Lower-income countries that are banking on their fossil fuels lack the capacity to assess carbon risks, and may be left behind by shifts in investment and credit.

How Energy Transition is Changing the Prospects for Countries with Fossil Fuels

Research paper

Published 12 July 2018

Updated 19 November 2021

ISBN: 978 1 78413 279 8

Lower-income countries that are banking on their fossil fuels lack the capacity to assess carbon risks, and may be left behind by shifts in investment and credit.

Following the Paris Agreement, the issue of carbon risk has risen rapidly up the international agenda. The trajectory implied by a 2°C carbon budget has significant implications for financial stability and the value of assets and investments over time – particularly fossil fuels. In response to this, public and private sector stakeholders in advanced economies are now re-evaluating their long-term strategies against a 2°C scenario, as well as nearer-term policy signals and demand-side shifts.

It is important that developing countries that are banking on securing foreign direct investment (FDI) into their fossil fuel sectors have a good understanding of the ways in which different actors are responding to evolving uncertainties and risks, and how this is re-shaping global investment patterns. This chapter uses UCL modelling (see Annex II for a full methodology) to show what a least-cost pathway for achieving a ‘well below 2°C target’ implies for oil, coal and gas markets. It also draws on dialogues held with MDBs, donors and the wider investment and finance communities, in order to explore real world thinking, trends and factors that will influence markets. The last section focuses on investment, both in terms of institutional investors, many of which are IOC shareholders, and other commercial financiers that will influence capital available for infrastructure and energy systems.

The international commitment to limit global warming to well below 2°C above pre-industrial levels – and as close as possible to 1.5°C – means that fossil fuel use must fall dramatically over the next 30 years. This limit on temperature increases can be translated into a ‘carbon budget’, or the amount of carbon dioxide (CO2) that can be emitted through the burning of fossil fuels by 2100 (and beyond) before the average global temperature rise exceeds 2°C.40 This equates to a total carbon budget of around 830 gigatonnes of carbon dioxide (GtCO2) from 2017, which will be used up in 20 years under current emissions trajectories.41 Previous research estimated that under such a 2°C carbon budget, 80 per cent of coal, 50 per cent of oil and 33 per cent of gas reserves would be ‘unburnable’.42

The 1.5°C limit translates into a much smaller carbon budget of around 240 GtCO2, which at current rates would be used in just four years, and would in turn imply that a higher percentage of fossil fuel reserves are ‘unburnable’.

Moreover, the ambition expressed under the Paris Agreement is to aim for a 1.5°C limit, given the severity of climate impacts implied by even the 2°C rise. This translates into a much smaller carbon budget of around 240 GtCO2, which at current rates would be used in just four years (see Annex II), and would in turn imply that a higher percentage of fossil fuel reserves are ‘unburnable’.

Competition between different fossil fuels for their ‘share’ of the remaining carbon budget is likely to intensify in the coming years. Coal is the most carbon intensive fuel in the global energy mix, and all 2°C scenarios show a sharp reduction in its use within the next five years. A greater range of trajectories exists for oil and gas use, depending on the assumptions made regarding transition pathways and the availability and affordability of clean technologies.43

There are three broad areas of uncertainty that are subject to policy influence: the level of climate ambition and the speed of response; the role of carbon capture and storage (CCS), bioenergy44 with CCS (BECCS) and other negative emissions technologies (NETs); and ‘demand side’ drivers, including the speed at which new energy technologies and business models emerge and investment patterns shift.45

As a result of the varying assumptions that mainstream models make regarding these uncertainties, there are a range of possible pathways to a ‘well below 2°C’ world. This chapter explores the key assumptions and uncertainties inherent in the modelling undertaken for this paper, which shows pathways under five credible climate scenarios (see Table 1). These scenarios are based on the latest available data (2016), and explore the most cost-effective pathways to a given level of climate ambition, rather than reflecting what is happening, or what is most likely to happen. A full methodology is provided in Annex II.

|

Scenario |

Assumption |

|---|---|

|

NDC |

Reflects current country pledges (NDCs) under the UNFCCC process, resulting in around 3.5°C rise in global temperatures. |

|

2D |

Represents a 2°C limit based on a central carbon budget of 910 GtCO2 (between 2015–2100), or 830 GtCO2 (taking into account the last two years of emissions). |

|

2D590 |

Represents a 2°C limit based on a more stringent budget of 590 GtCO2 as a result of lower than anticipated action on non-CO2 GHGs. |

|

No CCS |

Represents a 2°C limit as under 2D but with no CCS deployment. |

|

Tech acceleration |

Reflects stronger cost reductions for solar PV, wind and electric vehicles (EVs), with vehicle cost parity in the mid-2020s compared to 2030s under 2D. |

Source: Compiled by authors.

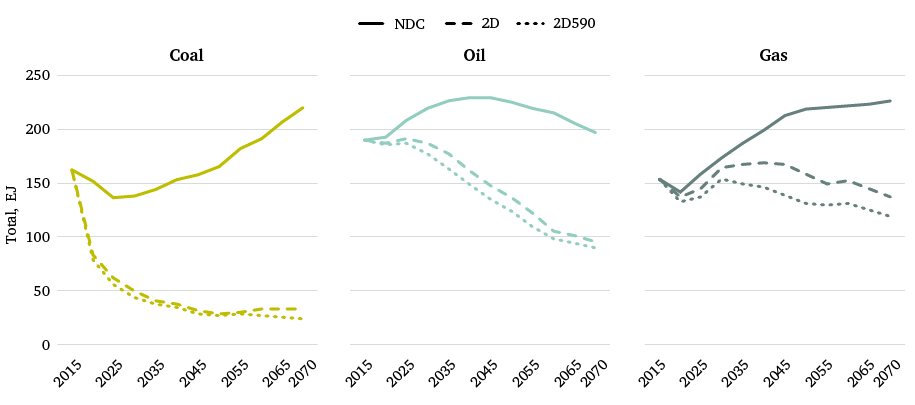

Figure 3 illustrates the difference between the climate commitments that countries have set out in their current NDCs, and the level of ambition required to stay within a 2°C carbon budget. There is much lower use across all fossil fuels in a 2°C budget, compared to a current NDC (equivalent to a 3.5°C temperature rise) budget. While oil and gas remain an important part of the global energy system within a 2°C carbon budget, oil production falls to around half of current levels shortly after 2050, and there is little growth in gas, which remains at similar production levels as today.

These, like most mainstream scenarios, assume a rapid reduction in coal use; a pathway that is most cost-effective, but may be challenging to realize politically. While coal use slowed in 2016, it is not yet on the 2D pathway shown in Figure 3. Higher-than-expected coal use in the near future would imply the need for further reductions in oil and gas use by 2050, constraining their potential role within a 2°C carbon budget.

The scenarios also assume rapid action. If action is delayed and near-term emissions remain at high levels there would need to be much sharper subsequent reductions in CO2 emissions. This would also likely reduce future ‘space’ for fossil fuel use, as well as incurring much greater systems costs, as more energy, transport and other infrastructure is ‘stranded’.

A further uncertainty in the size of the carbon budget relates to overall climate ambition and efforts to reduce non-CO2 greenhouse gases (GHGs), which account for almost one-third of global emissions.46 Their primary sources include fugitive emissions from the energy sector, industrial processes and agriculture. Within the 2°C budget, an aggressive non-CO2 GHG reduction scenario could imply a larger available carbon budget of 1,160 GtCO2, while weak efforts to mitigate non-CO2 GHGs could result in a smaller available carbon budget of 590 GtCO2.47 This is shown by the 2D590 scenario in Figure 3, and has particular implications for the role of natural gas.

In recent years, natural gas has been promoted by development actors as an alternative to coal and as a ‘bridge’ to a low-carbon future. Many IOCs have pivoted towards gas as part of their efforts to adapt to a decarbonizing world. The discovery of new information regarding non-CO2 emissions may also have implications for the role of gas within the global carbon budget. Due to its high global warming effects, methane (CH4) emissions from gas production, transport and use have the potential to undermine the benefits of gas over other fossil fuels, in terms of its carbon intensity.48 The risks of methane leakage typically remain underexplored and poorly addressed at both the global and country levels.

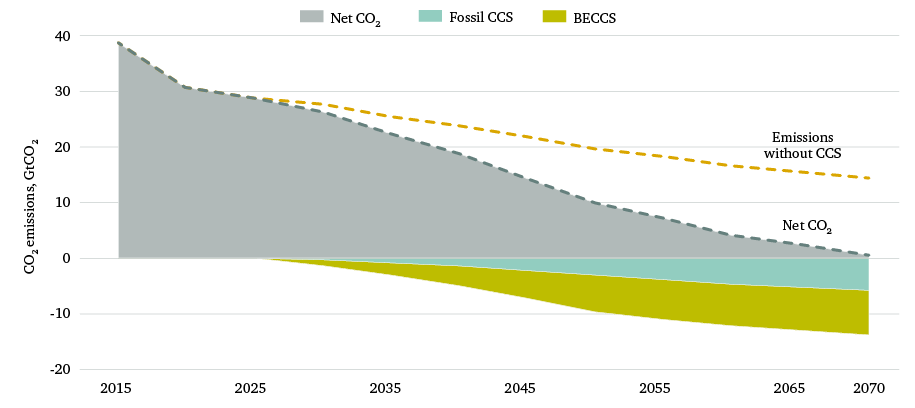

Most mainstream scenarios – including those produced by the IEA and major oil companies – assume a significant role for CCS and BECCS.49 The deployment of CCS could allow the continued use of some fossil fuels for power generation and in heavy industry, where substitution is more challenging.50 The use of BECCS would help offset remaining fossil fuel-based emissions via negative emissions, generated by a net transfer of CO2 from the atmosphere, through the biosphere and into geological layers. In all but the most rapid and deep decarbonization scenarios, global emissions effectively overshoot the 2°C carbon budget by mid-century – many 2°C integrated assessment models (IAMs) assume net-negative emissions by 2070, with BECCS compensating for this earlier overshoot.51

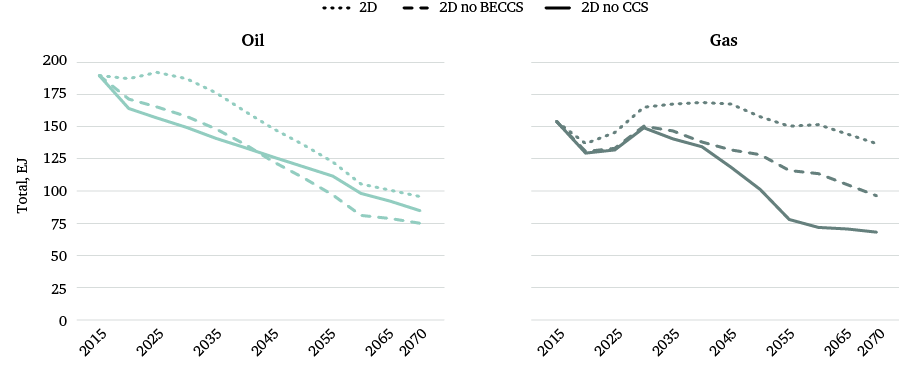

The global supply and emissions trajectories in Figure 4 are also premised on the availability of CCS and BECCS. Figure 4 illustrates the roles that CCS and BECCS play in the 2D scenario in this paper; in order for net CO2 emissions to reach zero in 2070, CCS must deal with around 15 GtCO2 (shown by the blue and green shaded areas). The cumulative CO2 emissions that CCS would need to capture to 2100 are equivalent to the entire 2°C carbon budget – so the use of CCS effectively doubles the available carbon budget in this instance. The scaling of CCS and the bioenergy resource levels required for BECCS (along with the assumption that this resource is sustainable) therefore represent critical uncertainties for the available carbon budget and in turn, for future fossil fuel use.

The risks of CCS and BECCS not materializing – namely locking energy systems into a high emissions pathway – are not generally factored into mainstream scenario analyses, or made explicit to the policy community, nor are the sizable downside risks of deploying BECCS at the scale modelled.52 At present, few countries are currently planning for CCS or BECCS, or mention them in their NDCs.53 The 22 large-scale CCS projects currently in operation are clustered in North America, Northern Europe and China, and have typically emerged where they represented a small, incremental investment on an existing process, or where the resulting CO2 has commercial value.54 From an investor perspective, CCS is not on the horizon; few commercial opportunities have arisen, and CCS does not typically feature in ‘green finance’ discussions.55 Meanwhile, depending on the energy crop used and the efficiency of production, the level of BECCS deployment in many 2°C scenarios could require between half to five times the land area used to grow the world’s entire current cereal harvest.56

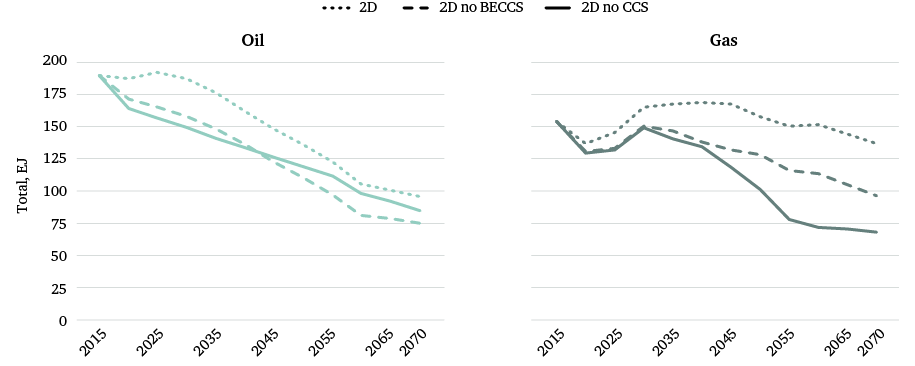

Without these technologies, the future role of fossil fuels will be strongly curtailed. A ‘no CCS’ scenario, which represents the current outlook, would have the greatest impact on gas. Compared to the standard 2°C scenario (with CCS), the production outlook is about 50 per cent lower in 2070 (Figure 5). Oil is considerably less sensitive to CCS; reflecting the fact that oil is considered the hardest of the fossil fuels to displace, given its central role in the transport sector. For growth areas of demand such as freight, shipping and aviation, there are few viable substitute clean energy technologies at present. The increased cost of mitigation without options such as CCS and BECCs – due to the greater production and use of advanced biofuels, hydrogen from electrolysis, and higher-cost RE it would imply – also presents a major challenge.57

Moreover, even without CCS or BECCS, other NETs – including afforestation, reforestation and biochar – would still be required for these reduced levels of fossil fuels to be sustainable. To meet the long-term objective of the Paris Agreement, CO2 emissions would need to total around 830 GtCO2 between 2017 and 2100; yet under the ‘no CCS’ scenario, cumulative CO2 emissions would already be around 1,000 GtCO2 in 2070, requiring other NETs to reduce this total. Once again, without NETs, the scenarios show an overly optimistic outlook for fossil fuel production.

A 1.5°C scenario was not included in the modelling undertaken for this paper by UCL. Based on IPCC estimates, in order to limit temperature increases to 1.5°C above pre-industrial levels, the carbon budget would be approximately 240 GtCO2, from 2015 onwards. This is significantly lower, and even more ambitious than the low and mid points of a 2°C budget range of 590 GtCO2 and 830 GtCO2 (estimated with a 66 per cent probability of achieving the target).

As shown in the paper by Hughes et al. (2017), even with optimistic options for CCS and BECCS, the TIAM-UCL model was not able to provide a feasible solution for a 1.5°C carbon budget.58 The main reasons for this limit to increased ambition (compared to the already challenging 2°C case) include the limited NETs options considered (BECCS only), and a cap on global bioenergy resources of 130 exajoules (EJ) per year after 2050, which in turn constrains the negative emissions available to the system via BECCS.

By contrast, IAMs clearly are able to run 1.5°C scenarios.59 However, they typically assume significantly higher contributions of negative emissions and bioenergy use than those assumed in the TIAM-UCL modelling.60 Bioenergy use for a 1.5°C scenario (in the equivalent growth scenario used in TIAM-UCL), increases to over 200 EJ per year while cumulative levels of CO2 captured are also more than 50 per cent higher than those observed in the TIAM-UCL modelling.61

A number of scientists have noted the danger in increasing reliance on the large-scale deployment of new technologies and resources for mitigation,62 and have suggested that this is a high risk strategy.63 For these reasons, the modelling in this paper has not sought to further relax model assumptions in order to meet the target, as the deployment of such technologies under the 2°C carbon budget is already highly ambitious and requires an unprecedented rate of change. The forthcoming IPCC Special Report on 1.5°C will shed further light on mitigation pathways compatible with the 1.5°C target in the context of sustainable development pathways.

While 2°C scenarios provide a clear indication of the long-term direction that policy and public finance should take, demand will ultimately be influenced by a combination of government policies, fuel and fuel-substitute prices, technological advances, and new information and investment trends. Lines will not follow a smooth curve. For mainstream scenarios, anticipating non-linear drivers of demand – including disruptive shifts in technologies and behavioural shifts among consumers – has proved challenging. In recent years, the providers of these scenarios have repeatedly underestimated RE uptake and overestimated fossil fuel demand.64 A similar picture is now emerging around projections of battery storage capacity and electric vehicle uptake.

Providers of mainstream scenarios have repeatedly underestimated RE uptake and overestimated fossil fuel demand. A similar picture is now emerging around projections of battery storage capacity and electric vehicle uptake.

Expectations for future oil demand provide perhaps the best example of this uncertainty. The global scenarios developed for this project show relatively limited impact on oil production to 2030, compared to the reductions seen in the models for gas and coal. This is in part due to the ‘head room’ created by declining coal use and increasing CCS deployment, but it is also a result of transport being a more costly sector in which to effect change. It is assumed that electrification beyond light-duty road vehicles will be limited for the foreseeable future, given the difficulty of electrifying other sub-sectors such as freight and aviation. At the same time, the prospects for the displacement of oil by biofuels are also limited due to bioenergy resource constraints.

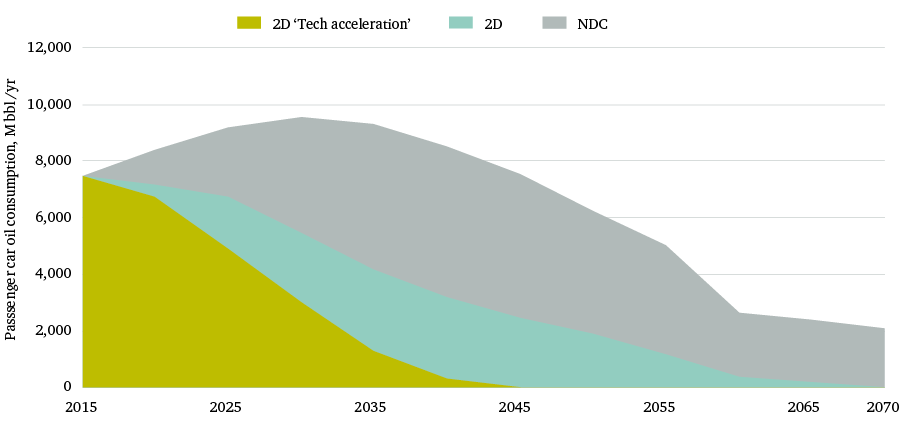

As Figure 6 shows, more ambitious electrification rates in the passenger car sub-sector could have a significant impact on oil demand in the longer term. Under the NDC and 2D scenarios, it is assumed that EVs reach price parity with internal combustion engine (ICE) vehicles in the 2030s, and account for 6 per cent and 22 per cent of the global fleet in 2040. Under the ‘tech acceleration’ scenario it is assumed that price parity is reached in the mid-2020s and that EVs account for 75 per cent of the global fleet by 2040. Under such a scenario, oil use in the passenger car sub-sector would collapse by the 2040s (rather than the 2060s), and cumulative oil consumption in the sub-sector would reduce by over one-third to 2040.

Many factors will ultimately affect future oil demand in the transport sector, including efficiency improvements in ICE vehicles and reductions in the size of the global car fleet (due to urbanizing populations and the growth of business models such as ride sharing, which negate the need for car ownership), as well as the speed of EV uptake. Policies in major fuel consumer markets, driven by pressure for clean air are preparing to phase out the ICE. Governments in the EU and China have announced dates by which the sale of ICE vehicles will be outlawed. In shipping, a growth area for demand, an international agreement under the International Maritime Organization has set the goal of halving emissions from this sector by 2050.

While the ‘tech acceleration’ scenario is far more ambitious than even the most optimistic current forecasts for EV uptake,65 it illustrates the impact that a more disruptive shift in the sector could have on demand, even when limited to the passenger vehicle sub-sector.

Scenarios based on what ‘should’ happen to reach the internationally agreed emissions targets appear highly theoretical for country governments, investors and others wishing to know what is likely to happen on the demand side. However, the implications of climate mitigation goals are informing policies, regulation and consumer and shareholder preferences, so even from a purely commercial perspective, there is growing interest from a wide range of large investors and financiers regarding how to interpret these trends in a way that can inform the deployment of capital. There are two issues here:

The varying time horizons of different market actors have presented one of the greatest barriers to effective coordination around both issues. In his landmark speech in 2015, Governor of the Bank of England Mark Carney described climate-related financial risks as a ‘tragedy of the horizons’; with those engaged in monetary policy and sovereign ratings looking 2–3 years ahead, those concerned with fiscal policy looking up to a decade ahead, but few considering impacts beyond this.66 Long-term investors, including institutional investors, pension funds, and sovereign wealth funds (SWFs), which face the dual challenge of ensuring short-term (3–5 years) and long-term (30–40 years) returns are perhaps the exception.

Traditionally, the varying time horizons of different market actors have presented one of the greatest barriers to effective coordination around both carbon risk and direct climate impacts.

Long-term investors have been among the most active in managing their exposure to carbon risks. Some are using their shareholder voting rights to influence IOC behaviour; the New York State Common Retirement Fund and the Church of England, for example, successfully passed a shareholder resolution in 2017 with the support of 30 major institutional investors, compelling Exxon Mobil to report climate-related risks to its business.67 Others have committed to divestment as part of a wider diversification strategy. Norges Bank, which manages Norway’s $1 trillion SWF, stated in late 2017 that the ‘government’s wealth can be made less vulnerable to a permanent drop in oil prices’ by divesting of its $35 billion of oil and gas stocks.68 In early 2018, Mayor of New York Bill De Blasio announced that the city’s pension fund would divest its $5 billion of fossil fuel company shares (as well as launching a lawsuit against five IOCs for climate damages).69 This movement is prompting major IOCs to pre-emptively adjust their strategies to demonstrate a less carbon-intensive portfolio, which will in turn influence how they choose to invest their capital.

Clear signalling at the international level has helped build consensus and improve alignment among these market actors. In 2015, the G20 asked the Financial Stability Board (FSB) to establish the Task Force on Climate-related Financial Disclosures (TCFD), in order to better understand the materiality of market risks (e.g. devalued or stranded assets) and physical risks (e.g. rising sea-levels, extreme weather events).70 The TCFD’s final report in July 2017 provided guidance on scenario analysis and a framework for the disclosure of climate risk and technical advice. At the One Planet Summit in Paris, in December 2017, FSB Chair Mark Carney and TCFD Chair Mike Bloomberg announced that 237 companies with a market capitalization of over $6.3 trillion, including 150 financial firms with over $81.7 trillion assets under management, had committed to TCFD implementation.71

As set out above, there are significant uncertainties regarding the speed of transition and the likely pathway in terms of technologies and energy mix over time. There is little in the way of a common baseline for analysis.

These companies and investors are looking to both ‘top-down’ policy signals – including what is required at the global level over the long term, and what countries have pledged in their NDCs in the shorter term – and ‘bottom-up’ trends including shifting demand patterns and disruptive new technologies. Commercial and asset allocation strategies reflect an actor’s time frame and risk threshold; some may still invest in high-carbon areas, provided that assets can be quickly divested (or written-off) and capital re-allocated.72 There is scope here for knowledge-sharing in terms of the creation and use of carbon pricing, and the development of investment strategies that take advantage of lower carbon portfolios with a track record of outperforming the market. The One Planet group of long-term investors and SWFs is now developing a carbon sensitive investment framework, for instance. The asset owner-led Transition Pathways Initiative (TPI) is looking to ‘management quality’ – from the acknowledgment of carbon risk to its incorporation in strategic decision-making – as a key indicator of future performance.73

By comparison, there remains limited understanding of how carbon risks are likely to play out in national economies. Central banks and regulators are moving to understand these carbon risks. In March 2018, the governors of the UK, French and Dutch central banks called for growing regulatory oversight, including the potential development of forward-looking ‘carbon stress’ tests over longer time horizons, and a shift from voluntary to mandatory disclosures. The first technical challenge, according to Governor Villeroy de Galhau of the French Central Bank, is ‘how can we elaborate on the link between climate scenarios and economic scenarios?’74 Ratings agencies are also beginning to consider exposure to climate and carbon risks as factors in sovereign credit ratings, which may in time affect the cost of borrowing.75 This presents a particular challenge for developing countries with fossil fuels – which tend to be highly reliant on FDI and external debt and heavily exposed to volatile export revenues.

Taken together, these shifts may have implications for the speed of transition and access to finance. While MDBs and donors are increasing their climate finance commitments, the ability of the least-developed countries to access these mechanisms remains unclear. At the same time, green finance and other sustainable investment mechanisms are growing rapidly, but regulatory shifts including the introduction of BASEL III may constrain longer-term lending to emerging markets.76 This presents a challenge for investment into RE and clean energy systems, which tend to rely on capital markets for a higher percentage of their finance than upstream and thermal power investments.77 MDBs and long-term investors may help de-risk and facilitate longer-term capital where these barriers are present.