Lower-income countries that are banking on their fossil fuels lack the capacity to assess carbon risks, and may be left behind by shifts in investment and credit.

How Energy Transition is Changing the Prospects for Countries with Fossil Fuels

Research paper

Published 12 July 2018

Updated 19 November 2021

ISBN: 978 1 78413 279 8

Lower-income countries that are banking on their fossil fuels lack the capacity to assess carbon risks, and may be left behind by shifts in investment and credit.

To understand how the uncertainties described in Chapter 2 might affect fossil fuel producing countries, it is useful to review the linkages that tend to form between the fossil fuel sector and the wider economy. This chapter considers how these linkages might translate into carbon risks at the country level, with a focus on export revenues and fossil fuel supply to domestic energy and industrial infrastructure as the key dynamics. To illustrate how these risks might play out in practice, this chapter discusses some potential production, consumption and revenue scenarios for Ghana, an early stage and expanding oil and gas producer, and Tanzania, an experienced onshore gas producer with a relatively large-scale offshore gas discovery. However, these examples have broader relevance for a range of developing countries.

Well-managed fossil fuels can contribute to economic development and long-term wealth generation in a number of ways, including through:

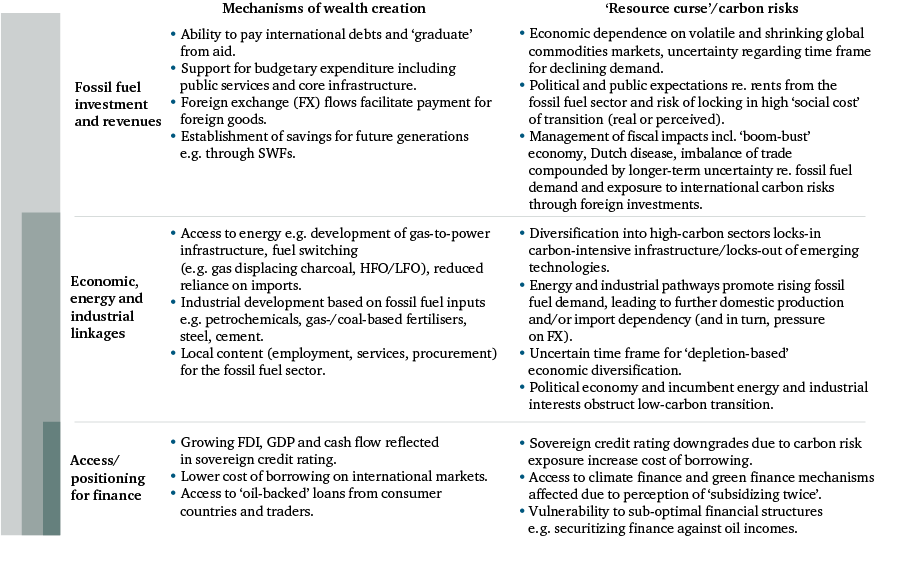

However, there is a long list of potential negative governance and economic ‘side effects’ endured by countries that come to rely on the sector, often grouped as ‘resource curse risks’ (Figure 7).79

Standard advice given to producer countries in order to avoid negative resource curse impacts normally centres around support for ‘good governance’ of the sector. This is particularly notable around the transparency of revenue and other payments to government, and where the effectiveness of fiscal measures to stabilize and invest fossil fuel revenues are concerned. As noted in the introduction, there is also now growing emphasis on the development of economic and energy ‘linkages’ between the fossil fuels sector and the wider economy. Economic linkages may include direct employment within the oil and gas sector, indirect employment in industries that supply the sector, and broader private sector development where new markets for goods and services open up as a result of incoming capital and workers. Energy linkages often focus on the utilization of associated (or non-associated) gas in the domestic economy.

The global shift to a decarbonized energy system, discussed in Chapter 2, challenges many of the prevailing assumptions that underpin fossil fuel driven development pathways. Potentially sharper declines in export markets as a result of decarbonization may translate into lower overall revenues than anticipated, reduced investor interest in new fossil fuel developments and ‘stranded’ resources and assets.80 Subsidized or ‘cheap’ domestic fossil fuel consumption and the political economy that emerges around the sector may act as a barrier to sustainable economic diversification, and undermine opportunities to harness new energy technologies and support ‘green growth’.81 These factors suggest that carbon risks have the potential to exacerbate and change the nature of many well-known resource curse risks (Figure 7).

For the reasons outlined in Chapter 2, scenarios cannot be taken as a reliable guide to the future, nor are they intended to be. Scenarios can help provide a common basis for the discussion of national development plans and the role of fossil fuel within them. They can also help bring the relevant planning and decision-making centres together, and encourage consideration of the trade-offs associated with different development pathways and the resilience of plans to gradual and more disruptive change.

Scenarios covering several decades are often drawn up by fossil fuel producing countries, or for them. They typically chart either production and revenues or production and domestic consumption, but rarely the interaction of all three. Past experience demonstrates that new and prospective fossil fuel producers tend to overestimate the opportunities presented by fossil fuel development, and underestimate the risks. These expectations may be exacerbated by the scenarios and projections produced by international organizations, development advisers and private sector partners, which often assume reliable investment and international demand, and optimistic export prices. These scenarios also often fail to factor in domestic infrastructure investment needs, and the levels of domestic demand and prices that would be required to facilitate domestic use of the resource.

Ghana and Tanzania illustrate the potential interaction between fossil fuel production, revenues and consumption under a range of credible climate scenarios.

In order to understand how carbon-related trends might intersect with common resource curse challenges in different contexts, this chapter uses simple modelled scenarios for two countries with different fossil fuel reserves and economic contexts – Ghana and Tanzania. They illustrate the potential interaction between fossil fuel production, revenues and consumption under a range of credible climate scenarios.82 A full methodology and sources for the modelled country scenarios are presented in Annex III.

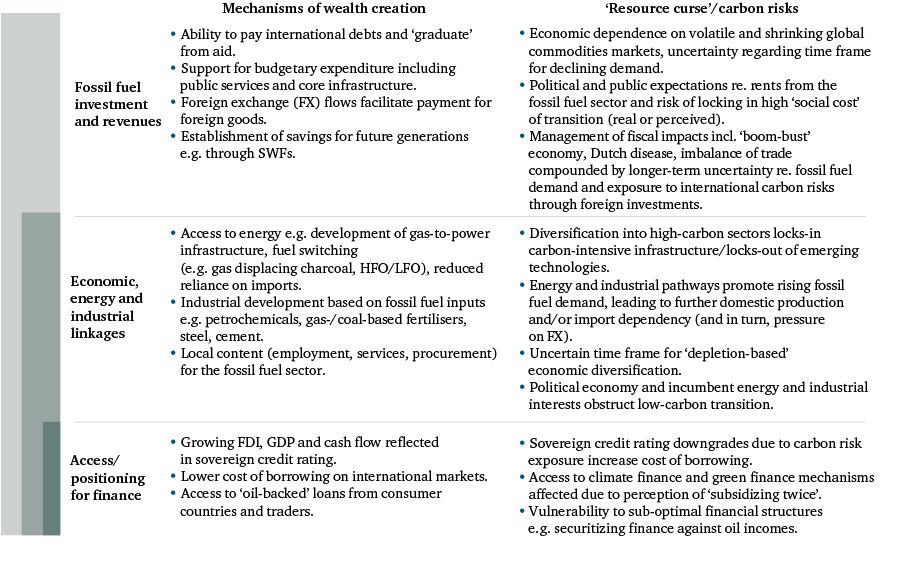

A producer government’s net revenues are shaped by the policies, regulations and contracts that guide the development of fossil fuel reserves, including the operator’s and government’s respective share of production (and related capital and operating expenditure), the fiscal regime that the operating company is subject to (bonuses, royalties, taxes), and international market demand and prices. Many of these factors – particularly contractual terms – are not publicly available. International prices, meanwhile, will be affected by a number of drivers in addition to supply and demand fundamentals, including the effect of geopolitical risk and climate impacts on fossil fuel markets (see Box 4). For the purposes of this paper, gross revenues to government are calculated as:

([Export level] × [Market price] - [Total production & transport costs]) × [Government share]

The price inputs are based on figures for market demand and costs in the TIAM-UCL model, which were cross-checked against IEA projections. Gross revenues are charted under three climate scenarios – NDC, 2D, and 2D No CCS – presented in Chapter 2 of this paper.

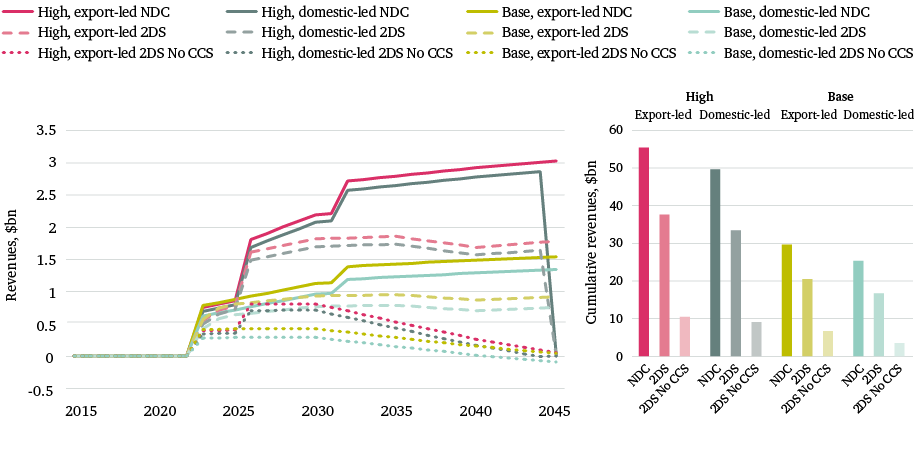

Oil production is typically exported, unless the scale of the production is sufficient to support domestic refinery activities. Figure 8 shows Ghana’s potential oil export revenues over a 30-year period to 2045. Production in a ‘high case’ – where all proven reserves are developed – could deliver a cumulative $31.4 billion in revenue to 2045 under an NDC scenario, compared to just $15.3 billion under a 2D scenario and $10.6 billion under a No CCS scenario. In the NDC, 2D and No CCS scenarios, average annual revenues stand at $1 billion, $720 million and $510 million, respectively. Production in a ‘base case’ – where only those projects that are currently under development come online – could deliver $18.9 billion under an NDC scenario, compared to $10.2 billion under a 2D scenario and $7.7 billion under a No CCS scenario. Their respective average annual revenues stand at $630 million, $340 million and $260 million. The difference between cumulative and average annual revenues in the NDC and No CCS scenarios is around 50 per cent.

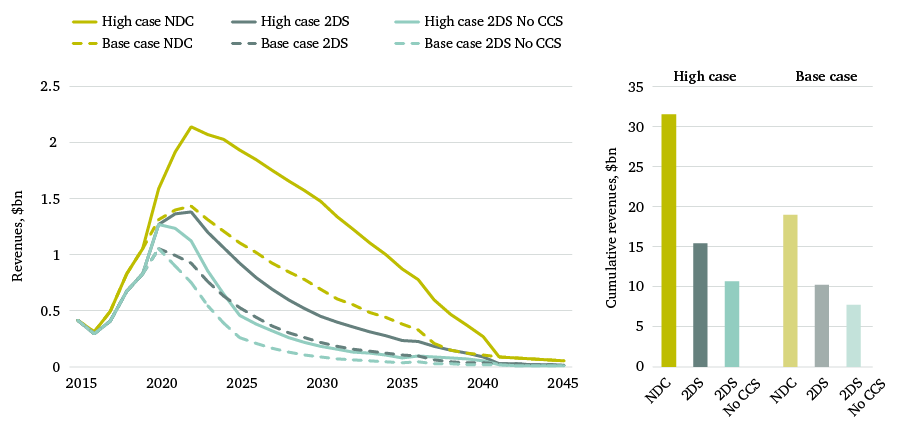

Where gas discoveries are made, governments often plan to deploy some or all production in the domestic market, where it can be made economically viable. The modelling for this paper also explored the potential outcomes for gas production in Tanzania, which has larger gas reserves than Ghana, and is at an earlier stage of production. Tanzania plans to allocate an as yet unspecified percentage of its forthcoming offshore gas production to the domestic market.

Figure 9 shows the range of potential gas export revenues. Gas production in the high case – with four LNG trains in use – could generate cumulative revenues of $49–$55 billion under an NDC scenario, $33–$37 billion under a 2D scenario, and $9–$11 billion under a No CCS scenario. These ranges depend on how production is allocated to the domestic and export markets – prioritizing supply to the domestic market results in lower revenues. Cumulative revenues differ by 80–82 per cent between an NDC and a No CCS scenario; gas exports typically incur higher production and transport costs than oil, particularly where liquefied natural gas (LNG) infrastructure is required. At the same time, gas demand is more sensitive than oil to some of the uncertainties set out in Chapter 2, particularly lower rates of CCS deployment, given its role in the power sector.

A similar pattern is evident for average annual revenues, which range from $2.2–$2.5 billion, $1.5–$1.7 billion and $410–500 million under the high case, depending on the climate scenario, and from $1.1–$1.3 billion, $750–$920 million and $160–$300 million under the base case, which assume a slower rate of production, with two LNG trains in operation (depending on how production is allocated between export and domestic markets). By contrast, in 2014, the IMF estimated that Tanzania’s revenues from offshore gas production would plateau at $3.6–$3.7 billion per year from 2029 to 2044 under a high case, and $2.5–$3 billion from 2025 to 2039 under a base case, assuming that production began in 2021,83 and that gas prices averaged around $11 per million British thermal units (MMBtu).84 The IMF now acknowledges that these projections were ‘over-optimistic’.85

A low case for production – where there is no final investment decision and Tanzania’s offshore gas resources remain undeveloped – would mean no export revenues or additional fossil fuel flows to the domestic market. While this may be a politically unpalatable scenario, there is a risk that increasing global uncertainty regarding long-term gas demand and price outlooks (see Box 4), political risk, rising project costs and difficulty accessing finance for gas infrastructure could contribute to such an outcome, especially in light of the repeated delays that Tanzania has already experienced. In such a case, Tanzania would only receive low-level revenues from the existing sale of onshore gas to the domestic market (not shown in Figure 9). This raises the importance of planning for the ‘worst case’ scenario, particularly where national energy and industrial plans are dependent on the development of domestic supply.

While sweeping conclusions cannot be drawn from a sample of two, there are two notable observations from the revenue scenarios:

There are three further observations where Tanzania’s gas revenues are concerned:

While the challenges of managing dependence on a volatile export commodity are not new, they are likely to evolve under growing carbon constraints. Through previous boom and bust cycles for commodities, it has typically been assumed that high demand and high prices will return; indeed the idea of using the downturn to ‘prepare for the next boom’ has underpinned many ‘good governance’ narratives in recent years.87 This paper’s analysis gives some indication of the potential range of revenues that may occur under three credible climate scenarios, in addition to the many other drivers of global supply and demand and, in turn, price and volatility (see Box 4). The material impact of these trends will of course be determined by the country context.

The range of possible supply and demand volumes under different climate scenarios also suggests that some oil and gas assets may go undeveloped. For instance, where new Norwegian oil production is under consideration, analysis from the Stockholm Environment Institute (SEI), suggests that only production with a break-even point of $60 per barrel or less could be commercially viable in a 2°C world (assuming that the lowest-cost fossil fuel projects come to market first).88 It is worth noting the difference between the break-even price, which underpins the decision to invest in new capacity, and the shut-in price, which determines whether to continue or halt existing production (effectively, whether oil prices cover the short-run variable costs of production).89

It seems prudent for prospective and existing producers to consider longer-term downside price and cost scenarios and plan for the ‘worst case’ scenario for fossil fuel investment and revenues.

The ‘winners’ and ‘losers’ in the race to secure investment in fossil fuels will ultimately be defined by a combination of factors, including the type and scale of resource, the cost of production, the wider investment environment (political risk, sovereign risk, cost of capital) and the likely markets a producer can lock-in. Nonetheless, it is reasonable to assume an increasingly competitive market for the remaining ‘burnable’ carbon budget, which will place marginal producers and those still at the exploration stage or awaiting final investment decisions at a distinct disadvantage, in terms of securing investment in the coming years. For these reasons, it seems prudent for prospective and existing producers to consider longer-term downside price and investment scenarios and plan for the ‘worst case’ scenario for fossil fuel investment and revenues.

The price scenarios presented in this paper provide a picture of possible long-run average and cumulative revenues, but they do not reflect shorter-term price volatility. Several dynamics will affect oil and gas prices in the short to medium term. These include upward price pressure from major producer countries, which need higher prices to support their export-dependent budgets (particularly to cover rising welfare, civil service and subsidy costs), as demonstrated by the OPEC-plus decisions (led by Saudi Arabia and Russia) to cut production in 2017/18 in order to shore up low oil prices.90 At the same time, downward pressure from commercially-produced US shale oil provides an effective ‘price ceiling’ for oil.

International contract and spot prices of natural gas exhibit much greater variance between regions than oil prices, despite still being partly linked to oil prices (although gas prices are becoming more independent with greater trading of LNG). LNG spot prices are likely to be affected by shifting supply and demand fundamentals. For example, new supplies of natural gas following Qatar’s decision to lift the moratorium on its Northern Field, and increasing LNG production from the Russian Arctic – could increase gas supply and ‘loosen’ the market in the coming few years. In the longer term, delayed and cancelled LNG investments, due to such uncertainties, may result in the market tightening up again thereafter, sending prices higher.

Other, less predictable drivers also play a role. Political decisions in major markets – such as China’s 2017 closure of coal-fired power generation in order to reduce air pollution and consolidate the domestic coal industry – will inevitably affect demand for, and thus the price of, other fossil fuels. The perception of geopolitical risk can raise the prospect of short-term oil and gas supply disruption, and prompt sporadic price volatility, as seen following the Trump administration’s announcement that the US would withdraw from the Iran nuclear deal and re-impose sanctions on Iran in May 2018.

Over the longer term, however, the fundamentals of demand will change. Rising temperatures are already increasing demand for cooling of air and water. Climate impacts – for example, extreme weather events that lead to sudden changes in energy supply or demand due to the shutdown of affected production, refineries, power plants or transmission and distribution infrastructure and their knock-on effects – could increase price volatility, while the prospect of electricity outages or fuel shortages may encourage consumers to turn to decentralized power sources for energy security. Many are now raising the prospect of spikes in oil and LNG spot prices, due to the relative lack of upstream investment in recent years and the increasing reluctance of IOCs to invest in longer-term projects.91 Demand surges would prompt importers to increase ‘national energy security’ measures (as seen following the oil price spikes of the 1970s and over the last decade), including rapidly increasing energy efficiency and RE investment, which would effectively destroy long-term fossil fuel demand.

As more fuel is diverted to the domestic economy, countries face a choice between making less production available for export, or increasing production and depleting reserves at a faster rate. This is a problem because, as shown earlier, domestic use does not typically generate the same level of revenue as exports; it is sold either at cost price (plus a margin for processing, transportation, etc.) or subsidized, in order to incentivize use (this is common with gas and LPG, but also oil fuels).92 Ghana is unusual here; its gas production, which is all destined for domestic consumption,93 has not reduced the consumer price below import costs.94 In addition, revenues from domestic sales and other taxes and duties will be in the local currency rather than foreign exchange.

This can present a fiscal challenge, as foreign exchange reserves are crucial for a county’s ability to make international payments. When a product can be exported, the more that is sold domestically, the less foreign exchange is generated. In addition, US dollars are generally the preferred payment for IOCs and foreign investors, given their low volatility and their role as a benchmark currency. IOCs and foreign investors are typically wary of investing in projects to supply the domestic market in countries with ‘non-convertible’ currencies, given the exchange rate volatility that this may expose them to. This can result in significant fiscal dependencies, with countries relying on the foreign exchange from the export commodity (LNG or crude oil) to finance gas buybacks for the domestic market.

This paper illustrates this risk by charting upstream fossil fuel production against a range of simple energy demand trajectories. These are purely exploratory and are presented in Figure 10, alongside

official demand projections (the ‘official’ trajectory). They draw on key drivers of growth (GDP, sector growth, population) and energy and technology assumptions:

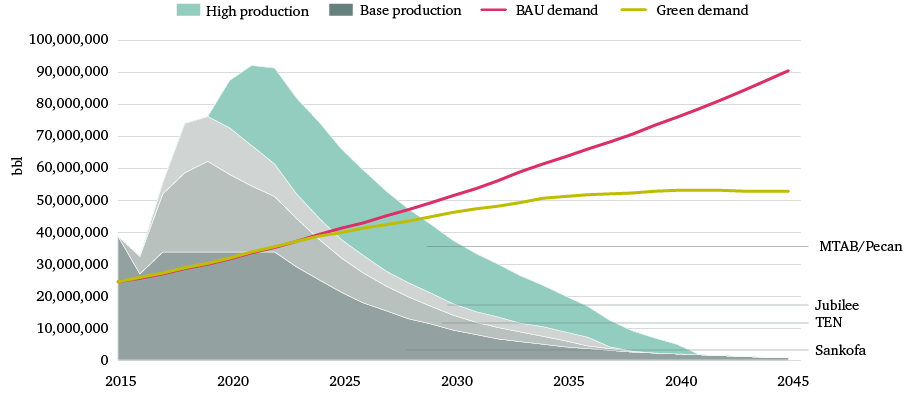

Figure 10 shows Ghana’s oil production against a range of domestic oil demand trajectories. Ghana’s imports of oil products currently meet the bulk of national oil demand, and while an expansion of its small-scale refinery capacity may supply some additional product to the domestic market, a significant increase in import-dependence is anticipated. Ghana could become a net oil importer between 2025 and 2030. At this stage, there would be implications for its foreign exchange due to the combination of decreasing production (and export revenues) and increasing demand, and thus imports. The lower ‘green’ demand trajectory, shown in green, could mitigate this over time.

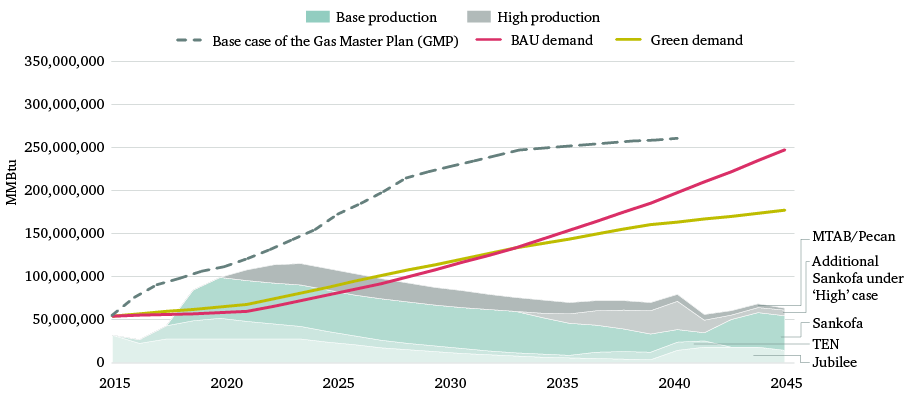

Figure 11 shows Ghana’s domestic gas production against a range of demand scenarios. It suggests that Ghana will be a net gas importer in the early 2020s (as per Ghana’s Natural Gas Master Plan), it will be able to meet its own demand for a few years as new gas supplies com online in the mid-2020s, and will then become import-dependent again from the mid- to late-2020s, as gas demand outpaces supply. While import infrastructure is in place, with the West Africa Gas Pipeline and plans for an LNG terminal, these scenarios present real energy security and fiscal stability questions. Lower and more flexible demand growth, with higher efficiency and RE deployment, could mitigate these risks by reducing import dependence and related current account stress.

Economic diversification away from the sector is now seen as the ‘litmus test’ of successful fossil fuel-led growth. For most developing countries, reducing dependence on exports of raw materials and imports of consumer goods is also a development priority. At the same time, as outlined above, development assistance to the fossil fuel sector has increasingly focused on the development of economic linkages between the fossil fuel sector and the wider economy. This means leveraging fossil fuel revenues, fossil fuel flows and the sector itself (through local employment and local content) for broad-based economic growth. For economic diversification to be sustainable non-oil sectors of the economy must become competitive without dependence on subsidized or ‘cheap’ inputs from the fossil fuel sector, before the sector’s production begins to decline.

The productive lifespan of upstream assets typically spans decades. In many cases, the inflows of revenue and FDI will already have begun to influence economic dependence at an early stage. Under ‘BAU’ conditions, there is a compelling argument that slowing production and extending the export plateau phase could help enhance wealth creation from the sector, as the government, the private sector and the wider workforce have longer to develop the necessary institutions and capacities.96 Under the most carbon-constrained scenarios, this may not be feasible; the No CCS scenario in Figure 9 shows Tanzania’s gas revenues plateauing for up to a decade (compared to 20 plus years in the NDC and 2D scenarios) and declining from 2030. These uncertainties suggest that new producers cannot afford to wait to reach full production before concentrating on stimulating economic diversification.

The prospect of declining global demand before an asset’s expected lifespan is reached could, in theory, encourage the rapid depletion of reserves. This is often described as the ‘green paradox’ effect, where countries – particularly those with larger reserves or higher-cost production – compete for what demand remains. Recent research has found little evidence of policy decisions that constrain carbon being a driver for this green paradox effect, except in a few cases of oil.97 Nonetheless, it highlights the kinds of trade-offs that governments have to consider when planning and pacing fossil fuel production – including the real cost of rapid financial inflows (including the risk of corruption and rent-seeking), and the risk of infrastructure lock-in and/or stranded infrastructure (gas, thermal power, oil refineries) against the ‘opportunity costs’ of capturing more value domestically.

Ghana’s recent experience with associated gas illustrates the impact that delays in investment and project delivery can have. Gas deliveries to the power sector and the completion of gas-fired power generation were delayed throughout 2014–15 (see Box 5). This exacerbated the power crisis (or ‘Dumsor’, meaning ‘off, on’) and led to dependence on ‘power barges’ supplied by imported fuel oil, which is an expensive and emissions-intensive fall back. It also contributed to a change of government in the 2016 elections.

Delays in bringing associated gas to the domestic market have hindered Ghana’s energy security and economic diversification and its commitment not to flare.

When the first oil contracts for the Jubilee field were signed, the intention was to allow the Ghana National Petroleum Company (GNPC) to own and process the Jubilee gas through a public–private partnership (PPP). GNPC was in talks with the World Bank and private entities for the financing of the processing plant.98 In 2008, the new government decided to set up a separate gas company, Ghana National Gas Company (GNGC), to be responsible for development of the processing plant and to manage the midstream gas gathering, processing and transportation. This delayed the implementation programme by two years, and led to the use of future oil revenues as collateral for a $3 billion Chinese Development Bank facility, $1.5 billion of which financed the gas plant.

This delay directly affected Ghana’s energy security. Load-shedding (the deliberate shut down of parts of an electricity system to prevent total system failure) has been a recurrent feature of Ghana’s power sector since the 1980s. This was originally prompted by reduced levels of water in hydro-electric dams but in 2012, load-shedding began when gas supply from the West Africa Gas Pipeline (WAGP) was cut off after it was damaged by the anchor of a ship off the coast of Benin. Had the processing plant been constructed in time, domestic gas would have been available to replace the curtailed Nigerian gas. It wasn’t, and the country faced periodic power shortages until 2015.

It also affected Ghana’s economy. First, the power crises or ‘dumsor’ is estimated to have cost the energy sector over $1 billion,99 and the wider economy somewhere between $320 million and $924 million annually through business losses, according to the Institute of Statistical Social and Economic Research (ISSER).100 Second, Ghana’s no flaring policy was suspended in 2014 and operator Tullow Ghana began flaring as it was no longer safe to continue re-injecting gas into the oil wells, and because it would begin to affect oil production volumes. Third, by financing the gas project with $1.5 billion of public debt rather than allowing private capital to come in and deliver it, the government lost the opportunity to spend on critical social investment such as education, health and infrastructure, which do not attract investment as easily. Fourth, gas revenues are affected by non-payment from power generation companies, which, in turn, are not paid by power distribution companies. Revenues from offshore gas are owed to the Petroleum Holding Fund (PHF), which was established by the Petroleum Revenue Management Act in part to help diversify the economy. According to the Auditor General, GNGC owed the PHF over $2 billion (comprising revenues and penalties) by the end of 2016.

Ghana’s experience illustrates both the difficulty of commercializing gas and the potential pitfalls in governance once interests begin to crowd around the sector. In this case, political interests overrode good governance frameworks. It illustrates the burden that may be imposed on a country when debt is used to finance infrastructure against expected future returns from the fossil fuel and power sectors. In this case, the loan taken for the gas plant continues to constrain government revenues and encourages a cycle of non-payment between SOEs: electricity distribution companies fail to pay for power purchased from the generation companies as a result of their inefficiencies and government interference with their operation, which, in turn, results in their non-payment to the national gas company and ultimately to the PHF. In this context, greater private-sector involvement could have encouraged more discipline and accountability in the power sector.

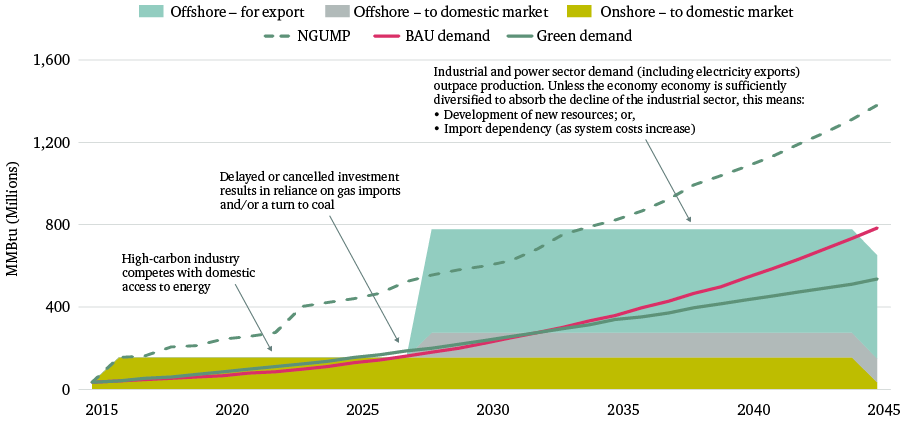

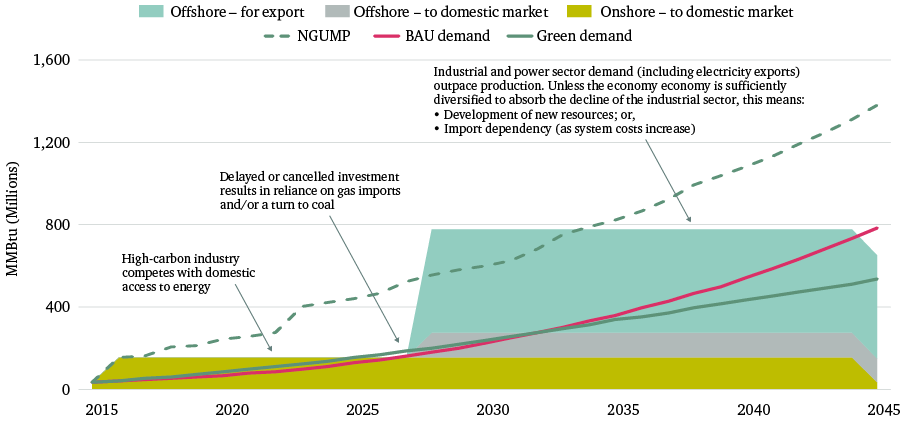

In the case of Tanzania, the country’s new offshore gas production was expected to be online in around 2015. This was subsequently delayed until 2018, as a result of global market conditions, and is now expected online between 2023 and 2025. Here again, domestic demand is likely to outstrip supply. Figure 12 illustrates the high level of demand outlined in Tanzania’s Natural Gas Utilization Master Plan (NGUMP), compared to the exploratory demand scenarios developed for this paper. Gas demand could outpace production by the late 2020s under most demand cases. It suggests growing import dependency or the risk that industry and power revert to domestic coal supplies to plug the gap.

Moreover, there still appears to be little consideration that Tanzania’s gas reserves could remain undeveloped. In a ‘low case’ for production i.e. where there is no final investment decision and only small-scale onshore production continues, Tanzania’s gas demand could surpass production in as early as 2023.

One key area of investment that links upstream fossil fuel activities with the wider economy is infrastructure. Upstream energy and industrial infrastructure has particular relevance both to economic development and to a country’s long-term exposure to carbon risks. It is also almost always a priority for developing countries when considering how best to invest fossil fuel revenues and the foreign credit that may become available during a fossil fuel boom.101 Infrastructure choices play a key role in bringing fuels to export and domestic markets; but they are capital-intensive and last for decades. They also tend to promote a level of ‘path-dependency’ where there are plans to use fossil fuel production to support growing access to energy and industrial development (where the scale of the domestic market and price of production might realistically support this).

Infrastructure including processing plants, refineries, thermal power generation and distribution, and industrial infrastructure are all set out in national development plans. Table 2 sets out the broader range of infrastructure that can require fuel as either energy or feedstock, and thus affect national energy demand and emissions trajectories. Understanding how these areas interact is critical to evaluating the extent of a country’s vulnerability to carbon and transition risks. As set out below, most of this infrastructure has direct implications for primary energy consumption and in some cases, for the use of fossil fuels as feedstock.

|

Infrastructure |

Primary energy needs |

Fossil fuel feedstock |

|---|---|---|

|

Direct implications |

||

|

Oil and gas sector (upstream, midstream, downstream) |

||

|

Drilling platforms |

Electricity |

n/a |

|

Mines and washing facilities |

Electricity |

n/a |

|

Pipelines |

Electricity |

n/a |

|

Liquefaction/gasification terminals |

Heat/cooling, electricity |

n/a |

|

Ports |

Electricity |

n/a |

|

Gas processing plant |

Heat, electricity |

Gas |

|

Refineries |

Heat, electricity |

Oil |

|

Power sector |

||

|

Thermal power plants |

Gas, coal, oil fuel |

n/a |

|

Dams and hydropower |

Water |

n/a |

|

Utilities-scale solar |

Sunlight |

n/a |

|

Wind power |

Wind |

n/a |

|

Nuclear power |

Uranium |

n/a |

|

Grids (transmission, distribution) |

Electricity |

Gas, coal, oil, RE, nuclear |

|

Industry |

||

|

Petrochemicals complexes |

Heat, electricity |

Oil, gas |

|

Steelmaking |

Heat, electricity |

Coal (coking) |

|

Fertilizer |

Heat, electricity |

Gas, coal |

|

Cement factories |

Heat, electricity |

Coal, gas |

Source: Chatham House analysis.

Note: This table is not intended to be illustrative, not exhaustive. It includes the energy/power consumption and fossil fuel feedstock required by infrastructure, but not embodied energy or material inputs. Naturally, transport infrastructure in particular is likely to use large amounts of bitumen, and most built infrastructure will require steel and concrete – both currently produced by CO2 intensive processes.

Like the upstream fossil fuel projects they rely on, large-scale power and industrial infrastructure tends to be built with an anticipated lifespan of at least 30 years and often much longer. In order to meet the ‘well below 2°C’ global target, all new infrastructure would ideally be – or have the capacity to become – carbon neutral. This would mean that infrastructure is either designed to have zero emissions in use, or that emissions are offset in some other way, e.g. through some combination of CCS, afforestation and other NETs. However, CCS is only physically viable in certain places, and is commercially and technologically out of reach for developing markets at present. The ideal approach would be to design and build infrastructure to be as energy efficient as possible, with the capacity to integrate an increasing share of RE from grid or decentralized sources.

Access to sustainable infrastructure investment represents a significant opportunity for those developing countries and regions with the largest ‘infrastructure gaps’. An estimated $90 trillion in infrastructure investment is required over the next 15 years, with annual spending of $6 trillion per year, with the global South accounting for around two-thirds of this and energy-sector investments around 60 per cent.102 As the United Nations Economic Commission for Africa (UNECA) and others have argued, ‘greening’ infrastructure from the outset – including urban energy and transport systems and industrialization – will lend these countries competitive economic advantages.103

Access to sustainable infrastructure investment represents a significant opportunity for those developing countries and regions with the largest ‘infrastructure gaps’.

The risk is that infrastructure built today will lock-in energy (and water) demand for decades unless it is replaced or retrofitted – both are far more expensive (not to mention inefficient) options than building to the best available design in the first place. It may also ‘lock-out’ new technologies and business models as they become more competitive (just as mobile phone and satellite technology bypassed conventional telecoms and banking networks in sub-Saharan Africa). Developing economies would be particularly vulnerable in such a scenario, given their plans for the rapid development of new infrastructure – typically using carbon-intensive ‘off-the-shelf’ designs – and lower economic capacity to absorb such shocks.

While the considerations above are relevant to all developing economies, they present a particularly complex set of challenges for those with fossil fuel resources. These aspirations may seem theoretical and idealistic where a government’s priority is to raise the country’s standard of living through the provision of reliable power, infrastructure (access to economic markets) and fresh water supplies, but they are central to longer-term resilience throughout the transition. The extent to which it still makes sense to explore for and develop hydrocarbon reserves will depend on the type of oil or gas and its likely export markets, the scale of the resource and the cost of development, as well as its impact on land, water and other resources for socio-economic and environmental services.

In summary, the development of fossil fuels can result in linkages to the rest of the economy that heighten ‘carbon risks’ at the country level. The greater range of uncertainty around investment and revenues and the prospect of a declining export market is likely to change the value proposition for emerging and early-stage producers that have embarked on production or are considering expansion of the sector.

The scenario analysis reveals several issues that are likely to be of concern for producer countries:

Scenarios such as those conducted for Ghana and Tanzania can help plot the interaction of production, domestic consumption and revenues under different climate scenarios. Although beyond the scope of this paper, they would ideally be supplemented with implications for emissions and other quality of life indicators.

Such exercises could be used to bring together several areas of strategic planning in a country in order to ‘carbon-stress test’ national plans relating to revenue management, energy and industrial policy, and the fossil fuel sector itself. They could also help better decision-making in terms of whether to develop or expand the fossil fuel sector in the first instance, in light of alternative options for revenues, access to energy and economic growth.

Above all, the scenarios strongly suggest that developing countries expecting significant development gains from fossil fuel production urgently need new information, capacities and governance approaches that can challenge the short-termism of political cycles.