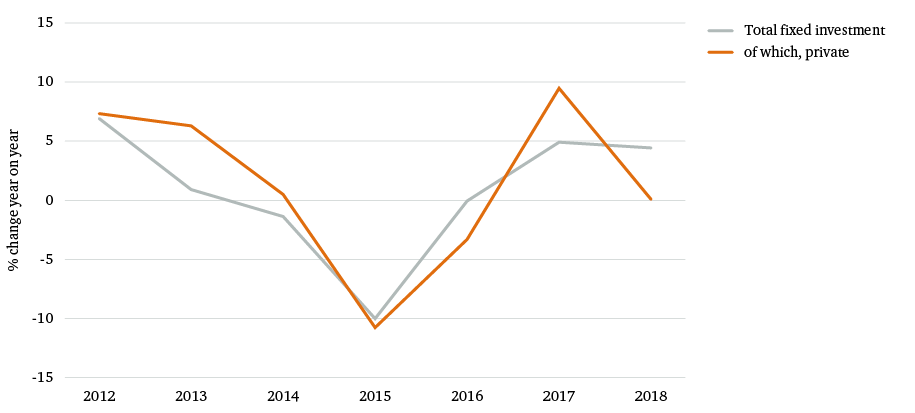

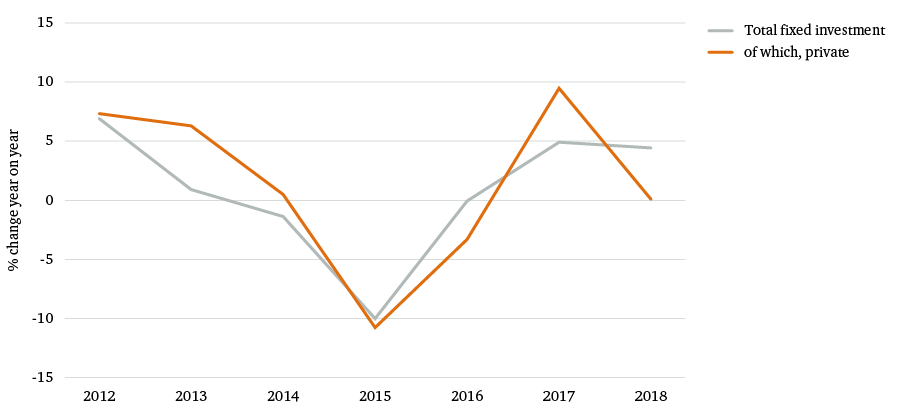

Weak private investment probably reflects increased uncertainty about the state of the world economy (and especially economic performance in Europe), about international political tensions, and perhaps about changing rules of the economic game in Russia as state influence expands.

Weak investment and a declining working-age population might in principle be offset by strong growth in the productivity of labour and capital combined (i.e. total factor productivity – TFP). This has not been the case in recent years. In a working paper for the World Bank, Okawa and Sanghi estimate that TFP growth averaged 2.9 per cent annually in 2000–09, and that it was down to 1.3 per cent in 2017. Their baseline projection of potential output (i.e. output at full employment of capital and labour) has it edging down from 1.5 per cent in 2017 to 1.3 per cent in 2023.

Examining possible sources of acceleration, Okawa and Sanghi estimate that pension reform could add 0.3–0.4 percentage points to annual growth in 2020–28. A rise in the investment share of GDP from 23 per cent in 2017 to 34 per cent in 2028 would raise GDP by 0.6 per cent per year by 2028. A reform scenario (achieving more competition) could lead to a 0.1 per cent increase in average annual TFP growth in 2017–28, instead of the 0.2 per cent decrease projected in their baseline scenario (to 1.1 per cent growth). All of the above, plus a rise in net immigration, would by their assessment contribute to an enhanced growth rate in potential output of 3 per cent by 2028.

This would be a less rapid acceleration than Putin is calling for, but it would be a step in the right direction. What are the obstacles to such an improvement? Demographics account for the near-zero growth in employment, but what are the influences that sap investment and productivity growth?

According to Aleksei Kudrin, speaking in a personal capacity and in one of his more radical moments, Russia is in a ‘stagnation pit’, ultimately because of the lack of political competition. The general line of argument is that corrupt political incumbents at local, regional and national level offer protection in deals with favoured firms, creating unpredictable risks for firms without such protection (particularly asset-grabbing by insiders) and thus weakening both the confidence of potential losers and the competitive pressures on incumbents to invest and innovate. The overall result is low private investment, slow innovation, stunted development of small firms, and therefore slower growth than would otherwise be achieved.

What is meant by asset-grabbing in today’s Russia? To give a typical example, firm A conspires with law-enforcement officials to bring charges of ‘economic crime’ (say, fraud) against the main owner of firm B. A complicit judge rules that the accused must go into pre-trial detention – where conditions can be harsh, and the custody of uncertain duration. The ‘raiders’ (i.e. asset-grabbers) work on the detainee to surrender some or all of firm B to firm A and eventually he or she gives in and is released. The case does not come to trial, and the judge and the law-enforcement officials get their cut. There may or may not have been any fraud to begin with.

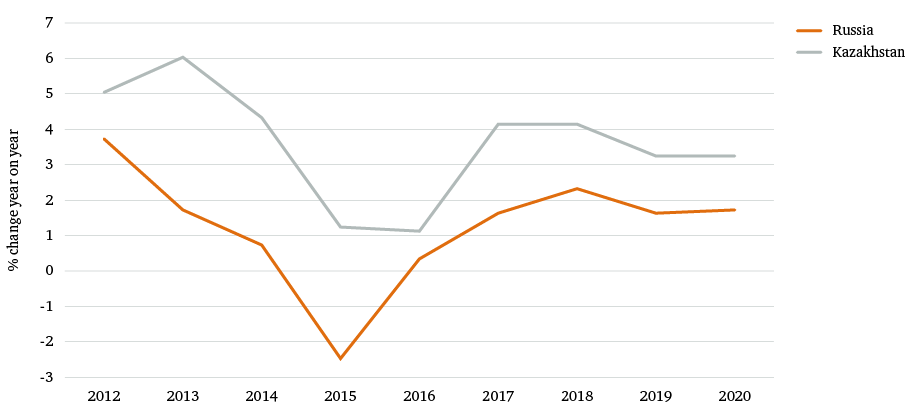

There are two obvious objections to this linking of weak growth to the lack of political competition. One is that there was no political competition in the 2000s, when the Russian economy was growing quite strongly. The other is that there are countries with an apparently similar political economy, notably Kazakhstan, that have continued to grow at, or a bit above, the global average rate.

So far as the change in trajectory over time is concerned, it appears that Russian economic growth of the 2000s was supported by other factors that have subsequently ebbed. A substantial growth accounting exercise for the boom period, estimating the contributions to growth of different factors, makes this clear (see Table 1).