As the Chinese authorities prepare their 15th Five-Year Plan (for 2026–30), to be unveiled in the autumn of 2025, emerging economies seeking to exploit China’s ambition for closer political relations should make the case for the leadership in Beijing to adopt a domestic macroeconomic framework that gives developing countries more chance to sell goods and services to China. What’s needed, in effect, is for China to sacrifice some of its large and persistent current account surplus in the service of better relations with these trading partners.

The policies needed to deliver more rapid domestic spending growth in China are well known. They include: increasing the provision of public healthcare and education, to reduce Chinese households’ incentive to save; supporting domestic credit markets with additional monetary stimulus; reforming the hukou labour registration system to give migrant workers more confidence to spend; and lowering trade barriers for a wider set of developing countries than the low-income countries to which China offered zero-tariff access in 2024.

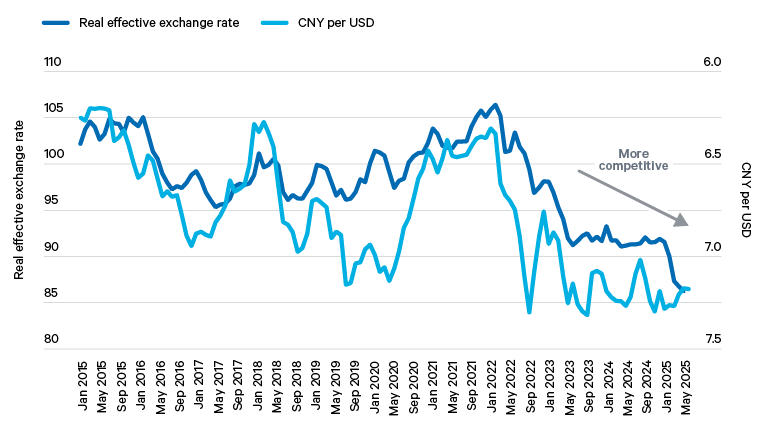

If there is a single policy that countries in the Global South might usefully encourage China to adopt, it is to allow the renminbi to appreciate, thereby increasing the attractiveness to Chinese consumers of imported goods relative to domestically produced ones.

Yet if there is a single policy that countries in the Global South might usefully encourage China to adopt, it is to allow the renminbi to appreciate, thereby increasing the attractiveness to Chinese consumers of imported goods relative to domestically produced ones. A stronger currency would not only boost China’s imports from emerging economies, of course, but would increase its imports across the board. That does not matter: the more China can play a role as a global importer overall, the more emerging economies stand to benefit, not only because of increased Chinese demand for their own goods, but also because of the increase in overall trade that is likely to result from such a move. International pressure on China to revalue its exchange rate has been picking up recently, based partly on a growing body of analysis suggesting that the renminbi is undervalued. Emerging economies should make use of this momentum to add their own voices to this debate.

China will have one obvious and substantial objection to a stronger currency, namely that this is likely to intensify the deflationary pressures the economy is facing. Set against that, however, is President Xi’s emphasis on the need for a ‘strong currency’ to support China’s ambition to enhance the renminbi’s global importance. Indeed, exchange rate movements in recent weeks offer some encouragement that this latter argument is dominating: the renminbi has been strengthening modestly, a possible harbinger of further gains.

Countries of the Global South can usefully put the case to Beijing that the international prestige of the renminbi, and indeed of China itself, would be strengthened by a further measurable appreciation of the currency. They might also argue that this is the only way in which China can take fuller advantage of the diplomatic gifts that Washington seems inadvertently to have bestowed on it. Of course, it is not only, or even primarily, developing countries whose trade balances might benefit from a stronger Chinese exchange rate: manufacturing exporters in the US and the EU could well benefit to a much greater extent than those in the developing world. But if China is seen to be responding to a plea from the Global South, rather than to pressure from trading partners in the G7, the diplomatic benefits for China could be considerable, especially if combined with a more liberal trade policy that offers advantages to emerging and developing economies.