1. Introduction

The electricity sector is undergoing a set of profound disruptive shocks, due to a confluence of technological innovation, tougher environmental policies and regulatory reform. This is most apparent in Australia, the EU and parts of North America, where once-powerful utility companies are struggling (many are restructuring in order to survive). Decision-makers elsewhere are asking whether these power markets are outliers, or whether they herald a global trend.

Within the regions most affected, the economics of the power market have undergone a structural shift. Renewable generators tend to have lower operating costs and priority access to the grid. As such, when renewable electricity is being produced, it is typically used in preference to electricity from fossil fuel generation – thus reducing the revenues of traditional utilities reliant on oil-, gas- or coal-fired generation. At the same time, improvements in the energy efficiency of household appliances have dampened the prospects for growth in electricity demand that might partially offset the impact of renewables.

These transformations have occurred, in many OECD countries, within the context of power sector liberalization that has allowed consumers to choose between a growing number of suppliers – thus threatening incumbents. While factors such as the extent of renewables deployment, the slowing of demand growth and the opening of markets to new players vary across regions, the transformation of the sector looks set to continue and extend into other markets. In countries such as China and South Korea, the operation, management and market structure of power systems remain similar to historical practice elsewhere: companies with large dispatchable1 power plants sell electricity to consumers who continue to have the same, passive relationships with their suppliers. Yet few countries can ignore the wider sectoral transformations under way. Regardless of the market structure, renewables are being deployed at scale.

Meanwhile, technological innovation continues to redraw the prospects for the sector. Fast-rising sales of electric vehicles (EVs) could have a huge impact on future electricity demand. Households are increasingly installing batteries to store excess power generated by rooftop solar photovoltaic (PV) units. Multinational technology companies are vying with traditional utilities to capture the new opportunities from the growth of the ‘Internet of Things’ (IoT) or to optimize the grid. New payment systems such as blockchain protocols are enabling transactions that could bypass traditional intermediaries. Finally, investments in super-cooled power lines are increasing electricity flows across borders.

These transformations are often considered in isolation from each other, framed as changes either to the electricity sector or to the wider energy system (i.e., including transport, heating and cooling). Yet it is unclear how developments such as changes in network infrastructure, digitalization, optimization, smart appliances, EVs and battery storage will affect the electricity system as a whole. This paper explores several questions. To what extent is an emerging second phase of disruptive technologies, and the associated rise of new market players, poised to have further transformational impacts on the electricity sector? Might these technologies enable greater deployment of renewables while keeping the costs of integration into the system reasonable? Finally, what might be the impact and response of the traditional utilities to these shifts?

The paper is organized into four chapters, including this introduction. In the rest of Chapter 1, the paper explores the three elements of what can be called the ‘first phase’ of electricity sector transformations: renewables, energy efficiency and market reform. It goes on to survey the impacts of these transformations on traditional utilities, and utility firms’ responses to these impacts. Chapter 2 investigates the ‘second phase’ of electricity sector transformations, which are being driven by technological innovation and the need for system flexibility. Emerging developments are examined within the context of falling barriers to further deployment of renewable energy, the outlook for future electricity demand, the emergence of new market actors, and the implications of the sector’s structural changes for utilities. The chapter includes analysis of the main transformations that utilities will need to undergo. The analysis is segmented by the technologies driving increased flexibility, including: EVs, digital infrastructure, interconnectors, storage, and digital control of demand and the wider electricity system. Chapter 3 explores the emerging power landscape, the competition between the new market actors and incumbent utilities, as well as a potential new role for utilities that operate the grid – all within the context of the shift towards energy service platforms and new transactions methods. The chapter also looks at the regulatory shifts that will need to accompany the second phase of flexibility transformations. The conclusions in Chapter 4 draw together the main themes of the second phase of transformations.

Transformations driven by climate and air quality

Climate and air quality policies are responsible for some of the most profound changes to have occurred during the first phase of electricity sector transformations. By burning fossil fuels and releasing carbon dioxide (CO₂), energy production and use are responsible for around 60 per cent of global greenhouse gas (GHG) emissions.2 Consequently, according to the Intergovernmental Panel on Climate Change (IPCC) and others, without a move away from a ‘business as usual’ approach in the energy sector, the rise in global temperature could exceed 4°C above pre-industrial levels by the end of the century.3 The largest proportion of energy-related emissions originate from the heat and power sectors, which are responsible for approximately a quarter of all GHGs.

The Paris Agreement of December 2015 increased and cemented global ambition on climate mitigation, calling for ‘aggregate emission pathways consistent with holding the increase in the global average temperature to well below 2°C above pre-industrial levels and pursuing efforts to limit the temperature increase to 1.5°C above pre-industrial levels’.4 At the same time, the agreement recognized that the cumulative effect of individual countries’ climate mitigation plans, known as their Nationally Determined Contributions (NDCs), was insufficient to meet agreed targets and that additional action was therefore needed.

Policy activity on climate change has undoubtedly broadened and deepened in recent decades. The number of climate change-related laws and policies adopted globally has doubled every four to five years since 1997, and now exceeds 1,250. However, the rate of growth in legislation and policy formation has slowed in recent years, suggesting a shift towards implementation and consolidation.5

Not only are concerns about CO₂ emissions driving change in the power sector. More immediate worries about air quality are also prompting the early closure of power stations and/or the cancellation of plans for the construction of new plants; although these changes chiefly affect coal-fired facilities, oil-fired plants are also under pressure. In the EU, 60 per cent of power stations, accounting for around 120 GW of capacity, do not comply with the EU’s 2010 Industrial Emissions Directive. As a consequence, they will need to be retrofitted or closed. In China, older and less efficient power stations accounting for 10.8 GW of capacity were closed in 2016, and further action is being targeted to reduce pollution in major cities.6 Beijing closed its last coal-fired power stations in 2017,7 and cancelled plans to build an additional 100 coal-fired plants.8 In South Korea, 10 of the country’s oldest coal stations are due to close on account of pollution reduction efforts.9

Electricity is a vital societal resource, providing energy services for light, heat, cooking, transport, telecommunication, commerce and industry. Global annual electricity consumption stands at around 21,000 terawatt hours (TWh), yet 1.1 billion people still do not have access to electricity. Recognizing this, some traditional utilities in mature electricity markets are seeking to move into emerging markets. However, new technologies may be moving faster than the utilities.

The first phase of transformations

The rise of renewables

This section illustrates how the renewables sector has become central to the first phase of electricity system transformations. Three main technologies provide, or aim to provide, significantly lower-carbon and lower-pollution electricity: nuclear power, carbon capture and storage (CCS), and renewables. Of the latter, solar PV and onshore wind power are now significant contributors to new generating capacity. This is due partly to the failure to commercialize CCS, and also to the rising costs of building new nuclear plants compared to falling costs for renewable generators.

Nuclear power plants are operating in 31 countries. However, high costs and safety concerns, following major accidents at Chernobyl in Ukraine in 1986 and Fukushima in Japan in 2011, have dramatically affected the level of deployment. As a result, the contribution of nuclear power to global electricity supply is decreasing, from a peak of 17.6 per cent in 2006 to 10.3 per cent in 2017. New nuclear capacity is being added in 17 countries, with a total of 57 reactors in the pipeline. Eighty per cent of all new-build units (42) are in Asia and Eastern Europe, with 20 of these projects being in China.10 Most reactors still operating in Western Europe and North America were built in the 1970s and 1980s. Despite the widespread practice of extending the operational lives of these plants, the amount of electricity produced by nuclear power is likely to continue to diminish in the coming decades. While the Chernobyl and Fukushima accidents undoubtedly raised public and political concerns over nuclear safety, the main obstacles to deployment in most markets are difficulty of financing and lack of economic competitiveness.

Of the 162 national pledges, 144 mention renewable energy; and of these, 111 refer to a target for, or planned expansion in, the use of renewables.

The electricity sector was expected to be a pioneer for the use of CCS. In March 2007, the European Council called for 12 CCS projects to be operational by 2015,11 while in 2008 the G8 called for the creation of 20 large-scale CCS demonstration projects globally by 2010, with a view to beginning broad deployment of CCS by 2020.12 The EU set aside considerable funding through the European Energy Recovery Programme (€1 billion) and the New Entrants Reserve 300 Scheme (NER) (more than €2 billion for CCS and renewables). However, to date no commercial-scale CCS systems are running at power plants, and leading proponents of the technology such as the UK have cancelled their programmes.13 At a time of low electricity prices and low carbon prices, rapid and widespread deployment of CCS seems unlikely.

Given the lack of deployment of CCS and limited construction of new nuclear capacity, renewable energy is thus dominating the decarbonization of the power sector.14 Between 1997, with the agreement of the Kyoto Protocol, and 2016, global electricity generation from nuclear power grew by 225 TWh.15 Over the same period, the increase in generation from non-hydro renewables (primarily biomass, wind and solar PV) was seven times that of nuclear power. Hydropower generation recorded similar growth.16 The trend is likely to continue, as renewables dominate NDCs. Of the 162 national pledges, 144 mention renewable energy; and of these, 111 refer to a target for, or planned expansion in, the use of renewables.17

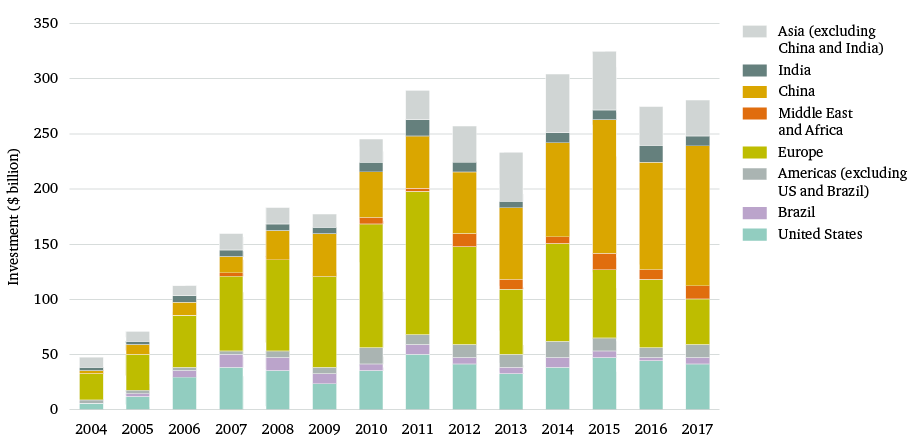

According to data published by Bloomberg New Energy Finance (BNEF) and the United Nations Environment Programme (UNEP), global investment in renewable energy – excluding large hydropower facilities – was just under $279 billion in 2017, a rise of 2 per cent on the previous year. Wind and solar PV dominate the growth in non-hydro renewables, accounting for around $107 billion and $161 billion in investment respectively.

Due to lower technology and installation costs, the global capacity of small-scale non-hydro renewables18 increased by 157 GW in 2017, compared with 2016.19 This accounted for 61 per cent of net new installed capacity (including all fossil fuel, nuclear and hydro) in 2017. Solar PV added 98 GW and wind 52 GW. Globally, China is the single largest contributor of new renewables, with $126.6 billion in investment (45 per cent of the global total) in 2017, including $86 billion in solar PV and the deployment of 53 GW of new solar PV capacity. In contrast, investment in renewables in the US fell by 6 per cent to $40.5 billion, and in Europe by 36 per cent to $40.9 billion.20

Investment rates for renewables have varied around the world in recent years, reflecting regional differences in policy formation and in the availability of new technologies. A decade ago Europe dominated, with large-scale deployment of wind power and solar PV led by Germany, Italy and Spain. Over the past five years, however, the main growth in investment has been in Asia, led by China (see Figure 1).

Figure 1: Global investment in renewables by region ($ billion)

Figure 1: Global investment in renewables by region ($ billion)

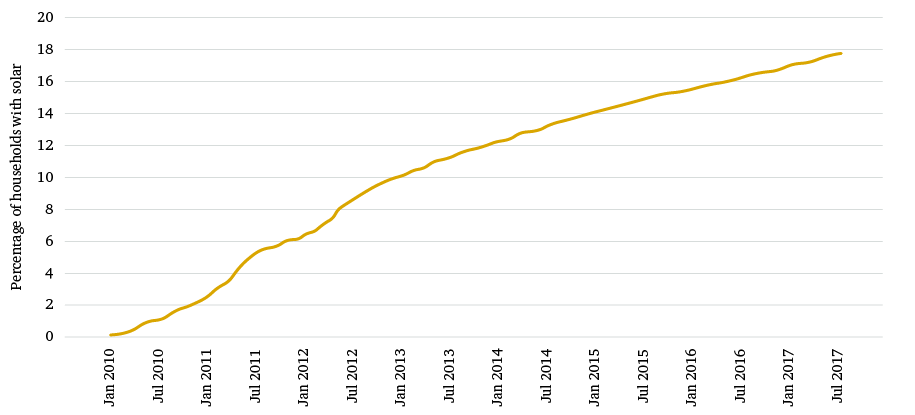

A distinct advantage for renewables is that deployment is cost-effective on a relatively small scale. The factory-based manufacturing model for renewables is more flexible than the highly capital-intensive, complex, infrastructure-based models associated with nuclear power and CCS. For solar PV, between 2010 and 2016, more than 23 million units of less than 100 W in capacity (also known as pico-solar PV) were sold worldwide for off-grid purposes.21 In the UK, more than 1 million homes now have solar PV panels, as do more than 1.4 million in Germany. Most recently, Australia has seen a huge uptake in the use of distributed solar PV installations. Since 2010 the share of Australian homes with a solar PV installation has risen from a negligible base to 17.7 per cent as of August 2017 (see Figure 2). Australia’s domestic solar PV penetration is the highest worldwide, and three times that of Germany and the UK.22 BNEF, in its New Energy Outlook,23 expects that Australia will continue to dominate small-scale – that is, decentralized – solar PV deployment.

Figure 2: Proportion of households in Australia with solar PV

Source: Chatham House analysis of data from Australian Photovoltaic Institute (2017), ‘Australian PV market since April 2001’, http://pv-map.apvi.org.au/analyses (accessed 9 Nov. 2017).

Figure 2: Proportion of households in Australia with solar PV

Source: Chatham House analysis of data from Australian Photovoltaic Institute (2017), ‘Australian PV market since April 2001’, http://pv-map.apvi.org.au/analyses (accessed 9 Nov. 2017).

Renewables’ domination of new capacity in the power sector is expected to continue. The International Energy Agency (IEA) forecasts that ‘solar PV and onshore wind together [will] represent 75% of global renewable electricity capacity growth over the medium-term’, with global renewable electricity capacity expected to grow by 42 per cent (or 825 GW) by 2021.24 It should be noted that significantly more renewable capacity is required to replace a unit of installed capacity from a non-renewable source. In other words, replacing 1 GW of non-renewable generation capacity, for example, would require the installation of more than 1 GW of renewable capacity. This is because renewable installations are weather-dependent and thus generate less electricity per installed unit of capacity. Recent figures for the US demonstrate this disparity. In 2016, the country’s nuclear facilities had a capacity factor – the ratio of actual to maximum possible generation – of 90 per cent. Coal and gas had capacity factors of 55 per cent and 56 per cent respectively. In contrast, the capacity factor for wind power was around 34 per cent.25 BNEF estimates that nearly three-quarters of the expected $10.2 trillion in investment in new power-generating capacity through to 2040 will be renewable.26

While decarbonization policies initially stimulated the deployment of renewables, economics are now driving accelerated rates of deployment. As renewable technologies continue to be deployed, their manufacturing and installation costs are decreasing, and their competitiveness is improving. Solar PV is already at least as cheap as coal in Germany, Australia, the US, Spain and Italy. By 2021, it is expected to be cheaper than coal in China, India, Mexico, the UK and Brazil, according to BNEF.27

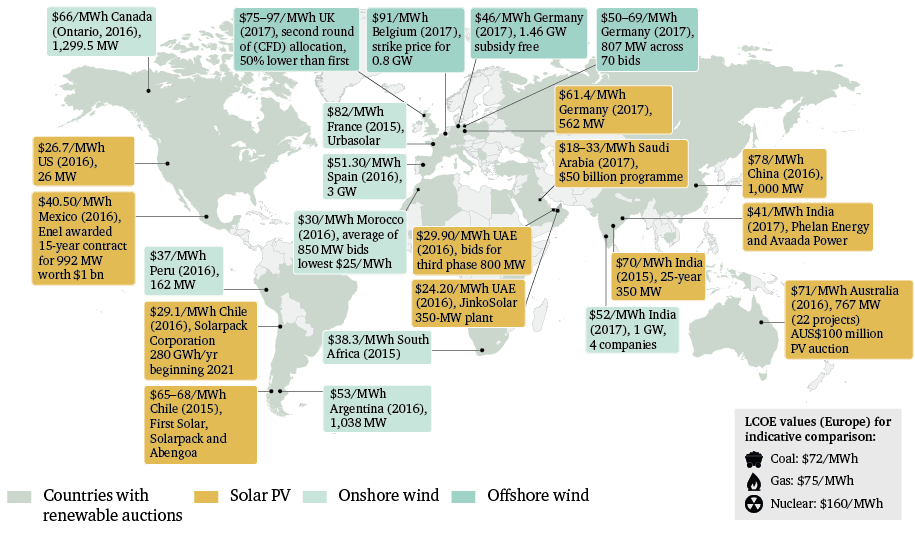

BNEF estimates that the cost of onshore wind power has fallen dramatically in the past 30 years, from more than $500 per megawatt hour (MWh) in 1985 to around $70/MWh in 2015, including a 50 per cent fall since 2009. BNEF anticipates a further 41 per cent drop by 2040, largely because of efficiency improvements. The price of installing solar PV has fallen by 99 per cent since 1976 and by 80 per cent since 2008; it is expected to drop by another 66 per cent by 2040.28 Yet BNEF’s price decline forecasts may even turn out to be conservative, as production, installation and authorization costs (particularly given more competitive auctions) further drive down the costs of renewable energy, as can be seen in Figure 3.

Figure 3: Renewable-power contracts agreed in 2015–17, with comparison of levelized cost of electricity (LCOE)29 values for coal, gas and nuclear generators

Figure 3: Renewable-power contracts agreed in 2015–17, with comparison of levelized cost of electricity (LCOE)29 values for coal, gas and nuclear generators

Globally, electricity generation increased by 29.2 per cent between 2006 and 2015, while renewables’ share of generation increased from 19.7 per cent to 24.2 per cent over the same period. The large-scale deployment of renewables, particularly solar PV and wind power, has already changed the electricity mix in Europe and other parts of the world. In the EU, renewables provided 12 per cent of electricity in 1990, 15 per cent in 2000, 21 per cent in 2010 and 29.6 per cent in 2016 according to Eurostat; unofficially, the share in 2017 was 30 per cent.30 That said, across the EU there have been considerable differences in uptake of renewables between countries. For example, in Austria 70.3 per cent of electricity is generated by renewables; in Sweden the figure is 65.8 per cent; in Portugal 52.6 per cent; in Latvia 52.2 per cent; and in Denmark 51.3 per cent.31 In 2016, Denmark managed a peak production level for renewable electricity of 140 per cent of demand, while Germany achieved 86.3 per cent.32 The contribution of solar PV and wind power to electricity generation in the EU increased from 2.5 per cent to 13.0 per cent between the end of 2006 and end of 2016. Traditional utilities have been slow to deploy and invest in renewables, and this has affected investor confidence. Between December 2007 and December 2017, European utilities lost around 45 per cent of their share price value, as measured by the 29 utilities comprising the Stoxx eurozone utilities index.33 The accelerated deployment of renewables has significantly contributed to this decline,34 and has been accompanied by write-downs of power station valuations.35

Box 1: The next wave of renewables

Combined with the falling costs of solar PV and wind power, new technologies for floating generation facilities could soon allow renewable power to be implemented in locations that are impractical for conventional installations. In addition to the implications for generation capacity, floating wind turbines and floating solar PV arrays offer potential land-use and political benefits: they reduce competition over land for food production and housing, and help to circumvent local opposition to new power projects. Although moving generation offshore currently carries additional costs compared to land-based facilities, these costs could be expected to fall over time, as has been seen in the UK, where guaranteed prices for offshore wind power in September 2017 were more than 50 per cent lower than those at similar auctions two years earlier.36

Growth in the use of floating solar PV facilities is likely to be led by their installation in the reservoirs of hydropower dams, which benefit from still water and established grid connections. In 2017, China turned on the world’s largest floating solar PV farm, with capacity to power 15,000 homes. The plant takes up no land space, and the cooling effect of the water improves efficiency by 3–5 per cent.37 The potential market for power generated in this way is expected to grow to 2.5 GW by 2024.38

The world’s first commercialized floating wind plant has been built in Scotland, supplying 30 MW of electricity 25 km offshore.39 Floating wind turbines can operate in water up to 220 metres deep. Their fixed-bottom counterparts can only be installed where water depths are 50 metres or less. As a result, floating turbines potentially open up steep continental shelf coastlines, such as around Japan, the Mediterranean and the US west coast, to wind power. Further away from the coast, floating turbines can also capture higher wind speeds, potentially boosting generation.40

Although Europe’s wind resource is vast, much of it is inaccessible to fixed-bottom turbines. If floating wind becomes competitive and deployed at scale, existing EU targets – including the 2030 target of 150 GW – could be delivered earlier, aided by new capacity in deepwater sites.41

The European Commission has been supporting research and development (R&D) programmes into floating wind power, via funding initiatives such as Framework Programme (FP)7 and NER300. In the US, the Department of Energy has invested more than $55 million to develop WindFloat technology on the east and west coasts. Japan has also strongly pushed for floating wind technology since the Fukushima nuclear accident in 2011.42

Energy efficiency and low demand growth

The introduction of new energy efficiency standards, alongside the accelerated deployment of renewables, has contributed to stagnating growth in electricity demand. This trend, which has compounded the negative pressure on the share prices of traditional utilities, forms the second major component of the transformations under way within the electricity sector.

Energy efficiency is generally regarded as the most cost-effective, economically prudent means to cut CO₂ emissions and enhance energy security. As such, 90 per cent of the Paris Agreement’s NDCs rely on energy efficiency to deliver their commitments. Although end-users of energy may not see the attractiveness of efficiency measures while prices are low, governments certainly do.

However, the impact of energy efficiency on the future of electricity demand is complex. Efficiency in the wider energy system can stimulate electrification, for example through the more stringent vehicle petrol standards that are partly driving the shift to EVs. Yet it can also inhibit electrification – for instance, in the buildings sector thermal insulation lowers the heating load, reducing the economic incentive to use heat pumps. Further, efficiency within the electricity sector reduces the cost of powering appliances. This results in some consumers buying larger appliances or running appliances for longer than they otherwise would, a phenomenon known as the ‘rebound effect’.43

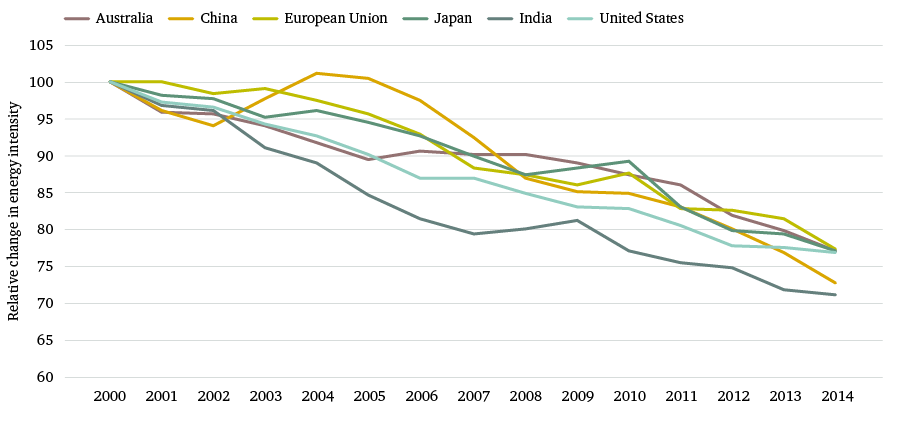

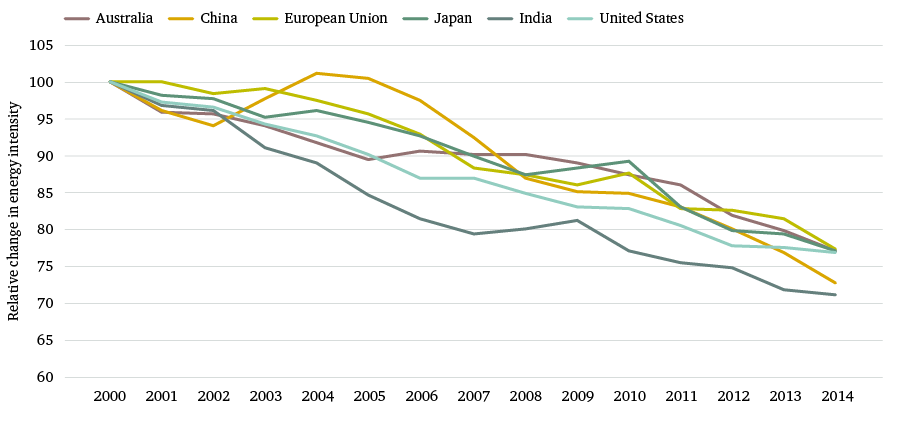

Forecasters and scenario-builders all too often assume that growth in energy consumption will be much higher than it turns out to be.44 The energy intensity of the global economy – defined as the amount of energy used per unit of gross national product – has actually declined from 6.49 megajoules per dollar at the turn of this century to 5.36 megajoules per dollar in 2014, according to the World Bank.45 As Figure 4 shows, energy intensity has improved (i.e. fallen) across major economies, but the extent of the change varies considerably. Clear improvements have occurred in the emerging economies, which have deployed energy efficiency measures, accelerated growth of service sectors and slowed infrastructure development.

Figure 4: Energy intensity since 2000 in selected economies

Figure 4: Energy intensity since 2000 in selected economies

Improvements in energy intensity and economic competitiveness have resulted in slower electricity demand growth. The average annual demand growth per decade is shown in Figure 5, highlighting that peak demand growth straddled the turn of the century at the global level. Even in China, power demand growth has slowed in the past decade. In OECD countries in Europe and North America, demand is now flat or falling.

Figure 5: Change in electricity consumption, 1985–2015

Figure 5: Change in electricity consumption, 1985–2015

Efforts to improve energy efficiency in the electricity sector have traditionally focused on lighting and appliances in buildings. In the wider energy system, such efforts have focused on thermal insulation in buildings and fuel efficiency standards in transport.46 Efficiency drives have been extremely successful in areas such as lighting, which accounts for around 15 per cent of global electricity demand. To date, nearly 200 million LEDs have been installed,47 saving around 100 TWh per annum. Mandatory Minimum Energy Performance Standards (MEPS) now cover around 30 per cent of global final energy use,48 and have played a key role in lowering energy demand. For instance, 90 per cent of electric motors sold globally are subject to MEPS49 (see Box 2).

Significant energy efficiency measures are yet to be implemented across buildings, transport and industry. Huge price reductions in LEDs have stimulated pledges from companies and governments to install in excess of 14 billion LEDs under the Clean Energy Ministerial’s Global Lighting Challenge.50 The use of MEPS is also likely to expand, and motor systems should become increasingly efficient. Two major areas for policy development in electricity efficiency are small appliances and electric motors. Small electrical appliances represent almost half of electricity consumption by appliances, but are generally not subject to MEPS, while motor systems represent more than half of global electricity consumption (see Box 2).

Box 2: Efficiency of motors

Within industry, electric motor systems in the form of pumps, fans, compressed air systems, material handling systems and processing systems account for around 70 per cent of electricity demand, equivalent to 30 per cent of global electricity consumption. Within buildings, around 33 per cent of electricity consumption is used to drive motors in everyday appliances such as hair dryers, vacuum cleaners, washing machines, tumble dryers, dishwashers, pumps, air conditioning units, fans, juicers and food blenders.

Electric motors have been subject to efficiency improvements and MEPS, but the nature of such motors means there is still room for large savings in the wider system in which they operate. As a motor is generally designed to work at one speed, much of its rotational motion is wasted prior to driving the end-use device. More widespread use of variable-speed drives and the introduction of wider system efficiency measures, combined with continued tightening of efficiency measures for motors themselves, could save around 40 per cent of electricity consumption within industry.51 Installing variable-speed drives alone can increase the efficiency of motors by 15–35 per cent.52 Due to rapid growth in the applications for which motor systems are used, the IEA anticipates that electricity demand from motors will grow by 80–100 per cent by 2040 relative to 2014, depending on the extent to which system-wide efficiency measures are applied. By 2040, efficiency measures could save around 1,600 TWh per annum.

Globally, investment in energy efficiency averaged around $220 billion per annum from 2010 to 2015. However, merely to fulfil NDC pledges and comply with recent policy measures, such investment will need to more than quadruple to an average of $920 billion per annum by 2040. In addition, climate projections suggest that it will need to rise to $1.4 trillion per annum to keep global warming below 2°C. If NDC pledges and recent policy developments successfully drive efficiency improvements across the energy system, final energy consumption could be 27 per cent lower than it would otherwise be in OECD countries, and 20 per cent lower in non-OECD countries. This would cause world energy intensity to fall by more than 60 per cent by 2040, approximately doubling the average rate of improvement over the past three decades.53

Market reform

For many decades large, centralized fossil fuel power stations and, in some countries, nuclear power stations dominated the electricity sector. These were usually owned and run by the same state-owned entities that operated the grids and supplied electricity to the final customers. Through a process of market liberalization, state-owned electricity companies in many countries were unbundled to separate the operation of the grid from power generation and retail operations, often leading to the privatization of assets. This process allowed new companies to enter the market all along the value chain, though primarily in the generation and retail segments.

As the power sector responds to environmental, economic and security-of-supply concerns, the pace of change will be determined in part by the current market structure and the vision of policymakers.

In the US retail market, Inspire Energy was formed in 2010, offering a tariff in northeastern states with 100 per cent of supply generated by wind. Demand for such tariffs has grown: there are now at least 13 green tariffs in operation across 10 states, including one offered by a public power company.54 In Japan, liberalization has enabled established energy companies such as Tokyo Gas to enter the electricity retail market; 300,000 customers switched from their previous supplier to Tokyo Gas’s competitive tariff in the first months of liberalization in 2016.55 In the UK, new local authority-run suppliers such as Bristol Energy and, in Nottingham, Robin Hood Energy are joining the traditional utilities. Even international oil companies such as Shell are beginning to signal a move into electricity markets.56 As the power sector responds to environmental, economic and security-of-supply concerns, the pace of change will be determined in part by the current market structure and the vision of policymakers.

There is no global standard for market structure or ownership of electricity sector assets, and consequently structure and ownership vary across and within countries.

In March 2015, the government of China published its strategy document, Deepening Reform of the Power Sector, which recognized the need to reorient power sector reform around environmental goals while meeting growing demand for power. The top five state-owned companies still control 50 per cent of generation assets, and two state-owned grid companies control 100 per cent of transmission, distribution and retail. The reform’s founding principles include the increased use of market mechanisms and the protection of residential and agricultural consumers. Key elements of the strategy also include reform of the grid companies responsible for both wholesale and retail sales of electricity. In addition, the wholesale market will be liberalized, allowing non-state-owned wholesale electricity companies to enter the market. Industrial-scale consumers will be able to bypass the grid companies and negotiate directly with suppliers.57

The EU introduced three sets of legislation to liberalize electricity and gas, in 1996, 2003 and 2009. These reforms progressively unbundled previously vertically integrated electricity and gas companies, enabling greater consumer choice and moving regulatory control away from governments towards independent national and EU bodies. In 2016, the EU introduced further liberalization legislation, including proposals on a new market structure and regional cooperation.58 The legislative proposals seek to adjust the rules of the market (such as on infrastructure, investment and effective renewables integration), and also feature internal energy security elements (covering capacity markets and security standards, among other things). Other areas being discussed are greater involvement of household consumers in the market; the introduction of smart grids; data protection; and opportunities to save energy.

In the US, the electricity industry is governed by a complex set of regulatory rules set at municipal, state and federal levels. Most rules are set at state level, although the Federal Energy Regulatory Commission (FERC) has exclusive jurisdiction over the interstate sale of electricity. Federal regulations are also set for the licensing of infrastructure such as nuclear and hydropower facilities. Market liberalization policies have been introduced at state level, leading to very different models from one state to another. Potentially significant developments include the New York Reforming the Energy Vision (REV), and more gradual reform in California and Hawaii – in both states, renewables are a significant source of power, much of it from rooftop PV. In many states, however, power sectors remain vertically integrated.

Japan has also been reforming its power sector. The first reform, introduced in 1995, enabled independent power producers to enter the market. Three additional reform packages were subsequently introduced, in 2000, 2004 and 2008. For many years, the 10 electricity companies effectively remained regional monopolies, and opposed large-scale market reform. However, their political power and support within government diminished in the wake of the Fukushima nuclear accident and subsequent economic turmoil, enabling the reformers to push through their agenda.59 Following Fukushima, reforms established the Organization for Cross-regional Coordination of Transmission Operators (OCCTO) and the Electricity Market Surveillance Commission in April 2015. Full liberalization of the retail market, from April 2016, included the legal unbundling of transmission and distribution activities from generation, and the planned abolition (by 2020) of retail rate regulation.

Reform of the power sector in South Korea started in 2001, but national-level reforms largely stalled from 2004 onwards. The Korea Electric Power Corporation (KEPCO) is currently responsible for all transmission, distribution and retail of electricity. It fully owns five generation companies – four thermal and one nuclear. However, about 10 per cent of generation is provided by privately owned independent power producers. All power is traded through the Korean Power Exchange, which is also responsible for grid balancing, management of the market, and enacting and revising market rules.

Despite the changes in these markets, most of the power systems have continued to be largely operated and managed in similar ways, by companies with large dispatchable power plants,60 selling to consumers who continue to have the same, passive relationships with their energy suppliers. Many of the large traditional generating companies have also remained, and still dominate the market.

In many jurisdictions, the first government-owned electricity providers were deemed to be ‘utilities’ on the basis that they maintained the infrastructure that provided a public service. Liberalization brought a fragmentation of the market and infrastructure, which were to be operated and owned by many private companies. Generators, distribution network operators, transmission network operators and retail suppliers were subsequently created as potentially distinct companies, but the role of each entity is now significantly removed from that of a pure ‘utility’. In the coming sections, the term ‘utility’ is often used to describe an established or traditional utility, unless a specific segment of the electricity system is being referred to.

Impact on traditional utilities

Slower than expected demand growth (or in some cases decreasing consumption), coupled with greater deployment of renewables, is affecting the volume and price of electricity sales by incumbent generators. This can be seen in the intra-day price of electricity in countries with high volumes of solar PV. Historically, the price of electricity was high during the day, when demand increases; however, in countries with large amounts of solar PV, the peak intra-day price has disappeared for large parts of the year. This trend has been described as the solar PV ‘duck curve’.61 As renewable generators enter the market, even if they do not have priority access to the grid, their low production costs mean that they can underbid fossil fuel generators, which drives down the wholesale price. This is known as the ‘merit order effect’, and is now widely documented and observed in Spain, Germany, Denmark, Australia and the US.62 For example, in Germany, a study of the day-ahead spot market found that prices fell by €1.23 per MWh for each additional gigawatt hour (GWh) of wind power.63

Major traditional power utilities see current low prices not as a cyclical trend but as a permanent structural change. ‘The price of electricity has no reason to rise. It will never be like it was before,’ said Isabelle Kocher, chief executive of the French-headquartered company ENGIE, the world’s largest non-state-owned producer of electricity.64

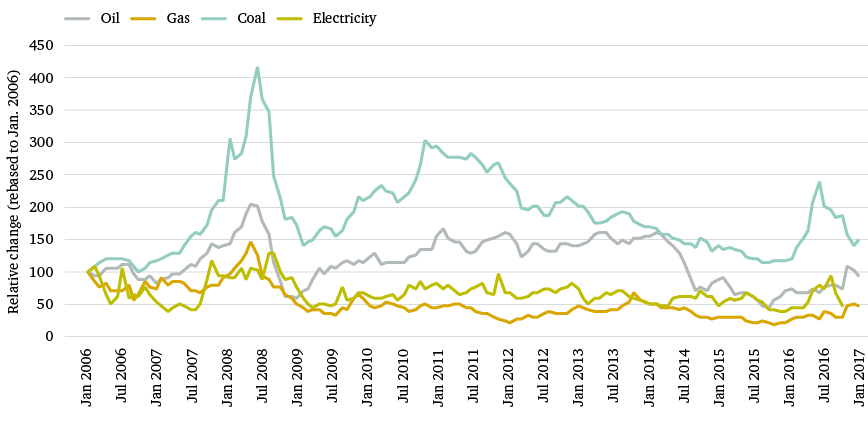

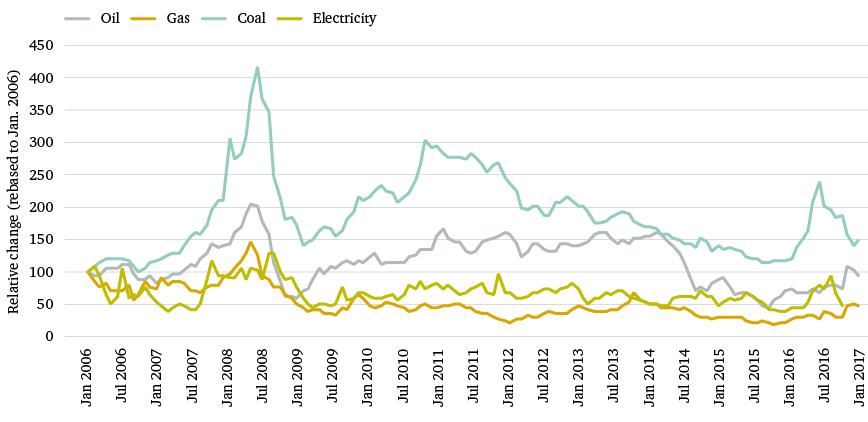

Box 3: Changing fossil fuel prices

Power prices have always fluctuated. They are directly affected by fuel costs, which in turn are affected by regional or global prices. In 2008, the cost of coal was approximately $200/tonne in Europe and about $175/tonne in Asia; in both regions it fell to less than $75/tonne in 2015, and as of mid-2017 was between $40/tonne and $85/tonne. Globally gas prices have also fallen. In the US, prices have slid from $5 per million British Thermal Units (MBTU) in 2013 to around $3/MBTU in 2017. In Asia and Europe, over the same period, prices have fallen from $20/MBTU and $11/MBTU respectively to around $8/MBTU. Although traditional power utilities are experienced in adjusting their prices to compensate for cyclical fluctuations in fuel costs, volatile markets can affect the profits and outlook of companies in various ways, depending on their different fuel mixes.

Figure 6: European fossil fuel and electricity prices (rebased to January 2006)

Figure 6: European fossil fuel and electricity prices (rebased to January 2006)

Source: Chatham House analysis of Thomson Reuters data (2018).

Unsurprisingly, given falling power prices and flat or falling electricity production, earnings before interest, taxes, depreciation and amortization (EBITDA) have fallen over recent years for most traditional power companies. German utilities, along with ENGIE in France, have suffered significant declines in EBITDA. Electricité de France (EDF) has bucked this trend, despite its increasingly precarious financial position. However, even here, it is anticipated that the changes in market rules in 2016 will reduce its income. As credit ratings agency Moody’s notes: ‘A prolonged period of low power prices will further affect EDF given its exposure to market-exposed generation activities. Moody’s estimates that approximately 50% of EDF’s EBITDA is derived from market-exposed generation following the end of certain regulated tariffs in France.’65 Other traditional power utilities in Europe, such as Enel of Italy, are protected from fluctuations in the market price for electricity, as they operate in more regulated markets where retail prices are fixed.

There have been significant changes in the operating income of many companies in Asia. Japanese companies that operated nuclear power plants have suffered significant impacts from the closure of their reactors: for example, the income of Tokyo Electric Power Company (TEPCO) fell from nearly $5 billion in 2010 to a loss of more than $3 billion in 2011. Higher retail prices subsequently enabled TEPCO’s income to recover, even though the company had not restarted its reactors. In 2015, TEPCO’s income topped $4 billion, although this fell to $1.2 billion in 2016.66 The company has also benefited from a government bail-out thought to have cost up to $137 billion.67 By contrast, KEPCO in South Korea experienced remarkable growth, with income rising from a loss of $2 billion in 2012 to a profit of $6.7 billion in 2016. This was largely because prices for fossil fuels – one of KEPCO’s chief costs – have fallen while the tariffs it charges have remained fixed, boosting profitability.

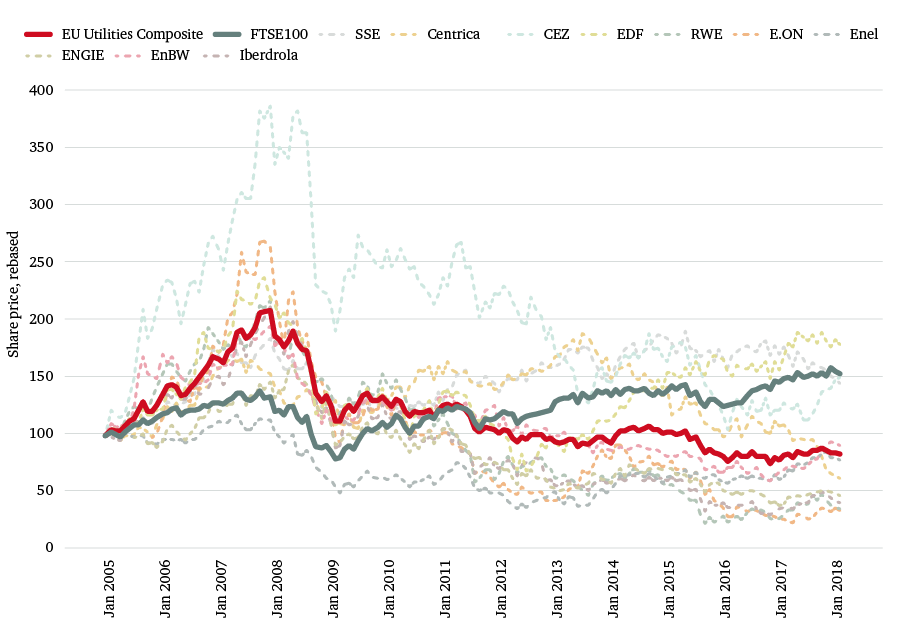

Share prices offer a clear indication of how the perceived value of the power sector in Europe has changed (see Figure 7). Shares of traditional utilities, like those of other companies, rose in the second half of the last decade until the 2008 financial crisis, when they fell sharply. Although utilities’ share prices briefly picked up after that point, they then declined again even as shares in other sectors rallied. The composite share price in Figure 7 is an average of the largest listed power utilities in Europe.68 RWE and E.ON of Germany and EDF of France experienced the greatest losses. SSE of the UK and CEZ (Czech Republic) outperformed the FTSE 100 Index until the end of 2015. Between the end of 2006 and end of 2016, the average share price of the major power utilities in Europe halved, while the FTSE 100 Index rose by 15 per cent.

Figure 7: Share prices of the 10 largest listed European power utilities, and the composite (average) share price compared to the FTSE 100, rebased to 2005

Figure 7: Share prices of the 10 largest listed European power utilities, and the composite (average) share price compared to the FTSE 100, rebased to 2005

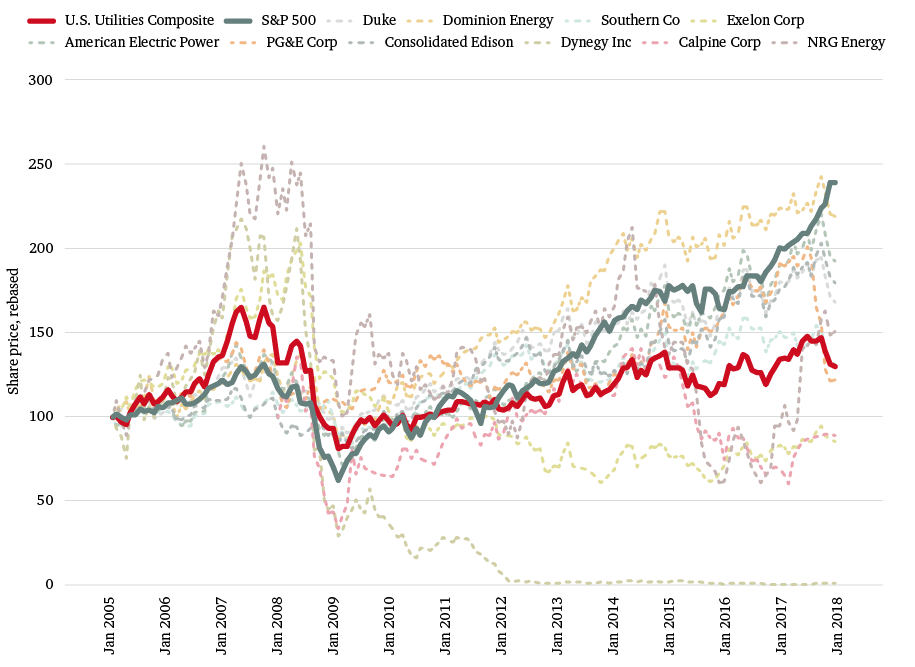

The situation is slightly different in the US, depending on the type of market in which a given utility is operating. Traditional utilities in regulated markets with guaranteed electricity prices are either surviving or, in some cases, flourishing. Those in markets without fixed prices are suffering. The 2018 Moody’s outlook for the unregulated power and utility sector has remained negative, due to ‘anemic demand, an oversupplied market and low wholesale power prices’. Power utilities primarily operating coal and nuclear plants are particularly affected. However, the credit ratings agency notes that ‘for regulated utilities, the stable outlook affirms Moody’s expectation that regulators will continue enabling utilities to recover costs and maintain steady cash flows’.69

Figure 8: Share prices of major power utilities in the US and the composite (average) share price compared to the S&P 500 Index, rebased to 2005

Figure 8: Share prices of major power utilities in the US and the composite (average) share price compared to the S&P 500 Index, rebased to 2005

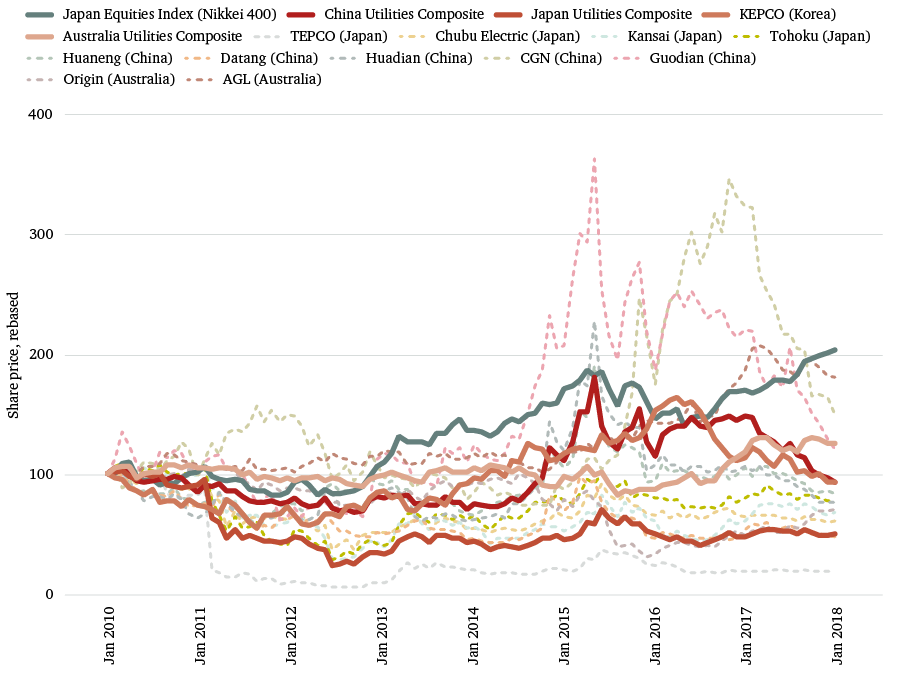

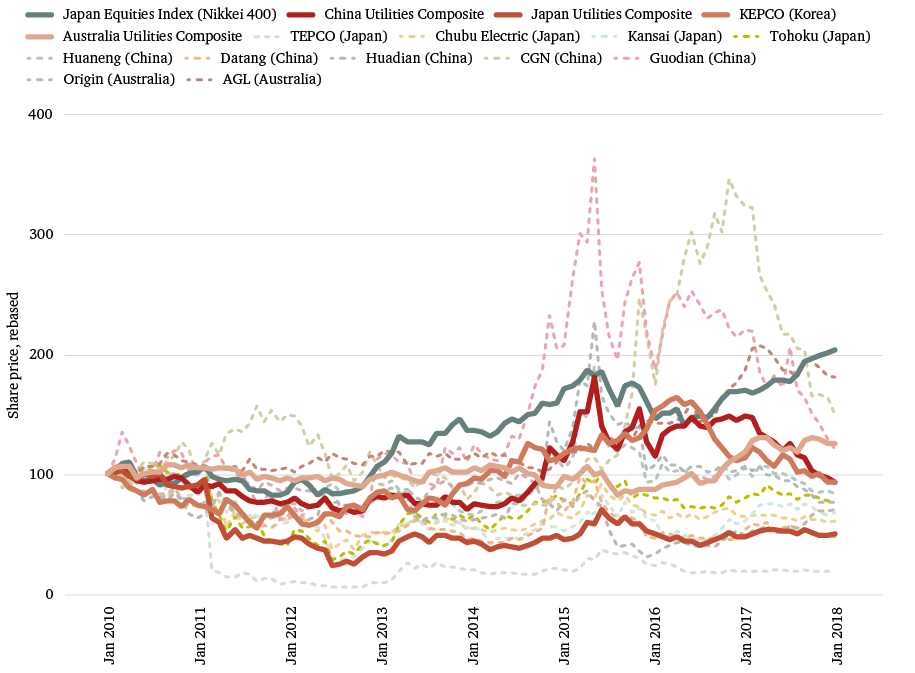

In the Asia-Pacific region, changes in share prices show clear differences between power utilities (see Figure 9). The immediate impact of the Fukushima disaster on Japanese companies is clear and expected, with a massive fall in value. Surprisingly, their share prices had not recovered even five years after the tsunami. This could be because nuclear power plants were not restarted. As of mid-2018, only nine reactors were operating. Legal battles are ongoing,70 as are actions by shareholders to prevent any further use of nuclear power.71

In Australia, the share prices of power companies have shown divergent trends, averaging each other out. Overall, power companies’ share prices have remained stable over the past five years. Although demand for power has been flat, the European trend of equity valuations falling in tandem with power prices and market share is not yet evident in Australia.

In South Korea, as mentioned, lower fossil fuel prices combined with fixed retail prices have boosted the earnings of KEPCO, which until 2016 was reflected in its higher share price. In China, the fall in share prices in mid-2015 likely reflected the turbulence of the stock market during that period, rather than the fundamentals of the companies per se. However, the fact that power demand in 2015 recorded its smallest increase for decades possibly undermined the outlook for Chinese power companies.

Figure 9: Share prices of major power utilities in Asia and the composite (average) share price compared to the Nikkei 400 Index, rebased to 2010

Figure 9: Share prices of major power utilities in Asia and the composite (average) share price compared to the Nikkei 400 Index, rebased to 2010

The credit ratings agencies have been worried about the power sector for some time. In February 2016, Standard & Poor’s (S&P) imposed negative rating actions on 16 parent utility companies across Europe. This included placing EDF, EnBW, E.ON and Vattenfall on ‘Credit Watch’, with negative implications for their long-term corporate credit ratings. S&P also placed ENGIE, RWE and Edison on Credit Watch negative, citing the fact that electricity prices were creating structural changes and that market design in the EU presented challenges for the sector.

For the Asia-Pacific region (excluding Japan), Moody’s offers a mainly stable or positive outlook for the power sector, due to steady demand growth, but with potential future divergences across the region as carbon transition policies differ between countries.72 In Japan, in 2015 Moody’s noted that proposed reforms could weaken the utilities’ credit quality: ‘The utilities’ relatively high ratings have been underpinned by their protected monopoly position, and a supportive and relatively predictable regulatory framework.’73 In 2017, Moody’s noted that the ‘competitiveness of renewable generation could increase the utilities’ risk of having underutilized thermal power assets’.74

In the US, the administration of Donald Trump has proposed new legislation that would enable coal, hydropower and nuclear generators to receive higher payments through a mechanism whereby ‘certain reliability and resilience attributes of electric generation resources are fully valued’, according to the US Department of Energy.75 Independent system operators and regional transmission organizations would be required to allow certain ‘resilient’ power plants to get a ‘fair rate of return’, even when prices would otherwise be lower.76

Response of traditional utilities

Among the three factors shaping the first phase of electricity system transformations, traditional utilities are currently responding most clearly to the continued cost reductions and deployment of renewables. Before the COP23 UN Climate Change Conference in Bonn in November 2017, Iberdrola, Enel, EnBW, EDP, Orsted and SSE collectively called for the EU to increase its target for renewables to 35 per cent of EU energy consumption by 2030.77 The move appeared to recognize the diminishing role and value of fossil fuel generators, which could be offset for the utilities by greater policy ambition to deploy renewables.

Privatization and liberalization have brought radical restructuring of the electricity sector, with state-owned monopolies forced to separate their business activities. In theory, new companies should enter the market and increase competition. However, the process has not fundamentally changed the operational regime, as new companies have usually been subsidiaries of established power companies. To date, these companies have not been interested in significant reform of their operational regimes, but rather have sought to maintain a business-as-usual approach.

The second phase of power sector transformations is set to further deconstruct energy services into smaller and distinct functions, which could be undertaken by new market actors. Unlike with previous market reforms, traditional energy companies may not be best suited to operating in these smaller market segments. In some cases, they may not even have the ability to do so.

Utility companies are aware of the technological and political transformations under way, and recognize that the pace of technological change is accelerating. In a 2016 global survey of power companies and utilities, 57 per cent of CEOs were concerned by the speed of technological change; significantly up on the 2013 share of 29 per cent. Over the same period, concern also grew over the potential shift in consumer spending and behaviour, with 64 per cent of respondents expressing concern, up from 29 per cent in 2013.78 Corporate strategies and structures are now being adjusted to reflect these issues.

Box 4: The three responses of utilities

In general, utilities have had three options for responding to ongoing and impending changes in the power sector: transform their business; try to entrench their market position; or leave the market. These options are not mutually exclusive, and some companies are attempting to undertake more than one strategy at a time.

Transform: This involves moving away from conventional generation to a business model focused on managing electricity flows. Key elements of this model include ownership of the electricity networks; grid balancing, including storage; development of non-fossil fuel generation (usually renewables); and greater engagement with consumers, including the sale of energy services.

Entrench: Many of Europe’s coal and nuclear power plants were built before the 1980s. Many of these assets are not expected to continue operating in the long term, because significant investment may be needed to meet new environmental standards. However, they have low operating costs and thus remain potentially attractive assets or investments in the short term.

Leave: Some European companies are choosing to focus their attention on new investments or parts of their existing businesses outside their home markets, particularly in North and Latin America. In such regions, the operating environment is more conducive to conventional utilities’ existing business strategies – which are based on large centralized production and often fixed retail prices, and which are therefore relatively low-risk.

Leading private-sector players are already undertaking corporate reform and investing in infrastructure and technologies to address shifting markets. In 2016, German utilities E.ON and RWE separated their clean and conventional energy assets into two listed companies. In 2018, E.ON proposed buying Innogy, a renewables-focused subsidiary of RWE, and the Italian utility Enel merged with its renewables subsidiary to boost revenue growth and generate synergies.79 GDF-SUEZ, now rebranded as ENGIE, has stated:

The world of energy is undergoing profound change. The energy transition has become a global movement, characterized by decarbonization and the development of renewable energy sources, and by reduced consumption thanks to energy efficiency and the digital revolution.80

Traditional European utilities have directly filed fewer patents in recent years.81 Energy companies can take advantage of new ownership structures by partnering with technology firms. The Italian utility Enel, for instance, has signed an agreement with Tesla of the US to test batteries in solar PV and wind plants and to integrate renewables into the grid.82

Japan’s TEPCO announced in 2016 that it would be restructuring the company into four different parts: a nuclear and decommissioning division; a fuel and thermal capacity division; a transmission and distribution division; and a retail operation. After retail markets were liberalized in April 2016, incumbent generators began losing millions of customers. As a result, 18 months later, 8 per cent of customers (5.1 million retail customers) had switched supplier.83

Unlike many other traditional utilities in Europe, EDF of France does not seem to be embarking on a significant restructuring, but rather is proposing to sell existing assets in other countries to maintain its current domestic supply mix, which is dominated by nuclear power. It has announced €55 billion in investment to extend the operational lives of its current reactors.84 EDF Energy, its UK subsidiary, is building two new European Pressurized Water Reactors (EPRs) at Hinkley Point. Despite this, EDF’s annual report notes the changes in the power sector and states the following:

The transformation of the energy sector and of society’s expectations is a spur to rebalancing our assets and production mix. As well as being an invitation to develop decentralised energy solutions and services.… it’s also an incentive to invest outside Europe in order to boost our growth.85

Press reports suggest that the French government is considering restructuring EDF, including creating a standalone company that holds all the nuclear assets.86

In China, despite many reforms across the country, dispatch is still centralized and incumbent generators are delaying widespread changes to the market. Local or regional planners allocate the power plants’ operating hours. This is different from most markets elsewhere, which prioritize operations in real time based on the lowest bids; in some countries, preference is given to low-emission generators. However, in China some reforms are being proposed that would factor in marginal pricing, thus rewarding renewable generation over coal.87

In South Korea, KEPCO remains a vertically integrated power company. Attempts to liberalize the sector halted in 2004. However, in 2015 the government announced a New Energy Business Model Initiative to encourage EV development, the development of microgrids and opportunities for individual producers to sell into the grid. In late 2017, the Ministry of Energy published a power supply plan to increase renewables’ share of power generation to 20 per cent by 2030, and to install an additional 47 GW of solar PV and wind capacity. Such deployment levels will require KEPCO’s support.88

Iberdrola is a European utility committed to reducing its emissions by 50 per cent on 2007 levels by 2030, and to being carbon-neutral by 2050. The company operates in five countries: Spain, the UK, the US, Mexico and Brazil. It has a total installed capacity of 44 GW, of which 14.6 GW consists of renewables. The company is shifting from coal into gas and renewables in Europe, and increasing power production in Latin America. International diversification is a key component of Iberdrola’s corporate strategy.89