2. The Second Phase of Transformations

The electricity sector – already in a state of flux due to the rise of renewables, more stringent efficiency standards and market reform – is also facing a ‘second phase’ of transformations characterized by enhanced flexibility and the emergence of new market actors.

A high proportion of generating capacity from variable renewables (wind and solar PV) leads to higher integration costs, in particular where national power systems are designed and operated for centralized and dispatchable generators. But a plethora of parallel innovations now promise to counter this dynamic, increasing system flexibility and thereby minimizing integration costs.

The challenge for regulators is how to incentivize sufficient flexibility in a way that enables the grid to remain affordable and reliable at higher penetrations of renewables – i.e. so that consumers benefit in aggregate from low-cost renewables while poorer households do not face higher energy costs.

The early parts of this chapter describe how flexibility lies at the heart of the dilemma for the electricity sector in terms of integrating low-cost renewables without incurring high system costs. Subsequent sections describe in detail the role of key technologies and infrastructure and their wider impact on the electricity sector and traditional utilities. These technologies and infrastructure applications include EVs, electrified heating, digital infrastructure, interconnectors, stationary storage, and flexible and responsive demand.

Box 5: System integration costs – the importance of the whole system

The connection of any new generator will impose system integration costs (SIC) on the larger system, depending on the characteristics of the generator involved. Determining whole-system costs (WSC) requires the quantification of SIC in addition to either generation costs or the levelized cost of electricity (LCOE). While most analyses focus on the SIC of variable renewables, the inflexibility of nuclear plants and the relatively slow ramp rates90 of coal generators also account for non-negligible SIC.91

The key determinant of the SIC of a newly connected generator is the mix of generators already within the system. The greater the diversity and flexibility of the system, the lower the SIC will be. Hence, renewable SIC vary significantly from one system to another, depending on the market share of renewables and the characteristics of the generators already in a given system.

There are several categories of SIC impacts, the quantification of each of which depends on the wider system and its flexibility. Impacts also overlap and interact, making quantification complex. Many recent studies advocate, and employ, a WSC approach to avoid double counting any impact, but such approaches require complex computational modelling.

The flexibility of the system to incorporate variable renewables at low SIC is dependent not just on the characteristics of the current system, but on the extent to which SIC impacts overlap and the market share of the generator being integrated. SIC are also increasingly determined by the uptake of emerging technologies and corresponding new system services that enable greater flexibility. SIC can broadly be divided into discrete but interacting categories (see Table 1). While these impacts exist for all generators, the descriptions of the impacts are given here in relation to renewables.

Table 1: Categories of SIC impacts in relation to renewable generators

|

SIC impact |

Description |

|---|---|

|

System balancing and reserve |

Variable renewables may increase supply fluctuations, leading to increased system balancing held in reserve. SIC: $14–42/MWh (35 per cent penetration).(i) |

|

Peak demand capacity (capacity credit) |

As a proportion of installed capacity, renewables tend to replace less of the capacity required to meet peak demand than conventional generators; as such, the system capacity increases. Capacity credit is a measure of how much capacity can be replaced without reducing system reliability. SIC: $3–25/MWh (30 per cent penetration).(ii) |

|

Network upgrading |

New and reinforced network cables may be required to enable power from renewables to reach centres of demand. SIC: $7–49/MWh (30 per cent penetration).(iii) |

|

Curtailment of renewables |

Curtailment (lowering the useful power output) tends to result either from the power being transferred exceeding network capacity or from renewable supply exceeding demand. |

|

Conventional plant ramping |

Balancing renewables’ variability results in ‘ramping costs’ – the burning of additional fuel to reach operating conditions. |

|

Frequency regulation |

The spinning inertia of conventional generators provides frequency stabilization. Renewables increase the need for dedicated frequency regulation services. |

|

Merit order effect |

Low-cost or prioritized renewable generation results in conventional generators operating for fewer hours, reducing their profitability. As their services may be still required (e.g. to provide peak demand capacity), subsidized operation (e.g. in the form of capacity credits) may be necessary. |

Sources: (i) Heptonstall, Gross and Steiner (2017), The costs and impacts of intermittency – 2016 update. (ii) Ibid. (iii) Ibid.

The most obvious overlap or interaction between impacts is that increasing the system balancing capacity held in reserve also provides the ability to meet peak demand. Therefore, costs associated with renewables in one SIC category could be offset by a reduction in another. Many SIC relate not just to renewables but to all generators. The danger of overestimating any SIC, combined with over-attribution of SIC to renewables, is a factor behind the increasing move towards WSC approaches.

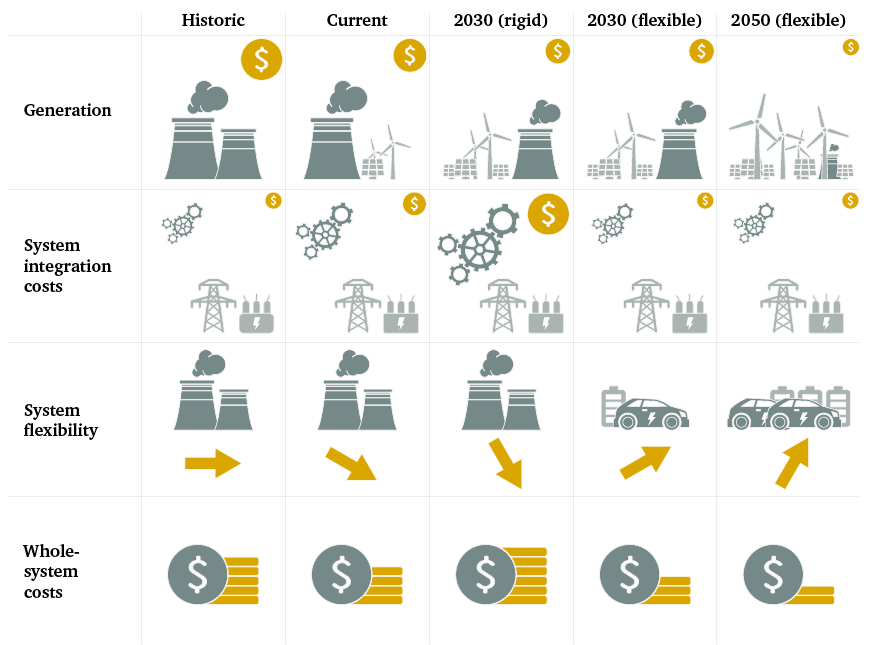

Figure 10: Illustration of the change in SIC and WSC with renewable penetration and increased flexibility of EVs and battery storage

Figure 10: Illustration of the change in SIC and WSC with renewable penetration and increased flexibility of EVs and battery storage

Sources: Compiled by authors.

An inflection point?

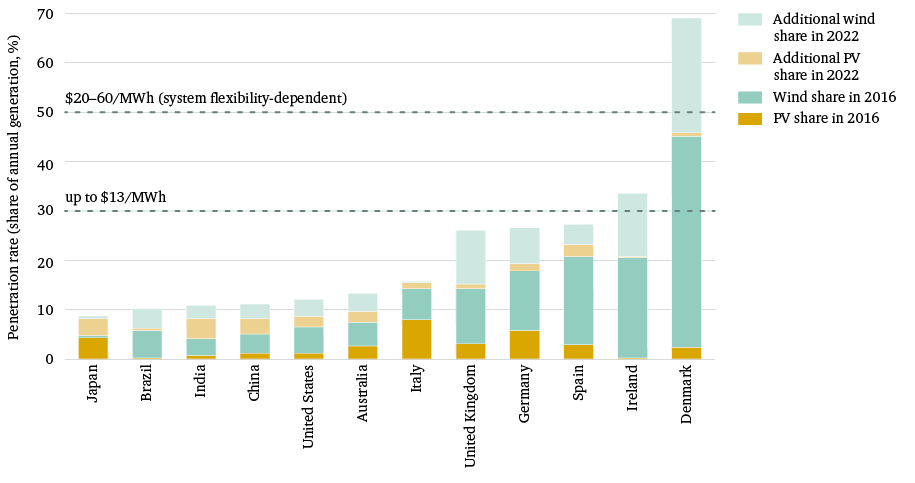

At their current penetration levels,92 solar PV and wind power are easily absorbed by the existing power system in most markets, with minimal impacts in terms of system integration costs (SIC).93 In China, India and the US, the penetration levels of solar PV and wind are currently at around 5 per cent, and rising rapidly. In European countries such as Spain and Germany, equivalent levels are at or marginally above 20 per cent.94 Certain regions within the above sets of countries are exceeding national norms: for instance, in the US state of Texas, solar PV and wind power are expected to exceed 20 per cent penetration this year; the state supplied 25 per cent of wind power in the US in 2016.95

With these technologies expected to reach 30 per cent penetration rates in many countries in the next five years, concerns over the costs of integrating solar PV and wind power into the system have increased. For up to a 30 per cent share of generation, variable renewables’ SIC are estimated to be up to $13/MWh (see Figure 11).96 With wholesale prices in Europe and the US at 10-year lows,97 SIC of $13/MWh would represent around 30–40 per cent of current wholesale prices. As Figure 11 indicates, as the share of generating capacity shifts increasingly to wind and solar PV, integration costs could rise substantially to between $20/MWh and $60/MWh at a 50 per cent share of generating capacity. Crucially, this range is dependent on the flexibility of the system.98

Figure 11: Solar PV and wind power – share of generation in relation to current and expected system integration costs

Figure 11: Solar PV and wind power – share of generation in relation to current and expected system integration costs

If generation costs continue to fall as renewable technology costs decline, how much will this compensate for higher SIC? A 2016 report published by Imperial College London explored a scenario in which wind generation capacity in the UK increased fivefold.100 Under this scenario, while the SIC associated with the provision of reserve and response services increased by an order of magnitude, the falling costs of wind generation more than compensated for this – resulting in system costs falling by 33 per cent.

Whole-system costs (WSC) and retail tariffs are more likely to remain affordable if policymakers prioritize system flexibility alongside the integration of low-cost renewable generators. WSC should, in theory, be passed through into the wholesale market price.101 However, a direct comparison between SIC or WSC and the change in market price is contingent on how any particular market is structured, and may not reveal the true economic cost.102

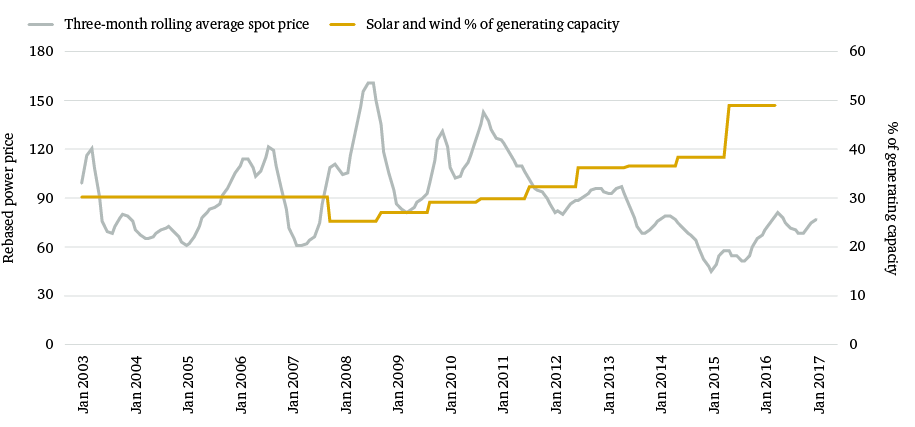

Denmark is an interesting exception. Its system has a high market share of wind power (over 40 per cent of installed capacity). Wholesale prices have declined in recent years even as wind generation has increased (see Figure 12). The Danish system is unique in that a significant proportion of electricity is generated by combined heat and power (CHP). Historically, electricity generation from CHP units has followed demand for heating. The introduction since 2005 of regulations to increase the flexibility of the power generated by CHP units, combined with increased interconnector capacity, has enabled prices to remain low, even as wind power has increased its share of generation.103

Figure 12: Denmark – wholesale electricity prices compared to solar PV and wind power’s share of generating capacity

Figure 12: Denmark – wholesale electricity prices compared to solar PV and wind power’s share of generating capacity

The importance and provision of flexibility

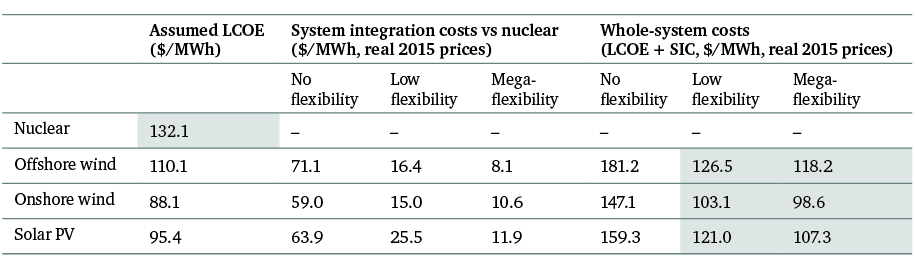

Although the Danish system is unique, it illustrates an important point: increasing the flexibility of the system as a whole can counter SIC impacts.104 The impact of system flexibility on SIC and WSC can be illustrated by contrasting a scenario of high renewables penetration, in which system flexibility is enhanced, with a scenario weighted towards nuclear power, which is generally regarded as the least flexible generator. As demonstrated by the shaded areas in Table 2, even a low-flexibility 2030 scenario in which variable renewables account for around 50 per cent of generation could enable the WSC of solar PV and wind power to be lower than the levelized cost of electricity (LCOE) of nuclear power. Under this (UK-focused) scenario, it is assumed that flexibility is provided by 5 GW of battery storage, a 25 per cent uptake of flexible demand, and an expansion of interconnection from 4 GW to 10 GW.105

Table 2: LCOE, SIC and WSC of solar PV and wind relative to the LCOE of nuclear power in 2030, at around 50 per cent variable renewable market share, under various flexibility scenarios106

Source: Adapted from Strbac and Aunedi (2016), Whole-system cost of variable renewables in future GB electricity system.

Table 2: LCOE, SIC and WSC of solar PV and wind relative to the LCOE of nuclear power in 2030, at around 50 per cent variable renewable market share, under various flexibility scenarios106

Source: Adapted from Strbac and Aunedi (2016), Whole-system cost of variable renewables in future GB electricity system.

System flexibility can be accomplished by several means. Denmark used regulatory reform to incentivize ramping of CHP generation, and also increased interconnector capacity. Flexibility can be provided through new technologies such as battery storage, interconnectors, flexible demand (via digitalization and control) and artificial intelligence system control; as well as through non-technology-dependent measures such as regulation and market design.108

Although second-phase transformations of the power sector are likely to revolve around the flexible, low-cost integration of competitive renewables, the exact mix of flexibility-enabling technologies and accompanying regulations is uncertain. For instance, the deployment of EVs and battery storage is likely to vastly increase system flexibility. However, flexibility could also be enhanced by hydrogen storage, as hydrogen vehicles reduce the cost of low-carbon hydrogen production via electrolysis. Uncertainty also exists over the development of market flexibility mechanisms such as locational marginal pricing and capacity markets. The following sections investigate the technologies likely to be integral components of the second phase of transformations, and their relevance to system flexibility.

Electrification – increased demand, flexible consumption?

Because growth in electricity demand is slowing in many regions, power companies are likely to welcome further electrification. In the coming decades, EVs will be at the forefront of this process. This could be followed by electrification in the heating sector, as well as within industry. Given the impacts of the first phase of transformations, a key question for traditional utilities and the wider power system is how system flexibility will be affected by these electrification technologies. Could the benefits for utilities of increased electrical demand be undermined by greater deployment of renewables, enabled by more flexible electrification?

The rise of electric vehicles

EV sales are set to increase dramatically, stimulated by government targets, policy support and sharp declines in the prices of lithium-ion battery packs. In the first quarter of 2018, worldwide EV sales grew by 59 per cent compared with the same period a year earlier. EV lithium-ion battery costs have fallen by three-quarters over the past six years.109 Another 30 per cent reduction in lithium-ion battery prices by the end of the decade could be achievable, as global manufacturing capacity for such batteries looks set to increase sixfold by 2020.110 Each time cumulative production of lithium-ion batteries has doubled, prices have fallen by 19 per cent.111 A similar phenomenon, known as the ‘learning rate’, has helped to drive down the cost of solar PV modules in recent years.

Many large and powerful car manufacturers are entering the EV market, prompted by the speed at which the total cost of ownership of EVs is approaching that of ICE vehicles, and by government sales targets.

Unrelenting global urbanization and increasing concerns over air pollution – especially in cities where EV range is not an issue – have pushed EVs further into the political limelight. China has asked all its car manufacturers to ensure that 8 per cent of their sales come from EVs by 2018, rising to 12 per cent by 2020.112 It has also started research into phasing out production of vehicles powered by internal combustion engines (ICEs).113 In Europe, the UK recently joined France and the Netherlands in looking to ban sales of diesel and petrol vehicles by 2040. The Norwegian government – a pioneer in EV deployment – thinks EV subsidies will be unnecessary as early as 2025.114

Many large and powerful car manufacturers are entering the EV market, prompted by the speed at which the total cost of ownership of EVs is approaching that of ICE vehicles, and by government sales targets. Honda is striving to ensure that two-thirds of its global sales are electric by 2030;115 BMW is aiming for 15–25 per cent by 2025;116 and both Volvo and Jaguar Land Rover are targeting 100 per cent EV or hybrid sales by 2020.117 Volkswagen has been aiming for 25 per cent for some time,118 and Nissan’s EV Leaf is doing so well that Nissan is branching into home battery storage.119

Analyst forecasts reveal the growing consensus over EV deployment rates. BNEF anticipates that by 2040 EVs will account for one-third of all vehicles on the road.120 Even OPEC, which represents oil exporters and might be expected to remain bullish on ICEs, more than quadrupled its EV deployment forecast between 2015 and 2016. Since then, its projections have risen still further. As of November 2017, OPEC was forecasting that the global fleet of hybrids, plug-ins and pure battery EVs would total 338 million in 2040.121

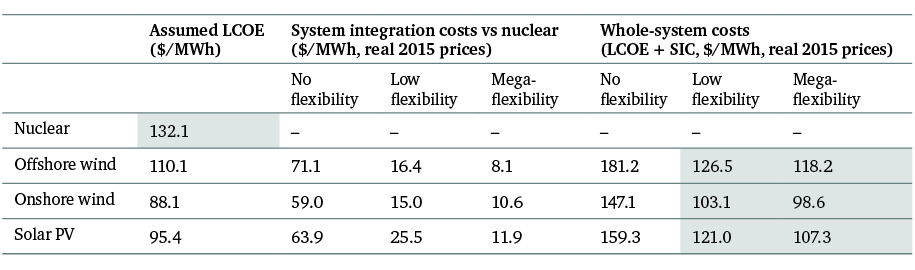

As a result, global EV electricity demand looks set to rise by at least 7 per cent by 2040, to more than 1,400 TWh (see Figure 13) – a level 40 per cent higher than global solar PV and wind generation in 2015. These increases in electricity demand are contingent not just on growth of the global fleet of EVs, but on how driverless technology develops. EVs capable of driving themselves would potentially significantly increase the vehicle miles travelled. If driverless technology led to a 50 per cent rise in EV miles travelled, as some suggest is likely, then global EV electricity demand could reach 2,200 TWh by 2040. That said, to put this in perspective, this would be equivalent to annual average growth of just 0.4 per cent in global total electricity demand, modest in the context of historic demand growth.

Figure 13: Projected increase in EV electricity demand by country or region, 2017–40

Figure 13: Projected increase in EV electricity demand by country or region, 2017–40

The use of fast-charging points could significantly inflate charging costs for EV owners. A recent study has shown that many fast-charging outlets cost the equivalent of $3–$4/gallon. However, as 80 per cent of charging occurs at home, the median annual savings on fuel costs offered by an EV compared to an ICE vehicle currently exceeds $770 in the US.122 While such savings are significant, policy attention could nonetheless benefit from ensuring that fast-charging costs do not hinder deployment rates.

Hydrogen vehicles remain a tiny niche market. Although their implications for the future of the power sector should not be entirely discounted, only 2,500 such vehicles were sold or leased in 2016,123 a number 100 times smaller than that for EV sales in the final quarter of the same year. The deployment of hydrogen refuelling stations also lags far behind that of EV charging points: as of the end of 2016, there were only 285 hydrogen refuelling stations globally124 – 3,000 times less than the number of EV charging points that were installed during 2016.

Box 6: Flexible EV charging

From the perspective of power utilities, transport electrification presents both opportunities and risks, depending on how EV charging profiles develop. If EV charging is staggered via smart technology, so that demand is spread over the evening when drivers return home and sufficient charging infrastructure is deployed to enable daytime charging while people are at work, then national demand profiles will flatten and peaks will reduce. Combined with increased electrical demand, this could strengthen power utilities’ traditional business models, as fossil fuel generators’ utilization rates125 could increase while less reinforcement of the grid could be required.

While flattened national demand profiles could enable greater use of fossil fuel generators, smart staggering of EV charging could go further, increasing the flexibility of the system and allowing greater integration of renewables. By 2030, the UK could benefit from 11 GW of additional flexibility, equivalent to 18 per cent of current generating capacity, due to smart EV charging.126 If smart charging were combined with powerful new methods of predicting wind speeds and solar irradiance, it could allow EVs to be charged in accordance with fluctuations in renewable supply. From the perspective of the power utilities, which own a greater proportion of fossil fuel generators, this presents a distinct risk – as it could undermine potential demand growth from transport electrification.

Investment in public EV charging infrastructure is accelerating. In 2016 it grew sevenfold globally, relative to 2015, to $6 billion, with 880,000 charging points added.127 Smart charging requires two-way communication between the system operator and charging point, but this capability is not currently built into standard EV charging points. Many smart-charging pilot schemes are under way. In the UK, for example, £2.2 billion worth of anticipated network upgrades could be avoided if trials such as Electric Nation demonstrate the feasibility of restricted charging, or of variable-tariff-incentivized charging.128

Staggered smart charging could also be complemented by vehicle-to-grid (V2G) charging, whereby an EV uses a charging point to discharge power back to the grid, just as a stationary storage battery would do. Nissan is currently working with traditional utilities in Denmark and the UK, offering free electricity for drivers of the new Leaf model in return for drivers using a bi-directional charger that enables power to be transferred from the vehicle’s battery back to the grid.129 Given the anticipated speed of adoption of V2G charging, this could result in unprecedented system flexibility. To match a typical 500-MW power station’s output over one hour would require around 83,000 V2G EVs fitted with 60-kWh battery banks to deplete their batteries by only 10 per cent (the calculation assumes the presence of a fleet of 330,000 such vehicles, 25 per cent of which are connected to the grid and willing to discharge to the network at a given time).

Power utilities and network operators will increasingly need to work with technology companies, EV manufacturers, policymakers and city planners to ensure that as electrical demand increases, smart staggered charging can capture the full benefits of the burgeoning EV market.

Buildings and the electrification of heat

Given that electricity demand growth from EVs may not be enough to rescue the power utilities’ business models, could electrification of heating support their revenues more?

The buildings sector accounts for around 32 per cent of global final energy consumption,130 using the equivalent of more than 35,000 TWh of electricity per annum.131 Of the 21,000 TWh of current annual global electricity demand, around 50 per cent is consumed in buildings.132 Appliances, lighting and cooling are almost entirely powered by electricity, while a significant proportion of heating applications (including space and water heating within buildings, as well as cooking) remain unelectrified. Growth in demand for the energy services that appliances and lighting deliver is likely to be offset by increased energy efficiency. Electricity demand for cooling is also expected to grow. Globally, almost 80 per cent of energy demand in buildings is for heat.133

Demand for heating and cooling varies significantly between countries. That said, just 27 countries in the northern hemisphere account for 90 per cent of all residential heating. China accounts for almost 40 per cent of global residential heating demand.134 Biomass is the dominant source of heating globally. In developed regions, coal is being replaced by electricity and gas. Gas provides 40 per cent of heating in residential buildings in the EU, and is likely to dominate up to 2040,135 as the European gas network infrastructure is widely established. There are, nonetheless, large regional differences – in the UK, 19 per cent of electricity is already used to supply space and water heating.136

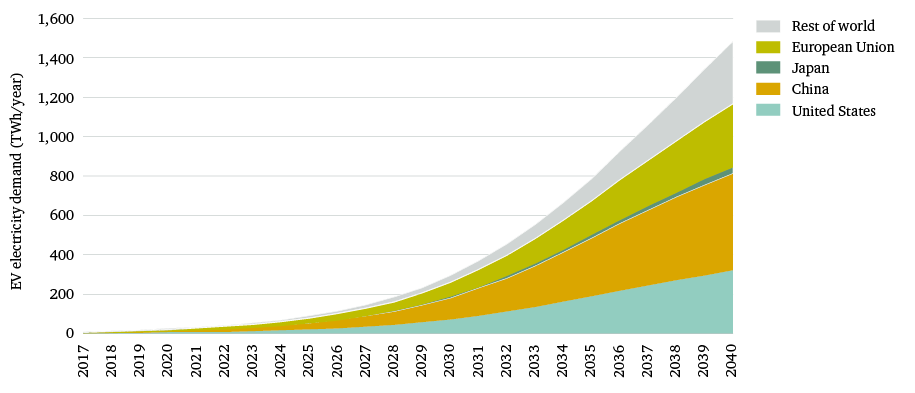

Decarbonization of the power sector and electrification of transport represent the principle focus of climate policy. Technologies to electrify the heating sector, such as heat pumps, are mature, but space and water heating remains largely unelectrified. This is principally because the cost competitiveness of heat pumps has remained weak. More than 7.5 million heat pump units were installed in the EU between 1995 and 2014; these produced 133.4 TWh of heat in 2014, equivalent to around 45 TWh of electricity demand.137 The competitiveness of heat pumps varies by region, depending primarily on the capital cost of boilers, fuel prices and the heating load. Heat pumps become more competitive as the heat load increases (see Figure 14); coupling heat pumps to multiple buildings within a district heating system, as is common practice in Sweden and Denmark, increases their competitiveness. This is particularly important in the context of efforts to increase the thermal efficiency of households; doing so reduces the heating load of individual dwellings and is increasingly cost-effective.138

Figure 14: Relative competitiveness of household heating technologies in the EU139

Figure 14: Relative competitiveness of household heating technologies in the EU139

A swift transition to electrified heating may yet occur. In northern China, district heating systems service almost half the urban floor area; 90 per cent of these systems were powered by coal in 2012.140 Increasing concerns over air pollution are starting to result in gas shortages, as the Chinese government attempts to shift households away from the use of coal towards gas.141 This could lead the Chinese government to direct more investment into the manufacture of heat pumps, thus lowering capital costs, a phenomenon already seen in China with solar PV and lithium-ion batteries.142

The UK provides a good case study of a country considering the impacts of the electrification of heating on total electricity demand. Across six 2050 UK energy scenarios (published in 2010), the average proportion of heat demand delivered by heat pumps was 67.3 per cent, resulting in 81 TWh of additional electricity demand per annum, equivalent to almost a quarter of current demand.143 Globally, heating electrification within buildings could add 5,000 TWh of annual electricity demand by 2040, an increase of 24 per cent on current levels.144

A significant hurdle to the integration of heat pumps into the electricity system is the coincidence between peak demand for heating and peak demand for electricity for other uses. Peak heating demand can be significantly greater than peak electrical demand, depending on the region, resulting in electrified heating significantly increasing peak electricity demand. In the 2050 UK scenarios, the average peak demand increases by 70 per cent.145 Unlike with EVs, it is much more challenging to shift demand for electrified heating to different times of the day. Consequently, increased system flexibility is less likely. One method of reducing peak demand for electrified heating is to install advanced thermal storage at the point of consumption, so that the heating load can be shifted forward in time. However, advanced thermal storage technologies, including phase-change materials, are currently prohibitively expensive.

As the burgeoning EV market requires less support, policy attention may soon start to refocus on the heating sector. Capturing the upside (for power suppliers) of increased overall electricity demand while mitigating the challenges of increased peak demand will require traditional utilities to manage many of the same trade-offs that EV integration increasingly requires of them. Cost-effective advanced thermal storage will be critical.

Box 7: Industry electrification

Across six 2040 scenarios – two each from the IEA, Shell and the International Institute for Applied Systems Analysis (IIASA) – it is anticipated that electricity will supply between 23 per cent and 38 per cent of industrial energy demand. The differences reflect variations in the sectoral demand mix, the relative cost of electrification and efficiency improvements, and the carbon mitigation options employed. Based on the average of these six scenarios, an increase of around 3,300 TWh in annual demand could be anticipated by 2040, equating to an annual growth rate of 0.6 per cent.

Many industrial processes require high-temperature heat (from 400°C to above 2,000°C).146 The electrification technologies available to supply such temperatures are limited, and the challenges across the subsectors of industry are more diverse than for domestic or commercial sectors. Electric-arc furnaces for secondary steel production show the greatest promise in terms of delivering industrial electrification;147 the technology currently accounts for around 29 per cent of global steel production.148

Flexible electricity demand within industrial processes offers substantial promise for traditional utilities seeking to strengthen their business models. As the electrical load of industrial applications is significantly larger than that of individual residential households, the economic barriers to flexibility are lower. The decision to reschedule industrial demand to weekends or night times depends primarily on the increased labour costs incurred, which may reduce as automation increases.

Future electricity demand growth

Globally, electricity demand within OECD countries – the markets for the majority of unbundled utilities – is likely to stagnate further in the coming decades, with most growth in demand originating from China, India, Southeast Asia, the Middle East and Africa.

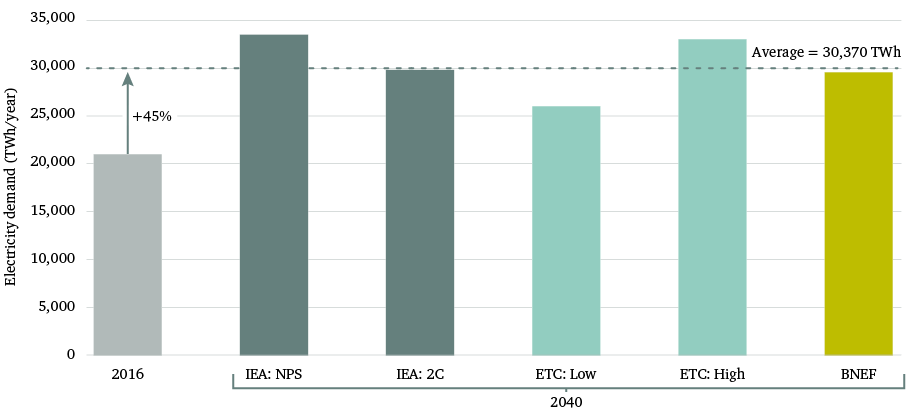

Stagnating or even declining growth in electricity demand has been one of the principle factors undermining traditional utilities’ business models. In the decade leading up to 2005, global annual demand growth averaged 3.3 per cent, slowing to 2.8 per cent in the following decade.149 Although more energy services, such as EVs, are likely to be supplied by electricity in the future, annual demand growth is still likely to slow to around 1.6 per cent out to 2040. This growth rate is derived from a comparison of five 2040 scenarios, illustrated in Figure 15.

Figure 15: Global electricity demand across a range of scenarios

Sources: IEA (2016), World Energy Outlook 2016; ETC (2017), Better Energy, Greater Prosperity; and BNEF (2017), New Energy Outlook 2017.

Figure 15: Global electricity demand across a range of scenarios

Sources: IEA (2016), World Energy Outlook 2016; ETC (2017), Better Energy, Greater Prosperity; and BNEF (2017), New Energy Outlook 2017.

Network transformations

The second phase of electricity system transformations will also bring significant changes to power networks. This section looks at the digital infrastructure revolution, the expansion of interconnection between national electricity systems, and the integration of modular battery storage at various levels of the network. All are part of the wider trend of enhanced system flexibility in response to the existing deployment of renewables, and are likely to reduce the future costs of further integration of renewables.

Even though new players in the renewables sector have undermined the power utilities’ stranglehold on generation, large network assets remain largely in the hands of the traditional, unbundled utilities. A 2°C world will require annual investment of at least $500 billion in renewables, 68 per cent up on 2016. Projected investment in future electricity network infrastructure, compliant with 2°C scenarios, is broadly in line with historic expenditure, at around $270 billion per annum.150 But while the absolute amount spent on the infrastructure of electricity networks may not significantly change, the allocation of investments is showing signs of a dramatic transformation.

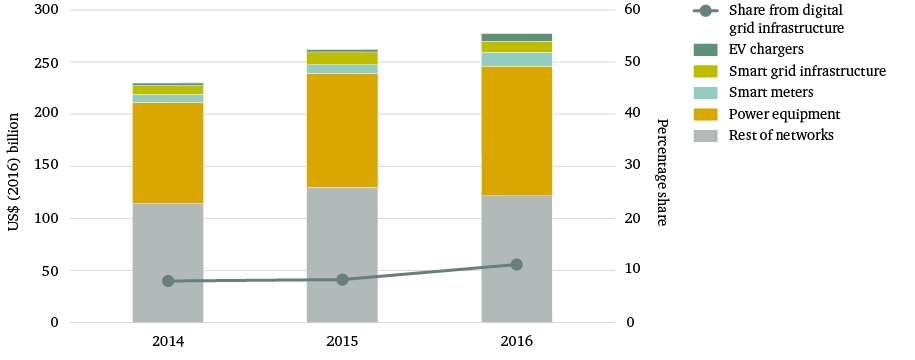

Currently 80 per cent of electricity network investments go into equipment such as cables, transformers, substations and switching gear. However, a growing proportion is being spent on the new digital infrastructure that will form the smart, flexible networks of tomorrow (see Figure 16). Almost half of such spending is intended to allow the connection of new sources of generation with new customers, the majority of whom are in non-OECD countries where networks are still growing. As such, 60 per cent of network investment decisions in 2016 in countries such as China and India were made by central government or grid monopolies, rather than by unbundled utilities.151

Figure 16: Share of spending on electricity network equipment by type

Figure 16: Share of spending on electricity network equipment by type

China offers a prime example of the need for rapid network transformation to accompany the integration of renewables into the electricity system. In the western provinces of China, which are rich in renewable resources, network investments have focused on high-voltage connections to high-demand centres in the east of the country, in order to reduce curtailments152 of power from wind generation and solar PV. In 2016, the curtailment ratios for wind power and solar PV in China were 17 per cent and 10 per cent respectively.153 The Chinese government is aiming to reduce curtailments to 5 per cent by 2020. The country reduced the curtailment of wind power, due to lack of grid capacity, by 7 percentage points during 2017, and officials have claimed that the problem will be solved by 2020.154 Significant amounts of hydropower were also curtailed in Sichuan and Yunnan provinces in 2017 – 142 TWh and 314 TWh respectively – representing a five- and sixfold increase respectively on 2013.155

Digital infrastructure

Digital infrastructure enables consumers and traditional utilities to monitor supply and demand as well as network performance. They can use such infrastructure to gather and share data, allowing real-time modification of supply, demand and network asset operation. This in turn helps to reduce peak load stresses on the network and optimize network assets, extending their operational lifetimes and boosting their value. The result is real-time, more accurate and often lower costs for consumers and utilities.

In a 2016 global survey of the 50 largest distribution utilities, 92 per cent of respondents said they were planning to invest in digital infrastructure in the next 12 months.156 On the demand side, these assets include smart meters, internet-connected fridges and smart EV charging facilities. For the network itself, digital infrastructure relies on advanced sensors, such as phasor measurement units (PMUs) that monitor grid stability; relay switches that detect and recover from faults in substations; and advanced feeder switches that redirect power around faults. Together these reduce the need to build costly high-voltage transmission lines, or to reinforce and upgrade substations and distribution networks. The subsequent lower network costs are another example of the reduction in SIC that is beginning to occur across the electricity system.

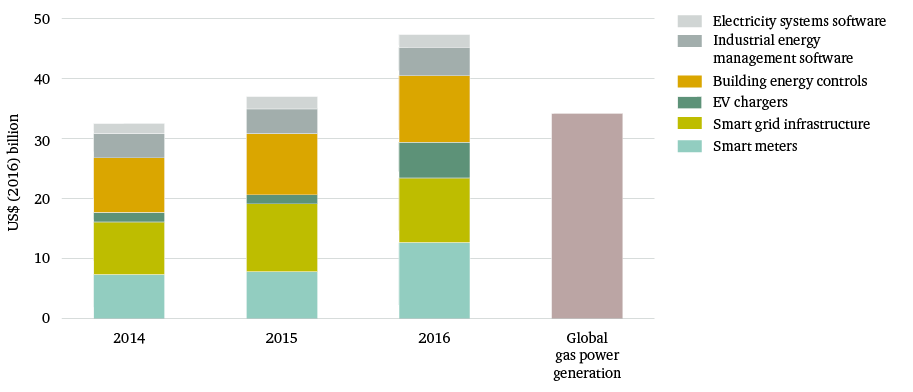

Digital infrastructure now represents 10 per cent of network spending; more is now spent on digital infrastructure globally than on gas power stations.157 In 2016, around $47 billion was spent on digital smart hardware and a further $2 billion on software and computational services (see Figure 17). Smart meters within buildings accounted for the greatest expenditure ($13 billion). Spending on smart grid infrastructure (grid monitoring and sensors) totalled around $10 billion.158

Figure 17: World investment in digital infrastructure and software in the electricity sector, by technology

Figure 17: World investment in digital infrastructure and software in the electricity sector, by technology

Software may account for a relatively small share of investment, but such spending promises dramatic improvements in system flexibility. In late 2017, grid operators from across Europe were reported as being in the final stages of launching a ‘digital information exchange platform’ in order to develop and share new applications for managing electricity flows and the growing amounts of renewable energy.159

Interconnection

One of the principle options for increasing system flexibility is increased trade of electricity via interconnectors160 across borders. During one day in May 2016 in Germany, for instance, generation from renewable sources was equivalent to almost 100 per cent of demand, but total supply exceeded demand by 16 per cent, indicating significant exports of electricity via interconnectors during this period.161

Increased interconnector capacities can reduce the impact of seasonal supply variations associated with some renewables, while also increasing competition and driving down wholesale electricity prices as markets become intertwined. It is estimated that the ‘Capacity Allocation and Congestion Management’ regulations, adopted by the EU in 2015 to enable greater interconnection-based electricity trade, could save EU consumers around €2.5 billion to €4 billion per year.162

The complexity of integrating electricity markets is prompting governments to pursue rapid expansion of cross-border interconnector capacity: over the 10 years ending in 2015, capacity grew by 81 per cent; it is likely to double by 2025, relative to 2015. Globally, there are currently around 12 proposals for regional grids; in 2016 high-voltage projects (regional and cross-border) accounted for 10 per cent of global transmission investment.

The scale of the infrastructure being built and planned is likely to lead to a significantly more flexible electricity system, further enabling renewable integration. Power utilities will need to adapt to this increased flexibility, and will need to acknowledge that the technical and cost limitations applying to the integration of renewables are likely to diminish.

Box 8: Microgrids in emerging power markets

Power utilities may increasingly seek to internationalize as traditional markets undergo the next phase of transformations. However, the growing number of microgrids and increased decentralization of renewable deployment within emerging economies could undermine this strategy.

In countries with a well-established centralized grid, microgrids do not make economic sense. But emerging economies and remote regions are increasingly combining hybrid renewable and storage systems with localized microgrids. Within countries where grids are already established, microgrids are relatively costly. In urban areas, the need to bury cables adds significant cost. In rural areas, long distances between buildings result in high cabling costs.

In emerging economies and remote locations, where power utilities may see future growth potential, low-cost solar PV and battery storage are enabling hybrid and microgrid systems to develop before centralized grids can be established. Globally, sales of diesel generator equipment fell by 25 per cent in 2016,163 while 36 per cent of Tesla’s battery storage capacity has been sold to remote islands for microgrid applications.164 Much of this renewed emphasis on microgrids has been stimulated by companies such as Facebook, Microsoft and others setting up the Microgrid Investment Accelerator,165 which aims to raise $50 million by 2020 in order to accelerate the deployment of microgrids in Indonesia, India and East Africa.166 Clearly it makes good business sense for digital media providers to enable new demand for their services by first supplying target markets with electricity. However, this may limit the opportunity for power utilities to expand into new markets.

Storage

Significant falls in the cost of lithium-ion battery storage could present the single greatest challenge to power utilities’ business models. The flexibility offered by affordable storage could undermine the need for peaking gas and coal capacity as the balancing technology of choice.

A virtuous circle is developing: the EV battery sector is finally providing increasingly affordable storage, which in turn is enabling greater integration of renewables as the system becomes ever more flexible.

Rapid cost declines in the EV lithium-ion battery sector are enabling cost-competitive stationary battery storage. Excess production capacity is causing manufacturers to sell new lithium-ion batteries into the stationary storage market at low prices.167 In the first half of 2017, lithium-ion batteries provided more than 90 per cent of utility-scale stationary storage. Of the 3.3 GW of installed battery capacity globally, more than 80 per cent is now lithium-ion.168

As such, a virtuous circle is developing: the EV battery sector is finally providing increasingly affordable storage, which in turn is enabling greater integration of renewables as the system becomes ever more flexible. This could allow EVs to be increasingly supplied by renewably generated power. The impacts on the electricity sector and power utilities will be significant, not least because vehicle manufacturers are such powerful companies.

Aurora Energy Research, a British research consultancy, estimates the 2016 intermittency SIC of solar PV in the UK at £1.3/MWh, assuming 11 GW of solar PV in the UK system. Under its 2040 scenario, which envisages capacity of 40 GW of solar PV, integration costs rise to £6.8/MWh. However, the introduction of 8 GW of battery storage could cause SIC to become negative, falling to -£3.7/MWh and thus providing a net benefit to the system rather than a cost.169

Figure 18: Total energy storage by commissioning date, excluding pumped-hydro

Figure 18: Total energy storage by commissioning date, excluding pumped-hydro

For now, electricity storage is still dominated by pumped-hydro storage. Of the 193 GW of global electricity storage, 95 per cent consists of pumped-hydro. Power utilities own just less than half of all pumped-hydro storage capacity, roughly the same share as for battery storage.170 Due to the vast reservoirs of water that pumped-hydro schemes maintain, on average pumped-hydro storage can discharge electricity at full power capacity for 10 times longer than batteries. However, due to the modular nature of batteries, capacity – and hence capital expenditure – can be optimized for specific functions and market requirements. Batteries also provide near-instant response times, therefore supporting more services such as frequency response, distribution network reinforcement and renewable integration.

Unlike pumped-hydro, batteries are not constrained by the need for a water reservoir at high altitude. The geographical specificity required for pumped-hydro also limits the amount of storage that can be built. Batteries are more versatile, capable of providing services at the varying scales needed for transmission, distribution and end-users respectively. For this reason, batteries are increasingly considered within the category of network infrastructure.

Build times on battery projects are also rapid, as demonstrated by the six-month build time of the Tesla storage facility at Mira Loma in California, and by the new AES Energy Storage system in San Diego, which took less than six months to complete.171 Both of these systems have been sited at substations. Many projects have not disclosed their capital expenditure. However, the authors estimate172 capital expenditure on the Mira Loma project at $0.46 million/MWh and $3.9 million/MW, compared with an estimated $0.12 million/MWh and $2.3 million/MW for the Nant de Drance pumped-hydro project in Switzerland. Nant de Drance is in its ninth year of construction – normal for pumped-hydro projects, which can take 10–13 years to complete.

At present, electricity prices do not fully capture spatial and temporal differences, meaning that the services provided by batteries are not fully valued in the market. Batteries can be deployed at various scales, almost anywhere on the network, unlike a gas generator or pumped-hydro facility. Some electricity market regulators treat batteries as power plants that use cheap electricity, while others consider them grid assets. The European Commission’s clean energy package attempts to clarify these differences by valuing flexibility. In the US, authorities in New York, Massachusetts, California and Oregon have set storage targets. By 2020, California aims to have 1.3 GW of electricity storage.173

The current rapid declines in the cost of lithium-ion batteries could mean that new mechanisms to capture the value of batteries will not be needed. General Electric has developed a hardware and software package that enables batteries to be integrated into any of its pre-existing steam and gas turbine power stations. These ‘hybrid electric-gas turbines’ can instantly respond in balancing markets, providing the generator with revenues that were previously inaccessible. At least two of these systems have been installed already, for Southern California Edison.174 This is not only an example of a utility transforming its business to directly integrate new technology into its existing offering, but is also an instance of transformation to a model based on increased flexibility – one that will enable increased integration of renewables at low SIC.

Box 9: The next generation of batteries and a second life for the old

Next-generation battery technologies will deliver greater energy densities. Metal-air batteries could achieve a density of 800 Wh/kg, three and a half times greater than that offered by lithium-ion batteries.175 While non-rechargeable metal-air batteries have been deployed commercially, rechargeable options are struggling176 due to low cycle efficiencies.177 The global metal-air battery market is expected to grow to $1.7 billion by 2018, initially dominated by zinc-air models.178

By around 2025, the first generation of EV batteries will need to be replaced to optimize vehicle performance, but they could still have a valuable ‘second life’ in stationary storage.179 The Renault-led Powervault partnership is one of several industry initiatives exploring the use of retired EV batteries in home storage systems.180 The business case for reuse could improve once complicated re-manufacturing processes are automated, but higher-performance next-generation batteries are likely to offer tough competition.

Software for the smart grid

Software to aggregate data and control assets in functionally smarter ways will likely have the greatest impacts on the flexibility of the electricity system. Machine-learning algorithms have the potential to optimize the rules governing system balancing and congestion management, thereby dramatically increasing system flexibility.

A flexible smart grid is only achievable if balancing mechanisms – such as battery storage, interconnectors, flexible demand and digital network infrastructure – can be controlled in smarter modes. Cloud computing, artificial intelligence, machine learning and distributed computing sit within the $2 billion investment bracket (for ‘software and computational services’) mentioned in the earlier ‘Digital infrastructure’ section. Spending on software currently accounts for less than 5 per cent of the $47 billion invested in digital infrastructure.181 However, such spending is expected to grow as development of a flexible smart grid, capable of processing and optimizing the network and wider system, progresses.

In the UK, congestion management costs have risen from £180 million to £463 million per year in five years, and in Germany from €165 million to €255 million.182 Currently, congestion management is based on overlapping rules, services, mechanisms and safety margins, handled by humans and standard sequential algorithms. This is where artificial intelligence teams such as DeepMind are now contributing expertise. DeepMind’s machine-learning optimization capabilities were used at Google to achieve a 40 per cent reduction in the energy used to cool servers.183 DeepMind is also reportedly working with National Grid in the UK184 to explore ways of reducing electricity demand by 10 per cent without the need for new traditional network infrastructure.

The digital and flexible demand transformation

Digitalization of the electricity system is not limited to the supply and network side. Automation technologies are also creating new capabilities for digitalized demand management. Digitalization could enable traditional utilities to increase their operational efficiency – for example, by enhancing control of infrastructure via remote sensors, improving management of supply chains, or optimizing internal accounting and customer billing.

The UK’s Electricity Networks Strategy Group sees the smart, digital grid as an ‘enabler for a radical departure from the operation of the current power system, with extensive balancing on the demand side’.185 Demand could be shifted forwards and backwards in time, within both the domestic and non-domestic electricity markets. National Grid anticipates that 2 GW of flexible demand will be required by 2020 to balance the UK system.

Flexible demand can reduce peak demand and flatten national 24-hour demand profiles, increasing centralized power generators’ utilization rates and strengthening power utilities’ revenues. That said, smart meters and control of appliances could also increase system flexibility and therefore reduce SIC for renewables, offsetting the benefit to traditional generators by allowing renewables to capture greater market share.

Flexible-demand markets: the current state of play

There is around 4,000 GW of fossil fuel generation capacity worldwide, yet in 2016 there was only 56 GW of flexible demand. The latter is anticipated to expand to more than 300 GW by 2040.186 By that time, flexible demand could account for 7.5 per cent of traditional dispatchable generation, having grown at around 7 per cent per annum.

Large commercial applications of flexible demand are already in operation. In the UK, Flexitricity was one of the first providers of national demand-side balancing services, achieved via the aggregation of large commercial consumers. In the US, Zen Ecosystems recently launched Zen HQ, a product designed to target smaller businesses that typically have not participated in flexible-demand markets due to the three- to five-year payback periods on the investments required. Currently 20 per cent of the 5.5 million commercial buildings in the US are already on energy management systems. Zen Ecosystems hopes to integrate flexible demand into such systems to enable payback periods of 12 months or less.187

Across the seven major organized wholesale electricity markets of North America, wholesale flexible-demand capacity has averaged around 28 GW over the past three years. The Midcontinent Independent System Operator (MISO) accounts for 11.7 GW, or more than 40 per cent of this capacity. The total generation capacity of MISO is around 191 GW,188 or 18 per cent of US generation. Consequently, one of the largest North American electricity markets already has flexible demand capacity equivalent to 6 per cent of traditional generation capacity. Most of this flexible demand is from industrial and large commercial consumers.

Of the 1.2 GW of flexible demand included in the New York Independent System Operator (NYISO) capacity market, only 10 per cent originates from regulated utilities.189 This is likely to change following a recent FERC ruling that exempts flexible demand from the floor price.190 But the situation does illuminate a major barrier that traditional utilities face in participating in this flexible-demand market – nimble new market players are able to benefit from new revenue streams, while utilities are struggling to keep pace.

It is unclear how much flexible demand will compete with batteries to provide balancing services,191 or if the two will complement and support each other. Utility-scale battery projects are likely to be disadvantaged as demand flexibility increases; however, decentralized batteries could aid household participation in flexible-demand markets. Not only will the split between battery deployment at the utility level and household level determine the outcome, but so will the relative costs. Either way, as the flexibility of the system increases, the future is likely to bring greater market competition to the provision of balancing services.

With more system balancing on the demand side, the traditional role of power utilities in supplying electricity in response to uncontrolled but predictable demand will come under further threat. Traditional utilities are likely to experience increased competition for balancing services from batteries and interconnectors, and also as flexible demand gains market share in balancing markets. However, working with agile new market players could help traditional utilities to secure some of these additional revenue streams.

Importantly, while commercial and industrial flexible-demand markets are maturing, those for household electricity are yet to develop. Such markets, if successfully established, could offer utilities an opportunity to build on long-standing relationships with household consumers.

Smart meters – the entry point for smarter demand

At the heart of power demand digitalization is the smart meter. Automatic meter readings for large commercial consumers began in the 1980s. The transformation now under way is supported by the rapid deployment of smart meters featuring two-way communication (between the household and wider system), which enable time-varying pricing, monitoring and control of demand.192 The control of appliances afforded by smart meters could help utilities to avoid some traditional network investment, as peak demand and network congestion are lessened. The European Commission anticipates that smart meters may save European countries, on average, €60 per metering point over the lifetime of each smart meter.193 These savings could increase if SIC impacts and the benefits of flexibility are captured by cost–benefit analyses – an important next step given that almost all analyses fail to do this.

Smart metering represents both an opportunity and a threat for traditional utilities – utilization rates of generators may increase and the need for grid reinforcement may be avoided, but this could be offset by lower electricity demand growth.

As households and commercial consumers increasingly install smart appliances, smart meters could help to reduce aggregate demand by around 3 per cent.194 Hence, smart metering represents both an opportunity and a threat for traditional utilities – utilization rates of generators may increase and the need for grid reinforcement may be avoided, but this could be offset by lower electricity demand growth. Smart meters could also usher in new market entrants, such as those supplying technology and services for the IoT.

The biggest smart meter company by market share is Landis+Gyr, accounting for 26 per cent of global smart meter supply contracts (excluding China). Enel accounts for almost a quarter, giving the Italian utility giant a significant advantage in the digital transformation. Itron and Aclara, both based in the US, account for around 10 per cent each. Each company offers a different type of smart meter, some with greater functionality than others. All allow remote meter readings, but not all meters currently enable two-way communication or the connection of smart appliances.

Trust is key for widespread roll-out and optimized use of smart meters. A survey by Accenture found that 76 per cent of consumers did not trust their utility company.195 In the US, 43 per cent were ‘uneasy about smart meters in their homes if the information obtained could be used by utility companies to infer how many people live there and what they are doing at certain times of day’.196 These findings are somewhat contrary to market experience. At the end of 2015, 30 US electricity suppliers had deployed smart meters to all their residential customers;197 in the few US states that allow smart meter opt-outs, fewer than 1 per cent of customers chose to do so.198 As household flexible-demand markets expand, it is imperative that those households vulnerable to price rises are insulated from the high-cost periods associated with time-of-use tariffs.199

Box 10: The smart meter revolution by numbers

The US in 2016 had an estimated 70.8 million smart electricity meters, of which 88 per cent were installed for residential customers.200 At the end of 2016, there were 700 million gas and electricity smart meters installed globally. This global figure is expected to rise to nearly 800 million by 2020.201 In the EU28+2, 112 million smart electricity meters had been installed at the end of 2017, representing 40 per cent of all metering points.202 According to the terms of the EU’s Electricity Directive 2009/72/EC, EU member states are required to replace 80 per cent of meters with smart meters by 2020. The European Commission estimates that 72 per cent of households (200 million) will have smart electricity meters installed by 2020, a transformation that will require €45 billion of investment.203

Smart appliances, the Internet of Things and a world awash with data

Smart meters are increasingly able to control appliances and equipment within homes and businesses to help achieve demand-side flexibility. In the electricity sector, these products include everything from smart fridges, washing machines and phones to huge pieces of industrial equipment.

Around 20 billion internet-connected devices globally, across a diverse set of sectors, currently make up what is known as the Internet of Things (IoT).204 Although not all of these IoT devices are significant for the electricity system, the rapid expansion in sales of smart, internet-connected major domestic appliances (MDAs) marks a potentially consequential development. Excluding North America, global sales of these products more than doubled in the financial year ending March 2017, from 5.2 million in 2016 to 13.2 million.205

With more than 75 billion IoT devices expected to be connected to the internet by 2025,206 the volume of data processing required for new smart energy services will be vast. Cisco, a US network equipment maker, estimates that global IoT-generated data in 2020 will total 19,000 terabytes per second, 275 times greater than the amount of data sent from data centres to end-users or devices in that year.207

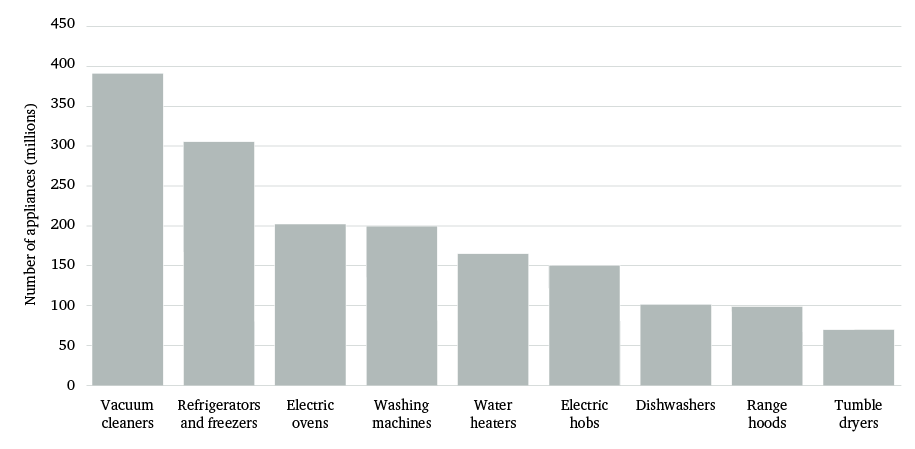

Yet even with today’s low levels of smart meter deployment, many traditional utilities are struggling to manage growing volumes of data.208 The UK’s 27 million households currently generate one meter reading per month, equivalent to 324 million meter readings per year. Once all households have a smart meter, with readings communicated every 15 minutes, 946 billion packets of data will be created each year. Once data sent from smart MDAs as well as smart meters are factored in, it is clear that the data processing required is likely to be beyond the current capabilities of traditional utilities. In 2015, there were 1.7 billion MDAs in Europe alone (see Figure 19). Although the vast majority of these were non-smart, the figure underlines the potential for growth in deployment in the future.

Figure 19: Installed stock of major domestic appliances (smart and non-smart) in Europe, 2015

Figure 19: Installed stock of major domestic appliances (smart and non-smart) in Europe, 2015

The question of who owns and has access to IoT data will also be increasingly important. In the US state of Illinois, for example, the regulatory authority recently granted approval for third-party companies to access the smart meter data of the state’s utility, Commonwealth Edison. For a fee of $900 per month, companies will be able to access anonymized consumption data, identified by zip code and customer segment. More granular locational information will be available for $145 per hour.209 The aim is to encourage and support smart home and IoT energy management innovations beyond those provided by the traditional utility. Eight US states, including New York and California, are conducting utility reform studies in order to encourage similar innovations in the smart home space.

Box 11: Layers of cybersecurity

Following reports of baby monitors being hacked in 2016,210 public attention is increasingly turning to the risks of cybersecurity around the so-called Internet of Things (IoT). Areas of concern include digitalized electricity infrastructure. Grid cybersecurity, in particular, is likely to become increasingly problematic as more access points emerge within the electricity system that hackers can exploit. In addition to IoT devices, the rapid rise of distributed energy resources is compounding the vulnerability of power grids to attack.

In December 2015, the Ukrainian grid was attacked, causing 225,000 consumers to lose power. Geopolitical tensions over the potential for state-sponsored cyberattacks, including on energy infrastructure, increased in January 2018 as the UK defence secretary claimed that Russia could cause ‘thousands of deaths’ by targeting UK energy infrastructure.211

Governments have begun to respond. US senators recently introduced a bill to ensure that imported products regularly receive security updates, have no known security vulnerabilities and have changeable passwords. In Australia, IoT products will soon be required to display a cybersecurity rating standard.212

The responsibility for ensuring grid cybersecurity stretches to the traditional utilities. The North American Electric Reliability Corporation (NERC) provides and enforces rules within the US and Canada that govern how power utilities and grid operators protect the grid. Compliance with NERC’s Critical Infrastructure Protection framework requires multi-factor user authentication and continuous monitoring of the grid for attacks. NERC also hosts regular simulation exercises.213 In Europe, equivalent standards and procedures are set out under the European Programme for Critical Infrastructure Protection.

The US National Institute of Standards and Technology recently provided updated non-mandatory guidelines for traditional utilities. The guidelines focus on the need to ‘collect and converge monitoring information’ by using commercially available products that improve the ‘situational awareness of security analysts in each silo’.214 Power utilities and grid operators are therefore being encouraged to integrate products from companies such as Cisco, Schneider, Sierra Nevada Corporation, VeriSign, Raytheon, ViaSat, Leidos, BAE Systems and IBM.215