Lower-income countries that are banking on their fossil fuels lack the capacity to assess carbon risks, and may be left behind by shifts in investment and credit.

How Energy Transition is Changing the Prospects for Countries with Fossil Fuels

Research paper

Published 12 July 2018

Updated 19 November 2021

ISBN: 978 1 78413 279 8

Lower-income countries that are banking on their fossil fuels lack the capacity to assess carbon risks, and may be left behind by shifts in investment and credit.

All MDBs and donor countries are committed to the long-term goal of the Paris Agreement, and have rapidly scaled up their climate finance commitments in the last decade. Reforming development assistance to the fossil fuel sector to ensure its alignment with these commitments has proved more difficult, given the potential for fossil fuel production to support some key development goals. At the same time, support to the sector tends to have disproportionate political influence in developing countries and may therefore be a priority area where requests for international assistance are concerned. This means that financing and support for green growth and lower-carbon pathways needs to engage with the challenges that developing countries with fossil fuels face. Deploying climate finance effectively in these contexts will require understanding of politically viable alternative development models or support for transition that accounts for existing fossil fuel interests and exposure to carbon risks.

The first question for donors and MDBs is whether and how international support for fossil fuel sectors can be made consistent with the carbon budget necessary to meet the ‘well below 2°C’ target. The potential conflict between support to the fossil fuel sector and climate considerations was raised as early as 2004, in the World Bank’s extensive Extractives Industries Review.135 Yet until recently, MDBs and donor countries had rolled out inconsistent messages on fossil fuels, which reflected inconsistencies and internal differences at home regarding what they should support internationally. The result was generally a withdrawal from coal, growing support for gas as a ‘bridge’ to a lower-carbon future, and ambiguity where oil was concerned.

Only now are MDBs and donors beginning to make meaningful reforms to the ways in which they assist the fossil fuel driven economies (see Annex I for selected case studies). Most are in the process of revising their energy and mining policies in order to better align them with climate commitments. The World Bank Group’s decision in late 2017 to stop financing upstream oil and gas and apply ‘shadow pricing’ across its investments – including thermal power generation – marked a turning point in this respect, and has the potential to re-invigorate discussion around whether MDBs and donors should still be supporting fossil fuel development, and if so, under which circumstances this can be justified.136 The EBRD’s decision to support the TCFD process in early 2018 represents another important step towards the mainstreaming of carbon risk in development assistance.137

For these reforms to be effective, it is critical that they are aligned with country priorities, including NDC and long-term emissions reduction plans to 2050. One area worth exploring is whether MDBs could screen investments for compatibility with the potential recipient country’s plans and targets as outlined in their NDCs, while allowing scope for rising ambition to 2050. This should include assessments of implied emissions pathways and the potential for investments to support low-carbon goals, such as encouraging the role of gas or LPG in displacing higher carbon fuels and increasing energy access. However, this must be supplemented with a clear and full assessment of the systems costs through integrated energy planning of the sort outlined in Chapter 4, as well as the market requirements to enable this, and the level and coordination of development assistance that would be required. There are already some efforts in this direction; while they have little engagement in fossil fuels related activity, the French development agency (AFD) stated in 2017 that all its activities will be ‘Paris-compliant’, with an emphasis on avoiding the lock-in of unsustainable industrial dependencies that will place countries at a disadvantage in a ‘well below 2°C world’.138

At the same time, it is important that policy discussions and practical approaches to carbon risk and the need for transition are grounded in developing-country perspectives of fairness. Development assistance to fossil fuels has typically avoided engagement with the decision to explore or develop resources. All countries consider the decision to explore for and extract resources as ‘sovereign’; indeed, this sovereign right to leverage natural resources is enshrined within the founding documents of the UNFCCC.139 Low-income countries also rightly view their historical contribution to emissions as negligible, and addressing the issue of ‘equity’ has been critical to recent progress in climate negotiations.

Many decision-makers and civil society actors in developing countries view oil and gas resources as assets, and development of them as an opportunity to drive economic development. For these actors, there is the perception of an ‘opportunity cost’ associated with the stranding of fossil fuel resources. This sits uncomfortably with a 2°C global carbon budget, which implies that not all oil and gas reserves can be developed. As development agencies and MDBs reform their policy positions on fossil fuels, it will be hard to avoid the question of whether there is scope for ‘fairness’ in the way fossil fuel resources are ‘stranded’. Better understanding of the economic implications of a ‘fairer’ approach may help MDBs and donors in their conversations with country decision-makers (Box 9).

New research on the distribution of unburnable carbon could also usefully inform a number of policy areas that fall within the sphere of influence of individual donors or ‘coalitions of the willing’. For example, the reallocation of production implies give and take at the international level, with high-income producers constraining production in order to provide ‘space’ for lower-income producers. If Norway or the UK support overseas oil production in developing countries, should they concurrently reduce their own oil and gas production? Acknowledging the issue of ‘fairness’ through other policy levers – such as the removal of upstream subsidies, for instance – could help support a ‘level playing field’ for remaining fossil fuel production, as well as supporting the managed decline of less economic fossil fuel supply.

Previous attempts to estimate the remaining ‘burnable carbon’ budget by region, as originally modelled by Ekins and McGlade, have done so on the basis of least-cost production and transport, and have not considered equity.140 At the same time, there is a growing body of literature that examines the relevance of equity for policy decisions relating to future fossil fuel supply.141 Setting aside the political feasibility and the risks of any such approach, there is value in understanding whether there is any economic argument for redistribution. Who would be the winners and losers under any reallocation of production rights? Would any form of strategic ‘allocation’ make economic sense given the costs of production?

This box presents a reworking of the geographical distribution of unburnable carbon under a ‘development first’ scenario, which accounts for equity by allocating greater fossil fuel production rights to less developed countries. The global-level modelling uses the TIAM-UCL model and applies a UNDP Human Development Index (HDI) ranking to each of its regions to determine ‘priority’ levels (see Table 3) for allocating production levels. This draws upon the first of the three criteria proposed by Caney142 for informing the integration of equity considerations into the hypothetical allocation of ‘extractive rights’:

|

HDI group |

HDI level (0–1) |

TIAM-UCL regions |

|---|---|---|

|

Low-medium |

<0.7 |

Africa, India, Other Developing Asia |

|

High |

0.7–0.8 |

Middle East, Mexico, South and Central America, China, Former Soviet Union |

|

Very high |

>0.8 |

Western Europe, Eastern Europe, UK, Canada, USA, Australia, Japan, South Korea |

Source: Compiled by UCL (2018), based on TIAM-UCL regions and UNDP HDI rankings.

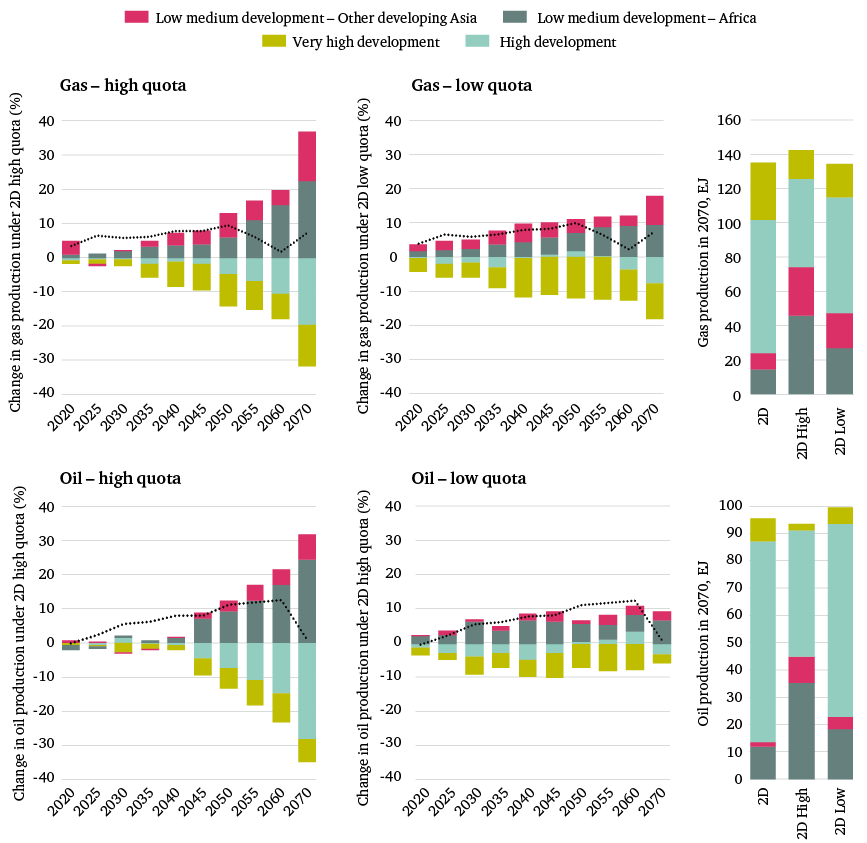

The model allocates production ‘quotas’ to each HDI group, determined by the application of an HDI-differentiated carbon tax on production (a full methodology is provided in Annex II). The resulting redistribution of oil and natural gas production can be seen in Figure 14, which show how under these assumptions, least developed regions could increase their production compared to that under the reference 2°C scenario, while production from the most developed regions would be constrained. For both oil and gas, a low quota results in a redistribution of up to 10 per cent per annum (in the case of oil, this increase comes primarily at the expense of production from the ‘very high’ HDI group). Under a high quota, there are almost no immediate benefits, and a strong redistribution only occurs after 2040. In the case of oil, the limited change prior to 2040 is due to relative cost competitiveness of ‘high’ HDI group, which includes low-cost Middle East producers.

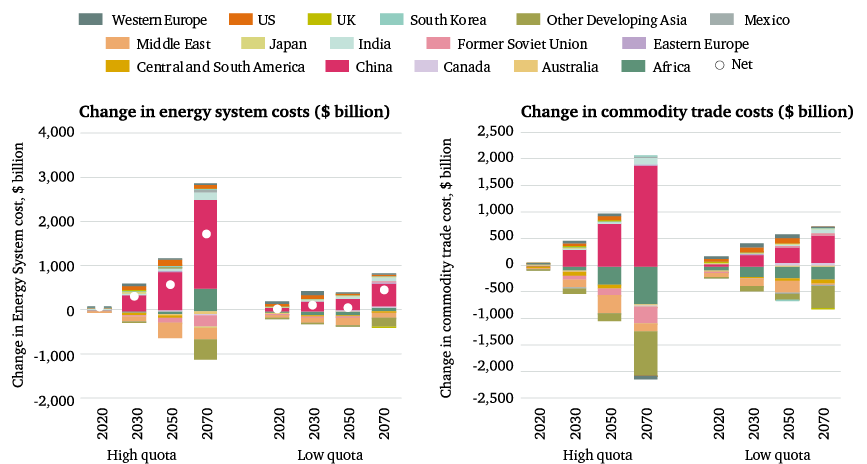

The wider implications of integrating equity considerations in the allocation of fossil fuel production are shown in figures 15 and 16. Figure 15 shows how the reallocation of production results in higher net system costs overall, particularly under the high redistribution, where annual systems costs increase by 2.1 per cent by 2050 and 4.4 per cent by 2070. There is, then, a clear trade-off between optimality and equity. Figure 16 shows how the increase in costs due to reallocation would negatively impact those regions without large fossil fuel resources, who may be highly import dependent; the changes in both system and commodity trade cost are borne largely by China, shown in pink. This reflects the fact that a ‘development first’ perspective is inherently a producer perspective; equity for net producers may not result in equity for net consumers.

While these governments might welcome the consideration of equity in policy discussions regarding future fossil fuel supply, the initial findings of ‘development first’ modelling suggests that the reallocation of remaining fossil fuel production does not necessarily yield economic benefit for developing countries. This is before the wider decarbonization trends addressed in this paper are considered. The reallocation of production may not yield any net benefit where the costs of production exceed the market price. This is the case for many producers in sub-Saharan Africa, for instance, where reallocation to the region would imply the development of high-cost resources.

Source: UCL and Chatham House modelling and analysis. See Annex II for full methodology.

As stated in Chapter 2, the clear signal sent by the G20 regarding the risks that climate change might present to the global financial system has been critical in furthering international cooperation around scenario analysis and carbon risk disclosure (through the TCFD). With rising levels of external debt in (often resource-driven) developing economies, the IMF is now warning about the risk of an impending debt crisis.143 In this respect, the failure to manage carbon in developing economies may also contribute to wider fiscal stability risks. This is not just an issue for the IMF and World Bank, but also for the commercial banking sectors of many advanced economies, which have increasingly lent to higher-risk emerging economies in search of better returns, given the low interest rates elsewhere (and on the assumption that the IMF would intervene in the event of non-payment).

MDBs and major donors are well placed to raise the issue of carbon risk in fossil fuel-driven developing economies on the international agenda. Given its role in furthering international cooperation on the development of standardized carbon risk metrics and frameworks (through the TCFD), the G20 presents a leading forum in which to do this. The G20 has frequently made commitments to assist developing countries in sub-Saharan Africa and Southeast Asia, for instance, through its Energy Principles and its New Industrial Revolution action plan. Meanwhile, it pushed green finance up the international agenda when China was chair of the G20 in 2016. Raising the issue of how developing countries can manage carbon risk on the G20 agenda could help build consensus among member states, other donor countries such as Norway, and developing countries on the need to develop new approaches to managing carbon risks and transition in assistance to the developing countries with fossil fuels.

To be effective, this will require engagement with a growing range of non-traditional donors. These include emerging economy countries and their export-import banks, OPEC, Arab and Islamic development banks, new multilateral banks such as the BRICS, NDB and the AIIB, as well as philanthropic trusts. As MDBs reconsider and re-allocate development finance and assistance in line with international climate commitments, there is a risk that assistance from different actors supports conflict development models. This makes deepening cooperation with non-traditional donors – and particularly the Asian MDBs, policy banks and ECAs, which provide the vast majority of finance for coal-fired power – even more important.

The rapid acceleration of climate finance is critical to the deployment of energy efficiency and the development of low-carbon energy systems, as well as the protection of critical forests and ecosystems services. The Paris Agreement set out a roadmap for richer countries to mobilize $100 billion a year in climate finance for developing countries from 2020.144 Policy and technical advice around climate finance can help prepare the business environment and ‘crowd-in’ green finance and sustainable investment, as well as support the development of local SMEs. These are critical parts of the picture, but in their current form, they do not fully engage with the challenges faced by countries with existing or growing national dependence on the fossil fuel sector, or the political-economy barriers that fossil fuel development may present to NDC implementation and green growth ambitions.

The rapid acceleration of climate finance is critical to the deployment of energy efficiency and the development of low-carbon energy systems, as well as the protection of critical forests and ecosystems services.

This demands better understanding of how finance can be channelled to programmes that support the sustainable diversification of exports, a reduction in domestic dependence on imports, and the development of an autonomous monetary system and domestic financing capabilities.

Working with ministries of finance to encourage longer-term perspectives on fiscal and current account risk related to export prices, as well as valuation, pricing and taxation strategies, which take into account both global and national transitions, is one entry point for MDBs and donors. The EBRD is currently trialling this approach in two of its fossil fuel producing countries, Kazakhstan and Egypt, with the objective of building a carbon risk strategy to augment its focus on enabling countries’ sustainable transition to market economies (see Annex I).

It is far from proven that climate finance, green finance and other mechanisms will be able to offer a comparable alternative to large-scale oil and gas development, in terms of short-term investments and access to regular inflows of foreign exchange (via exports). Not only have least developed countries found it difficult to access climate finance in the past, but it does not alone provide an alternative value proposition for most producers. Renewable energy, for example, will not generate the kind of economic ‘rents’145 that countries including Nigeria, Angola, Sudan and South Sudan have grown accustomed to.

For those countries facing the challenge of reducing dependence, questions will include how to replace lost foreign exchange flows, readdress the balance of trade and develop an increasingly autonomous monetary system with an expanding tax base and growing domestic financing capacity, thereby reducing reliance on external debt. Where fossil fuel driven economies are concerned, MDBs and donors should consider whether and how climate finance, concessional finance and other investments can help create the conditions for transition; for example, how can climate finance and green growth opportunities including energy efficiency, RE and circular economy approaches be harnessed to help broaden the tax base.

MDBs can play a role in providing credit enhancements to crowd-in private finance into infrastructure that enables a low-carbon pathway in the domestic economy. Banks and other commercial investors are interested in the ways that these low-carbon investments (often too small and difficult for them to assess and evaluate individually) can be packaged to reduce their risk. Such packages could be linked to national and international decarbonization objectives, and could have the objective of ‘levelling the playing field’ and providing viable alternatives to fossil fuel development, where the primary intended use of fossil fuels is domestic. As stated above, country NDCs and long-term 2050 plans under the UNFCCC provide valuable guidance in this context.

Practically, there are several ways that MDBs and donors can better coordinate support for fossil fuel-related sectors and good governance with support for climate-smart, green growth. As stated in Chapter 1, for many donors, policy and technical advice is their sole form of support to the sector. Chapters 3 and 4 demonstrate the need and the demand for better information and capacity to manage an evolving range of carbon-related risks at country-level. This entails first allowing understanding of the economy wide implications of carbon risk to inform country assistance, and second incorporating new approaches into existing assistance programmes for both established and prospective producers.

For countries depending on fossil fuels exports or expecting large production expansions, assessing carbon risk means not only thinking about the carbon intensity of the fossil fuel sector (e.g. increasing its efficiency, reducing flaring) but thinking about the economy-wide impacts of upstream decisions. Oil and gas sector approaches to carbon risk tend to focus on the fossil fuel sector itself and on fossil fuel supply – for example, Tanzania’s stated efforts to mitigate carbon risk focus on deployment of natural gas in place of firewood and charcoal, and converting vehicles to run on CNG.146

This is a narrow approach compared to that taken by more established producers such as Mexico, UAE and Malaysia. For these countries, resilience means putting in place market mechanisms to avoid exposure to carbon risk and to guide the economy, such as developing shadow carbon prices within the NOC and wider economy, re-evaluating the price for vital resources in the domestic economy, including fossil fuels, water, air, and land, as well as planning for an economy-wide transition away from the sector.

Where prospective and early-stage producers are concerned, MDBs and donors can play an important role in the development of replicable analytical approaches, including scenario analysis that considers the full range of revenue and fossil fuel supply scenarios, as well as emissions and other externalities, which can, in turn, help inform resilient long-term decision-making where the role of oil and gas is concerned.

There is a clear role for donors and MDBs in building the evidence base and processes required in making a decision over whether or not to proceed with exploration or the development of oil and gas discoveries, particularly where marginal, higher-cost reserves are concerned. This requires the accurate valuation of land, air quality and environmental services, as well as an assessment of the economic and societal trade-offs associated with different development pathways, particularly where decisions are based on the value of land, water and its potential alternative uses.

Support for the development of approaches such as natural capital accounting (NCA) and payments for ecosystem services tend to be situated in ministries of environment or agriculture but to take real affect they will need to be mainstreamed in central banks, treasuries, ministries of finance, energy and of national planning. Capacity-building could build on ongoing work on mapping and accounting for natural capital, including in Ethiopia, Madagascar, Uganda, Mozambique and Kenya and benefit from South–South learning.147

Working through these issues effectively will require listening to voices from other government entities and civil society areas of expertise. The political economy that forms around the fossil fuels sector tends to reinforce its prominence over others in national development expectations, even before production begins. There will always be other national institutions and groupings whose perspective and engagement can represent a broader set of views. Ministries or committees on national planning, agriculture, forests, fishing and national parks and tourism as well as regional and local communities all have interest in areas of the economy and industries whose prospects will be affected by the development of fossil fuel resources and associated power and industrial infrastructure.

As chapters 3 and 4 highlight, the risk presented by the ‘worst case’ for fossil fuel investment and demand will play out differently between the oil and gas sectors, and from country to country. Countries could improve resilience by conducting ‘carbon stress tests’ around fossil fuel revenues over the next 30–50 years, including under the most disruptive climate scenarios, and considering the resilience of energy, industrial and national development plans under each of these scenarios.

Working with ministries of finance to encourage longer-term perspectives on fiscal risks presented by uncertainty around export revenues and the time frame for diversification (including the sustainability of imports and external debt), is one entry point for MDBs and donors.

Support for carbon pricing and taxation strategies, which take into account both global and national transitions, is another. With MDBs, donors, investors and companies – including IOCs – increasingly applying a carbon price to investment assessments and screening, country governments must be better equipped to see their economies and development prospects through this lens. Development partners can help to build carbon accounting capacities within the relevant agencies such as central banks, treasuries and ministries of finance, ministries of energy, NOCs, and national planners. Effective support for green growth may also provide leverage to broaden the national tax base, given its bottom-up characteristics compared to the very narrow tax base that fossil fuel-led development tends to lock in.

There is already consensus among extractives advisers and the majority of developing countries on the importance of revenue transparency as a means of improving accountability for management of the fossil fuel sector. Where revenues are already flowing, greater accountability for how they are spent and whether these contribute effectively to economic diversification is an issue of great interest to society and particularly younger generations in fossil fuel exporting countries, and can be used to foster consultative processes.

In light of the global investment trends defined in Chapter 2 and the carbon trends outlined in Chapter 3, the development of new fossil fuel resources and related power infrastructure requires very careful risk assessment. The cost of large-scale solar continues to fall – with record low RE tariffs continuing to be set at auction in India, Mexico, UAE and other emerging markets on a regular basis. At the same time, established, low-cost producers such as Saudi Arabia are likely to drop their attachment to depletion policy based on the logic that ‘production ratio is no longer such a sign of strength. Better to have money in the bank than oil in the ground.’148 As a result, low-income fossil fuel producers are likely to face increasing pressure to offer better terms to upstream investors and to accept the conditions from importing countries wishing to offer long-term credit i.e. for future power and related industrial infrastructure.

Development advisers generally agree on the need for better coordinated and more holistic approaches to planning for energy and infrastructure (including upstream, power sector and transport sector). Those that already provide assistance to upstream fossil fuels and wider energy sector are well placed to support governments in more integrated assessments and planning capacities, which take a multi-sector approach to risk and incorporate a wider range of trade-offs, costs, externalities and options. USAID’s Integrated Resource and Resilience Planning (IRRP) is one approach to strategic energy planning that has been trialled in Ghana and Tanzania, which takes into account costs, centralized and distributed energy, demand side and efficiency measures and more recently, climate change impacts.149 DFID has also committed to a ‘whole system’ approach to its work on energy and climate. The aim is to begin with assessing demand for energy services by poor households and firms, and look back across the stages (and delivery modalities) of energy systems needed to deliver these e.g. distribution, transmission, and generation, and upstream decisions on extraction (see Annex I).150

Integrated planning can also raise traditional energy security questions, the response to which is likely to involve decisions in favour of greater diversification and increasing the share of RE in the energy mix. A country that relies on one gas field and one pipeline, for example, has clear energy security vulnerabilities.

The systems approaches mentioned above are relatively new, and would benefit from a stronger evidence base showing how fossil fuel development may impact on other development priorities. IRRP, for example, does not yet incorporate the costs of the externalities of energy choices including emissions, land-use change and water demand. Gas pricing, as noted above, remains an important factor where gas is expected to displace higher-carbon activities.

Moving away from a supply-led approach and towards an ‘energy services’ perspective can help more accurately project demand growth. In the development of models and scenarios, there is a risk of leaving assumptions unstated, such as the level of ambition, the role of CCS or the acceleration of low-carbon technologies. There is also a risk of reinforcing mainstream narratives that suggest ever growing demand for energy, and that underestimate the contribution of efficiency, improved planning, RE and new technologies and business models. Such demand scenarios are frequently cited as justification for large-scale supply-side loans and assistance.

In this context, the importance of demand-led planning should be re-stated. There is an old discussion that ‘development’ looks like what happened in the global North yet energy systems in these countries developed in response to demand. An energy system shaped by a top-down perception of what development ‘should’ look like may result in large-scale losses. Integrating new technologies including RE and decentralized technologies in established, centralized systems is a great challenge for advanced economies. Avoiding the problems of an entrenched system demands special attention in countries with low-energy access, which plan rapid development of grid systems.

Donors can play a key role here in enhancing country capacity and improving decision-making. USAID’s ‘Greening the Grid toolkit’, for instance, helps countries use policy, market and regulatory measures to integrate traditional and new, centralized and decentralized energy through grid-integration road maps.151 Developing effective markets to support new, flexible business models and enable competition between product ‘solutions’ rather than fuel supply e.g. light, cooling or pumping is another area worth special attention, particularly in rural areas.

Development assistance to the upstream should ultimately help countries plan for transition. Key agencies – fossil fuel ministries, petroleum sector regulators, NOCs – are frequently represented in good governance and technical capacity dialogues, and MDB and donor experts in extractives often seconded or involved in training. These experts are of course shaped by their experience; many are veterans of the oil and gas sector. Agencies funding or leading good governance programmes, strategic and technical advisory programmes for the upstream sector could make an immediate difference by ensuring the inclusion of expertise and skills to effectively align the sector’s development with NDC implementation and green growth. Much could be also be gained from peer-to-peer exchanges between established NOCs and emerging ones sharing practical lessons learnt, for example around emissions management, carbon pricing and markets, and the integration of energy efficiency measures and RE within the industry, as well as the reform of long-term commercial strategies and national mandates.