Lower-income countries that are banking on their fossil fuels lack the capacity to assess carbon risks, and may be left behind by shifts in investment and credit.

How Energy Transition is Changing the Prospects for Countries with Fossil Fuels

Research paper

Published 12 July 2018

Updated 19 November 2021

ISBN: 978 1 78413 279 8

Lower-income countries that are banking on their fossil fuels lack the capacity to assess carbon risks, and may be left behind by shifts in investment and credit.

Countries developing oil and gas today cannot expect to follow the same fossil fuel-led development model that has underpinned growth in many upper-middle and high-income countries over the last half century, including Norway, the UK, Saudi Arabia, Mexico, Kazakhstan, and Trinidad and Tobago. Two major new challenges to a fossil fuel-led development pathway have emerged in recent years:

This paper considers how these challenges might affect the development prospects of low and lower-middle-income countries with fossil fuel resources, both in terms of carbon risks and low-carbon opportunities. It also addresses the challenges faced by multilateral development banks (MDBs) and international donors that offer development assistance to upstream fossil fuel projects and linked power and industrial infrastructure, while at the same time making international climate change commitments. Based on the findings of dialogues with country stakeholders, and the MDB, donor and investment communities, and global and country-level modelling, this paper suggests ways that developing countries with fossil fuels might best enhance their resilience to carbon risks and benefit from low-carbon opportunities throughout the energy transition, and how MDBs and donors can support this.

The convergence of three major trends – growing global and national climate action, the increasing range and falling cost of clean energy technologies and the relative decline in oil prices – present a rapidly evolving landscape for emerging and early-stage fossil fuel producers. These trends provide the context for this paper.

Markets for fossil fuels will be profoundly affected by climate, environment and energy-related policies in major consuming countries. Donors and MDBs (and their partner countries) are all committed to the ‘well below 2°C’ target of the Paris Agreement.1 The concept of the global ‘carbon budget’ – or the amount of carbon that can be emitted under any given temperature target – has direct implications for future fossil fuel supply. The burning of coal, oil and gas is responsible for over 65 per cent of greenhouse gases.2 In 2015, University College London (UCL) attempted to show how a ‘2°C carbon budget’ might be distributed between regions on a ‘least-cost’ basis, as a first attempt to map the likely landscape of ‘burnable’ and ‘unburnable’ fossil fuel reserves.3 It showed that in order to meet the long-term goal of the Paris Agreement, over 80 per cent of the world’s proven coal reserves, half of its gas and one-third of its oil would need to remain unburned.4

As documented in an earlier Chatham House research paper, Left Stranded? Extractives-Led Growth in a Carbon-Constrained World, the prospect of unburnable fossil fuels presents clear risks to export economies.5 Which raises the question, is it prudent to develop fossil fuel resources for which there may be less or no demand, as fossil fuel consumption peaks and declines? While the time frames for this are unclear, and the impacts will differ by fuel and by region, the overall consensus is that a combination of climate and air quality policies, fuel price reforms and clean technology developments in key export markets will significantly reduce demand for fossil fuel imports over time. Chapter 2 sets out some of the key uncertainties at the global level, and the way the investment and finance communities are responding to them. Chapters 3 and 4 explore how these trends might translate into challenges at the producer country level, drawing on modelled scenarios for Ghana and Tanzania. More recently, researchers have explored policy options to ‘limit’ future fossil fuel supply6 and the equity implications of the global carbon budget.7 These are discussed in greater detail in Chapter 5.

This paper re-states the urgent need for coal phase-down. Chapter 2 acknowledges the interplay between coal phase-down and the prospects of other fossil fuels, particularly gas. However, in its discussion of carbon risks and opportunities, and their implications for country planning, this paper concentrates on oil and gas projects and linked power and industrial infrastructure. It does not consider coal projects in any detail, for two main reasons:

Many countries have benefited from developing their fossil fuel resources. Development models like those of the Gulf, Trinidad and Tobago, and Malaysia all provide compelling examples of fossil fuel-led growth that many less-developed countries are keen to follow. At the same time, however, fossil fuel producers in the developing world are increasingly embracing the concept of climate-smart, ‘green’ growth. They have made commitments to mitigate carbon emissions through their initial Nationally Determined Contributions (NDCs) under the Paris Agreement, which cover the period 2020–25, and plan to increase this ambition every five years under the ‘ratchet’ mechanism of the Paris Agreement.9 The development of long-term emissions reductions plans to 2050 under the United Nations Framework Convention on Climate Change (UNFCCC) will help guide this.10

The concrete policy measures that are required for the implementation of these ambitions generally entail reforms in the energy, transport and forest sectors. Stated measures in the NDCs of low and lower-middle-income fossil fuel producers such as Ghana, Uganda, Tanzania and Kenya include:

Access to RE, storage and other clean technologies will be key to delivering many of these ambitions. In many developing countries with low levels of access to electricity and a heavy reliance on diesel generators, decentralized RE already provides the cheapest access to energy. Competitive procurement through RE auctions, for instance, is now driving down the costs of utility-scale RE in key markets. In India, for example, new wind and solar generation is now cheaper than around two-thirds of the country’s coal-fired generation, and costs are continuing to fall.12 Recent research from the International Renewable Energy Agency (IRENA) suggests that globally, utility-scale RE will be competitive with or cheaper than fossil fuel generation by 2020.13 Since 2015, developing economies (including China, India and Brazil) have dominated the record sums of money being invested in RE systems.14

Such rapid shifts in the global energy landscape raise serious questions for country decision-makers. As global energy systems, trade flows and investment patterns change, and with related changes in the cost curve for different energy technologies, is the development of high-carbon industries, followed by a period of economic diversification still the best pathway?

National policies, plans and investments in the fossil fuel sector and linked energy, industrial and transport infrastructure are rarely coordinated with clean technology investments or wider climate commitments, and may even conflict with them. As noted earlier, the development or expansion of fossil fuels in developing countries (or even the expectation thereof) can affect the political economy, and the concentration of political power and institutional development in a country, leading to the over-dependence of state budgets on investment flows and export revenues from the fossil fuel sector. This is often coupled with overblown societal expectations about the benefits the sector can provide (in terms of infrastructure, employment and wider economic impetus).15 Structural features that emerge in fossil fuel economies include cheap or subsidized fossil fuel energy and inputs and the development of carbon-intensive infrastructure, as well as strong political interests that tend to gather around the influence and profits associated with the sector; all have the potential to complicate the development of a low-carbon economy.16

The above trends come at a time in which country politics and economics are being shaped in response to the commodities price collapse of 2014.

Emerging economies that had enjoyed high GDP growth rates over the previous decade, such as Angola and Nigeria, suffered severe economic shocks as oil and gas prices dropped.17 Facing balance-of-payments pressures as foreign direct investment (FDI) dried up and commodity prices collapsed, many governments were forced to make spending cuts, raid foreign exchange reserves or continue to borrow to stay afloat, risking either economic or societal instability. This became a reality in Venezuela, where collapsing oil revenues affected the government’s spending capacity and ability to import essential goods, including food and medicine, which led to civil unrest and a humanitarian crisis.

For well-established export economies, such as Mexico and the Gulf States, economic diversification away from fossil fuels has become a priority – in the case of Saudi Arabia this has been as part of a comprehensive vision for a post-oil future.

For well-established export economies, such as Mexico and the Gulf States, economic diversification away from fossil fuels has become a priority – in the case of Saudi Arabia this has been as part of a comprehensive vision for a post-oil future. After decades of high oil revenue dependence and policies to promote energy-intensive industries in these countries, the often-overlooked challenges of creating effective energy policy and reducing consumption subsidies, while increasing the productivity of non-oil sectors, are now becoming priority policy areas.

Unsustainable spending often begins before any major discoveries, for example in São Tomé and Príncipe and Madagascar, where a ‘resource curse without natural resources’ emerged due to overspending in expectation of the ‘resource boom’.18 In Ghana and Mozambique, international borrowing against expected income from large-scale fossil fuel development became unsustainable when these projects were delayed, creating a ‘pre-source curse’.19 Most recently, in Papua New Guinea, LNG development has failed to deliver the economic boost that was anticipated.20 The resulting debt and the international dependencies associated with it will shape politics and development choices in these countries for many years to come.21

Taken together, these trends suggest that the risks of dependence on fossil fuel sectors for income, energy security or industrial growth will only increase and evolve in nature over the coming decades.

This paper is aimed at the governments of aid-dependent developing countries that are looking to explore for oil and gas, develop existing discoveries, or expand existing reserves for export and/or domestic use. For this purpose ‘developing countries’ are defined as least developed, low and lower-middle-income economies as defined by the OECD.22 At least half of the 143 countries that fall under this definition, including 80 per cent of all least developed countries and low-income countries (LDCs/LICs) and one-quarter of all lower-middle-income countries (LMICs), are currently exploring for oil and gas, developing discoveries or have existing production (Figure 1). The strategic choices that the governments of these countries take will affect the lives of over 1.6 billion people.

Given that the majority of developing countries looking to further develop or expand their fossil fuel resources are in sub-Saharan Africa and Central America and the Caribbean, these regions are a natural focus for this paper. As set out above, countries in these regions were among the least prepared to manage the commodities price falls of recent years. Drawing on country case studies of Ghana and Tanzania, and discussions with many other low and lower-middle-income countries, this paper provides examples of how the issue of carbon risk might be approached, including through scenario analyses and multi-stakeholder dialogues on the role of the fossil fuel sector in national planning.

The country examples presented in chapters 3 and 4 are not intended to be representative of all developing countries. They are presented as useful comparisons, given their different stages of development and contrasting fossil fuel reserves and revenue prospects. The upper-middle-income, industrializing economies of developing Asia face different challenges, not least because the governance profiles of donors and recipients of development assistance, and the mechanisms and channels of support, are markedly different. The same is true for some of the upper-middle- income economies of Latin America, Eastern Europe and Central Asia. Nonetheless, the analysis presented in this paper should still be of broad relevance, and may help signpost areas in need of further research.

With MDBs and donor countries promising to increase climate finance and assist countries in their transition to a low-carbon development pathway, it is essential that they consider how their support for fossil fuel development affects these objectives. MDBs and donor governments have faced growing pressure from a range of civil society actors to demonstrate how their assistance to fossil fuel development abroad aligns with their international commitments to emissions mitigation.23 Many MDBs and donors are now reforming their approaches to fossil fuel development to ensure their alignment with climate commitments (see Annex I for case studies on MDB and donor strategies).

This paper focuses primarily on MDBs and donor agencies, although it acknowledges the significant influence of non-ODA state institutions with an interest in overseas development (see Box 2). It also has relevance for other development actors, including NGOs, philanthropic foundations and for-profit consultancies, which often deliver ODA-funded programmes and projects.

Foreign aid works in many ways, not all of which are covered here. This paper defines ‘development assistance’ to the fossil fuel and energy sectors as development finance and programmes of technical, capacity and policy assistance that is delivered via the primary channels of ODA, e.g. bilaterally, via a donor country’s development agency, and multilaterally, primarily through MDBs.

Bilateral development assistance is where aid is provided directly by a donor country to a recipient country. The bulk of this assistance is typically delivered by a state development agency such as the UK’s Department for International Development (DFID) or the US Agency for International Development (USAID). The remainder may be spent by other departments – typically those related to foreign affairs, business and trade – or ‘cross-government’ funds. In 2016–17, for instance, 72.5 per cent of the UK’s ODA was spent by DFID, 5.5 per cent by the Department for Business, Energy and Industrial Strategy (BEIS), 4 per cent by the Foreign & Commonwealth Office (FCO) and the remaining 18 per cent by other departments.24 Donor countries have full control over where and how this assistance is delivered.

Multilateral assistance covers support from MDBs (or other multilateral development finance institutions) including the World Bank Group, the European Bank for Reconstruction and Development (EBRD), the Asian Development Bank (ABD) and the African Development Bank (AfDB). It also covers multi-stakeholder financial vehicles including the World Bank-administered Global Environment Facility (GEF) and the Climate Investment Funds (CIF). International organizations with a development mandate such as the United Nations Development Programme (UNEP) also offer assistance to the fossil fuel sectors. These institutions are owned by their respective stakeholder countries, which have voting rights and influence, if not full control over how assistance is delivered.

Development assistance delivered via these multilateral and bilateral channels tends to share similar objectives – namely alleviating poverty, and promoting sustainable and equitable economic development. While they are not the focus of this paper, other state institutions with a development remit tend to have wider objectives, often including an element of trade and investment promotion for the donor country. They include:

The activities of these actors may be coordinated with bilateral and multilateral ODA to a degree, but they are rarely completely aligned. Their governance structures and investment processes vary; some have their investment strategies set by the relevant ministry and have ministerial representation on their boards, while others operate more or less independently.27 In some cases, such as where finance for coal-mining and coal-fired power is provided,28 their support may be in direct conflict with emerging norms in ODA.

This paper focuses on the established MDBs and donors that are members of the Development Assistance Committee (DAC) of the Organisation for Economic Co-operation and Development (OECD).29 However, it acknowledges the rapidly expanding role of emerging donors – including those of the BRICS and the GCC countries; and emerging development banks such as the Asian Infrastructure Investment Bank (AIIB). These institutions are at a much earlier stage of their operations and policy development, and may also find the paper’s analysis and recommendations of interest.

Development assistance to the fossil fuel sector takes a number of forms, from finance and guarantees for upstream activities and (often linked) thermal power infrastructure, to programs of technical assistance, policy advice and institutional capacity-building. MDBs tend to play a greater role in financing upstream fossil fuels than development agencies, for whom technical and policy advice is often their sole or primary form of support to the sector. The six major multilateral development banks provided over $13 billion in financing and guarantees for fossil fuel-fired electricity generation and almost $9 billion for upstream oil and gas activities between 2010 and 2015.30 OECD-DAC data suggests that bilateral ODA to the fossil fuel-fired power and the oil and gas sectors stood at almost $5.5 billion and $525 million over the same time frame.31 Both are likely to be low estimates.32

These are small sums of investment when considered against total global investment in fossil fuel supply and generation, which stood at $706 billion in 2016 alone.33 These are also small sums when considered against rapidly scaling MDB commitments to climate finance, which reached $32 billion in 2017 (of which 79 per cent was for climate mitigation).34 Why then, with so much private capital available and with growing climate commitments, would MDBs and donors support upstream activities? There are several reasons.

First, in economic development terms, FDI and export revenues from the sector can offer a source of income (foreign exchange) for developing countries, for which there are few if any comparable alternatives. Fuel supplies also have the potential (with the right infrastructure) to improve domestic access to energy and support industrialization. Many MBDs and donors have promoted oil and gas development as a potentially ‘transformative’ economic opportunity and a ‘chance to graduate from aid’. The role of natural gas as a ‘bridging’ fuel within a wider low-carbon development vision has also been of interest to development actors in recent years, particularly where it has the potential to displace coal-fired power or reliance on fuel oil.

In economic development terms, FDI and export revenues from the sector can offer a source of income (foreign exchange) for developing countries, for which there are few if any comparable alternatives.

Second, support for ‘good governance’ and policy and institutional development can help avoid negative resource curse impacts. The focus of development assistance has evolved over the decades. Following the economic crises of the 1980s, development assistance emphasized attracting FDI through favourable investment terms. In the 1990s, it incorporated rising concerns about negative governance, economic and social outcomes associated with the resource curse. In the early 2000s, the emergence of ‘good governance’ regimes stressed transparency and greater accountability as the ‘cure’ for resource curse ills. Since the late 2000s, there has been a growing focus on cross-sector linkages and integration with the wider economy.35 Climate considerations have not typically featured in this assistance, beyond sector-specific measures to eliminate flaring, enhance energy efficiency and increase RE use.

Third, support to the fossil fuel sector can lend considerable strategic influence. Long-standing relationships with country partners mean that MDBs and donor countries often influence fossil fuel investment frameworks, development decisions and models of growth through their policy and technical assistance. Development assistance is typically offered in response to country requests, and given that upstream development is often a political priority for governments, these requests may present an opportunity for increasing influence in a developing country. Particularly where fragile and conflict-affected states such as Iraq, Somalia and Afghanistan are concerned, assistance to the sector may be considered as a means of stabilization, particularly where it centres on good governance and transparency.36

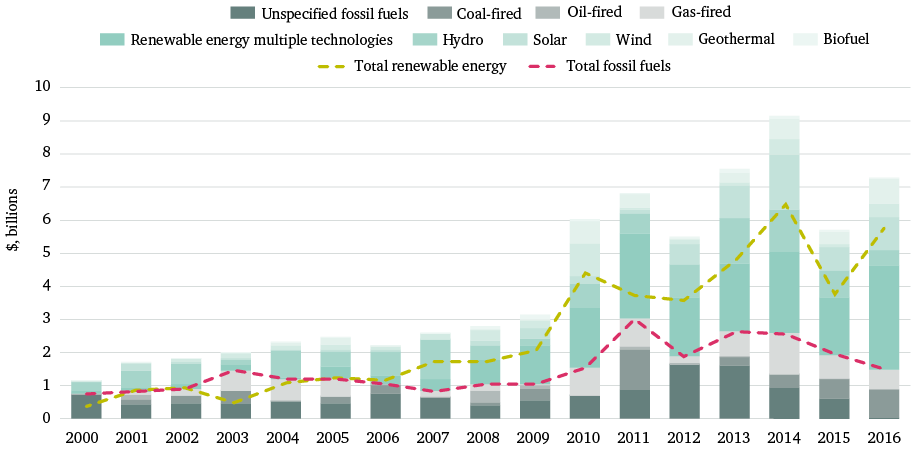

The rationale for assistance to the energy sector (including both fossil fuel and RE generation, as well as transmission and distribution) is more straightforward. MDBs and donors consider access to energy as crucial to supporting economic growth, and at the same time, the sector often fails to attract commercial investment. Notwithstanding the limitations of OECD-DAC data, there appears to be a clear and accelerating trend towards clean energy. Figure 2 shows how support for RE has outpaced support to thermal generation since 2006, and now accounts for 65 per cent of total energy ODA.

The real impact of MDB and donor engagement in these sectors is even greater than the sum of their investment. Where the policy and business environment is perceived to be high-risk and the cost of capital is prohibitively high, finance and guarantees provided by MDBs can effectively ‘de-risk’ investments and help mobilize and leverage much larger sums of private capital into the sector.37 The OECD estimates that ODA – and particularly investment guarantees – helped raise $81.1 billion from the private sector between 2012 and 2015, including $20 billion in the energy sector and $5.2 billion in natural resources and mining.38 Securing downstream investments in energy and industry are often critical to getting upstream investments agreed in the first place. The World Bank’s largest ever guarantee of $700 million, for Ghana’s gas-to-energy infrastructure, was intended to leverage a further $7.9 billion in private finance. It was key to the development of the Ghana’s Sankofa gas field.39