Latin America’s trade policy hostility towards China focuses heavily on the steel industry. Latin American producers have come under huge competitive stress in recent years as a result of rapid rises in Chinese imports. This is a trend most evident in Brazil. Previously, between 2017 and 2020, the country’s annual steel imports from China had never exceeded $1.5 billion. However, by 2024 Brazil’s steel imports from China had reached $3.9 billion, a near-threefold rise. Brazil is a very large iron ore producer, and it sells this ore to China. In turn, China makes finished steel products and sells these back to Brazil at prices which Brazilian manufacturers cannot compete with. Since June 2024, the Brazilian government’s response has been to apply a tariff-rate quota (TRQ) system under which steel imports above specified quotas face a 25 per cent tariff. Mexico and Colombia have also responded to sharp increases in Chinese steel imports by imposing tariffs of their own.

Yet developing countries need to be careful in pursuing trade remedies like this, since China has a track record of retaliation. In 2010, for example, China effectively banned imports of Argentinian soybean oil after Buenos Aires imposed anti-dumping measures and import restrictions on Chinese products including shoes and steel pipes. Retaliation of this kind has not been seen more recently, but given that it has featured in Chinese trade policy before, it may well do so again.

For Brazil specifically, an additional vulnerability arises from China’s attempt to diversify its own iron ore supplies and become less dependent on producers in Brazil and Australia; together, the two countries have accounted for over 80 per cent of China’s imports of iron ore in recent years. The diversification agenda has led China to seek deeper partnerships in Africa, including with Cameroon, Congo, Guinea, Liberia and Sierra Leone. On balance, this reduces Brazil’s negotiating leverage, since Beijing can wield the threat of accelerating China’s efforts to procure alternative sources of iron ore.

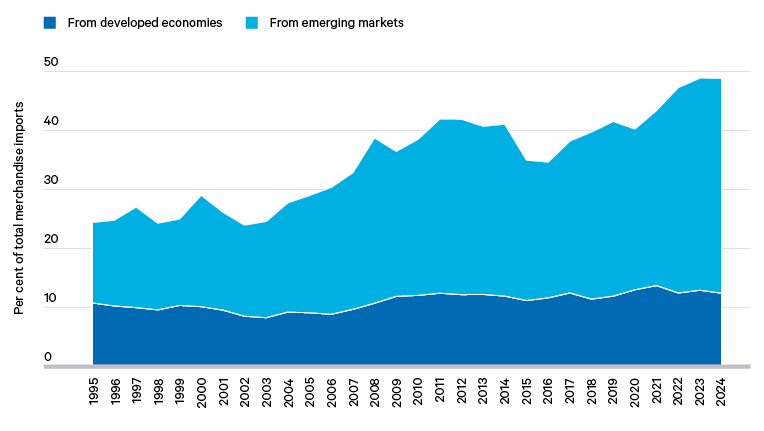

Growing dissatisfaction with Beijing is compounded by the sense that China’s trade relationships with emerging economies are asymmetrical.

For many, growing dissatisfaction with Beijing is compounded by the sense that China’s trade relationships with emerging economies are asymmetrical: China imports commodities from them, and exports manufactured goods to them. This is partly an outcome of China’s industrial strategy, which can be characterized as a simultaneous effort, on the one hand, to reduce China’s reliance on the rest of the world by substituting imports with domestic production and, on the other hand, to increase the rest of the world’s reliance on China by establishing the country as an export-oriented manufacturing powerhouse (zhizao qiangguo). Both elements of this strategy mean that China’s demand for emerging economies’ manufactured exports is likely to stay low.

A growing share of China’s imports consists instead of commodities, increasingly supplied from the developing world. A common criticism of this pattern of trade is that it leaves emerging economies struggling to increase their industrial value-added, and that it locks them into dependence on production of primary goods (i.e. commodities and raw materials), unable to convert their natural resource endowments into a meaningful base for industrial development.