Lower-income countries that are banking on their fossil fuels lack the capacity to assess carbon risks, and may be left behind by shifts in investment and credit.

How Energy Transition is Changing the Prospects for Countries with Fossil Fuels

Research paper

Published 12 July 2018

Updated 19 November 2021

ISBN: 978 1 78413 279 8

Lower-income countries that are banking on their fossil fuels lack the capacity to assess carbon risks, and may be left behind by shifts in investment and credit.

All countries need to adapt to carbon risk. As set out in Chapter 2, this is a rapidly evolving area for policy and finance in the advanced economies of the OECD, which is being driven in many cases by the investment and regulatory communities. To date, developing countries have had little engagement in this conversation. They are also likely to have lower institutional and technical capacities and fewer resources to develop carbon risk assessments and incorporate their findings into policymaking. Many will have limited capacity to plan for the long-term future, appraise investments and make sound cost-benefit analyses as they try to deliver basic services for their citizens. Some face severe capacity constraints due to conflict or endemic corruption.

In this chapter, we set out the considerations and policy areas for responding to challenges described in Chapter 3, bearing in mind that different countries will have different entry points into this process, and that success will depend on a government’s willingness to engage on long-term issues, and on development assistance to address gaps in information and capacity. The stage of opening up or developing reserves matters in terms of what choices are on the table and where the focus should be.

Efforts to build resilience to carbon risks will stand the best chance of success if efforts are pursued through existing policy frameworks and framed by national priorities. For countries that are exploring for oil and gas and those that are about to begin or expand production, weighing up the trade-offs, opportunity costs and options for alternative development is critical. For those already producing, the role of revenues, the allocation of production, the ability to manage domestic demand and decarbonize the domestic energy mix, and the sustainability of infrastructure choices are all important tools for limiting exposure to carbon risk.

Drawing both on the findings of the scenario analyses in Chapter 3 and discussions with country stakeholders, there are three key areas for better information and capacity-building to emerge:

For countries that have made the decision to explore for or develop reserves, effective management of the revenues and other payments associated with the fossil fuel sector is the first challenge. This means planning for the future and taking into account the potential delays in receiving any revenues – for example, a large-scale gas-to-power development may not deliver any significant returns for 10–15 years, given the fiscal terms agreed for companies (in terms of recouping their costs). During that time, public expenditure (including the payment of international debt) can become increasingly dependent on the sector, presenting obvious fiscal risks and creating a barrier to sustainable diversification and low-carbon transition. This raises two questions:

In order to address these questions, central economic governance institutions including central banks, ministries of finance and those managing sovereign wealth funds (SWFs) should incorporate carbon risks and transition strategies into their long-term outlooks and planning from the earliest possible opportunity. They could begin by studying the implications of carbon linkages on fiscal stability over time, including budgetary dependence, the current account impacts of rising fossil fuel demand and infrastructure investments, and the sustainability of external debt, in the ‘worst-case’ scenario for fossil fuel demand.

Revenue distribution is often a point of political contention. Fossil fuel revenues should not be classed as ‘income’ but as ‘reshuffled’ assets: cash assets in return for depleting below-ground assets. For fossil fuel development to be worthwhile, some revenues must be used to stimulate economic activity and/or investment that will sustain the economy beyond reserves depletion or a declining market price.104 The shift to a decarbonized economy, and the narrowing window for wealth creation from the sector, increases the importance of effective revenue management, and accountability for the sector’s impact. Existing guidelines for the saving and spending of revenues, both regularly through the national budget and ad hoc capital expenditure, may need revision in view of decarbonization trends.

Developing some level of national consensus over long-term economic priorities, alongside setting performance measures over time, would help to establish how spending is contributing to priority areas and demonstrating gains in diversification. In Ghana, there is interest in how to direct revenues so that they stimulate market growth in key employment-generating areas like agriculture and tourism, both of which can be well-aligned with a ‘green growth’ pathway. For example, investment in Ghana’s agriculture might have eliminated the country’s rising import bills for basic foodstuffs, such as rice, which can be grown domestically. Investment in energy efficiency and the RE sector is another, perhaps obvious growth area. According to one workshop participant, ‘Given the existential threat faced by the fossil fuel industry, it would be wise to invest the proceeds in the alternative industries that are likely to replace fossil fuel as an energy source’.105

Well managed fossil fuel revenues could, in theory, provide a source of revenue for NDC implementation and support a wider ‘green growth’ strategy at home while production is exported. However, this conflicts with the traditional ‘fossil fuel-led’ development pathway, which emphasizes the development of linkages between the fossil fuel sector and fossil fuel-based value chains. It also assumes that revenues will flow in time to support transition, when in reality, governments often see little return from the sector until a decade or more after ‘first oil’. Nonetheless, given the right context, growing carbon risks and the competitive advantages of a green growth pathway might make this an attractive option for some countries (see Box 6).

At the Guyana National Seminar of the Chatham House New Petroleum Producers Discussion Group in June 2017, Minister of Natural Resources Raphael Trotman and Minister of Finance Winston Jordan both re-affirmed a national development vision for Guyana that was green and sustainable. The origins of this vision lie in Guyana’s long history of forest conservation and its economy, which is driven by agriculture and mining, with some light manufacturing. Guyana has the world’s second highest percentage of rainforest cover (85 per cent) and one of the lowest deforestation rates on Earth, making it a globally important carbon sink, storing some 5.31 gigatonnes of carbon.106

Guyana is also home to some of the world’s largest oil discoveries of recent years. Since 2015, major oil discoveries by Exxon Mobil and partners have confirmed over 3 billion barrels of oil offshore, and this figure may still rise, with ongoing active exploration. Oil production is expected to begin in 2020. At the same time, Guyana currently relies on imported fossil fuels (largely from neighbouring Trinidad & Tobago) for most of its power generation. Electricity demand grew 18 per cent in 2010–15, despite the volatility of imported fuel prices and some of the highest retail electricity rates in Latin America and the Caribbean. Expectations of benefits from fossil fuel production are now growing among Guyana’s small population of less than 800,000.

As President Granger put it, Guyana’s vision is to develop ‘a petroleum economy and a green economy, walking side by side, neither contradicting nor dominating one another’.107 The key question is how oil development might influence Guyana’s ‘green’ vision. Both its NDC and national development plan set out specific measures and a low-emission economic-development pathway to a ‘green economy’, including the target of developing a national energy system that is 100 per cent renewable by 2025 (supported by the country’s ample wind, solar, biomass and hydropower resources), and commitments to mangrove restoration and avoiding deforestation. Delivering Guyana’s ‘green’ vision will require careful assessment of the trade-offs associated with different energy and economic development pathways.

Oil revenues could, in theory, enable Guyana to fund many of the programs contained within its NDC and its wider green-growth agenda, including affordable access to energy. Guyana is planning to establish an SWF that will benefit future generations, as well as protect government spending against volatile commodity markets, and support spending to meet the country’s urgent development priorities. Given its small population, geography and economic structure, Guyana could pursue an alternative development path to the traditional high-carbon industrialization model. In this context, ‘greening’ budgetary expenditure and the SWF may help enhance Guyana’s management of carbon risks, while also delivering shorter-term clean energy and green growth goals.

At the same time, oil development has raised major infrastructure questions, including whether the development of joint refinery and industrial projects with neighbouring Suriname could boost economic activity, and whether the domestic use of associated gas for domestic power generation might be technically and economically feasible. However, unless carefully designed, the former risks locking-in high-carbon industrial activities, while the latter is incompatible with Guyana’s ambition to use 100 per cent RE by 2025. However, acting upon robust analysis of the carbon risks and low-carbon opportunities associated with different energy and industrial pathways, particularly around revenue management and industrial infrastructure will demand strong political leadership.

Note: This box draws upon the Chatham House New Petroleum Producers Discussion Group Workshop ‘Managing Resources Post-Discovery’, which was held in Georgetown, Guyana in June 2017. A wider workshop summary is available at: https://www.chathamhouse.org/sites/files/chathamhouse/publications/Meeting%20Summary%20-%20Managing%20Resources%20Post-Discovery.pdf.

Diversifying the economy based mainly on cheap inputs of domestic fuel is likely to result in fiscally unsustainable, high emitting industries. These can ‘crowd out’ other sectors and reduce productivity and competitiveness across the economy, including the areas where most citizens work, often agriculture. Surprisingly little of the literature on avoiding the resource curse and good governance has focused on getting the appropriate tax system for a country in place. Yet this is vital to supporting a diverse set of sustainable, competitive industries outside of the fossil fuel sector. Where revenue allocation is designed to promote other areas of the economy, this should be complimented by ongoing efforts to broaden the country’s tax base and increase professionalism in this area.108

Ministries of finance, revenue authorities and other entities that shape fiscal policy will benefit from growing their competency in accounting for carbon.

Ministries of finance, revenue authorities and other entities that shape fiscal policy will therefore benefit from growing their competency in accounting for carbon. Donors and development financiers will increasingly apply a carbon price in screening projects for financing eligibility. In addition, a growing number of emerging economy governments are deploying carbon pricing instruments (taxation and other levies as well as trading), including large fossil fuels producers China, Colombia, Kazakhstan and Mexico, as a way to account for externalities, drive green growth and provide a source of additional revenue.109 For a less developed country, this may begin with applying ‘shadow pricing’ to accounting, forecasting and performance indicators.

Building these capacities will not only help prepare for access to finance but also for potential application of carbon pricing mechanisms. Many existing measures in developing countries already implicitly put a price on carbon, e.g. duty taxes, fuel taxes, subsidies, feed-in tariffs and other green incentives. A 2017 Carbon Pricing Leadership Coalition meeting with sub-Saharan African countries, for example, highlighted how alignment of these with carbon pricing instruments could speed up NDC implementation but would require ‘a good data basis and specific sector expertise to understand the dynamic interaction between carbon pricing and other green policies.’110 Learning from other countries experimenting with tax, pricing and trading systems would help countries to find the best fit for their society.

Many fossil fuel exporters have developed some form of SWF in order to insulate the economy from price volatility in the short-term and support future generations in the long-term.

Stabilization funds can help countries manage price volatility and declines. Recent experience suggests that developing producers with heavy dependence on a single export commodity and high levels of public expenditure and external debt have been quick to raid these funds during times of low prices (e.g. Nigeria’s Excess Crude Account). Ghana’s stabilization fund, although designed and implemented with the best technical advice and capacity-building, was not sufficient to cushion the 2015–16 drop in export revenues. In a cyclical market with booms and busts, well designed and well managed stabilization funds should be sustainable. However, in a declining market, repeated draw-downs may leave producers in an increasingly vulnerable fiscal position over the years.

Sovereign wealth fund investments in fossil fuel and other high-carbon assets effectively represent a ‘double exposure’ to carbon risk through a country’s international investments.

The international investment of revenues also warrants attention, in light of wider divestment trends. SWF investments in fossil fuel and other high-carbon assets effectively represent a ‘double exposure’ to carbon risk through a country’s international investments. For those starting out, there is an opportunity to follow the lead of the world’s largest SWFs and pension funds from the outset. As set out in Chapter 2, many of these actors are now moving to divest from fossil fuels and diversify their portfolios. Effective management of carbon risk through the SWF requires effective partnerships between the leading institutions in-country – the central bank or ministry of finance, for instance – and where applicable, their international investment managers in order to develop and implement ‘best in class’ strategies for the sustainable investment of the SWF, including diversification and divestment from international assets that are at risk of losing value through the energy transition.

Countries should also consider the extent to which investments can help support domestic transition. In an era of low-interest rates, countries that have traditionally invested a percentage of their fossil fuel revenues in international markets are re-assessing their investment strategies. Some have questioned whether a different investment strategy – for example by investing at home in sustainable infrastructure or the protection of assets through forest conservation and afforestation – could deliver better returns in the long run. However, countries relying on raw materials export are often subject to volatile currency exchange rates meaning that keeping a reserve in a more stable currency can increase economic security.

For some countries, oil and (more often) gas supplies may also be available to the domestic economy. Effective management of these fuel supplies and their role in the economy can reduce exposure to carbon risk and support decarbonization over time.

Countries need information and planning capacity ahead of that time, in order to head off unrealistic expectations. When fossil fuel resources are discovered, there is a tendency for politicians and industry alike to ‘crowd around’ the resource and compete for access to the perceived political or competitive advantages that rents and cheap inputs might confer. In the case of gas, national ‘master plans’ frequently highlight a role for gas across the domestic power sector and multiple industries, but rarely examine this against overall fossil fuel supply or the required investment. This ‘supply-led’ approach tends to result in over-inflated expectations of the role that fossil fuels can play in the economy and potentially detrimental competition between sectors for fuel (e.g. between power and industry).

Moreover, the ‘competitive advantage’ that the use of domestically produced fuels might confer is changing rapidly with the diversification of the global economy. Developing the value chain domestically and building economic linkages with the rest of the economy (mainly through power and energy intensive industry) has become part of the received wisdom for producers since at least the 1970s. However, the countries that have made a success of this, such as the Gulf Cooperation Council countries and Trinidad and Tobago,111 are now facing challenges with respect to sustainable diversification and job creation mean a reassessment of this model is needed.

This raises two important questions for country decision-makers:

As discussed in Chapter 3, energy and industrial policy and national development plans have a major role to play in shaping these two dynamics.

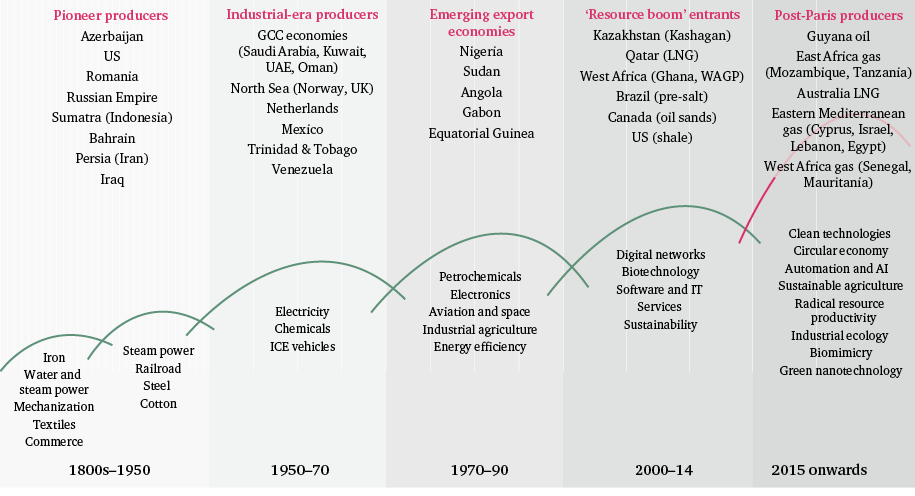

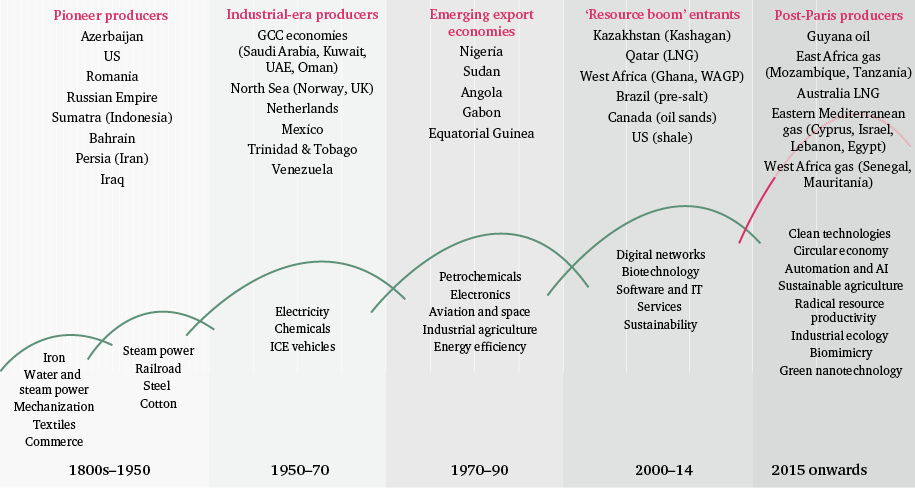

The continued viability of fossil fuel-led industrial plans warrants greater scrutiny. Industrial innovation comes in waves, shaped by wider macroeconomic trends. Figure 13 shows the emergence of new oil and gas producers on each wave of innovation and global structural transformation. Emerging producers may have an opportunity to leapfrog traditional industrial value chains, and avoid the development of high-carbon industries that entail exposure to carbon risk, as well as ‘crowding out’ agriculture, light manufacturing, services and other industries that can support sustainable economic diversification. Greening industrialization and ensuring compatibility with long-term 2050 plans can also help avoid the need for expensive retrofitting or the retirement of carbon intensive infrastructure down the line.

In the case of Ghana, despite initial optimism, gas-based industries do not appear prudent given the scale of the resource or the time frame for production. While a number of government and industry leaders interviewed in Ghana, in late 2016, expressed hope that gas would be used in power (including exports to regional neighbours), petrochemicals, fertilizers and transportation,112 the updated Gas Master Plan (GMP) of 2016 is more measured in its expectations for gas use in the domestic economy. Ghana’s Ministry of Energy estimates that gas-based industries might be commercially viable within a gas price range of $9–$12/MMBtu, effectively ruling out the use of domestic gas in urea, steel and aluminium industries, and casting doubt on its prospects for use in methanol and transport.

By contrast, Tanzania maintains ambitious plans for the development of heavy industry fuelled by domestic gas (and coal). The expectation is that electricity will account for the bulk of fuel demand in the short-term and that nascent industrial sectors – including steel, cement, chemical fertilizer and petrochemical industries – will be supplied by the surplus. Politically, these industries appear attractive; steel industries could add value to domestic iron ore and coal production, and supply emerging urban national and regional demand centres, while the development of a fertilizer industry could create linkages to the agricultural sector, and enhance its productivity and employment prospects. This is dependent on a final investment decision from their international investors, and a range of factors including domestic fuel pricing and export potential in a market where established lower cost producers have a surplus (e.g. Chinese steel, Gulf and Chinese petrochemicals).113

While it is hard to imagine any way in which developing domestic coal supply could contribute to NDC goals, there are, in theory, ways that the oil and gas sectors could play a role. For example, there may be opportunities for domestic gas production – and liquid petroleum gas (LPG) processed from gas or crude oil – to displace higher-carbon or more environmentally-damaging energy practices, namely coal for heat and power and biomass for cooking. Where there is ‘associated gas’ from existing oil production, utilization may also present an opportunity to eliminate flaring.

The utilization of fossil fuels in the domestic market carries significant costs. Natural gas discoveries may require prohibitive capital outlays and intensive policy efforts, particularly where there are no associated oil exports to help guarantee a government’s ability to finance the initial capital expenditure required in domestic gas-fired generation and grid infrastructure, and the operating expenditure to pay for gas supplies. Most developing countries require large-scale development assistance in order to access the foreign capital and technical expertise required to implement and operate such gas projects. In the case of cooking fuel, key considerations include the extent to which the government should subsidize gas prices to reduce deforestation, and the necessary reforms to sector regulation and the wider business environment that would be required in order to support the effective marketing of LPG as an alternative to firewood or charcoal (see Box 7).

Many countries shown in Figure 1 are suffering from high rates of deforestation. Most of their NDCs emphasize forest preservation and afforestation as a contribution to climate change mitigation in terms of reducing emissions from land-use change and providing ‘carbon sinks’. Thus, there is strong interest from emerging fossil fuel producers in how LPG and natural gas might displace wood and charcoal use in cooking, which is a contributor to deforestation.

Since at least the 1980s, the transition in cooking practices from basic fuels to more advanced and cleaner methods has been perceived as a move up the ‘energy ladder’.114 This is usually understood as households moving from dung and waste to firewood to charcoal to kerosene to LPG/biofuel, and finally, to electricity. To date this movement has been slow; the global SDGs and the Sustainable Energy for All (SEforAll) initiative are promoting a much faster transition from biomass to ‘tier 3’ fuels (LPG or second-generation biofuels), as this change promotes access to energy, health, and forest conservation benefits.

The use of LPG – propane, butane or a mix of the two that must be refined from crude oil liquids or natural gas – has taken off in countries across western Asia and parts of Southeast Asia and South America, which used to be dependent on biomass. It also holds promise as an alternative to wood and charcoal use in both Ghana and Tanzania, if infrastructure and pricing can stimulate demand. Like most countries where the majority of cooking uses biomass, both Ghana and Tanzania have a history of shortages and disruptions in LPG supply, as well as poor investment in infrastructure, packaging and safety, despite efforts to encourage LPG through subsidization. Problems include both limited availability of LPG to private sector retailers, and a lack of standardization and regulation.

For an LPG market to succeed and displace other fuels, a number of barriers must be addressed. The relative price of current fuels and LPG is critical, but there are other considerations. Many of the cooking fuels used among the poorest communities are collected biomass, which may not incur a monetary cost, but are time consuming to collect – mainly for women and girls. Therefore, stimulating LPG demand may require a broader approach.115 There are often cultural preferences for cooking with wood or charcoal, but equally there may be social incentives for switching, including cleaner living areas, less time spent collecting wood and clearing away soot, and the status associated with having a gas stove; all of which need to be recognized in any large-scale plan for LPG. Enabling the adoption and use of LPG stoves is critical in supporting long-term LPG use.116

There are also various critiques of the energy ladder hypothesis that deserve attention. Several studies have found that households will rarely make a complete shift from wood fuel to LPG and transitions may not be linear. Instead, LPG adoption often has a strong correlation to other socio-economic improvements and associated household upgrades, as well as changes in community conditions, such as improved road access.117

There is clearly the need for change in cooking practices in many countries that need to reduce deforestation. The use of domestic natural gas or oil as a cooking fuel is worthy of attention as an SDG enabler, and where wood fuel for cooking is a major challenge to forests, as an NDC enabler. But it must take into account the trajectory of natural gas/crude oil condensate availability, the timing and expense involved in domestic processing, and the likelihood of a return to imports after a period of self-sufficiency. At the same time, LPG may face competition from advances in solar cooking technologies that may result in their wider use alongside other cooking fuels and sustainably managed forests.118

A successful programme to transform practices must therefore consider and be prepared to finance a long-term, holistic approach. There should be no illusions as to the costs, times and effort involved. Multiple government agencies and the fossil fuel industry need to coordinate; initial investment must be ploughed into the distribution infrastructure and in getting the right cooking equipment to markets. Furthermore, culturally-appropriate awareness and training are needed at the local level to foster demand and ensure safety.

Gas should not necessarily be considered a ‘transition fuel’ in the switch to a low-carbon economy. Plans for the domestic use of natural gas need to be carefully interrogated in view of infrastructure costs, fuel prices, electricity tariffs and the capacity of the main off-takers to pay for the product – all of which present major challenges to the power sector in a less developed country context. They also need to be considered in light of technological advances and falling costs in energy storage; in Australia, for example, Tesla’s deployment of a 100MW battery has helped overcome gas power outages and price spikes.119 The company is also developing the capacity for ‘virtual power plants’ in post-hurricane Puerto Rico, Australia and Lebanon, with the installation of batteries in networks of up to 50,000 homes.120 Meanwhile, the rationale behind the use of gas as a balancing fuel for intermittent RE is questionable amid the wider shift from rigid baseload power to more flexible systems of energy delivery.121 In terms of emissions comparisons, methane leakage from gas projects must be also taken into account when considering the merits of gas as a ‘lower carbon’ transition fuel.122

Box 8 gives some of the key considerations and capacities for guiding the use of natural gas – and other fuels – in the domestic economy with reference to the experience and ambitions in Ghana and Tanzania.

Given the experiences and plans for development in Ghana and Tanzania, several considerations and competencies stand out as essential for making decisions about the gas sector and guiding the use of gas and other fuels in the domestic economy:

Infrastructure costs: A full understanding of the costs, timing and sequencing of putting in place measures for capture and utilization of associated gas is critical for effective decision-making. When gas is not delivered on time, it may lead to higher costs and higher emissions from emergency measures, such as power barges or increased fuel imports, as seen in Ghana. As Ghana’s Gas Master Plan (GMP) acknowledges, it is ‘faced with substantial challenges in the provision of new infrastructure in the coming years and is therefore unlikely to be able to meet all investments required under the GMP’.123 Tanzania’s 2016–45 Natural Gas Utilization Master Plan (NGUMP) is far more aspirational – its NGUMP projections for gas use are difficult to envisage, given the capital required for the necessary power, industrial and transportation infrastructure. It is currently being revised.

Fuel pricing: The pricing of fuel is a critical factor in domestic energy consumption and the transition to a diversified, low-carbon economy. To incentivize low-carbon pathways, where fuel substitution is considered, the consumer price of an alternative fuel has to be high enough to make investment in infrastructure and processing commercially feasible, yet low enough to ensure it is used instead of less efficient fuels, such as diesel, wood, charcoal and coal. Unlike oil, natural gas requires extensive infrastructure (processing, pipelines, gas turbines, city gas networks, compressed natural gas (CNG) stations etc.) in order to create demand. The international price plus transportation cost may not be appropriate as a reference price for domestic sales of gas, given the investment needs of domestic gas infrastructure, local costs of production and the relative value of this sector to national industrialization, poverty alleviation, and energy access objectives.124 It is important that countries have access to the full costs of production (including emissions, water demand and depletion costs). The ability to ‘price in’ carbon (as mentioned earlier) and other emissions will be useful in this regard, even if the full cost is not immediately applied to the domestic fuel price.

Electricity tariffs: The level of electricity tariffs can have an impact on consumer fuel choices. This was demonstrated in Ghana in 2016 when electricity tariff reforms were introduced. These reforms were generally considered ‘a step in the right direction’ by government technocrats; however, they were not without controversy, and were considered a ‘step too far’ by others. Larger consumers such as hotels and factories responded perversely to the tariff reforms by using their allocated lower tariff blocks from the grid and then switching to their own diesel generators, which were less expensive per kilowatt hour (kWh) than the higher tariff blocks. As a result, demand for power through the national grid was said to have fallen by 25 per cent, causing further revenue generation problems for suppliers.125 In 2018, the government partially reversed the tariff reforms to address these misaligned incentives.

In addition to costs arising from distribution losses and other inefficiencies, and the inflated costs of new power plants (ostensibly due to uncompetitive practices), the inflated costs of new thermal power plants, ostensibly due to uncompetitive practices, also contribute to high systems costs. According to one workshop participant, ‘It should have cost $120 million for a 100MW plant but [the government] has paid twice that, and now the consumer is paying for that’.126

The scenarios in Chapter 3 highlight the importance of a country maintaining export flexibility by steering domestic energy demand away from dependence on domestic fossil fuel supply. Once dependent on fuel supplies, domestic energy demand growth can compound current account stress in a number of ways. Energy policy can deploy several levers to ensure fuel is efficiently allocated, and incentivize transition over time including target setting, establishing the right price regimes to incentivizing cleaner, more efficient practices, and gradually taxing higher-emissions fuels and using the revenues to invest in low-carbon public goods, such as mass transit systems. In particular, demand-side interventions, including exploiting the most efficient and cost-effective technologies and systems can help reduce current account stress, enhance energy security and support NDC implementation.

Regulators and planners tend to express strong interest in keeping up with rapidly shifting technological advances, pricing and business models, which will affect the competitiveness of different energy sources and technologies over time. This area is rich for discussions at the outset of plans to develop or expand fossil fuel production to ensure that there is sufficient emphasis on energy policy and integration with sustainable energy goals. A professional, independent electricity or energy regulator has been critical in several fossil fuels exporting countries (Oman, Saudi Arabia, South Africa, UAE) in driving programmes to increase power and water efficiencies to rein in the waste of fuel.127 It can also help create an investment infrastructure and operating environment to take advantage of new practices and technologies and scale the use of RE over time. If one does not already exist, at least as much effort should be directed into developing this institution at the outset of a discovery as goes into developing an NOC.

A greater focus on demand can help shift the emphasis of energy discussions in fossil-fuel producing countries from a supply-led approach to a demand-led energy services perspective. Energy policy and investments should prioritize the end goal, e.g. reliable and affordable access to clean energy services, rather than the means, e.g. development of the fossil fuel sector. This may provide something of a counterbalance to the political economy and ‘path dependency’ that tends to emerge around the development of a fossil fuel sector.

There are also great opportunities to scale up energy efficiency, RE systems and sustainable infrastructure where a pipeline of ‘bankable’ projects can be developed, and where the right combination of climate or concessional finance, green finance and other support can be secured. Those countries with the most stable and competitive regulatory and legal frameworks governing investment in the power sector and infrastructure will be best placed to attract such investment as the experiences of RE in South Africa and Uganda demonstrate.128 With a demand-side focus, understanding the end consumer of power becomes key. The planned roll out of electricity metering in Nigeria, for example, is expected to increase utilities revenues and thus enable needed investment as well as increase investor confidence in solar power.129

Looking ahead, urbanization and industrialization trends can be exploited as an entry point to help ‘shape’ future energy demand, through smart urban planning and the procurement of the most efficient, low-carbon designs and materials. Such structural shifts, for instance the rural–urban spread of population and the rate of urbanization over time, will be important in decisions on expansion of grid power, and whether gas could effectively displace wood and charcoal use, for instance. The procurement, financing and delivery of sustainable urban and industrial energy systems and related infrastructure are key areas, and are rich for South–South learning, facilitated by MDBs and donors.

The institutions that manage and operate in the fossil fuel sector, including the ministry of petroleum, the upstream regulator, the SWF and the NOC, can all develop in ways that either help or hinder carbon risk management and green growth. As set out in chapters 2 and 3, while the overall implications of the global carbon budget suggest less investment in fossil fuels, the prospects of different fuels varies depending on their specific carbon intensity factors.130

Almost all major IOCs are considering how to extend their profitable lifetime and find competitive advantages, as demand for their current primary products declines.

Almost all major IOCs are considering how to extend their profitable lifetime and find competitive advantages, as demand for their current primary products declines. In contrast to IOCs, where strategy is influenced by the need to return fairly short-term dividends to shareholders, NOCs have a special role as the government is its only or largest shareholder and they are usually established with a mandate to serve national interests. For these reasons, NOCs should experience less conflict of interest in planning for transition. In reality, NOCs often develop without much connection to other national goals and processes, and are sometimes captured by a group of elite interests. They often have ambitious growth targets, including taking a greater share of (carried) equity in projects, and even developing operational competencies.

This raises important questions about how, from the outset, the right incentives can be set, and the right capacities and interlinkages built, to ensure that state entities are able to concentrate on their core task, while avoiding exposure to carbon risk and supporting transition.

This paper sets out a number of uncertainties that decarbonization trends present for national governments. Actors in the upstream fossil fuel sector are used to dealing with risk.131 These risks fall broadly under three categories: the risk associated with exploration, i.e. that drilling fails to make a commercial discovery, and therefore generate a return (‘prospect’ risk);132 the risks associated with upstream contracts (contract risk);133 and, the risk that changes in the project (operating costs, accidents) or international context (demand, prices) affect the development of a discovery or the returns of a producing asset (commercial risk).

Governments are exposed to some level of risk through their share of revenues or through the changing prospects for exploration or development where there are proven reserves. In general, upstream contracts have developed over the past few decades, so as much risk sits with the operator and away from the state. They are typically structured so that exploration costs are borne by a company, as are the costs and risk of development, if there is a discovery.

Disruptive shifts in international prices may affect the perceived ‘fairness’ of contracts, raising the prospect of parties reneging on sales (off-take) contracts, for instance; although this risk tends to sit with the operator.134

The establishment and mandate for an NOC should therefore be re-considered in light of growing carbon constraints, and wider national development goals. This could include a role concerned with maximizing the value of fossil fuel assets to the country, but also with optimizing their role over time. The distribution of risk between the state (and public finance) and the private sector should be carefully considered, where re-investing in the upstream and developing operational competencies are concerned. For example, where the government share of revenues is delayed until after the private investor has recouped their capital, this may effectively increase the costs and reduce the returns of governments.

Many established NOCs are now re-considering their long-term commercial strategy and national mandate, in light of the decarbonization trends. Evolution of the NOC as a ‘manager of carbon’ may be an appropriate role for some. This includes developing the skills to understand consumer preferences in their export markets, and shifting international investment patterns. Pursuing a long-term transition from an NOC to an ‘NEC’ (national energy company) may be an attractive proposition for others. Just as many IOCs are attempting to build their RE and clean technology investments and capacities, so too are established NOCs such as Saudi Aramco. However, such strategies should be underpinned by a robust national conversation about the most appropriate institutions and processes to promote the integration and scale-up of RE and other clean technologies.

Building capacity within the ministry, regulator or NOC represents a first step towards managing emissions (including methane) and carbon risk. Some competencies, such as reducing the life-cycle emissions of their products, and the monitoring and enforcement of efficiency and RE standards in the sector will likely be owned by the leading institutions in that area. Others, such as the application of shadow carbon pricing, will have relevance across the energy system and wider economy, applying to both upstream decision-making and (where production is to be allocated to domestic market) power sector stakeholders and national planners, among others. The associated skill sets are also likely to be in increasing demand across the domestic economy and internationally (as mentioned earlier).

Using NOC and government licensing and procurement power to stimulate the domestic market in low-carbon products and services is another area for consideration. The fossil fuel industry is usually a significant energy consumer. Particularly where there are local content measures, where competitive, how could it promote energy efficiency services and the deployment of RE technologies within the sector, and set procurement standards for sustainable infrastructure that take into account long-term emissions reductions? Other considerations involve industry-related infrastructure, the procurement and deployment of which can contribute to green growth sectors of the economy.

Peer-to-peer networks with more established NOCs such as those in the Gulf and East Asia can help accelerate learning at the technical and policy and strategic level. MDBs, donors and other development advisers to the sector have a role to play in facilitating such platforms.