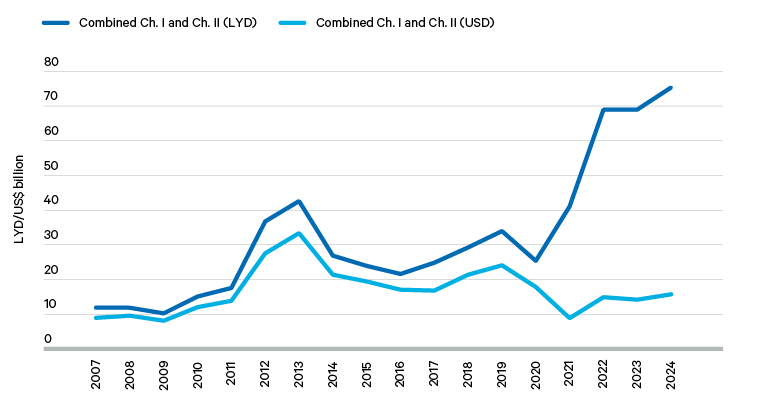

This pattern has corresponded with a reduction in the delivery of public goods by the state, as governance and public sector performance have been undermined by corruption, a lack of capacity, internal disputes and inefficiency. State largesse has remained visible in persistent public sector salary increases, as shown in Figure 1. However, the salary bill is divided among an increasing number of state employees on modest salaries, while other channels of spending show lavish payments to supporters of well-connected elite interests. (In just one example, videos emerged on social media in September 2025 depicting a games lounge kitted out with luxury computer gaming stations and a café for members of the state-affiliated 111 Brigade, which is closely aligned with the GNU in Tripoli.) The result is that reported spending on ‘Chapter I’ of the state budget (salaries) and Chapter II (operating expenses, including state officials’ salaries and other procurements) has grown from 11 per cent of GDP in 2008 to 34 per cent of GDP in 2024.

Economic and political marginalization – real and perceived – has played a potent role in Libya’s conflict and continues to present significant questions about the future of the Libyan state with regard to the locus of authority between the country’s western and eastern regions. Groups that clearly have been marginalized – such as the Tebu and Tuareg communities, based predominantly in the country’s south – have fought to improve their status, but have had relatively little impact over national-level governance. Yet, in recent years such problems have become increasingly subordinate to the governance challenges associated with state capture.

The state as a resource

Libya’s economy is dominated by the state at all levels. To the extent that hyper-centralized, Gaddafi-era structures remain in place, economic governance has, formally at least, changed little since 2011. Gaddafi’s regime had accelerated ‘Libyanization’ reforms – whereby internationally owned commercial enterprises were nationalized by the state – following his ascent to power in 1969. This resulted in all oil companies and banks being under state ownership by the end of the 1970s. In the 1980s, the regime went further as political institutions were reformed to deliver ‘direct democracy’. In the economic realm this translated into the partial abolition of the private sector in favour of state-run enterprises, and in the nationalization of most remaining foreign-owned companies and assets. This state dominance created a complex web of committees, agencies and monopolies. If anything, the situation has become even more complicated in the post-2011 period, as more institutions have been formed while existing institutions have remained in place.

This legacy means that state institutions and state-owned enterprises effectively have dominion over the sectors in which they operate. For example, the Central Bank of Libya (CBL) not only is responsible for monetary policy and financial regulation, but also has ownership stakes across most of the banking sector. Consequently, the CBL has over the last 10 years been able to influence appointments at commercial banks which the CBL owns. In the post-2011 period, a number of CBL employees accepted board roles at these commercial banks, creating potential conflicts of interest. Moreover, the CBL maintains a monopoly on the distribution of foreign currency and must authorize all documentary letters of credit for the import of goods. These extensive powers place the CBL in a dominant position in the banking sector.

The situation is mirrored elsewhere in the state system, notably in relation to the National Oil Corporation (NOC). The NOC owns 15 subsidiaries and is part owner of nine joint ventures. International companies operating in the Libyan oil sector can only hold minority shares in these joint ventures.

Private companies operate as contractors to the state in areas ranging from construction to catering to oil services. In recent years, companies associated with armed groups have expanded in these areas.

The dominance of state institutions and state-owned enterprises leaves little room for development of the private sector based on fair competition. Indeed, the principal customer of Libya’s private sector is very often the state itself, rendering private companies reliant on cultivating relationships with state entities and officials. Private companies operate as contractors to the state in areas ranging from construction to catering to oil services. In recent years, companies associated with armed groups have expanded in these areas. Because state institutions are the customers, control of these institutions in turn assures control over the distribution of contracts. Private companies also complain that state-owned enterprises enjoy market-distorting advantages. In some instances, procurement rules explicitly stipulate that state-owned entities should be given preferential treatment. State-owned enterprises are also often shielded from considerations of profit and loss, meaning that works can be subcontracted to the private sector at inflated prices, sustaining corrupt practices.

These factors have facilitated the expansion of patronage networks and the rise of vested interests. Officials in control of state institutions are often able to use their positions to sign contracts with companies in which they may hold a beneficial interest. Where this happens, the state entity loses money and the official gains private profits. This pattern has become particularly notable in sectors such as healthcare, where procurement is strongly impacted.

Elite capture and shifts in economic governance

More widely, these dynamics reflect the fact that the Libyan state is increasingly being captured by elite networks associated with a handful of leaders. It appears that some of these leaders have overseen a massive expansion of corruption that has been dubbed a ‘kleptocratic boom’.

The ever closer links between elite networks and the state have been particularly noticeable in the oil sector, where private Libyan and foreign companies alike have received significant contracts to sell oil on behalf of the Libyan state. On the domestic side, one example is the emergence of Arkenu, a private Libyan firm believed to be controlled by vested interests connected to prominent political families, and noted by the UN Panel of Experts to be ‘indirectly controlled by Saddam Haftar’. On the international front, meanwhile, Turkish and Emirati political influence appears relevant to the growing role of BGN in Libya’s oil sector.

Such developments suggest that the consolidation of commercial influence also has an international dimension. Indeed, the nature of international engagement with Libya’s state has shifted in recent years: where once there was multilateral consensus on the need for unified and stable governance, this shared understanding has given way to competition between foreign actors over spheres of influence and access to Libyan territory and resources.

Similar dynamics are visible in other sectors. In telecommunications, a new company, O3, has emerged with close links to Libya’s rulers. In the infrastructure sector, al-Aamar Holding Company offers a further such example. These trends appear to indicate that where the private sector is replacing public companies, it may be doing so in concert with vested interests.

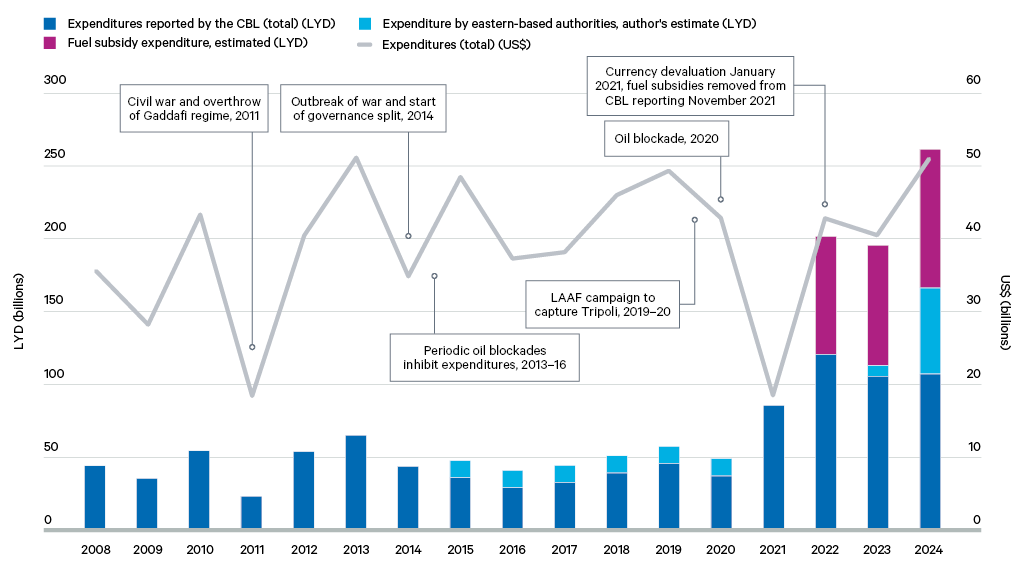

In short, a predatory political economy dominates Libya’s state landscape, with a number of vested interests extracting increasingly large amounts of funds from the state for little in return. Figure 2 illustrates how this trend has driven an expansion of state spending, albeit one that has been masked in the official figures because two major sources of spending are absent from the CBL’s figures. The first is the massive increases in fuel subsidies, data for which were removed from the CBL’s disclosures in November 2021. If the CBL and Libyan Audit Bureau’s own estimates of fuel subsidy expenditure are factored in, an additional US$50 billion was spent between 2022 and 2024. Figure 2 includes these expenditures.

A predatory political economy dominates Libya’s state landscape, with a number of vested interests extracting increasingly large amounts of funds from the state for little in return.

The second reason for the discrepancy between official data and actual fiscal outlays is that expenditures by the eastern-based authorities, made via their own financing mechanisms, are also excluded from the CBL’s figures. The World Bank estimates that the government debt owed by the eastern authorities totalled LYD 71 billion (approximately US$65 billion) in 2014–20. In 2023, the eastern branch of the CBL engaged in monetary financing of around LYD 7.2 billion (US$1.5 billion) in support of the GNS. Also in 2023, capital expenditure escalated significantly through the Haftar family-controlled Libyan Development and Reconstruction Fund; such spending reached LYD 59.1 billion (approximately US$12.3 billion) in 2024. Figure 2 also includes these expenditures.