If a new trade policy framework can be developed, Trump’s presidency could offer a chance to move the debate forward and actually strengthen global trade by addressing some genuine shortcomings within the current system.

Implications for the US and the World

Research paper

Published 3 November 2017

Updated 18 May 2023

ISBN: 978 1 78413 244 6

If a new trade policy framework can be developed, Trump’s presidency could offer a chance to move the debate forward and actually strengthen global trade by addressing some genuine shortcomings within the current system.

While trade policy under the Trump administration is still in its early stages of evolution, and its eventual shape cannot be predicted with total certainty, there are already pointers that give a good sense of the direction it will take. Trade – unlike many other policy areas – featured heavily in Trump’s presidential election campaign, and while there is the question of how far his rhetoric may translate into policy actions, Trump’s extensive commentary on trade offers insights into his thinking. The now president has, moreover, been fairly consistent in his publicly expressed views on trade since the 1980s. With key appointments on trade in place, the 2017 USTR trade policy agenda published, and some initial actions taken, the indicators of the likely priorities of the administration are coming into focus. In addition, there are domestic and international legal, political and economic constraints that will further narrow the likely path for Trump’s policy on trade.

Although the constitution gives the president the authority to negotiate treaties and international agreements (with the consent from the Senate), Congress has the power to regulate foreign trade and thus plays a key role in trade policy.38

In terms of striking new trade agreements, Trade Promotion Authority (TPA) – a legislative process enacted by Congress – allows the executive to negotiate based on congressional guidelines.39 TPA thus involves a specific delegation of power for a limited time. Once the president (or usually the USTR) has successfully negotiated an agreement, Congress considers legislation to approve and implement it under expedited legislative procedures, with a simple up or down vote with no amendments. The most recent Trade Promotion Authority Act was signed into law in 2015, and can be used by the Trump administration until 1 July 2018 (with a possible extension until 1 July 2021).

If Trump wants to restrict trade, however, the constraining power of Congress is much more limited. Numerous statutes enacted since the Second World War give the president the power to impose tariffs and quotas on imports, for instance: to strengthen national security; to deal with a large and serious balance-of-payments deficit; or to retaliate if a foreign country denies the US its rights under a free-trade agreement or ‘carries out practices that are unjustifiable, unreasonable, or discriminatory’.40 This would allow Trump to implement some of his campaign pledges without approval from Congress; and, indeed, President Trump has already started to invoke some of these statutes.

It is generally believed that the president does not need congressional consent to withdraw the US from a free-trade agreement.41 For example, subject to six months’ written notification to the other parties, Trump could terminate NAFTA. This could be the option taken if the existing agreement cannot be renegotiated to the satisfaction of the administration. However, any process of renegotiating a trade agreement – currently under way in the case of NAFTA – has to involve Congress.

Given the current Republican majorities in both the Senate and the House of Representatives, President Trump should in theory find it easier to get congressional support for his trade policy than did President Obama in his final years in office. The balance of control could change after the mid-term elections in 2018, but even before then political divisions within the Republican Party could lead to Trump’s trade agenda being challenged in Congress.

Trump’s antipathy to trade exposes a split within the Republican Party, which has – in line with its pro-business attitude – largely been committed to promoting a free-trade agenda since the end of the Second World War. Notably among the leading Republicans in Congress, House Speaker Paul Ryan and Senate Majority Leader Mitch McConnell are free-traders, and were instrumental in securing Republican support for the 2015 Trade Promotion Authority Act. Without their support for TPA – which helped to pave the way for the conclusion of the TPP – President Obama would not have been able to advance his trade agenda, particularly because his fellow Democrats largely voted against the measure. Congressional Republicans vehemently opposed most of Obama’s initiatives, but Ryan and McConnell’s willingness to sidestep partisanship in order to advance trade liberalization suggests that they may not automatically help Trump down a protectionist path.

Trump’s antipathy to trade exposes a split within the Republican Party, which has – in line with its pro-business attitude – largely been committed to promoting a free-trade agenda since the end of the Second World War.

Although Trump may try to tap into the anti-trade sentiment within his voting base and use this to pressure Republicans in Congress to fall in line, with all seats in the House of Representatives and 33 of the 100 Senate seats up for renewal in 2018, Republicans will likely prioritize constituency interests over those of the president. For instance, it was reported in July 2017 that a group of Republicans first elected to the House in 2016 had sent a letter to the USTR, Robert Lighthizer, expressing their concern about the potential damage to US businesses, farmers and workers of Trump’s trade policies – particularly withdrawal from NAFTA. The 32 signatories, 27 of whom represent parts of the US that voted for Trump in the presidential election, warned that the US risks falling behind as other countries negotiate trade agreements and expand access for their own industries.42

In anticipation of the 2018 mid-term elections, Senate Democrats have unveiled trade proposals as part of their ‘Better Deal’ agenda. The ‘Better Deal for Trade and Jobs’ emphasizes that US trade policies ‘are not working for many working families and small businesses’, and pledges to ‘crack down on foreign countries that manipulate trade rules and penalize corporations that outsource American jobs’.43 Thus, at least in terms of rhetoric, Trump has more in common on trade with congressional Democrats than with Republicans. But while this means that Democrats could align with the president on trade, the wide differences in other policy areas mean that such cooperation is unlikely to materialize.

How Trump’s trade policy will play out will also depend on who within the cabinet and the wider administration will have his ear, and how well the various agencies involved in trade policy work together.

Trump’s appointments for key positions on trade matters seem to be cut from the same cloth. USTR Robert Lighthizer, Commerce Secretary Wilbur Ross and Peter Navarro, director of the newly established Office of Trade and Manufacturing Policy (OTMP), all regard the US trade deficit as a major problem, hold protectionist attitudes and view China’s trade practices with particular concern.

Nonetheless, this unity could be undermined by rivalries stemming from duplication and overlap of interests as well as competing policy processes.44 Making trade policy has always involved numerous agencies, with the Office of the USTR at the heart of the process, and President Trump has added further complexity with the insertion of the OTMP.45 Its defined responsibilities – inter alia to ‘advise the President on innovative strategies and promote trade policies consistent with the President’s stated goals’, and ‘serve as a liaison between the White House and the Department of Commerce’46 – could lead to a turf war with the Office of the USTR, which is responsible ‘for developing and coordinating U.S. international trade, commodity, and direct investment policy’.47 However, the limited staff of the OTMP, as well as recent reports that it is now housed within the National Economic Council, suggest that its function will be more restricted. In addition, Trump has expanded the role that the commerce secretary will have in trade policy, including being a key player in the talks with Mexico and Canada on renegotiating NAFTA.48

Congress may, moreover, become stuck in the middle of this struggle for dominance between the Office of the USTR, the Department of Commerce and the OTMP. Expertise for negotiating trade agreements sits largely within the Office of the USTR, and the House Ways and Means Committee and the Senate Finance Committee (the congressional entities with jurisdiction on trade policy) will likely insist that the negotiating function remains with the USTR so that these two committees can continue to exercise oversight. The Department of Commerce is accountable to different committees, and the OTMP is not subject to regular congressional oversight.

Another potential contributor to an internal clash over trade is the faction of committed free-traders in the cabinet – most prominently Vice-President Mike Pence and Secretary of State Rex Tillerson. While they are not the central players when it comes to trade policy, they could influence – or seek to influence – objectives in this area.

Cabinet members will also have to work with – or potentially against – a close circle of advisers in the White House. Gary Cohn, director of the National Economic Council, has notably emerged as an important figure. Jared Kushner, Trump’s son-in-law and senior adviser, and Jason Greenblatt, Special Representative for International Negotiations, were initially regarded as having a say on trade policy as well, but have since focused on other areas.

So far, the hardliners on trade issues have been sidelined. An executive order to withdraw from NAFTA – which had reportedly been drafted by OTMP head Peter Navarro and the then White House chief strategist Steve Bannon – was in the end not signed by Trump after more moderate trade voices intervened.49 Bannon’s departure from the White House apparently tips the balance in favour of the globalists on Trump’s trade team. Moreover, with the OTMP now reportedly part of the National Economic Council, the trade nationalist Navarro would have to report to globalist Cohn – a sign that the former’s influence is being further reduced.

Commerce Secretary Ross was initially in the driver’s seat on US trade policy in the early months of the Trump administration, but with the confirmation of Robert Lighthizer as USTR in May 2017 the primary official in charge of trade policy is now in place. However, key appointments in the Office of the USTR (including the deputy ranks) have yet to be confirmed, and this will likely slow the pace of action on trade.

President Trump has promised to jump-start the US economy and return it to 4 per cent annual growth. He has also pledged to create 25 million new jobs over the next decade.50 Some of his proposals, such as tax reform and cuts, or infrastructure spending, could stimulate the economy if they are moved forward, although probably not to the degree vaunted by the president.

According to many of those who are sceptical of Trump’s ambitions for the US economy, his protectionist trade proposals are likely to act as a drag on growth by raising the cost of imports, discouraging exports, hampering innovation and creating uncertainty for businesses. It is highly probable that businesses and citizens in sectors of the economy and in regions of the US that will be most severely affected will speak out against protectionism in US trade policy.

The administration will need to achieve a careful balance between its ambitions for growth and the economic implications of a protectionist agenda.

The administration will thus need to achieve a careful balance between its ambitions for growth and the economic implications of a protectionist agenda, as well as the often competing demands of various stakeholders.

One of the critical factors influencing Trump’s success in the 2016 presidential election was his ability to tap into the frustrations of voters who felt left behind by globalization and trade. He has promised to address these voters’ grievances, and their continued support will largely be contingent on whether he is perceived as delivering on these promises. But it is very unlikely that Trump’s trade policy will be able to meet the needs and expectations of this constituency in full. Despite his campaign pledges to reduce the trade deficit, rip up bad deals and get tough on countries that do not play by the rules, these measures will not in practice bring many manufacturing jobs back to the US. Moreover, many of his campaign proposals for trade policy, such as raising tariffs, would primarily hurt a large number of the disenchanted constituencies who brought him to power. Those on modest incomes spend a much larger proportion of their pay on goods that are imported, such as footwear and clothing, and higher tariffs would mean that the prices of these goods would increase for consumers.

Trump’s trade policy – even though it was a central part of his campaign – cannot thus be at the heart of the solutions to accommodate the grievances of these same voters. Other policies regarding healthcare, tax reform and infrastructure will be more central. In practice, if not in rhetoric, therefore, if the administration is to move these initiatives forward, the trade agenda may need to be played down.

Repealing and replacing President Obama’s Affordable Care Act, tackling tax reform and launching a $1 trillion infrastructure plan have emerged as the key legislative priorities for Republicans.51 This ambitious agenda will require significant efforts to build a party-wide consensus among Republicans in Congress, as they have latterly shown themselves to be not all on the same page when it comes to reforming healthcare, and will not all support the ballooning deficit and debt trajectory that the tax and infrastructure plans could give rise to. Moreover, progress towards these objectives has been slow in a Congress preoccupied by the ongoing controversies and investigations concerning a possible collaboration between the Trump campaign and Russia. In this context, it is unlikely that President Trump will try to implement some of his more provocative trade policy objectives; these would risk a further rift within the Republican Party and undermine the advancement of his other policy priorities.

Consideration of how various policy plans interact may also serve to constrain Trump’s trade agenda. For instance, if the US was to withdraw from NAFTA, the Mexican economy would likely enter a severe downturn, thus increasing the incentives for Mexicans to migrate to the US. This would create a situation at odds with Trump’s goal of reducing immigration. And his economic stimulus plan is widely considered as an initiative that would cause the dollar to strengthen. This would make US exports more expensive and imports cheaper, thus frustrating Trump’s stated objective of narrowing the trade deficit.

In short, the Trump administration will have to weigh its policy priorities and their intended and unintended consequences, which points to the probability that a more moderate trade policy agenda will emerge.

There are certain international constraints that will temper the president’s ability and willingness to pursue his trade promises. As a member of the WTO, the US is guided in trade policy by the organization’s rules and decisions. Thus, for instance, the imposition of across-the-board and/or unilateral tariffs on imports from Mexico or China would be inconsistent with WTO rules. And if the Trump administration was to impose tariffs, other countries could retaliate. China has already identified US companies and industries that it would target – including Boeing, Apple and soybean producers – in a tit-for-tat approach.52 Although increasingly unlikely at present, whether a trade war between the US and China does eventually materialize will depend not only on US actions, but also on China’s reaction.

While ‘China-bashing’ was a core theme of Trump’s presidential campaign, since taking office he has adopted a much more measured stance, in part because of national security considerations. Notably, for example, the president has latterly stepped away from his campaign pledge to name China a currency manipulator on ‘day one’ of his administration, aiming instead to get Beijing’s support in dealing with the growing nuclear threat from North Korea.53

Although President Trump has the authority to withdraw the US from NAFTA, a renegotiation of the agreement requires the willingness of Mexico and Canada to come back to – and remain at – the table. So far, all sides are ready to engage, with negotiations having got under way in August 2017. With a general election due in Mexico in July 2018, its government has been keen to wrap up the NAFTA renegotiation process before the end of 2017,54 although – as noted below – progress hitherto suggests that this ambition is now unrealistic. Despite all the focus on the Trump administration’s threats to scrap NAFTA, Mexico and Canada could also walk away from the negotiating table if their own red lines are crossed. Mexican and Canadian officials are also exploring areas of mutual interest on which they can collaborate to strengthen their position vis-à-vis the US.55

Trump’s trade plans and actions so far have raised questions about the US’s reliability as a partner and international leader in the trade arena, which could prompt its rivals and allies alike to assume a greater role themselves. In the wake of the US withdrawal from the TPP, China has been only too willing, via initiatives such as the Regional Comprehensive Economic Partnership (RCEP), to move into the void left in the Asia-Pacific region. The EU has also signalled that it will work to advance trade talks around the globe, including with TPP countries.56 These efforts are already bearing fruit, with the EU and Japan having reached an agreement in principle on the main elements of a bilateral trade agreement in July 2017.57 In this shifting international context, the Trump administration may come to realize that the US risks falling behind as other countries take a more prominent role in advancing trade liberalization.

Even if President Trump is less than willing to engage in international forums such as the G20, he will still have to work with a G20 trade consensus that has traditionally resisted protectionism. US dissent meant that G20 finance ministers struggled, at their meeting in March 2017, over the wording of the customary statement opposing all forms of protectionism. By the time of the G20 leaders’ summit in Hamburg in July, however, the US position had softened to some degree,58 thus easing the path to agreement on a common statement. The leaders at the G20 summit in Hamburg recommitted themselves to ‘keep markets open’ and ‘continue to fight protectionism’.59 All the same, in an apparent nod to the concerns of the Trump administration, compromise language acknowledged the ‘importance of reciprocal and mutually advantageous trade and investment frameworks’, as well as the role of legitimate trade-defence instruments in tackling unfair practices.60 On balance, language on trade at the outcome of the Hamburg summit was remarkably robust.

While it is not yet possible to pinpoint the precise direction – in particular the degree of retreat from free trade – that the Trump administration will take in its trade policy, it is already clear that the US will no longer be taking a leadership role in pressing for new free-trade agreements and multilateral rules that set standards for a global system. It is also more than likely, given the constraints set out above, that Trump’s trade policy will be less radical in its execution than was signalled in his campaign-trail rhetoric.

Indeed, during Trump’s early months in office, the sole definitive action on trade was the decision to withdraw from the TPP.61 He did not, as promised during the campaign, designate China a currency manipulator on ‘day one’; nor did he take any action to impose across-the-board tariffs on imports from China and Mexico. He signed a number of trade-related executive orders, mostly to commission the study of the source and consequences of perceived problems such as the US’s bilateral trade deficits or violations of trade agreements by partners abroad, but the deadlines for reports have so far been missed. The NAFTA renegotiation is now notably under way. But it remains to be seen how different US trade policy will be as a result of these initiatives.

The 2017 USTR trade policy agenda sets out the principles that will drive US actions. The overarching objective is ‘to expand trade in a way that is freer and fairer for all Americans’.62 The trade agenda is directed at, inter alia, increasing economic growth, creating jobs, and promoting reciprocity with trading partners. Reducing the trade deficit, enforcing existing agreements and tackling perceived unfair practices will be central elements of the administration’s trade actions. Thus, while the Trump administration is not against free trade per se, it will follow a more protectionist path than its recent predecessors.

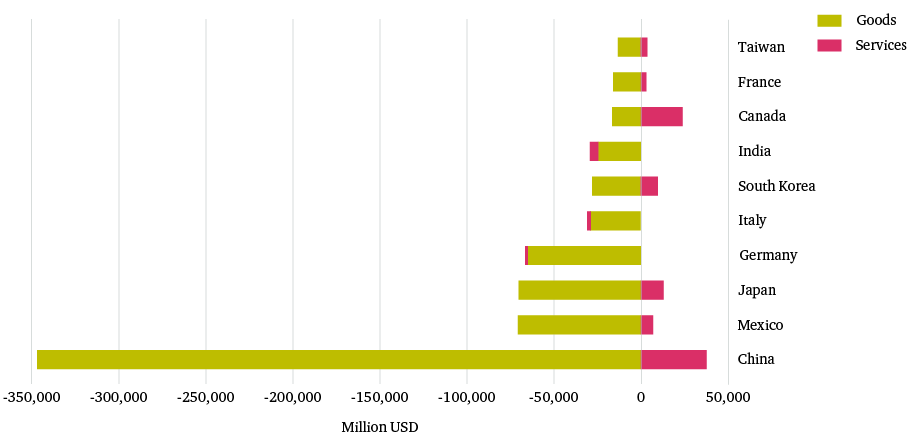

When the Trump administration bemoans the US trade deficit – the world’s largest over four decades63 – it is almost exclusively focused on trade in goods. The trade deficit in goods and services stood at $505 billion in 2016, but whereas the trade deficit in goods amounted to $753 billion, this was partially offset by a surplus in services.64

The countries with which the US runs the largest merchandise trade deficits are under scrutiny: an executive order in March 2017 initiated a review of the US trade deficit with key countries,65 among them China, Germany, Mexico and Japan (see Figure 2). China and Mexico were singled out by Trump on the campaign trail; and since his inauguration Germany and Japan have also been targeted for alleged unfair trade practices that contribute to their large merchandise trade surpluses with the US. Peter Navarro, now head of the OTMP, has accused Germany of exploiting the euro for its own trade gains,66 while President Trump has taken to Twitter to denounce Germany’s trade surplus.67 Trump has also held Japan responsible for hampering automobile imports from the US through unfair trade practices.68 Trade issues will always be on the agenda during meetings between the Trump administration and representatives of the countries concerned, and could become a major sticking point in bilateral relationships if progress is not made to the satisfaction of the former.

A US–Chinese trade war has been avoided thus far. At their meeting held at Mar-a-Lago, Florida, in April 2017, Presidents Trump and Xi Jinping agreed to develop a 100-day trade action plan,69 but the dialogue had produced few concrete results by the time the deadline passed in mid-July. The US and China did reach a deal in May on trade in certain agricultural products, financial services and energy.70 Since then, however, little further progress has been made; and ongoing differences over China’s excess capacity in the steel sector and cheap imports that allegedly hurt the American steel industry suggest that this and other tensions over trade will continue to loom large in the bilateral economic relationship.71

The US maintains a free-trade agreement with only two of the 10 countries with which it has the largest bilateral merchandise trade deficits (Mexico and South Korea). The bilateral deficits result from structural factors, and are magnified by supply chains and the ways in which trade is measured.

The Trump administration’s focus on bilateral trade deficits is misguided. While the total US trade deficit matters, it is largely due to macroeconomic forces (driven by savings and investment) and not trade policy.72 The US maintains a free-trade agreement with only two of the 10 countries with which it has the largest bilateral merchandise trade deficits (Mexico and South Korea). The bilateral deficits result from structural factors, and are magnified by supply chains and the ways in which trade is measured.73

In this context, it is unlikely that the emphasis on narrowing the trade deficit, especially through bilateral efforts, will produce the desired outcome. More probably, the deficit will continue to widen (also given a projected stronger dollar if the administration’s planned fiscal policies are implemented). It can be expected, therefore, that the US will pursue a few high-profile actions that seemingly address the trade balance (such as current initiatives to impose tariffs on steel imports) in an effort to distract attention from a deficit that is widening overall.

Instead of withdrawing the US from existing free-trade agreements, the Trump administration is more likely to renegotiate them if US goals are perceived as not being met. And given Trump’s focus on NAFTA during the election campaign, the agreement with Mexico and Canada – in force since 1994 – is firmly at the top of the list for renegotiation.

Calls for the renegotiation of NAFTA – including by Barack Obama and Hillary Clinton during the 2008 election campaign – are nothing new. President Obama in a sense delivered on this undertaking through the conclusion of the TPP negotiations, which would have updated many parts of the US’s trade relationship with its NAFTA partners. With the NAFTA renegotiations now under way, if done right, the US once again has the opportunity to upgrade its trade relationship with Mexico and Canada.

In May 2017 the Trump administration formally notified Congress of its intention to renegotiate NAFTA, thereby initiating a 90-day consultation period.74 In July it provided a summary of objectives for the negotiations.75 While some goals (such as reducing the US merchandise trade deficit with Mexico and Canada) are notable hallmarks of the Trump administration, others (such as measures to upgrade labour and environmental standards, address the regulation of state-owned enterprises, and incorporate governance rules for digital trade and cross-border data flows) echo provisions of the TPP.76

For the most part, the US objectives for the NAFTA renegotiation are rather vague. As currently set out, some may be agreed relatively easily, while others will be far more contentious. In particular, eliminating the dispute settlement section dealing with anti-dumping and countervailing duty matters (referred to as Chapter 19), focusing on the bilateral trade balance, and reducing or eliminating barriers for US agricultural exports will likely become sticking points. Rules of origin in the auto industry are also poised to be a highly charged issue. Reported US proposals to include a ‘sunset clause’, which would allow NAFTA to be terminated after five years unless all parties agree to renew it, could further heighten the tension.77

The negotiations, which began in August 2017, have already exposed some of these differences between the three parties. Despite the common ambition to conclude the process quickly – especially Mexico’s stated aim to wrap up well before its elections due in July 2018 – it seems more likely that the renegotiation will be drawn out beyond the US mid-term elections in November that year. In light of stalled progress during the first four negotiating rounds, the talks are indeed already delayed and have been extended into the first quarter of 2018.78

Mexico and Canada seem willing thus far to agree to modest changes to NAFTA, but it is unlikely that they will accept the introduction of new trade barriers. The US, for its part, may be prepared to withdraw from the agreement if it cannot secure a favourable renegotiation, but this seems unlikely in the face of lobbying against such a move by businesses and members of Congress in potentially adversely affected US states.

Although the NAFTA renegotiation will be the priority for the Trump administration in terms of revising existing trade deals, the US–Korea Free Trade Agreement (KORUS) will likely be next on the list. The US and South Korea held special meetings of the KORUS Joint Committee in August and October 2017 to consider ‘needed amendments’ to the current agreement.79 A key point of concern for the US is that its merchandise trade deficit with South Korea has almost doubled since KORUS came into force in 2012, and the Trump administration wants to remove barriers to US market access.

The prospects for the TTIP and TiSA negotiations under the Trump administration are uncertain. Although Trump did not single these out on the campaign trail, and the 2017 USTR trade policy agenda states that the administration is ‘currently evaluating the status of the negotiations’,80 they are unlikely to advance in the near future. To a large degree, this reflects the current administration’s stated preference for bilateral over mega-regional or multilateral trade agreements.

TTIP, as a bilateral arrangement between the US and the EU, would technically fit with this preference. Trump’s key advisers initially regarded it as, in Navarro’s words, ‘a multilateral deal in bilateral dress’,81 but have since come to the realization that negotiations must be conducted at EU level and not with individual member states.82 Even though Commerce Secretary Wilbur Ross has put the possibility of reviving trade negotiations with the EU back on the table, it is highly unlikely that this will happen anytime soon. EU Trade Commissioner Cecilia Malmström has publicly acknowledged that the negotiations will remain on hold for some time, and has also emphasized the EU’s need for time ‘to evaluate and reflect’.83

Moving TTIP forward would require a substantial commitment of political capital from the US and the EU, but, given its other priorities, it does not seem that the Trump administration will commit time and effort to TTIP in the foreseeable future. And even if the negotiations are resumed, there will be substantial hurdles to overcome. In particular, given the president’s focus on ‘Buy American’, it is unlikely that his administration would be willing to give in to the EU’s demand on market access in government procurement.84 The recognition and protection of geographic indications – another issue that emerged as a sticking point well before Trump’s election – could also be expected to resurface.

The TiSA negotiations, although close to completion by late 2016, are now on hold. There is some chance that the negotiations could progress, not least because the US maintains a trade surplus in services. However, given both the Trump administration’s focus on reducing the trade deficit in goods and curtailing imports of manufactures, and the complexity of the TiSA negotiations involving (currently) 23 parties, the prospect of an early revival appears slim.

The age of negotiating mega-regional trade deals seems over, but it remains to be seen whether the Trump administration will pursue any new trade negotiations.

The age of negotiating mega-regional trade deals seems over, but it remains to be seen whether the Trump administration will pursue any new trade negotiations at all. If it does, it is clear that these will be on a bilateral basis. Trump and his advisers see bilateral deals as easier and quicker to negotiate than regional or multilateral arrangements, and they consider that the US gets, in Wilbur Ross’s phrasing, ‘picked apart’, country by country, in multilateral negotiations.85 In terms of potential new trade deals, the administration has expressed an interest in pursuing trade agreements with the UK and with Japan. There would be significant hurdles in both instances, however.

That the UK cannot formally begin negotiating trade matters while it remains a member of the EU precludes a quick bilateral deal for the Trump administration. Moreover, the terms of the post-Brexit arrangement between the UK and the EU will influence to what extent the former is able to set its own tariffs and determine regulations bilaterally. Until a UK–EU deal is finalized, US negotiators will not know how valuable access to the UK market is likely to be, making even informal talks difficult. Thus, negotiations for a discrete US–UK trade agreement may proceed only towards the end of the current presidential term. Some US officials even put the EU ahead of the UK in terms of striking a trade deal.86

A potential US–Japan free-trade deal could therefore move to the front of the queue; and could in theory be completed quickly, using the TPP as a blueprint. But, rather than repurposing what was agreed in the TPP, the administration will likely push for additional concessions, particularly concerning better market access for US automobiles and agricultural products such as beef. Addressing the large trade deficit with Japan would likely be a focal point of the negotiations, further complicating talks. The prospects for a rapid deal are thus uncertain here too.

Enforcement of existing trade agreements, as well as responding to perceived unfair trade practices (such as dumped or subsidized imports, theft of intellectual property rights, or currency manipulation), will be a major priority for the Trump administration. The 2017 USTR trade policy agenda emphasizes that the US will break down ‘unfair trade barriers in other markets that block U.S. exports’, while ensuring that all US trade laws are ‘strictly and effectively enforced’.87

The US can take some unilateral actions under domestic law, and the Trump administration will likely make increased use of established trade remedies that are already frequently employed, including anti-dumping and countervailing duty laws, probably in a more aggressive fashion. According to recent practice, the Department of Commerce initiates an anti-dumping or countervailing duty investigation after a domestic interested party files a petition. More rarely, as happened mostly in the 1980s, investigation is also possible at the Commerce Secretary’s own initiative.88 Wilbur Ross’s remarks during his confirmation hearing in January 2017 suggested that the Department of Commerce will self-initiate more investigations under the present administration.89

The Trump administration will also be inclined to invoke – and to self-initiate investigations under – less commonly used US laws in order to take unilateral actions. Indeed, the administration has already done so three times. In April 2017 it self-initiated two separate investigations under Section 232 of the Trade Expansion Act of 1962, on the grounds that imports of steel and aluminium pose a threat to national security.90 And in August it self-initiated an investigation under another rarely used trade law (Section 301 of the Trade Act of 1974), examining whether China’s handling of technology transfer and intellectual property ‘are unreasonable or discriminatory and burden or restrict U.S. commerce’.91

Despite Trump’s campaign rhetoric – particularly his undertaking to designate China as a currency manipulator on ‘day one’ – cracking down on currency manipulation will in reality be less of a focus for his administration. Treasury Secretary Steven Mnuchin has been seen to take a much more moderate approach. In the Treasury’s 2017 April and October reviews of foreign-exchange markets, China was not classed as a currency manipulator, although it continued to be included (along with Japan, South Korea, Germany and Switzerland) on the ‘Monitoring List’ of major trading partners that merit close attention to their currency practices.92 Even if the Treasury identifies China as a currency manipulator in the future, current laws do not authorize the imposition of countervailing duties. The Treasury would be able to initiate ‘enhanced bilateral engagement’, and the president could take subsequent steps, only if China does not adopt appropriate policies within one year of designation.93

The administration is also expected to bring more cases at the WTO, particularly against China. Although Trump pointed to a potential US withdrawal from the WTO on the campaign trail, this is highly unlikely in reality, given constraints ranging from the prospect of severe market reaction and congressional resistance at home to opposition from other countries. With Robert Lighthizer – a long-time trade attorney who previously served under the Reagan administration – as the USTR, the US will remain in the WTO as a more combative member. During his confirmation hearing in March 2017, Lighthizer stated that he would bring as many trade enforcement actions as are justified under WTO rules, bilateral trade agreements and US law.94 Compared with his predecessors, he will be more focused on trade enforcement rather than trade liberalization. In addition to initiating cases, Lighthizer is likely to push for reform of the WTO’s dispute settlement process.95

The 2017 USTR trade policy agenda states that the administration will not be bound by WTO rulings that ‘undermine the ability of the United States and other WTO Members to respond effectively to these real-world unfair trade practices’.96 In other words, if a WTO panel or appellate body finds the US to be in violation of its obligations, US law or practice will not automatically be changed. This would have implications for the WTO as a forum for dispute settlement.

A central campaign pledge made by Trump was to reverse the trend of US companies offshoring jobs – particularly in manufacturing – to other countries. As president-elect, he threatened to penalize offshoring companies with a 35 per cent tariff on imports of products for sale back in the US.97 Such a disincentive would encounter significant opposition from industry.

A central campaign pledge made by Trump was to reverse the trend of US companies offshoring jobs – particularly in manufacturing – to other countries.

Beyond trade policy – and even before Trump’s victory in 2016 – the idea of a border tax adjustment has also been floated to deter offshoring. In June 2016 House Speaker Paul Ryan and House Ways and Means Committee Chair Kevin Brady called for border adjustments as part of a wider reform of the tax code. According to their plan, a 20 per cent business tax would replace the current 35 per cent corporate income tax, and a destination-based tax system would replace the current worldwide tax system. The border tax adjustment would be implemented through a tax on imports (by denying business deductions for imports) and a rebate to exports (by excluding export revenue from a company’s tax base).98

Faced with significant opposition, however, the White House and congressional leaders decided in July 2017 to set this controversial plan aside in the interests of advancing broader tax reform efforts.99 While the border tax adjustment would have raised significant revenues and reduced the incentive for US multinational corporations to shift their production abroad to take advantage of lower foreign tax rates, it may not have helped to address the trade deficit.100 Numerous questions were raised about the compatibility of the border adjustment tax with WTO rules. The plan also drew strong opposition from parts of the business community: importers such as Wal-Mart and Nike notably lobbied against it.101