state-legitimized) armed groups – such as the Kurdish Peshmerga, the PMU and tribal forces – to maintain influence over the conflict economy.51

Iraqi officials often hold or control multiple political, economic and military roles, a status that provides lucrative economic opportunities in both the public and private sectors. After the Iran–Iraq war, the state was bankrupt. By 1990, many state-owned enterprises had been privatized. As a result, the regime had to cultivate new alliances with newly empowered economic actors. These mutually beneficial relationships strengthened the black market and the smuggling sector, seeding the informal economic networks that helped Iraq survive international sanctions. The networks incorporated a wide array of actors: government officials, Baathist regime-allied individuals, external business partners, local political and business entrepreneurs, tribal leaders and workers within the oil sector.

In the 1990s, international sanctions on oil exports pushed Saddam’s Baathist regime to establish alternative overland smuggling routes via Jordan, Syria and Turkey (a practice known as the ‘truckers’ trade’), as well as maritime smuggling routes via the Persian Gulf. Those involved in this trade became known as the ‘cats of the embargo’ (qitat al-hisar). The informal economy also provided income for many of the estimated 200,000 battle-trained soldiers who had returned from the Iran–Iraq war and the Gulf war but could not find employment. Today, war veterans (as well as lower-class labourers) remain closely associated with smuggling, often working as truck drivers, in a sector that has become increasingly dangerous. Traversing smuggling routes necessitates contact with an array of armed forces.

The rise of ISIS in 2013 and 2014 revealed the extent to which the conflict economy had become embedded. ISIS engaged in very similar economic practices to those that had begun during the Baathist era – it even employed many of the same Baathist loyalists, who had experience with the system as government economic advisers. By 2014, ISIS had become the richest terrorist organization ‘in history’ after conquering almost one-third of Iraq’s territory in a matter of months. Annual turnover equivalent to an estimated $2 billion provided the Salafi-jihadi organization with unprecedented finances that fuelled its fight against the Iraqi armed forces and their international allies.52

By 2014, ISIS had become the richest terrorist organization ‘in history’ after conquering almost one-third of Iraq’s territory in a matter of months

Many policymakers and writers identified the swift rise of ISIS with its command of a ‘new’ conflict economy, one based on the proceeds from oil and gas smuggling and taxation policies. Yet this is a misconception. The principal actors in, and overall structure of, the conflict economy pre-dated ISIS and even the 2003 US-led invasion. Instead, the present economic networks had their roots in the post-Iran–Iraq-war period. ISIS simply captured these networks by taking over the operating environment and employing Baathists and traders experienced in using the trafficking and trading routes. Since the collapse of ISIS, control of such networks has fragmented: now a mixture of the forces jointly responsible for defeating ISIS – the PMU, the Peshmerga, tribal forces, and individuals in the armed forces of the ministries of defence and the interior – profit from the same trade and smuggling routes.

Libya’s economy is heavily dependent on hydrocarbons: an estimated 96 per cent of state revenues were derived from the sale of oil and gas in 2013,53 leaving the economy highly vulnerable to fluctuations in international oil and gas prices. Since 2010, successive governments have replicated Gaddafi-era policies of free or state-subsidized social services but have circumvented legal restraints on public spending to do so. An estimated 25,000 fighters participated in the uprising against Gaddafi, but 10 times that figure were believed to have received payments as ‘thuwwar’ (revolutionary fighters) as of May 2012. In 2013, the government confirmed that it would continue making these payments.54 However, runaway expenditure on state-sector salaries proved increasingly unaffordable: international oil prices were falling and Libyan oil production was hampered by a major blockade of its eastern oil fields. In response, the state drew upon its foreign currency reserves to cover the deficit between government spending and state revenues. Libya’s reserves consequently fell from an estimated $115 billion in 2011 to around $75 billion in 2017, according to the World Bank.55

Most of Libya’s oil and gas wealth is distributed through state channels, making the control of the state itself the prime target for competing actors. The effects of the conflict economy are visible in Libya’s 2018 budget, with state-sector salaries accounting for 57 per cent of the agreed budget; this compares with an estimated 17 per cent in 2010, prior to the overthrow of the Gaddafi regime.56 However, the increase excludes spending by rival authorities in the east of the country, which official data do not account for.57 Most armed groups remain on the state payroll, giving the Libyan government the peculiar distinction of funding its own civil war.

As detailed later, the fragmentation of the Libyan state has evolved into a competition for control of state institutions, assets and revenue streams. Amid the battle among political actors, the Central Bank of Libya (CBL) has put a brake on runaway expenditure of Libya’s foreign currency reserves. However, the independence of the CBL has been constrained by a highly volatile security environment.

Import fraud has become a critical part of Libya’s conflict economy. The growing disparity between the official rate for the dinar and the black-market rate created substantial opportunities for arbitrage, until September 2018 when a fee was imposed on access to foreign currency (over which the CBL has a monopoly) for the import of goods. As also detailed in Box 2, import fraud has become a significant revenue-generation opportunity for networks of profiteers – directly involving, among others, armed groups that have coercively and cooperatively exploited privileged access to foreign exchange. In addition to currency arbitrage, profiteers use fraudulent documentary letters of credit for the import of goods to transfer large amounts of money outside the country. Sometimes the value of goods imported is less than that documented in the letter of credit, and sometimes no goods are imported at all. In 2017, the CBL opened LYD11.2 billion ($8 billion) in documentary letters of credit for imports. The extent to which these funds were diverted remains unclear. The Libyan Audit Bureau claimed to have identified more than $570 million in fraudulent letters of credit in the 11 months from January to November 2016, based on the records it had reviewed, but it has since been denied access to the CBL database which keeps track of letters of credit.58

Most armed groups remain on the state payroll, giving the Libyan government the peculiar distinction of funding its own civil war

Libya’s generous fuel subsidy regime has been widely abused by corrupt actors and smugglers. Smuggling of refined fuel (not to be conflated with the smuggling of crude oil) has become lucrative in the country’s conflict economy. Around one-third of refined oil products are diverted from the formal fuel distribution network, according to the Libyan Audit Bureau.59 In January 2017, the head of the investigations office of the Libyan attorney general told a press conference that fuel smuggling had cost the state LYD5 billion ($3.3 billion) over an unspecified period.60 In the past, state subsidies for basic commodities such as wheat and flour had also contributed to cross-border trade in the Maghreb and Sahel, laying the foundation for informal economic activity and the development of illicit trafficking pathways.

Human smuggling and trafficking, which generate the most attention outside Libya, are a key part of the country’s illicit marketplace. On the northwest coast, armed groups have become directly involved in such activities as a result of their physical control of launching points and detention centres. In other areas of the country, it is very difficult for human smugglers to operate without paying armed groups for protection or submitting to demands for taxes on the movement of people. Taxing people flows is also a particularly significant form of income for the armed groups in Libya’s south. At their peak in 2016, revenues from human smuggling were in the region of $1 billion, according to Chatham House estimates.61 Since mid-2017, however, Mediterranean crossings have fallen significantly, and revenues for human smugglers are likely to have fallen correspondingly.62

Prior to the conflict, Syria’s economy was among the most diversified in the Middle East. It relied on a mix of sectors including energy, agriculture, trade, transport and manufacturing.63 Years of intense conflict have transformed this picture, however. Government services and agriculture now contribute together up to 47 per cent of GDP, compared to 30 percent in 2010. Oil exports, which once represented a meaningful share of both government revenues (a third of the 2010 budget) and foreign currency receipts (around 25 per cent), now contribute much less to the economy than they used to. In 2017, approximately 64 per cent of Syrians in employment worked in the public sector, compared to around 25 per cent in 2010.64

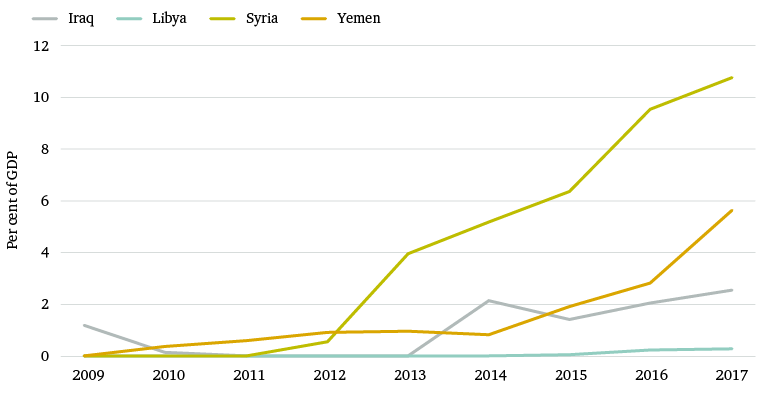

The conflict has drastically reduced export receipts, which fell from $13 billion in 2010 to less than $900 million in 2017. This has created a foreign currency crisis, with significant economic, political and social consequences. Despite the dire economic circumstances, the regime has managed to continue providing employment, as well as basic government services, to residents within its areas of control.

In 2016, the UN Economic and Social Commission for Western Asia (ESCWA) estimated Syria’s GDP at $25 billion, less than half its level ($60 billion) in 2010. GDP has fallen each year since 2011, with ESCWA putting total economic losses by the end of 2016 at an estimated $328 billion, split between approximately $100 billion in lost capital stock and $228 billion in accumulated GDP losses. While these macroeconomic figures tell us little about the violence on the ground, they provide a snapshot of how profoundly Syria has been affected.

The Syrian government budget has shrunk significantly in the past seven years, from around $18 billion in 2011 to $9 billion in 2018. Actual government expenditures have been even lower, since only half of the budget is estimated to have been spent in recent years.

To cope with funding shortfalls, the regime has provided loyalist figures with privileged access to government contracts, land, and import and export functions in return for financial and military support. In doing so, the regime has empowered individuals (including some based in neighbouring Lebanon) to bypass Western sanctions. In order to access resources from areas of the country no longer under its control, the regime has recruited new brokers to manage its relationships with ISIS and other groups, and to ensure a steady supply of energy and food products from the northeast (where these resources are located). It has also given a free hand to its militias to loot areas captured from the opposition.65

The regime has benefited from uninterrupted support from Iran and Russia, its key foreign allies. Iran, for example, has provided $3.6 billion worth of oil supplies and $2 billion66 worth of other products (although the US imposition of sanctions in November 2018 on the shipping of oil to Syria reduced these supplies). The Syrian regime has further taken advantage of humanitarian aid to compensate for shortfalls in funding and supplies, and to finance state-owned businesses. Humanitarian aid flowing into Syria was estimated at $2.2 billion in 2018.67

The civil war has destroyed existing business and trade networks, while encouraging a major expansion of illegal and informal activities and networks. New activities such as kidnapping for ransom have become important sources of revenues for criminal actors. Unsurprisingly, war has diverted financial resources away from the formal economy into the informal one. This has included, for instance, the increased use of informal financial networks such as the hawala system, which residents of rebel-held areas have relied on following the withdrawal of the formal banking sector from those areas. The division of the country into different areas of control continues to provide opportunities for smuggling, as well as for arbitrage between the various fragmented markets. However, activities such as looting, kidnapping and trading in antiquities have become less prevalent in the past year as the intensity of the conflict has decreased. The reduction in the number of checkpoints, and in the number of men joining militias, has had a similar impact, particularly in regime-controlled areas.68

Yemen’s pre-conflict economy was dependent on sales of oil and gas, which accounted for almost 70 per cent of state revenues in 2014. The country’s GDP is estimated to have halved since then.69 Accurate data on the current composition of the economy are hard to come by, but publicly available estimates suggest that in 2017 agriculture accounted for 24 per cent of economic activity, industry 14 per cent and services 62 per cent. More than 80 per cent of people are believed to live in poverty.70

New hybrid systems and networks involving state institutions, the private sector and illicit trade actors increasingly underpin the Yemeni economy. These structures simultaneously ensure a continued supply of basic goods while exacerbating trade constraints caused by the conflict. Yet despite the often violent competition between actors, a bustling conflict economy has emerged since 2014, with ostensible rivals cooperating with one another to facilitate both licit and illicit trade. There is strong evidence that a robust arms trade still operates between different cantons of control, with weapons provided by the Saudi-led coalition available for sale in arms markets in Houthi-controlled territory. Qat, the semi-narcotic leaf that is chewed socially, is traded freely across internal borders, while milk and juices from Saudi Arabia are widely available in supermarkets in Sanaa. Simultaneously, the Houthis and the government of Yemen have engaged in a battle for control of the institutions that manage Yemen’s economy, most importantly the Central Bank of Yemen (CBY).

The Houthis’ takeover of Sanaa in September 2014 allowed them to achieve control of key state institutions – notably, those with revenue streams that could be used to support the war effort. Latterly, the Houthis have sought control of the main levers of the economy, including the import and distribution of basic goods, particularly fuel, via merchants with privileged access to the Houthi leadership. The Houthis have exploited the war and their position of dominance – achieved through violence and other repressive measures – to integrate the state, the formal economy and the informal economy into a system that allows them to sustain the conflict, while simultaneously enriching their own leadership. They have taken an increasingly predatory approach to the private sector, seizing assets and forcing businesses to pay prohibitive taxes to the de facto authorities in Sanaa. No business – from high-revenue sectors such as telecommunications and pharmaceuticals to local market stands selling fruit, vegetables and qat – has been immune. In order to operate, businessmen inside and outside Yemen have learned that they need to develop commercial relationships with the political or military leadership.71

The Houthis have taken an increasingly predatory approach to the private sector, seizing assets and forcing businesses to pay prohibitive taxes to the de facto authorities in Sanaa

The ports of Aden and Mukalla are conduits for various kinds of trade: particularly for shipping traffic between the Horn of Africa, the east of the Arabian peninsula and Asia; and, more recently, for containers entering Yemen. The south is also an important transit point for smuggled goods. Before the war, a variety of goods from drugs to arms to all-terrain vehicles entered the al-Mahra governorate by sea and overland (in the latter case via Oman, often after being trafficked from the UAE). Smugglers in al-Mahra also played an important role in the informal money-changing sector, transporting large volumes of physical currency from the UAE into northern Yemen.72 Smuggling networks in Shabwa and Hadramawt acted as a bridge between arms, drugs and human smugglers in the Horn, particularly Somalia and Djibouti.73

Another source of revenue is the seizure of arms, fuel and other materiel provided by Saudi Arabia. The arms market has been highly liquid since the war began, with weapons that can only have been provided by the Saudis (Austrian Steyr rifles, for example) available for sale in Sanaa. Local merchants have entered into lucrative contracts with the military for the provision of fuel, food and transportation. Media reports suggest that these merchants, as well as local military commanders, are inflating the value of such contracts for personal gain; and that food and fuel are being sold into the local market at marked-up prices, often to the benefit of the Houthis. It is widely accepted that the individuals involved in these practices understand they are effectively undermining the overall war effort. As in the Houthi-held north, fuel imports are seen as a major revenue generator.