Four years on from its Euromaidan revolution, Ukraine is fighting for survival as an independent and viable state.

Chatham House report

Published 18 October 2017

Updated 18 July 2023

ISBN: 978 1 78413 243 9

Four years on from its Euromaidan revolution, Ukraine is fighting for survival as an independent and viable state.

The problem in gauging Ukraine’s progress in economic reform is that its performance is all too frequently judged against unrealistic expectations – and by commentators who have an interest in promoting, or a bias towards, a particular narrative. At home, the euphoria generated by the success of the Euromaidan protests, and the fact that hundreds of thousands of people demonstrated – and many died – in support of political reform and closer economic relations with the EU, perhaps led many to hope for a rapid transformation in the economy following the ousting of President Viktor Yanukovych in February 2014.

Performance is all too frequently judged against unrealistic expectations

However, reform was always likely to proceed more slowly and be more difficult in practice. Limiting factors included 20-odd years of largely failed economic development since Ukraine’s independence, the legacy of Soviet rule and central planning, and the impact of Russia’s annexation of Crimea in 2014 and of the conflict in the east of the country.

In Western policy circles, years of Ukraine failing to modernize its economy had fuelled the lazy and sometimes self-interested narrative that the country was somehow beyond reform. For some Western countries, perhaps half-hearted in providing financial or political support, and even eager to push Ukraine back into the Russian orbit, this was a useful fiction. Further east, the regime of Vladimir Putin, Russia’s president, had a clear interest in the failure of a Western development model in Ukraine – Moscow was thus similarly interested in promoting the line that the Euromaidan reforms were doomed to failure.

As is very often the case, the reality has proven more complicated than either the overoptimistic or unduly pessimistic views of Ukraine’s prospects. Since the change of government in 2014, Ukraine has produced – against the odds – some remarkable achievements in terms of economic reform and stabilization. However, the job is incomplete, and more can and certainly needs to be done.

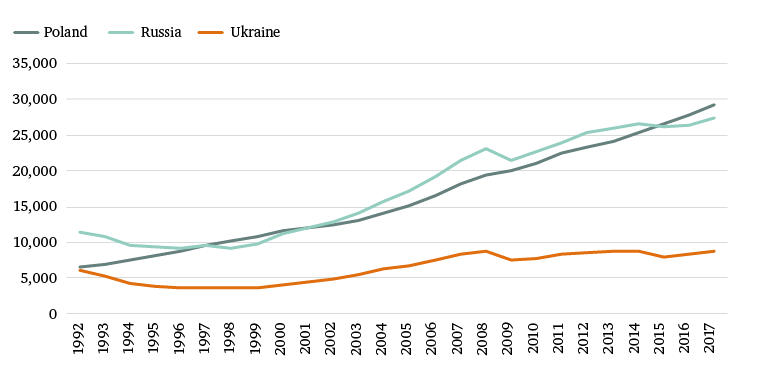

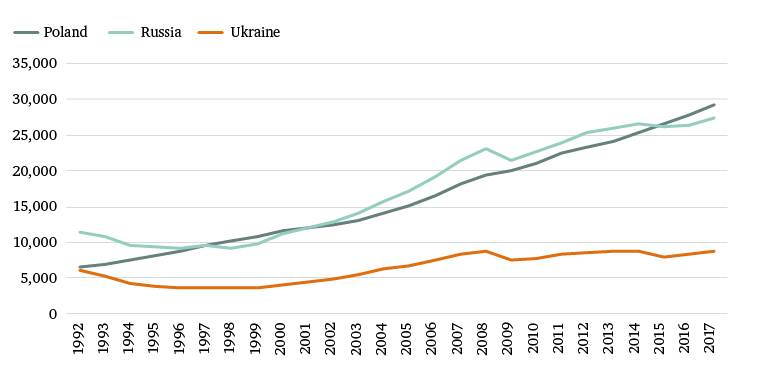

As a starting point, it is useful to put to rest a commonly held misconception that the Ukrainian economy was somehow doing well prior to the Euromaidan protests, and that it would have done much better to simply maintain its existing course of development as a so-called ‘bridge between East and West’. This fallacy can be challenged by comparing the respective changes in per capita GDP at purchasing-power parity (PPP) for Russia, Poland and Ukraine since the early 1990s, when their transitions from planned economies towards market-oriented models were just beginning. According to IMF data,84 in 1992 both Poland and Ukraine had per capita GDP of just over $6,000 in PPP terms, while the comparable figure for Russia was $11,500 or thereabouts.

Looking at their respective development models, Poland from 1989 chose Western liberal market democracy, formalized in the Treaty of Copenhagen in 1993 and anchored a decade later by EU accession. Russia, by contrast, chose a more statist orientation (a ‘power vertical’) that was assisted by the commodity super-cycle. Despite these different paths, incomes in both economies increased dramatically in the ensuing two decades: by 2013 Poland’s GDP per capita GDP had increased fourfold to $24,000 in PPP terms, while Russia’s had more than doubled to $26,000. In stark contrast, Ukraine achieved per capita GDP of only $8,676 at PPP in the same year (see Figure 1).85

Any casual observer of these statistics would quickly come to the conclusion that the Polish and Russian development models (for all their faults) were superior, and that the status quo in Ukraine was not working for the bulk of the population. By 2013, it was simply unsustainable. The Euromaidan movement was arguably a popular revolt against more than 20 years of failed economic development, and against long-running exploitation of the population by the country’s elites. Something snapped, or rather the prospect of Ukraine signing its Association Agreement and Deep and Comprehensive Free Trade Agreement with the EU inspired hope of a different, better and more inclusive model of development.

Dependency on cheap Russian oil and gas promoted rent-seeking and caused economic distortions

So to properly understand what has been achieved, or not, in terms of economic reform, perspective has to be given to the starting point in 2013, even before the Euromaidan. Ukraine’s level of development was far below that of its regional peers, and among the lowest in Europe. More importantly, the country followed a totally distorted economic model which was corrupt at its very heart, arguably institutionally so. This situation was arguably sustained by outside agents for whom Ukraine’s structural economic flaws were advantageous. Dependency on cheap oil and gas from Russia promoted rent-seeking, and caused economic distortions and inefficiencies that affected not only the energy sector, but also the financial system, the fiscal accounts and the balance of payments. These same distortions were exploited by Ukraine’s own elites.

And to further understand the challenges facing Ukraine, it is important to add the headwinds to the economy felt over the past three-and-a-half years since Yanukovych’s departure. A deep recession has ensued, with a peak-to-trough decline in real GDP of around 17 per cent. In US dollar terms, nominal GDP has dropped by almost half to just $93 billion, with per capita GDP at market exchange rates (as opposed to PPP) down to around $2,200 in 2016,86 the lowest in Europe. High inflation and a weakened currency have compounded the situation, their effects particularly evident in the initial aftermath of the Euromaidan. In early 2015, the rate of consumer price inflation spiked to close to 60 per cent, while in the year to March 2015 the hryvnia lost two-thirds of its value. The government, meanwhile, was forced into default on its private-sector Eurobond liabilities, resulting in a debt restructuring in November 2015.

It should not be forgotten that Ukraine’s recent economic decline was not all the result of its own systemic failings. A range of external forces also buffeted the economy. These included Russia’s annexation of Crimea, Russian military intervention and the conflict in Donbas. They also included a trade war with Russia and a marked drop in demand and prices for key Ukrainian exports, particularly metals, around this same time (2014–15). These forces added to the difficulties for Ukraine’s economic reform team. Indeed, set against a weak starting point and the considerable subsequent shocks to the Ukrainian economy after the Euromaidan revolution, it is remarkable what has been achieved to date.

Since the worst of the economic crisis in 2014–15, the outlook has brightened. A combination of a flexible exchange rate policy, tight fiscal and monetary policy, and energy sector reform/adjustment, among other actions, reinforced by two IMF support programmes, has brought a remarkable stabilization in the macroeconomy – perhaps the first proof of the success of the policy adjustment.

Macroeconomic stabilization has now set the stage for growth and recovery

Economic growth resumed, admittedly from a low base, in 2016, with preliminary data suggesting a respectable 2.3 per cent rise in real GDP.87 Prior to the blockade by Ukrainian war veterans of the separatist-controlled Donetsk People’s Republic (DPR) and Luhansk People’s Republic (LPR) in early 2017, full-year growth in 2017 had looked set to accelerate further, to perhaps 2.5–3 per cent at least. Inflation has dropped to around 15 per cent year on year, and the currency has strengthened to around UAH 25:$1. The current account went from a deficit of 9.2 per cent of GDP in 2013 to close to balance in 2015, admittedly helped by a recession-induced downturn in domestic demand; it has since moved back into a more modest deficit, equivalent to 3.6 per cent of GDP in 2016, as the resumption of real GDP growth has boosted imports.88 Ukraine’s weak fiscal position has also improved (see ‘Reform of public finances’, below).

Importantly, macro-stabilization has now set the stage for growth and recovery, with the pace of the latter dependent on the successful implementation of a range of micro-level policies to improve the business environment and encourage locals and foreigners to invest.

In terms of the specific reforms rolled out since the Euromaidan revolution, the following stand out as highlights:

The National Bank of Ukraine (NBU) moved to a more flexible exchange rate arrangement in 2015. This allowed the hryvnia to weaken significantly in nominal and real terms, which in turn supported the broader macroeconomic adjustment. The move was partly driven by the paucity of the NBU’s foreign exchange reserves, which had dropped to a low of under $5 billion in the first quarter of 2015, but there was also strong ideological support within the NBU to let markets work. Recognizing the need for financial stability, the NBU maintained certain restrictions on current- and capital-account transactions – tightening export surrender requirements and restricting the transfer of dividends out of the country. Subsequently, as the hryvnia has stabilized, and with foreign exchange reserves bolstered beyond the level of three months’ import cover typically deemed critical, the NBU has moved to relax these requirements.

The changes at the NBU are now hailed as a model for wider public-sector administrative reform

The central bank seems committed to a floating exchange rate, which was a requirement for the de facto introduction of an inflation-targeting regime in early 2016. In setting the stage for this reform, the NBU has substantially reformed its internal structures, streamlining and winding down non-core functions. It has focused resources on the traditional functions of an inflation-targeting central bank, while remaining cognizant of its role in regulation and supervision of the banking sector. The research function and markets departments at the NBU have been strengthened beyond recognition, even as overall reforms have reduced the bank’s staff from nearly 12,000 to around 5,000, with headcount likely to fall further still. The changes at the NBU are now being hailed as a model for wider public-sector administrative reform.

The NBU has been instrumental in transforming the Ukrainian banking sector over the past three years. In 2014 the country had too many banks (more than 180), many of which were close to bankruptcy and suffered from a range of problems that included: high non-performing loan (NPL) ratios;89 rapidly eroding capital bases; large, open foreign exchange positions; deposit flight; and a prevalence of connected-party lending and money-laundering. It is fair to say that the sector was on the brink of collapse, was a clear and present threat to macroeconomic and financial stability, and imposed a large contingent liability on the state.

The NBU has responded with an impressive restructuring programme. Supervision and regulation have been stepped up dramatically. The NBU has rolled out extensive stress-testing and asset quality reviews of banks, with asset and capital deficiencies identified and resolution plans agreed. Nearly 90 banks have been closed. These have included a number (around 20) deemed to have been engaged in money-laundering, and others with failed/failing business models and owners unwilling or unable to impart change and recapitalize operations. Connected-party lending has been reined in. Some high-profile and politically sensitive cases have proceeded, most notably the nationalization of PrivatBank, the country’s largest bank. The existing two main state-owned banks (Ukreximbank and Oschadnyi Bank) have undergone extensive internal restructuring, with management and boards changed or revamped. They have also benefited from substantial recapitalization by the state.

It is testimony to the skill and tenacity of officials at the NBU, and also at the Deposit Insurance Fund, that these revolutionary changes have been effected without causing broader systemic problems. The nationalization of PrivatBank went ahead without prompting the run on system deposits that some had feared. Extensive preparation seems to have been a major factor in the operation’s success – the preliminary work started two years in advance, supported by international financial institutions that included the IMF.

Successive post-Euromaidan governments have undertaken far-reaching fiscal consolidation, cutting spending and raising revenues. Helped to a certain degree by an inflation tax, the fiscal deficit fell from 10 per cent of GDP in 2014 to just 2.2 per cent of GDP in 2015, before rising fractionally to 2.3 per cent of GDP in 2016. By the first half of 2017, the fiscal position was in surplus. Central to this adjustment was the eradication of the deficit at Naftogaz, the state-owned gas supply and transit company. The fiscal position specific to Naftogaz went from a deficit of 5.5 per cent of GDP in 2014 to balance in 2016 (see ‘Energy sector reform’, below).90 Moreover, the 2016 budget introduced extensive policy reforms to simplify the tax system and reduce informality throughout the economy. It sought to widen the tax base, improve tax compliance and boost revenues. The main elements of the reform programme were as follows:

As yet, the benefits of these reforms have yet to accrue in terms of revenue. Much of the fiscal adjustment noted above came from budget cuts, with spending as a share of GDP falling from 44.8 per cent in 2014 to 40.6 per cent in 2016. Revenue itself dropped from 40.3 per cent of GDP to 38.4 per cent of GDP over the same period.91

The 2016 budget introduced extensive policy reforms to simplify the tax system and reduce informality throughout the economy

A key reform rolled out in 2016 was the introduction of the ProZorro public procurement system (see Chapter 6, in particular). There are hopes that this system will significantly improve transparency and efficiency in public procurement, while reducing scope for graft. Annual system budget savings of as much as $2 billion, equivalent to around 2.5 per cent of GDP, are anticipated.

Further savings have been achieved as a result of the Ministry of Finance (MOF)’s debt restructuring of $15 billion in sovereign and sovereign-guaranteed Eurobond liabilities in 2015. The landmark deal, which included a 20 per cent principal haircut and a three-year maturity extension, reduces Ukraine’s obligations by around $12.5 billion over the three-year period of the IMF Extended Fund Facility (EFF). While the operation was criticized for its generosity to bondholders (particularly its provision of GDP warrants with large potential long-term payouts), it bought time for the government to refocus on critical policy challenges and prioritize other reforms, free of concerns over the near-term debt-servicing burden.

Energy reforms have transformed Ukraine’s fiscal and balance-of-payments positions, and have created opportunities for the sector to become a dynamic driver of economic growth. As noted above, the Naftogaz contribution to the quasi-fiscal deficit has been cut, and the company is now running a profit. The gas import bill, meanwhile, has been cut from $12 billion in 2009, when gas imports ran at around 40 billion cubic metres (m3), to around $2 billion at present, with gas imports below 10 billion m3. Importantly, zero imports are planned from Russia in 2017.

Energy sector reforms have transformed Ukraine’s fiscal and balance-of-payments positions

The reform strategy has been orthodox. Domestic gas prices have been raised to cost recovery levels – implying price increases of 200–300 per cent in some cases – with price hikes accompanied by targeted financial assistance to around 5.5 million households disadvantaged by the rise in their fuel bills. The cost of subsidies paid to households has increased, from 1 per cent of GDP in 2015 to 1.75 per cent of GDP in 2016. This has cushioned the blow of the adjustment, while encouraging energy conservation and diversification. To put this into perspective, over the past decade annual gas consumption in Ukraine has been cut by around half to under 35 billion m3. With further reforms, consumption is likely to be cut even further, to the point that in the medium term it may be possible for Ukraine to become self-sufficient in gas or even a net gas exporter.

A new gas market law is intended to underpin the unbundling of Naftogaz and the national gas market, allowing third-party access to gas transmission facilities. Meanwhile, the management and supervision of Naftogaz have been overhauled, with assistance from international financial institutions. That said, the introduction of a new Naftogaz statute, which would reinforce improvements in corporate governance, is being resisted by vested interests, as is the unbundling process.

Further reforms in the energy sector will need to focus on several issues: executing the unbundling of the gas and electricity sectors; targeting social assistance more effectively (as the current system is arguably too generous to better-off families); improving the efficiency of district heating companies; addressing non-payment problems; and, more generally, improving efficiency across the network. On the latter point, despite progress over the past two to three years, there remains considerable room to reduce energy consumption through efficiency gains.

The success of the recent reforms is significant. It is worth stressing that for much of the period since independence, excuses for non-reform of the gas-pricing formula have abounded. Foot-dragging in this area likely reflected the fact that the rents extracted by Ukraine’s elites from this source were substantial – in the region of $2–3 billion a year. Yet despite resistance from vested interests and some economic hardship in the general population, the reforms have been rolled out without causing a social revolution.

The successful reforms identified above are primarily macroeconomic, providing a top-down impact on the environment in which business operates. While the resultant stability sets the stage for stronger economic growth in broad terms, the quality and precise pace of growth will now arguably be determined by micro-level reforms. These include measures to improve the underlying business environment, particularly by reducing bureaucracy, corruption and excessive regulation. On this latter score progress has been much more chequered. Some of the important reform priorities are as follows:

There is a pressing need to reform the antiquated pension system, which is simply not fit for purpose and remains a huge drag on the public finances. The current system provides entitlement to too many individuals. It imposes a financial burden both directly on the government and indirectly on businesses, which ultimately must fund the system through taxes and social security contributions. The pension system costs the equivalent of around 11–12 per cent of GDP, compared with a European average of 8–9 per cent of GDP. It runs a deficit equivalent to around 6 per cent of GDP, largely funded by direct transfers from the state budget.92 Not only is the retirement age too low, but special preferences in particular professions (the police, army, civil service) weigh the system down. Social security contributions have fallen, and widespread avoidance of payment by employers further inhibits revenues.

There is a pressing need to reform the antiquated pension system

The obvious solution is ‘parametric reform’ – that is, adjusting parameters such as contribution rates, the retirement age and so on – but populists within the Verkhovna Rada bitterly oppose this. Policymakers have suggested that hikes in the retirement age can be avoided by lowering the dependency ratio – at present, the ratio of pensioners to contributors stands at a remarkably low 1:1, but it is expected to rise to 1.3:1 (beneficiary to contributor) by 2040 as the population ages.

In addition to parametric adjustments, the most likely reforms entail increasing the pool of contributors by reducing informality in the economy. Change seems inevitable at some point, as the present system costs too much to run yet fails to provide a living pension (average pensions are the equivalent of just $2 per day). At the time of writing, there were hopes that the Rada would approve an IMF-compliant pension bill in the autumn of 2017.

Opinion polls consistently suggest that corruption remains one of the biggest problems for domestic and foreign businesses, and for Ukrainian society more widely. Successive governments have paid lip service to fighting corruption, with support from international organizations. Anti-corruption efforts have been the cornerstone of IMF, World Bank and EU/European Bank for Reconstruction and Development support programmes. Some institutional reforms have been rolled out (see chapters 6 and 7 in particular). They include the ProZorro public procurement system; an ‘e-declaration’ system, launched in September 2016, for recording the assets of Verkhovna Rada deputies, ministers and government officials; and the establishment of the National Anti-Corruption Bureau of Ukraine (NABU). The NABU has been operational since January 2016. Plans are afoot to create special anti-corruption courts and appoint anti-corruption judges – something the IMF is currently pressing the government to deliver on as part of the fourth review under the IMF EFF.

Despite all this activity, there has been little real progress in the investigation, prosecution and conviction of individuals over corruption. While the asset e-declaration system was hailed as a landmark for Ukraine, and indeed globally in the fight against corruption, few of the seeming irregularities uncovered in the initial set of declarations have been formally addressed. If the system is perceived as failing to investigate, prosecute and convict politicians and public officials for wrongdoing, the risk is of a popular backlash against reform, which could itself bring populist, less reform-minded individuals to power and affect overall prospects for economic/policy transformation.

The abolition of the tax police was also a major achievement

Dovetailing with the anti-corruption agenda is the urgent need to overhaul the State Fiscal Service (SFS), which encompasses the tax and customs administrations. The recent annual report of the business ombudsman showed the SFS to be the most complained-about government institution, accounting for 45 per cent of all complaints. The SFS has now been put under the control of the MOF rather than the Cabinet of Ministers. This should give the minister of finance more scope and responsibility to reform the service; hitherto, the SFS had operated in a murky no man’s land between the MOF and the prime minister’s office. A structural benchmark for the fourth review under the current IMF programme is the merger of the tax and customs administrations. If implemented, this should further boost efficiency and MOF oversight, and reduce the scope for graft. The roll-out of electronic systems throughout the SFS should result in a more rules-based system in which the use of arbitrary discretion by revenue officials becomes less prevalent.

Already some success has been achieved with the electronic administration of VAT returns. The abolition of the tax police with effect from January 2017 was also a major achievement, as corrupt officials in the organization had operated with impunity for years – indeed, doubts remain as to whether the tax police was ultimately revenue-enhancing or revenue-subtracting, given the prevalence and likely scale of embezzlement. Corruption remains hard to eradicate: following the tax police’s demise, other security agencies have sought to fill the void in terms of rent-seeking. Nonetheless, the recent arrest of the head of the SFS, Roman Nasirov, raises some hope that the administration under President Petro Poroshenko is finally willing to act on allegations of corruption.

The 3,000 or so enterprises (accounting for around 10 per cent of GDP) at present remaining in state ownership represent a source of inefficiency in the economy, a continued drain on the public finances through their need for subsidies, and a source of corruption.

There is acceptance within policy circles that to solve the problems at many of these entities, it be will be necessary to improve their corporate governance and transparency, privatize them or put them into liquidation. Some effort has been made over the past few years to improve the management and supervision of entities such as Ukrainian Railways and Naftogaz. However, privatization has struggled – not helped by the weakness of supporting infrastructure and legislation, a difficult macroeconomic environment, and the regional political and security setting. The hope had been that the Odesa Seaport privatization would prove to be a model for other SOEs to follow, but the sale ultimately failed, weighed down by legal controversy and challenges, and also perhaps by uncertainties over the broader business and investment environment. The future of the next big entity expected to go under the hammer, the power generator Centrenergo, is similarly clouded in uncertainty.

A recent announcement over a ‘triage’ solution to managing SOEs, including plans to privatize, liquidate or sell concessions in many firms while keeping only 15 strategic enterprises in state ownership, is encouraging.

It remains ironic that in Ukraine, home to the rich black soils known as ‘chernozem’ and arguably the best agricultural land in Europe, land reform has been sadly lacking. The potential of the Ukrainian agricultural sector is huge. Grain yields are currently one-third or more below those in Western Europe, but could easily reach parity given the right use of inputs and the right upstream and downstream support systems. This could push annual grain production from 60–70 million tonnes towards 100 million tonnes. However, the key impediment remains the lack of a functioning market for land, necessary for significant economies of scale to be extracted.

The potential of the agricultural sector is huge

Arguments against reform suggest that Ukraine is somehow ‘different’, and that special factors are at work compared to countries where land markets allow farmers to use land as collateral for loans (thus enabling them to invest). There is also the argument that small landowners will be exploited by large capitalist farmers – but that already seems to be the case with the existing leasehold system. It seems more likely that vested interests (well represented in the Verkhovna Rada) behind large leasehold farming systems are preventing much-needed change. But land reform, if well-constructed, could be truly transformational for Ukraine, once again making it the ‘breadbasket’ of Europe and enabling the agricultural sector to become a powerhouse for the rest of the economy.

There is a sense that the four major areas of reform on the agenda – pension reform, delivery on the anti-corruption agenda, privatization and land reform – have now brought Ukraine to something of a turning point. Delivery on these reforms could improve the outlook for economic growth and mark out a bright future for the country. Indeed, with effective institutional changes, there is no reason why Ukraine cannot top the European growth stakes and enjoy a rise in GDP growth – admittedly from a low base – to an average of perhaps 5 per cent per annum. Inevitably, vested interests will try to stand in the way. But what we have learned from successful reforms so far in banking, the energy sector and the public finances is that Ukraine – far from being a lost cause – is reformable, if international financial institutions and civil society continue to press reluctant elites to deliver.