Beijing’s new rules announced on Thursday stipulate that licenses will be required for the export of technologies used in rare earth mining and processing, as well as for the manufacturing of magnets, which can be used in military technologies. Crucially, any foreign firm that wants to supply rare earths produced in China or processed with Chinese technologies outside China will also need to get a license, according to China’s Ministry of Commerce.

These restrictions send a particularly powerful signal because Chinese companies control more than 90 per cent of the world’s processing capacity for rare earths.

The new rules could also give President Xi Jinping greater leverage as he prepares to meet US President Donald Trump in South Korea later this month to discuss bilateral trade frictions. The rare earths that Beijing is increasing its control over are critical to a range of technologies from electric vehicles to wind turbines and defence systems. The new restrictions on rare earths come amid a freeze by China on buying US soybeans from the autumn harvest – another instance of Beijing building leverage with Washington.

The move by Beijing refocuses attention on how China uses its influence as the world’s biggest trading nation and its dominance of manufacturing supply chains to project its power in international affairs.

China’s willingness to use its trade heft to advance geopolitical goals should make policymakers in the West wake up to the burgeoning power of China’s manufacturing supply chain and its control over certain so-called ‘chokepoint’ technologies – which it can limit access to at will.

China’s growing dominance of global manufacturing

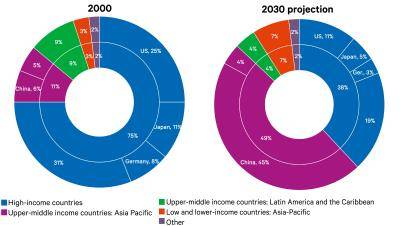

A 2024 report by UNIDO (The United Nations Industrial Development Organization) projects that by 2030, China will account for 45 per cent of global manufacturing value added, compared to 11 per cent for the United States, 5 per cent for Japan, 3 per cent for Germany and even less for the UK.

The report did not give a current value for China’s share of global manufacturing but according to the United Nations Statistics Division, China’s share of global manufacturing was 29 per cent in 2023. The scale of the projected transformation is therefore stark. China will gain around 16 percentage points in global manufacturing market share over the next five years, if the UNIDO predictions are borne out.

It will also mean the global manufacturing hierarchy has been completely upended. Back in 2000, the US accounted for 25 per cent of global manufacturing while China had just 6 per cent.

The changing structure of global industrial production

Source: UNIDO: The Future of Industrialization. UNIDO projections to 2030 are made based on historical average annual growth rates (between 2010 and 2019) and applied to the latest available observations (2024) up to 2030.

The inherent disruption that this scenario spells out for the West is sharpened by the fact that Chinese companies compete not only with mid-technology counterparts in the West but also at the apex of the tech pyramid. Research from the Australian Strategic Policy Institute (ASPI) shows that China leads the US in 57 out of 64 critical technology categories.

Thus, in the future, it may be the West’s technological leaders – many of them politically significant employers – that bear the disruptive brunt of China’s rise.

China’s stranglehold on key industries

The dominance of the supply chains that buttress China’s advances in manufacturing also give Beijing formidable commercial leverage – which it has proven willing to use.

This should focus the minds of policymakers in Europe and the US to identify other industries in which China exerts global dominance that could at some point in the future be used as leverage.

Some of these industries are well known. For solar panels, China’s share in all the manufacturing stages (such as polysilicon, ingots, wafers, cells and modules) exceeds 80 per cent, according to the International Energy Agency (IEA). In addition, the world’s top 10 suppliers of solar photovoltaic manufacturing equipment are all Chinese.

It also dominates in wind power, accounting for 50 to 70 per cent of the manufacturing capacity for key components like nacelles, towers and blades. This share is expected to continue to grow as Chinese makers feed into the country’s infrastructural build out and its competitively priced technology increases its market share overseas.