Chatham House exterior.

In the first of a new annual series, Chatham House experts examine how aspects of the established order in global affairs are shifting.

Risks and Opportunities in International Affairs

Chatham House report

Published 19 June 2018

Updated 15 February 2023

ISBN: 978 1 78413 285 9

Chatham House exterior.

In the first of a new annual series, Chatham House experts examine how aspects of the established order in global affairs are shifting.

The 2008 financial crisis made two facts about the global financial system inescapably clear. First, risk had become so concentrated that the failure of any one of several large financial institutions could significantly harm the real economy. Second, financial markets had become so interconnected that poor regulation in a single jurisdiction could have global implications. To combat these challenges, the international community – primarily through the G20 – developed an ambitious set of reforms designed to both prevent contagion and ensure that major financial institutions worldwide maintained similar, robust standards. However, as memories of the crisis begin to fade, momentum for greater international coordination is ebbing.

There are three main reasons why this process is stalling, and in places going into reverse. The first is simply fatigue. There was, in retrospect, a surprising amount of agreement and ambition across the G20 on unified principles for financial regulation. This regulatory push lasted from 2009 – when the G20 established the Financial Stability Board (FSB) to coordinate the reform process – until roughly 2015, and covered an incredibly broad agenda, including how banks hold capital and weigh risks, how derivatives are traded, how too-big-to-fail banks should be structured, and numerous other issues.169 However, progress inevitably slowed once the risk of financial collapse became less acute and reforms with broadest support were implemented.

Second, regulatory cooperation was almost all accomplished through consensus among G20 and FSB members, rather than through any binding system of obligations. The process was designed to be self-reinforcing – reliant on peer review170 but with no penalties for non-compliance.171 It could only be effective as long as there was political buy-in, particularly from larger economies.

While all regulation imposes compliance costs, the increased financial stability that comes with coordinated regulation makes it beneficial in net terms. Divergence has no such trade-off

Finally, domestic political drivers have started to erode that buy-in. In an environment in which policy fatigue has developed and cooperation is entirely voluntary, pressure from lobbyists and politicians can easily accumulate.

The degradation of the regulatory climate looks different from one jurisdiction to another. There are some examples of major prudential regulation being rolled back, most significantly in the US. In May, President Donald Trump signed into law a bill raising the size thresholds above which banks are subject to certain macroprudential regulations, and reducing the frequency and rigour of ‘stress tests’.172 Additionally, the Trump administration plans to limit use of the Financial Stability Oversight Council. This key piece of the Dodd–Frank reforms is responsible for designating financial institutions as ‘systemically important’ and therefore subject to increased oversight.173

Most changes are more benign in isolation. However, the problem is that different jurisdictions are increasingly seeking to manage financial risks through divergent, often incompatible, processes. This harms multilateral coordination. For example, the Basel Committee on Banking Supervision had to delay finalizing its latest round of standards by over a year174 due to a dispute between US and EU banks. Even now, the standards have seen their implementation delayed until 2020, do not cover all relevant issues175 and may not ever take effect in EU law.176

These trends imply several undesirable consequences. While all regulation imposes compliance costs, the increased financial stability that comes with coordinated regulation makes it beneficial in net terms. Divergence has no such trade-off: it costs the financial system over $780 billion a year177 and harms financial stability. Because cross-border compliance costs are more easily borne by larger institutions, divergence incentivizes consolidation – and thus, perversely, concentration of risk – while creating opportunities for regulatory arbitrage. Meanwhile, as regulators adopt less uniform supervisory standards, it becomes harder for them to monitor global risks, or cooperate in a crisis.

Finally, Brexit deserves special mention. London has one of the world’s most interconnected financial sectors, hosting globally significant exchanges and clearinghouses that require specialized regulation. The IMF has recognized the UK regulatory system as a ‘global public good’,178 a designation that implies far-reaching spillovers if the system is inadequate. If Brexit creates significantly more complex regulations for EU/UK financial transactions, or forces complex transactions into jurisdictions with less experienced regulators, it is likely to create global risks.

Moving away from a coordinated regulatory agenda will not necessarily cause a crisis next year, or in any given year. However, in an environment of new potential risks to financial stability – cryptocurrencies, tightening monetary policy, a still-significant global debt overhang, populism – a well-functioning global crisis-response capacity is ever more important. International coordination and trust between governments and regulators remain vital for this, and any weakness in the system designed to foster such cooperation will limit its ability to respond to emerging risks – or to deal with the next crisis.

Matthew Oxenford is a research associate with the Global Economy and Finance Department.

Ten years after the financial crisis, most advanced economies are still struggling to get their public finances under control. The burden of adjustment has fallen most heavily on individuals, especially the less well-off, while multinational companies have seen their profits surge, but their tax bills shrink. The resultant rise in inequality has contributed, among other factors, to the popularity of extreme political movements in many countries.

Companies, especially those operating multinationally, have been very successful at minimizing their global tax bills. Partly, they have done this by booking profits in low-tax jurisdictions, but they have also exploited the loopholes created by the reluctance of countries to harmonize their tax regimes.179 However, recent US tax reforms, while providing a temporary windfall for companies, have also removed one of the biggest obstacles to international tax harmonization. If other countries follow this lead, it could provide the opportunity for substantial progress in aligning international tax policies, and give a boost to tax receipts from companies.

Global revenue losses from tax avoidance could be as high as $650 billion according to the IMF

The IMF estimates that corporate income tax rates in advanced economies have declined from 50 per cent in 1980 to 25 per cent in 2016.180 Global revenue losses from tax avoidance could be as high as $650 billion. Public attention has been concentrated by controversies over the tax strategies of multinationals such as Apple, Amazon and Google. For example, the European Commission has taken Ireland to the European Court of Justice in order to force the country to recover from Apple up to €13 billion in what the Commission considers illegal tax benefits.

While high-profile legal challenges make headlines, a systematic approach to getting companies to pay more tax needs to address differences in corporate tax regimes and definitions across countries. If countries adopt broadly the same rules, and companies’ earnings are treated in broadly similar fashion wherever they operate, the scope to seek loopholes is in theory reduced. This can only be achieved by international cooperation, however.

To date, this has been hampered by the fact that countries jealously guard their ‘sovereignty’ over tax policy. Even in the EU, only limited progress has been made on tax harmonization, and tax issues are still decided by unanimity rather than qualified majority voting. Countries also continue to offer companies favourable tax treatment to attract the investment and jobs they bring. In the UK’s 2016 budget,181 for example, Chancellor George Osborne announced that the main rate of corporation tax would be cut from 20 per cent to 17 per cent by 2020, taking it to the lowest level in the G20. Most significantly, the US has always been an outlier, taxing worldwide profits of all US-based corporations, no matter where those profits are earned. This has created a huge incentive for corporations to shift profits into non-US vehicles in lower-tax jurisdictions, and to exploit offsets and allowances such as on intra-company interest payments.

In 2013 the G20, at its St Petersburg summit,182 recognized the need to tackle tax avoidance and protect revenue bases. To that end it commissioned the OECD to work on ‘base erosion and profit shifting’ (BEPS). Working on the principle that profits should be taxed where they are generated, the BEPS programme183 was designed to reduce the ability of multinationals to shift profits between jurisdictions or artificially reduce tax liabilities, for example by manipulating capital allowances.

But despite regular commitments by G20 members to implement the 15 agreed BEPS actions, peer review mechanisms are only now being put in place to monitor compliance. Without high-level political commitment, progress will remain slow and hampered by national interests. In particular, the US has tended to see any moves against the aggressive tax avoidance strategies of US multinationals as an attempt to erode their competitive advantage.

The US tax reforms provide an unparalleled opportunity to make substantial progress on international tax harmonization

That, however, may be changing. During the 2016 US presidential campaign, Donald Trump criticized multinationals for moving production capacity from the US to lower-cost countries, and threatened penalties. And in December 2017, the Trump administration passed a tax reform package. This gave a generous tax cut to corporations, lowering the main tax rate from 35 per cent to 21 per cent, and provided a temporary tax break for capital spending.184

However, the reforms also represent a significant shift in the overall design of US corporate tax policy. First, they exempt US corporations from US taxes on most future foreign profits, thus ending the present worldwide system of taxing profits wherever they are earned. This would align the US tax code with practice in most other industrialized nations, and was judged by Thomson Reuters to ‘undercut many offshore tax-dodging strategies’.185

Second, a new levy on global intangible low-taxed income (the ‘GILTI tax’) is likely to increase the rate paid by companies with high foreign earnings in low-tax jurisdictions, and provide an incentive for US companies to repatriate profits. In addition, a one-off levy on past profits held offshore will hit multinationals with large cash pools abroad.

Finally, measures to counter base erosion will prevent companies from shifting profits out of the US to low-tax jurisdictions abroad. An alternative minimum tax will apply to payments between US corporations and foreign affiliates. There will also be limits on shifting corporate income through transfers of intangible property, including patents. Thomson Reuters views this combination of measures as representing ‘a dramatic overhaul of the US tax system for multinationals’.186

These reforms move the US significantly towards the approach adopted by most other countries, and so provide an unparalleled opportunity to make substantial progress on the international agenda for tax harmonization.

It is now for other G20 countries to take up this opportunity to breathe new life into the BEPS agenda. Firstly, the OECD should be commissioned to identify all areas in which each G20 country fails to meet the 15 BEPS actions. Secondly, countries should be challenged to act on these issues within a fixed timescale. Finally, the G20 should continue to put pressure on offshore tax jurisdictions to meet their obligations to exchange information with other tax authorities.

The US reforms can be the catalyst for all G20 countries to take the actions they need to deliver a level playing field for multinationals: removing the substantial opportunities that these firms currently have for tax avoidance, and ensuring that they pay their fair share of tax.

Stephen Pickford is an associate fellow with the Global Economy and Finance Department.

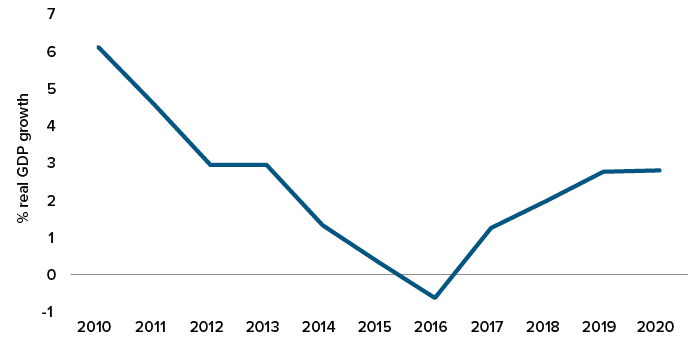

The buoyancy and confidence of the first decade of this century are no more, but Latin America is slowly recovering from the economic downturn that followed the sharp decline in commodity prices between 2012 and 2014. Regional economies expanded by a modest average of 1.3 per cent in 2017, but growth is tentatively expected to pick up further in 2018 and 2019.187 The turnaround is happening in spite of persistent political uncertainty ahead of a string of elections later this year and in 2019, and amid popular worries about corruption and rising violence and signs of social stress.188 In short, there are some signs of greater resilience – but also reminders of continuing risks to stability and growth.

A number of economies in the region did better in 2017 than in 2016, with the recovery in Brazil – which slid into its worst ever recession in 2014 – perhaps the most striking. Venezuela is an exception to recent positive developments: its newly re-elected socialist leader, Nicolás Maduro, has presided over five successive years of sharp economic decline and rising inflation, and the collapse of many public services.

For foreign investors, the regional recovery has highlighted opportunities in a number of areas. First, regional consumer markets remain much larger than they were two decades ago. The downturn made life more precarious for many Latin Americans, but on balance (at least outside Venezuela) many more people are buying consumer products as a result of the wider availability of credit and substantial reductions in both poverty and traditionally high rates of inequality.189

Second, Latin America’s natural resources – such as soya, meat, iron ore, copper, oil and gas – continue to make the region attractive to China and the more dynamic Asian economies. Brazil and Argentina are the second- and third-largest suppliers of soya to China. Chile and Peru provide a substantial share of China’s copper. Although Venezuela’s pivotal oil industry is declining very sharply, Brazil, Mexico, Colombia and Argentina are all taking steps to make their hydrocarbons wealth more accessible to foreign capital. All this is helping economic relations more generally. Last year China was the largest export market for five countries in the region – Brazil, Chile, Peru, Cuba and Uruguay – while eight countries imported more from China than they did from the US.190 Chinese investment flows into Latin America are hugely significant, helping shore up external accounts and reduce dependency on international capital markets. Asian support can also help boost much-needed investment in transport and energy infrastructure.

Recent market turbulence in the wake of US interest rate rises has highlighted the vulnerability of economies that have relatively high external and fiscal deficits

At the same time, the region’s plentiful water and record of developing sources of green energy (such as hydropower and sugar-based ethanol) represent significant comparative advantages as the world moves to reduce carbon emissions.

Several factors continue to make Latin America a risky region in which to invest, however. Recent market turbulence in the wake of US interest rate rises has highlighted the vulnerability of economies that have relatively high external and fiscal deficits – nowhere more so than in Argentina, where the pro-business and reformist government of Mauricio Macri has been forced to seek help from the IMF. Pressures are also increasing in Brazil again, in light of major industrial action. A longer-term economic issue for the entire region is low labour productivity. One particular concern is that the relatively young population is becoming older, closing the demographic window that ought to assist development.

Political and security risks also abound. Although democracy is now well established and its foundations much more solid than they were, organized crime poses a serious threat to stability in some parts of the region. Homicide rates are among the highest in the world. In Venezuela, independent institutions have almost completely collapsed, with an authoritarian and unpopular regime surviving largely by dint of Chinese and Russian support.

A wider concern is the weakness of moderate political parties and the growing unpredictability of politics in the region. Many voters are nostalgic for the hard-line security policies of the 1960s and 1970s, and deeply dissatisfied with political elites and the corruption with which they have been associated. The centre-left and centre-right parties that led the region’s return to democratic rule in the 1980s have often fared badly in recent elections, leaving the field open to populists of both left- and right-wing varieties.

A kind of right-wing populism seems well established in Peru. The party of former president Alberto Fujimori – released from prison in December last year – dominates the legislature and a few months ago forced the resignation of President Pedro Pablo Kuczynski, a pro-business conservative who had narrowly won elections in 2016. In Brazil the centre-right and centre-left parties that dominated the political stage for more than two decades have been devastated by the ongoing Car Wash (Lava Jato) corruption scandal, making the outcome of October’s elections unusually uncertain. One of the front-runners for the Brazilian presidency is a right-wing authoritarian called Jair Bolsonaro. In Mexico, the region’s second-largest economy, Andrés Manuel López Obrador, a left-wing nationalist, is well in front in polls ahead of the July 2018 presidential contest.

There have been exceptions to this trend. Under the splendidly named President Lenín Moreno, elected in 2017, Ecuador has tacked sharply to the centre, abandoning some of the policies introduced by its pro-Venezuelan former president, Rafael Correa. In Argentina, Macri’s 2015 victory ended 12 years of rule by the left-wing Peronists, the late Néstor Kirchner and his wife Cristina Fernández. Macri’s programme of gradual reform proved popular at last October’s legislative elections. However, recent market turmoil could damage his chances of securing a second term in office in polls due next year.

Inevitably, short-term turbulence and volatility will loom large in the thinking of policymakers and investors in Latin America. They should, however, perhaps take solace in more positive longer-term trends: bigger and more dynamic internal markets, attractive resource bases and – Venezuela notwithstanding – the strength of the region’s democratic institutions.

Richard Lapper is an associate fellow with the Global Economy and Finance Department and the US and the Americas Programme.

The case for increased infrastructure investment and improved connectivity in developing Asia has long been made.191 Last year the Asian Development Bank (ADB) raised its estimate of the region’s investment needs to $1.7 trillion a year192 between 2016 and 2030 – $26 trillion in total. The precise numbers depend on how both infrastructure and ‘need’ are defined,193 but the economic principles are clear: increased connectivity helps bring suppliers and consumers together, improves resource allocation, facilitates trade, and so raises productivity and incomes.

To date, bottlenecks in funding and project implementation have been the main obstacles to infrastructure expansion in the region. Now China’s ‘Belt and Road Initiative’ (BRI) promises to address both, and to take China’s experience of infrastructure-led growth overseas. It is, however, still early days – and succeeding at home is different to doing so abroad.

First, the all-embracing vision: China is deploying the BRI as a narrative or organizing principle with which to engage other governments on major projects. At least 68 countries are involved, although estimates vary (the number seems to keep rising). Originally the ‘Belt’ covered the land route from western China into Europe, while the ‘Road’, paradoxically, embraced sea routes from China’s coast down to the Indian Ocean and on to Africa. But the remit has continued to widen. Now Peru, Panama and others are included, as is the Arctic and space itself.

Understood like this, the BRI is a form of branding – which is then applied, sometimes retrospectively, to almost all infrastructure projects, whether new or already planned. This approach readily yields sizeable headline numbers – by some accounts, BRI investment could reach anything from $1 trillion to $8 trillion194 – though these sums are notably well short of the ADB estimate. Nonetheless, even the lower bound of this range of projections is seven times larger than post-war Europe’s Marshall Plan, adjusted for inflation.

Bottom-up calculations yield lower, though still significant, totals of investments so far: for example, $90 billion worth of transportation investments from 2014 to 2017.195 These active projects are often being implemented with rare speed and determination. They include the Hambantota Deep Sea Port in Sri Lanka, the East Coast Rail Link in Malaysia, the Khorgos Dry Port in Kazakhstan and a Belgrade–Budapest high-speed rail link.

To date, projects have adopted a common model: China’s policy banks lend the bulk of the money needed, and the receiving country figures out how to repay it. Interest rates vary – some loans are concessional, but many are at commercial rates. Construction contracts flow predominantly to Chinese state-owned enterprises, which then typically hire local subcontractors for part of the work.

The merits of the initiative are the subject of some debate. For China, BRI projects link it to the world, contribute to economic diplomacy and help fill excess capacity in the construction sector. For the receiving countries, they potentially provide much-needed infrastructure – but risk creating excessive debt burdens without generating significant local employment. There are also concerns about environmental damage. Success, in other words, is about more than funding alone. It includes broader community impact, the fairness of tendering processes and the extent to which corruption or bias against local firms is avoided.

Success is about more than funding alone. It includes broader community impact, the fairness of tendering processes and the extent to which corruption or bias against local firms is avoided

The pushback against China’s terms has already started, slowing implementation or stopping project starts. For instance, Thailand initially baulked at the contractual conditions surrounding the first section of the planned high-speed rail link with China via Laos. After further negotiations, work started in December 2017. Concerns over non-competitive tendering, at odds with EU requirements, have surfaced in Hungary. In Sri Lanka, both the original debt burden associated with the Hambantota Deep Sea Port and the subsequent conversion of debt to equity have caused popular resentment and problems for the government. Nepal turned down Chinese financing for hydropower, as did Pakistan. Mahathir Mohamad’s new government in Malaysia has announced its intention to review deal terms and renegotiate where it sees fit. Governments that are too eager for Chinese finance can run ahead of what their own people are willing to accept.

China alone will not be able to finance the BRI in full. The model for BRI projects will therefore need to evolve – consistent with China’s stated vision of welcoming competition, attracting private-sector financing and addressing local priorities – if the initiative is to fulfil its promise. As projects grow in number, so they will be more diverse. Private-sector finance will, by definition, flow only to projects structured to allow commercial returns, and supported by appropriate governance and the rule of law. For some countries (e.g. Thailand, Indonesia), Chinese financing is just one more option – albeit an important one – among others. Stakeholders in these countries will need to see broader benefits from participating in the BRI if they are to continue to commit to projects. Elsewhere (e.g. Tajikistan, Cambodia), China is effectively the only source of funding. These countries have correspondingly less leverage in negotiations, though they still need to ensure they understand the true costs and benefits for each project. Equally, some projects will make sense for strategic rather than commercial reasons, and here state-backed lending and government-to-government agreements will continue to be the order of the day.

Working all this out will proceed one project at a time. There will be no grand solution, but there is nonetheless the promise of steady progress and adaptation.

Andrew Cainey is an associate fellow with the Asia-Pacific Programme and the Global Economy and Finance Department.

An ambitious pan-African economic bloc – the African Continental Free Trade Area (AfCFTA) – was launched on 21 March at an African Union (AU) summit in Kigali, Rwanda. If it takes shape as envisaged, AfCFTA will comprise all 55 AU members, making it the world’s largest free-trade area by country coverage. Its creation presents an opportunity for continental-scale integration of African economies, currently held back by market atomization, disjointed regional trade arrangements and overexposure to the commodities sector. However, competing political and economic agendas, and resistance to market opening in some countries and sectors, present obstacles to success. In addition, harmonizing trade rules and standards among Africa’s existing patchwork of economic communities will be technically challenging.

African firms incur higher tariffs on their exports to other African markets than those that apply when they export outside the continent

Three principle factors reinforce the case for integration. First, the progressive elimination of most tariffs on intra-African trade (combined with measures such as regulatory harmonization and the streamlining of customs procedures) would boost trade and investment between AfCFTA members. African firms incur higher tariffs on their exports to other African markets than those that apply when they export outside the continent.196 The UN’s Economic Commission for Africa (ECA) estimates that AfCFTA’s elimination of import duties could boost intra-continental trade by 53 per cent, and could double it if non-tariff barriers are also lowered.197 The AU and ECA note that lowering tariffs on intermediate and final goods would be particularly beneficial, as tariffs on raw materials are already low. This could incentivize African economies to develop higher-value-added uses of their natural resource bases.

A consolidated internal market would help early-stage industries to become established, and build on the synergies already in evidence – though not yet fully exploited – in continental trade: African economies attain almost twice the value addition when exporting to their neighbours that they achieve when exporting to other parts of the globe. An increase in intra-African trade is also necessary in the context of historically low economic integration: intra-regional trade accounts for only 20 per cent of Africa’s total trade – albeit an improvement on the 12 per cent figure recorded a decade ago.198

Second, more frictionless borders would help exporters (particularly those in landlocked countries) to reach non-African markets more effectively and compete globally. AfCFTA countries would be better able to develop cross-border supply chains optimized according to comparative advantage and the location of suppliers and inputs. Moreover, trading as a bloc could encourage investment in transport infrastructure and trade facilitation services, creating a virtuous cycle of demand- and supply-side gains.

A third, and related, benefit of better connectivity is that it would support diversification: many African countries remain stuck in economic models that depend on exports, above all of commodities. Only Lesotho, Morocco, Tunisia, South Africa and Swaziland are considered by the UN Conference on Trade and Development as ‘export diverse’. Widening the export base would improve countries’ resilience, for instance to volatility in harvests and commodity prices.

As with most modern free-trade agreements (FTAs), AfCFTA will cover more than merchandise trade. In addition to the gradual elimination of tariffs, AfCFTA will seek to liberalize services, investment, intellectual property rights and competition policy. It will consolidate the current patchwork of bilateral and regional economic agreements and groupings into one coherent whole – boosting cooperation on shared infrastructure, standardized rules of origin and phytosanitary norms; and supporting investment in education, health and cross-national logistical hubs.

This breadth of coverage reflects growing recognition of the limitations of economic development predicated on low-end exports. The shifts occurring in the Chinese industrial model are illustrative, heralding the end of export-oriented manufacturing as a driver of structural economic transformation. With cheap labour and other comparative advantages, Africa can still profit to some extent from the delocalization of low-value manufacturing. However, with the continent a latecomer to industrialization, the prospects of such a model on its own providing a durable boost to employment or GDP growth are minimal.

More frictionless borders would help exporters (particularly those in landlocked countries) to reach non-African markets more effectively and compete globally

Rather, the real opportunities lie in manufacturing for the African consumer market. With a combined GDP in 2017 of around $6.4 trillion on a purchasing power parity (PPP) basis,199 a population of 1.2 billion,200 favourable demographics – given its youth bulge and rapid urbanization – and a burgeoning middle class, the continent is potentially attractive to global brands anxious to expand from mature markets. From an African perspective, the concern is that opening domestic markets could render local companies less competitive. However, AfCFTA’s common external tariffs will offer some breathing space. Exempt from such tariffs, African suppliers may be in a stronger position to develop regional value chains in closer proximity to their target markets – this may help emerging local firms to develop until they can compete with established international players.

A number of potential obstacles stand in the way of successful realization of AfCFTA. The first is that effectiveness is contingent on full, or near-full, membership (although only 22 countries need to ratify AfCFTA for it to come into effect – a development some expect by the end of this year).201 At the Kigali summit, 44 AU member states signed the AfCFTA consolidated text. The remaining 11 non-signatories included Nigeria and South Africa, the continent’s largest and third-largest economies respectively.202 South Africa has delayed signature because it considers the agreement incomplete, as no tariff schedules are in place and key annexes and protocols are unfinished (these are supposed to be finalized by the end of 2018). However, at the time of writing, South Africa’s parliament was already discussing AfCFTA. Other non-signatories have indicated their support in principle – Namibia, for example, has indicated that it will sign203 – though domestic and regional politics could complicate AfCFTA ratification, with the approach of elections in Nigeria in 2019, for instance, potentially motivating cautious political positions on market liberalization.

Assuming these issues are overcome, the main challenges will be around the technicalities and sequencing of implementation, including the need to consolidate under AfCFTA multiple provisions of pre-existing trade relationships and agreements. Although the continent’s regional economic communities (see table) have committed to the principle of alignment with AfCFTA, the harmonization process is complex and will take years to complete.

A final challenge to the successful implementation of AfCFTA’s ambitious agenda lies in the mood of protectionism that is shifting the rules of engagement in world trade. In the face of rising populist opposition to globalization, AfCFTA will have to remain a visible priority for African governments and institutions, able to demonstrate why it offers opportunities in a technology- and globalization-driven era of disruption to established economic models.

However, if commitment to AfCFTA can be sustained – and if accompanying efforts to liberalize movement of people also progress – the benefits could be substantial.

Carlos Lopes is an associate fellow with the Africa Programme.

|

Agreement |

Abbreviation |

Member states |

Combined population (million)* |

Combined GDP ($ billion)** |

|

Arab Maghreb Union |

AMU |

Algeria, Libya, Mauritania, Morocco, Tunisia |

94.2 |

425.7 |

|

Community of Sahel-Saharan States |

CEN-SAD |

Benin, Burkina Faso, Central African Republic, Chad, Comoros, Côte d’Ivoire, Djibouti, Egypt, Eritrea, The Gambia, Ghana, Guinea-Bissau, Libya, Mali, Mauritania, Morocco, Niger, Nigeria, Senegal, Sierra Leone, Somalia, Sudan, Togo, Tunisia |

553.0 |

1,350.7 |

|

Common Market for Eastern and Southern Africa |

COMESA |

Burundi, Comoros, Democratic Republic of the Congo, Djibouti, Egypt, Eritrea, Ethiopia, Kenya, Libya, Madagascar, Malawi, Mauritius, Rwanda, Sudan, Swaziland, Seychelles, Uganda, Zambia, Zimbabwe |

492.5 |

657.4 |

|

East African Community |

EAC |

Burundi, Kenya, Rwanda, South Sudan, Uganda, Tanzania |

168.5 |

159.5 |

|

Economic Community of Central African States |

ECCAS |

Angola, Burundi, Cameroon, Central African Republic, Chad, Congo, Democratic Republic of the Congo, Equatorial Guinea, Gabon, Rwanda, São Tomé and Príncipe |

158.3 |

257.8 |

|

Economic Community of West African States |

ECOWAS |

Benin, Burkina Faso, Cabo Verde, Côte d’Ivoire, The Gambia, Ghana, Guinea, Guinea-Bissau, Liberia, Mali, Niger, Nigeria, Senegal, Sierra Leone, Togo |

339.8 |

716.7 |

|

Intergovernmental Authority on Development |

IGAD |

Djibouti, Ethiopia, Eritrea, Kenya, Somalia, Sudan, South Sudan, Uganda |

247.4 |

218.2 |

|

Southern African Development Community |

SADC |

Angola, Botswana, Democratic Republic of the Congo, Lesotho, Madagascar, Malawi, Mauritius, Mozambique, Namibia, Seychelles, South Africa, Swaziland, Tanzania, Zambia, Zimbabwe |

312.7 |

678.8 |

* ECA (undated), ‘Regional Economic Communities’, https://www.uneca.org/oria/pages/regional-economic-communities (accessed 1 Jun. 2018).

** Ibid.