Attention is once again focused on Libya as the political process being convened by the United Nations (UN) has agreed the appointment of a new interim government to see Libya through to elections at the end of 2021. But, while the ongoing failure of governance in Libya continues to make international headlines, the impact it leaves on the management of Libyan state assets overseas receives minimal coverage – even though this impact is highly significant for the people of Libya.

Libya: Investing in the wealth of a nation

The extraordinary story of Libya’s overseas investments and seemingly endless battles over their control.

Feature

Published 24 February 2021

Updated 21 April 2023 — 19 minute READ

Contents

Since 2006, the country’s investments in global markets have been made principally through a sovereign wealth fund – the Libyan Investment Authority (LIA). And yet, after all this time, it remains unclear precisely what the total value of the LIA’s assets are, even to its current leadership. The commonly-cited estimate of the LIA’s value is $67 billion1.

Problems of structure and governance have persisted as the LIA struggles to escape the legacy of the Muammar Gaddafi regime. The LIA was formed not just as a means of allocating the windfall from the sale of oil and gas for the benefit of future generations, but also as a tool for distributing patronage and leveraging political influence.

Since the 2011 revolution, the LIA has been a battleground. Interests entrenched from the Gaddafi era have sought to preserve their stake while new actors work to wrestle control of parts of the organization.

Early investments and the debate over the 'mujanib'

In 1977, the Italian car giant Fiat was struggling2. On the hunt for investment it obtained $400m from Libya, the country’s first such major investment. The resulting shares in Fiat were held by the Libyan Arab Foreign Investment Company (LAFICO). But as Fiat’s fortunes improved in the 1980s, it reportedly feared that the Libyan investment could be an impediment to entering the US market because of allegations at the time of Libyan support for international terrorism3.

And these Libyan battles have been exported to courtrooms around the world – from London to the Cayman Islands – while the UN asset freeze on the LIA does not in reality cover all of its structure, meaning some elements remain up for grabs.

Examining these dynamics, and the story of how the LIA came to prominence, provides extraordinary insight into what has happened to the wealth of the Libyan population, as well as highlighting what external states – in whose markets the LIA still engages – should be doing about it.

Libya sold its shares in 1986 for $3 billion, a huge profit, which was placed in a new investment vehicle, the Long-Term Portfolio (LTP)4. But sinking global oil prices and the sanctions on Libya following the 1988 Lockerbie incident made similar international forays difficult.

Although the OilInvest Group emerged in 1988 after the Libyan state purchased Tamoil – a fuel refining and distribution company – the imposition of sanctions in 1992 saw Tamoil’s corporate structure amended to place the majority of its shareholding into non-Libyan ownership, seemingly to insulate the company from the impact of the sanctions5.

More was possible in African markets, to which Gaddafi pivoted to further his political influence, and a stream of investments overseen by Bashir Saleh – known as ‘Gaddafi’s banker’ – were made before being formalized as the Libya Africa Investment Portfolio (LAIP) in 2006. By now a significant surplus was being generated, but Libya’s budget remained under strict control as oil prices were high and running costs low – so the ‘mujanib’, essentially meaning ‘leftovers’, needed investing somewhere6.

At the time, the Libyan market had limited absorptive capacity and the rather frugal leadership of Libya’s existing sovereign institutions were cautious7.

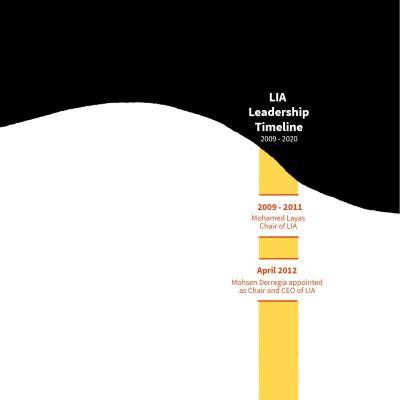

But a younger group of leaders, including individuals such as former Libyan prime minister Shukri Ghanem, argued for the establishment of a sovereign wealth fund. In 2006, a resolution within Libya’s then legislature, the General Peoples Committee (GPC), created the Libyan Investment Authority (LIA) as an investment department for regular and alternative investments, with around $8 billion of funds.

Coming in from the cold

The LIA’s emergence came just as Libya was being rehabilitated by the international community, and the financial world’s elite jetted into Tripoli to court Libyan investment. But a political power struggle was also now underway within Libya over which of Gaddafi’s sons would succeed their father, and institutional islands of influence were emerging along with different visions for how Libya should be governed.

The LIA fell under the influence of Gaddafi’s eldest son Seif al-Islam and the fiscally-liberal crowd surrounding him – such as Mohamed Layas who became the first CEO of the LIA and his deputy Mustafa Zarti. The pair built up the LIA investment portfolio, but generated losses from 2007-2009 which cast a shadow over the organization still apparent today. Insiders have suggested Seif was the real power within the organization.

The scale of these losses became clear in a 2010 KPMG audit of LIA assets8. The report, leaked and released publicly in 2011, made for grim reading as it identified five funds which made a loss of 23 per cent on a $1.4 billion investment, despite the market overall increasing 25 per cent in the previous year. Interestingly, it also valued the LIA’s overall assets in September 2010 at $64.2 billion9.

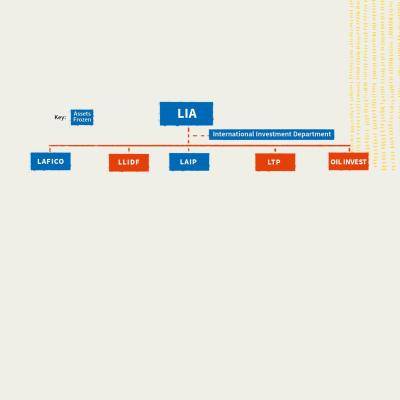

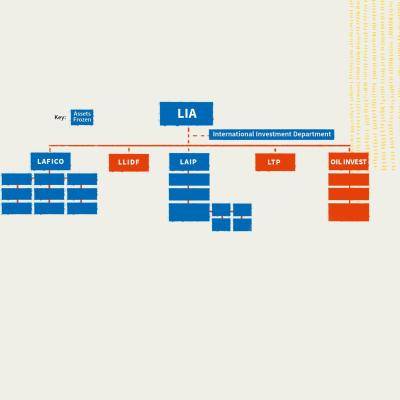

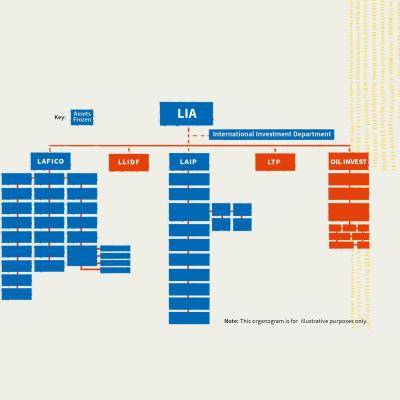

The audit was timely as lawmakers had recently decided to consolidate all of Libya’s major overseas investment vehicles under an expanded LIA. Law 13 (2010) brought LAFICO, the LTP10, OilInvest, LAIP and the Libyan Local Investment Development Fund under the aegis of the LIA11. In the words of Ahmed Jehani, a former Libyan minister who has worked with the LIA in various guises, the law had created a ‘humpy dumpty’ of five subsidiaries and around 550 companies12.

Revolution, upheaval and division

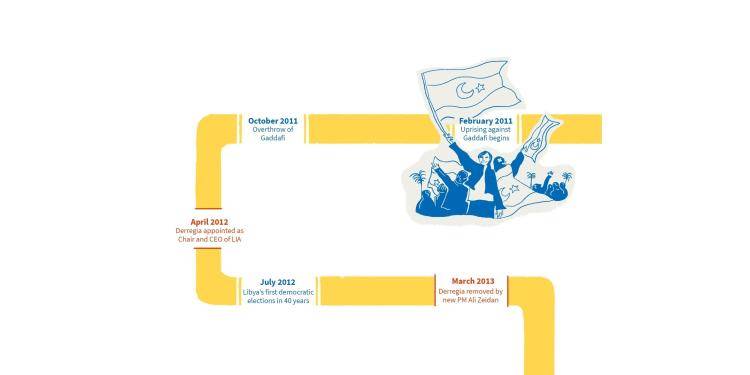

With the end of the Gaddafi regime in 2011, the LIA along with many other Libyan state institutions became embroiled in a post-revolutionary struggle for control, hindering necessary reform. Although Layas was retained as chair by the interim governing authorities, Zarti distanced himself from the organization and was replaced by Rafiq Nayed as acting CEO.

The first post-revolution prime minister, Abdelrahman al-Keib, appointed Mohsen Derregia as chair and CEO in April 2012 to replace Zarti and Nayed. He inherited an LIA that, despite the passing of Law 13, had not truly united. He complained there were no audited accounts since 2008 and that he received no official handover13.

Derregia decided to hire PwC to help fill in gaps in the accounts from 2009-2011, Deloitte to conduct an audit to value the assets of the LIA and its subsidiaries on the books, and Oliver Wyman to develop its investment strategy and reform governance. He also noted the value of the assets owned by the LIA had been treated as fixed at the historic price and not independently valued14. The systems established in the Gaddafi era meant nobody was prepared to report losses even if they came due to a global financial crash.

But Derregia insists he felt there was resistance to change and transparency from the outset, saying: ‘When I arrived, I found out that all of the departmental managers [for the LIA] had been given a one-month holiday.’15

Derregia says he tried to replace several LIA directors because, he felt they were subject to potential conflicts of interest as they worked, or had worked, with firms that received investments from the LIA. But support from the prime minister – who was the chair of the LIA board of trustees by virtue of his government position – was not forthcoming16. This brought Derregia into conflict with the new board of directors over allegations that appointments were being made without appropriate due process17.

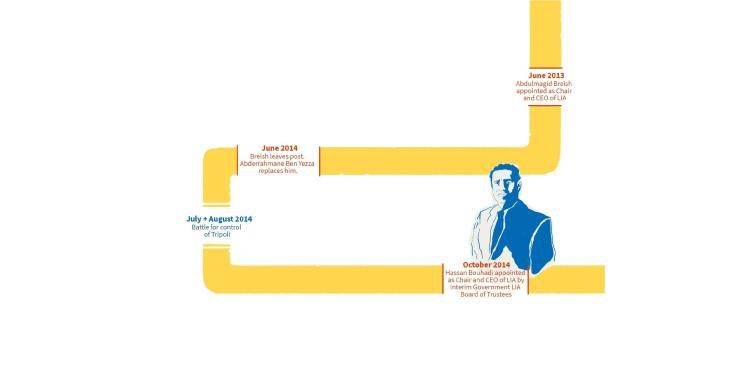

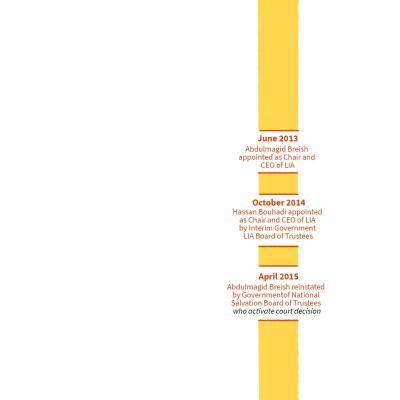

As relations with the board of directors worsened, Derregia was removed by newly appointed prime minister Ali Zidan in March 2013 after less than one year in post18. He was replaced by Abdulmagid Breish in June 2013. Breish again brought in the major international firms – Deloitte to value assets and undertake forensic accounting, and Oliver Wyman to use the information collected by Deloitte to benchmark the LIA against leading sovereign wealth funds, and to develop a strategic roadmap19.

Breish also wanted to investigate what happened in relation to some of the major investments in the LIA’s early years – identified as what he termed ‘$5-6 billion of highly suspicious’ assets20 – but his time as chair and CEO was curtailed by the new highly controversial Political Isolation Law which barred those who held leadership posts in state institutions under Gaddafi from holding them again. Breish was removed from his position in June 2014, timing that he noted coincided with his investigation into the assets21. He was succeeded by Abderahmane Ben Yezza as LIA Chair and CEO. The nature of Ben Yezza’s appointment – whether it was temporary, while Breish fought his case in court, or permanent – is contested. This would have a bearing on the future dispute over leadership of the organization22.

Meanwhile, following the disputed June 2014 parliamentary election results, Libya had once again descended into civil war. The House of Representatives – the newly-elected, albeit contested, parliament – relocated to the east of the country citing security concerns and would appoint a new ‘Interim Government’ based in the eastern city of al-Bayda. But many members of the House of Representatives did not relocate. A reconstituted rump of the General National Congress (GNC) subsequently appointed its own ‘Government of National Salvation’ in Tripoli.

The existence of two governments led to administrative chaos. The absence of both a unified and universally recognised executive and legislative led to the emergence of parallel leaderships of state institutions and undermined any checks and balances that did exist in Libya’s governance. The LIA was no exception.

In October 2014, the eastern-based Interim Government – then the only government in Libya – appointed LIA board member Hassan Bouhadi as the new chair and CEO of the LIA. Bouhadi, citing the same security concerns, set up the LIA office in Malta following the conduct of a memorandum of understanding with the Maltese government23.

Then in April 2015, the LIA board of trustees – made up of the executive members of the Tripoli-based Government of National Salvation – actioned a decision by the Libyan court to overturn the ruling of the Political Isolation Committee against Breish and reinstate him as chair and CEO of the LIA. This led to an ongoing dispute as to whether Breish could return to his position or whether Bouhadi had already succeeded Ben Yezza, meaning that there was no position to which Breish could return24. Practically, this meant the Tripoli headquarters of the LIA was controlled by Breish and the Malta office was controlled by Bouhadi – the LIA was split, albeit with all board members but Ben Yezza reporting to Bouhadi.

Legal disputes enter the world's courtrooms

Throughout all this, the LIA had been trying to bring legal proceedings in the UK courts against various international banks and asset management companies relating to the massive financial losses sustained by the LIA in the 2006-2010 period. But the split complicated these attempts – how could solicitors in the UK court say they acted for the legitimate chair of the LIA when this position was contested25?

Proceedings had begun in 2014 under Breish, who established a litigation committee directed by Ahmed Jehani to appoint solicitors and supervise the effort. In November that year, Jehani secured agreement from all LIA directors to put the leadership dispute aside while legal proceedings played out26. But differences then emerged over which further cases the LIA should seek to take to court and who should be overseeing the litigation committee27.

As a result, Bouhadi initiated separate legal proceedings in the UK courts in 2015 to establish who should be the legitimate legal authority for the LIA, which led to a court-appointed receiver instructing legal action on behalf of the LIA. But these proceedings to determine whom should be recognised as the legal representative of the LIA in the UK were just the start of a long, drawn-out legal battle in the UK courts – which expanded to include other parties as rival governing authorities in Libya tried to make their own appointments to the LIA.

BDO Global became the court-appointed receiver and instructed law firms to take on two major pieces of litigation in 2015 on the LIA’s behalf, against Goldman Sachs and Société Générale (SocGen) who had both being vying for the LIA’s business in its early days. These cases revealed the extent of the failure of the investments made under Layas’ and Zarti’s watch.

Under the guidance of Goldman Sachs, the LIA made a $1.2bn investment in derivatives trades in 2007-8. The entirety of this investment was lost. Ali Baruni, advising the LIA on its investments at the time, claimed that LIA officials working with Goldman Sachs only had a ‘limited understanding’ of the products being suggested to them, and that this was demonstrated by disclosures made to the UK court28. One email from a Goldman banker said that pitching to the LIA was akin to pitching ‘to someone who lives in the middle of the desert with his camels’29.

Video explainer

— Explaining how the Libyan Investment Authority (LIA) was formed, rivalries and court cases that emerged from its work, and ongoing governance challenges.

Legal disputes contd.

Through its disclosures to the court, the LIA alleged Goldman Sachs exerted ‘undue influence’ on the LIA, in part by offering lavish corporate hospitality to LIA staff30. Disclosures to the court show Goldman Sachs had underwritten all-expenses-paid trips to luxury resorts where prostitutes were said to have been present31. The disclosures suggested that Goldman Sachs had provided employment to Zarti’s brother, for which he was unqualified and was in seeming contravention of Goldman Sachs’ own hiring practices32.

Goldman Sachs’ legal team denied any wrongdoing. The LIA lost its case, with the court finding that the hospitality provided was not as ‘unusual or remarkable’ as had been presented33. The court concluded that undue influence had not taken place and that Goldman Sachs had not made excessive profits on the trades34.

The second major case, involving SocGen, was a dispute over $2.1 billion in trades made between 2007-935. The LIA alleged in court that SocGen had paid $58.5 million to a Panama-based company owned by a Libyan businessman to secure the trades. This was denied by SocGen. The parties reached a confidential settlement36 which included37 an apology from SocGen and the funds were collected by BDO, the receiver38.

Legal action in London was also brought by LIA subsidiary FM Capital Partners against its former CEO Frederic Marino. FM Capital Partners had been formed in London in 2009 by Marino in partnership with the LAIP, the majority shareholder39. But in 2014, FM’s CEO Sufian Creui launched an investigation into the conduct of Marino after identifying what he perceived as the payment of abnormal fees and matters of concern in trades with, and the setup of, new investment vehicles in tax havens40.

Creui stated he felt the company was a ‘compensation scheme under the guise of a business’ on his arrival with a ‘bloated staff and a lack of IT infrastructure’41. Following his investigation, FM Capital entered into legal proceedings against Marino and won the case in 2018 when the UK courts found Marino to be ‘liable in breach of fiduciary duty, dishonest assistance, and bribery’42. Marino’s appeal of the judgment was dismissed by the UK Court of Appeal43.

The asset freeze and the rest of the iceberg

Back in 2011, following protests in Libya, the international community was quick to freeze assets it deemed could be used to fund the Gaddafi regime’s military campaign. UN Security Council Resolution 197044, passed on 28 February 2011, announced an asset freeze on specific members of the Gaddafi family. This was then expanded in March to include designated assets and resources controlled by the Libyan authorities in Resolution 197345. These assets and resources were the LIA, LAIP, and LAFICO, along with those of the Central Bank of Libya and the Libyan Foreign Bank. The freeze on the latter two was quickly lifted but the freeze on the LIA, LAIP, and LAFICO remains in place. In September 2011, Resolution 200946 eased the terms of the asset freeze so that only assets outside of Libya as on 16 September 2011 remain frozen.

The asset freeze has been an effective means of safeguarding the wealth of the Libyan people but it is not well understood in policy circles, with some assuming it amounts to a blanket freeze. Two main issues have arisen – first, the freeze targets some LIA assets but not others and with no clear reasoning, meaning many of the LIA’s subsidiaries, and the subsidiaries of those subsidiaries did not have their accounts frozen. Second, application of the freeze was uneven – and at times non-existent – in some jurisdictions which meant significant transfers of interest and dividends continued to be made.

Issue one: Subsidiaries

Subsidiaries illustrate the oddities of the terms of the freeze. For example, the LAIP is listed on the freeze but its subsidiaries, OilLibya (now known as Ola Energy), the Libyan Arab African Investment Company, and LAP Mauritius are not47. This matters because the UN Panel of Experts, citing LIA internal sources, reported in 2013 that the ‘opaque nature of the ownership structure of the subsidiary hierarchy [of the LIA] was also a deliberate move by the former regime to facilitate the laundering of funds embezzled from the State to personal assets abroad’48.

While overall valuations of the LIA’s assets are hard to reach, a large proportion of them are held within subsidiaries, some as tangible assets such as buildings but others as liquid assets – which make them a focal point for competition for control and a potential source of funding. The plight of LAP Green Networks, a subsidiary of LAP Mauritius, illustrates how management failures at within subsidiaries continued after 2011 despite the asset freeze.

By 2012, LAP Green Networks had invested more than $1bn in telecoms in six African states but was performing poorly. In October 2015, Hassan Bouhadi announced the ‘strategic consolidation’ of LAP Green Networks’ own subsidiaries within the Libyan Post, Telecommunications and Information Technology Company (LPTIC), thereby transferring the assets out of the LIA49. He justified the move on the basis it would consolidate telecommunications holdings under one specialized management team50.

Bouhadi says he believes LAP Green Networks would have gone into administration had LPTIC not taken over its assets51. But the move does raise questions: why should Libya’s state-owned telecommunications company be directly running telecommunications agencies in other states? Questions over due process also arise. LPTIC says that the consolidation of LAP Green Networks into LPTIC was authorised by eastern authorities52. Yet a search on the corporate register in Mauritius in November 2020 indicated LAIP remains the owner of LAP Mauritius (which had been the holding company for LAP Green Networks).

A search on the Dubai commercial registry indicated LAP Green Networks Dubai changed its name to LPTIC International Ltd, but not until January 2017 – some time after the supposed transfer of LAP Green Networks from LAIP to LPTIC.

LAP Green Networks is currently embroiled in a legal battle over its holdings. In 2012, Zambia nationalized Zamtel, 75 per cent owned by LAP Green Networks, allegedly without compensation, and the LIA claimed Zambia had sought to exploit instability in Libya to obtain the company53. A UK court did order Zambia to repay $380 million in 2017, but – as of 2018 – LAP Green Networks said Zambia had yet to do so54. Receipt of these funds would be a significant influx of cash for, presumably, LPTIC.

Issue two: Interpretations of the terms of the asset freeze

The LAP Green Networks example illustrates how the LIA’s large unfrozen subsidiaries continue to function with limited clarity over their operating procedures and almost no public disclosures.

Differing interpretations of the asset freeze’s terms when processing payments for supposedly frozen LIA accounts came to the fore during the ongoing investigation into transactions involving the Belgian bank Euroclear. LIA and LAFICO accounts in Euroclear were frozen in 2011 but the bank separated interest and other proceeds such as coupons and dividends from that point onwards, and these were made available to the LIA55.

Documents provided by Euroclear to a Belgian parliamentary inquiry into the issue reportedly disclosed that €2.067 billion were transferred from Euroclear to LIA and LAFICO accounts in Luxembourg and Bahrain between 2011 and 201756, leading to important unanswered questions over what has happened to the funds. The UN Sanctions Committee believes such payments should have been subject to the freeze as per the provisions of UN Security Council Resolutions 1970, 1973, and 200957.

But the Euroclear case also raises serious wider questions for the international community over how major financial institutions operating in European jurisdictions could adopt divergent interpretations of the asset freeze for seven years resulting in significant flows of cash. It is also notable that the change in policy from Euroclear did not come from any internal review process or regulatory decision but was a result of the process unleashed by evidence uncovered as part of the attempts by Prince Laurent of Belgium to recover funds he claimed were owed to him by Libya58.

Back to the Future

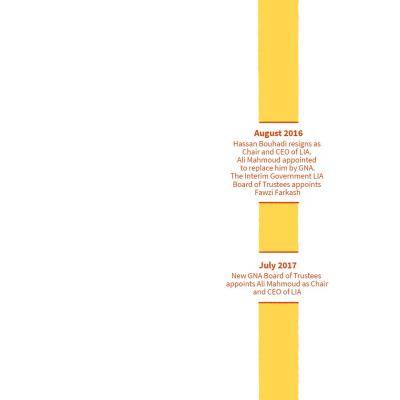

The creation of the Government of National Accord (GNA) following UN-mediated peace efforts in December 2015 was intended to reunify Libya’s governing institutions, but it has failed. Bouhadi says he met with the GNA’s prime minister Fayez al-Serraj and invited him to appoint a new LIA chair and CEO, but no decision came. Bouhadi came under pressure from the eastern-based authorities who do not accept the legitimacy of the GNA and decided to resign in August 201659.

Serraj moved to appoint Ali Mahmoud as the new LIA chair and CEO while the eastern-based authorities appointed their own replacement. This left the LIA with three rival claimants to its throne – one associated with the eastern authorities, Breish who was appointed by the former Zidan government, and Ali Mahmoud, appointed by the GNA. Due process seemed to have collapsed and a flurry of litigation was unleashed once again60, this time taking until July 2017 for the GNA to complete Mahmoud’s appointment.

There was also a struggle on the ground for control of the LIA headquarters in Tripoli with both Mahmoud and Breish seeking to remain in the offices. They even took turns ousting each other with Mahmoud asking security guards to escort Breish from the building in September 2016 only for Breish to return to the offices in February 2017 armed with a court order in favour of his return. Mahmoud eventually obtained control of the offices in May that year.

The legal muddle meant the armed groups in control of the LIA headquarters could in effect decide which leadership team would enter61. Armed groups had long been able to pressure those within the LIA – Breish recalls up to 40 ‘militiamen’ entering his office in 2014 to demand employment, noting he was then briefly detained by them when he refused to accede to their demands62.

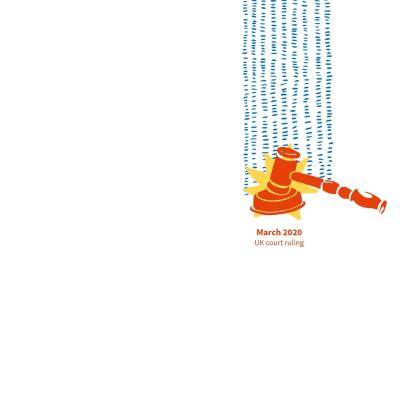

Such developments provided context for the ongoing London-based proceedings over the contested leadership of the LIA – a somewhat bizarre spectacle whereby a UK judge sitting in a UK court was being asked to rule on the procedural validity of LIA appointments as laid out in Libyan law. The judge eventually ruled in March 2020 that the GNA resolution appointing Mahmoud was ‘incapable of being successfully challenged before the Libyan courts’63.

Neither Mahmoud or Breish were in the courtroom when this verdict was delivered. Both were in fact in detention in Tripoli – apparently after yet another set of legal proceedings emanating from another of the LIA’s early investment decisions involving Palladyne International Asset Management (PIAM).

PIAM was appointed as an investment manager for $700 million of LIA, LAIP and Libyan Foreign Bank funds in 200764. Its CEO Ismail Abudher is the son-in-law of the late former Libyan prime minister Shukri Ghanem and, in 2013, the LIA became aware of investigations into concerns over allegations of possible financial impropriety by Abudher in the Netherlands, leading the LIA to refer the issue to its lawyers65.

Abudher denied the allegations but in May 2014 the LIA board of directors removed PIAM due to concerns over the management of the funds. The LIA claimed the funds were under complete control of PIAM without representation of the original investors, questioned the fees charged by PIAM as excessive and identified payments to intermediaries to be reviewed66.

PIAM challenged the decision to remove it in the courts in the Cayman Islands on the basis that it violated the asset freeze, and also brought proceedings against Ahmed Jehani and Ali Baruni, whom the LIA had appointed as replacement directors of the funds in 2014. In January 2019, the judge ruled in the LIA’s favour, noting that ‘concerns regarding the risks faced by the Libyan Investors in leaving the Plaintiff [PIAM] in control of the substantial investments held for the Libyan state were real and genuine… There were clearly a number of grounds for concern which included fees, performance and the absence or slow delivery of information’67.

PIAM lost on all counts in the court of first instance and in the Cayman Islands Court of Appeals. PIAM then appealed to the Privy Council which has reportedly refused to hear the application.

The case had ripple effects in Tripoli and laid bare the administrative chaos. Following the release of the draft judgement in the Cayman Islands, the LIA removed the directors it appointed in 2014 and reappointed PIAM68.

Mahmoud was subsequently arrested on 6 February 2019 on an arrest warrant issued by the Libyan prosecutor general69. He would remain in detention until April when he was released and returned to his post. Breish was arrested soon after seemingly on charges relating to allegations of inappropriately using Libyan public money. He was also released in April and says all charges against him have been dismissed70.

In Tripoli, the remaining members of the LIA board of directors subsequently denied knowledge of the decision to reappoint PIAM and voided the decision under the authority of its acting chair, only for the board of trustees to then rule the voiding invalid. Four new directors were then appointed to manage the investments instead of PIAM71.

The LIA has explained its decision to re-appoint PIAM as an interim solution because the LIA-appointed directors ‘refused to recognize the authority of the GNA-appointed board of directors and could legally act without any board oversight’72. Yet it is difficult to understand why PIAM would be re-appointed and not another entity given the legal proceedings and the concerns arising from the allegations levelled at PIAM. Mahmoud said he is unable to comment on the Palladyne case as it remains ongoing in the courts73.

Safeguarding a nation’s wealth

‘I took control under chaos’ said Ali Mahmoud when interviewed in January 2021. ‘I inherited a divided management and the LIA had lost control over many of its subsidiaries. There was a lack of information, no audit process and no risk management’74.

Mahmoud said his plans for the near future include a programme of internal governance reform in coordination with Oliver Wyman, the conduct of valuation of LIA assets worldwide conducted by Deloitte, and an audit of LIA accounts conducted by EY. He also says a ‘mega-project’ will soon be initiated to consolidate financial statements for LIA funds and investment portfolios75.

But despite clear goals, Mahmoud’s comments illustrate that almost ten years on from the ousting of Gaddafi, the LIA is still yet to adequately identify its assets and rationalize its management. The organization has now stated that, following the UK court decision in favour of Mahmoud, it can collect the requisite financial information from its subsidiaries and meet its financial reporting requirements.

But those with a close working knowledge of the LIA are sceptical whether this will happen to the desired standard76.

He argues this will undermine any auditing process as it is not the responsibility of the auditors to prepare accounts, and emphasizes the importance of establishing consolidated accounts which encompass all the LIA’s approximately 550 subsidiaries.

It also means any valuation of the assets made prior to that point could be fundamentally undermined. Abdulmagid Breish says it is relatively easy for the LIA to meet the standards in its own accounting but that the accounts of the subsidiaries need to move several levels up the scale in terms of accountancy practices for the LIA’s accounts to be properly consolidated77.

How much is the LIA worth?

Safeguarding wealth contd.

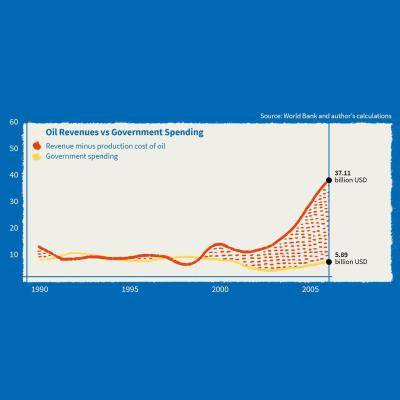

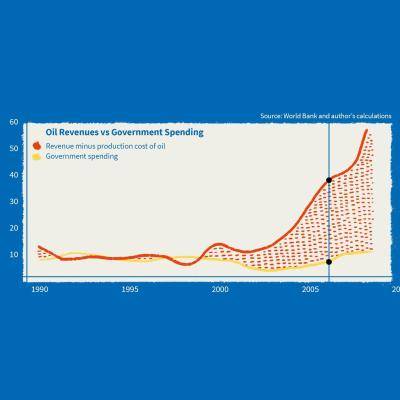

The next objective for the LIA is to seek amendments to the terms of the asset freeze. A report it commissioned announced in December 2020 that the LIA’s equity investments have underperformed market averages to the tune of $4.1bn since 201181. The LIA complains significant funds are being held in negative equity while investments in bonds that have matured are converted into cash without being reinvested82.

The LIA says it is seeking ‘feasible ways to more actively manage’ its portfolio83. Although not seeking the removal of the asset freeze, it has prepared a set of proposals to amend the freeze through the creation of a ‘special purpose facility’ under the management of a custodian institution – likely still to be subject to the oversight of the sanctions committee in some fashion. This, argues Mahmoud, would ensure the asset freeze serves its function of protecting, rather than punishing, the LIA and its assets84.

But several former senior employees of the LIA have rejected any amendment of the asset freeze, with most suggesting it be strengthened instead. Such a view emphasises the need for the LIA governance to first be improved before the terms of the freeze be considered for change.

In lieu of a change to the asset freeze’s terms, there also remains the potential for the LIA and its subsidiaries to obtain licenses to operate in international jurisdictions. Ali Baruni rejects the argument that licences to operate existing holdings are too difficult to obtain85 – and in fact, a number of LIA subsidiaries have obtained licences to navigate the freeze such as FM Capital Partners in London86.

Next comes the question of how the LIA should position itself for the future. Here, a root and branch reform of the LIA to steer it away from directly managing assets would be in keeping with the operations of other major sovereign wealth funds. Mohsen Derregia highlights the example of LAP Green Networks, where the LIA tried to run a complex telecommunications business in African countries when it could have subcontracted the task to an operator experienced in the sector. Similar examples include managing hotels in Tunisia and office buildings in London.

Among former employees of the LIA, there is a strong sense that the LIA should be an owner not a manager. Rather than being encumbered with the administrative challenges of operating 550 subsidiaries, it would be better served by placing its investments strategically with external fund managers, who can be held to clear performance targets and fired if they perform poorly. The LIA has proven it can do this – the Corinthia hotel chain is part-owned by the LIA but operated by a third-party87.

Removing direct management of the subsidiaries would also reduce potential opportunities for corruption via dispensation of paid positions and contracts. There are various stories of LIA subsidiaries creating their own subsidiaries and refinancing that have not been substantiated. Derregia likens such a process to a ‘Russian doll effect’ because it can help sustain patronage networks88. At times of political upheaval, the cash of the LIA and its subsidiaries can be an enticing potential target for political interests. The dysfunction in Libya and the ongoing competition is so severe that Breish believes the LIA should be ‘totally wound down, [its assets] placed in a fund and accessed in 25 years’89.

Regardless of the approach the LIA chooses for the management of its assets, a focus on returning to the strategic priorities outlined at its inception is certainly required – namely to invest the wealth of the Libyan people and to reduce its vulnerability to shifts in the global oil price and dependence on the oil sector. These remain priorities for the Libyan state.

The international community’s approach to freezing assets, developed in the early months of the 2011 uprising, has endured by default because the LIA has not been able to make the case for lifting the freeze. The international community has lessons to learn as illustrated by the inconsistencies in the application of the terms of the freeze and the lack of enforceability in some jurisdictions.

There is an opportunity for the UN Security Council to clarify its stance and remove inconsistencies that linger from previous resolutions over which entities should be affected and which should not. It should learn from the experience of the last decade to seek to close loopholes that have allowed funds to continue flowing to some parts of the LIA but not others, most notably its subsidiaries.

But amendments to the freeze should be contingent on the LIA first delivering on its stated aim of improving the governance and transparency of its holdings. If not, then states whose courtrooms have witnessed a raft of LIA-related litigation, should seek their own clarifications from the Sanctions Committee to reduce the potential for error and avoid any allegations of complicity being levelled at them.

Finally, the asset valuation currently being conducted for the LIA offers a valuable opportunity to bring some clarity and transparency to the fore. Presenting the findings of the assessment to the Libyan people to explain where their assets are being held and their value is a necessary first step in any reform process. The international community should encourage the public release of LIA financial information, especially with regard to subsidiaries operating within their jurisdictions.