3. The New Power Landscape

The previous chapter explored the technologies likely to shape the second phase of electricity sector transformations. This chapter explores the new actors and services emerging alongside these innovations, focusing on those actors and services that are shaping the digitalization of the sector. The chapter maps the ecosystem of technologies and new market actors, and discusses the new role of aggregators in managing the growing number of energy services and distributed energy resources (DERs). Utilities’ technical expertise will be critical to enable digital control of these DERs, such as EVs and household batteries. The chapter investigates the opportunity for utilities to leverage their expertise within this new power landscape, specifically in relation to energy service platforms. It also studies how blockchain technology could fundamentally reshape the way in which electricity and its associated services are paid for.

The chapter also considers some of the emerging regulations that aim to achieve a balance between ensuring innovation in energy service provision and redefining the role of utilities. Finally, the growing debate over ownership and market efficiency versus government intervention is set in the context of increasingly fragmented energy service provision.

The ecosystem of market actors providing flexibility

During the second phase of transformations, traditional utilities will need to respond to a multiplicity of challenges – many of which, if unaddressed, will further undermine their traditional business models. Peak demand could decrease as staggered smart EV charging, smart control of internet-connected appliances and the use of smart meters become more prevalent. On the one hand, this could bolster the business models of the power utilities, with EVs increasing electricity consumption and demand profiles flattening. The flip side of this argument, from the perspective of utilities’ profitability, is the prospect of greater competition from renewables, as flexibility increases. This scenario will be especially likely as lithium-ion battery storage technology reaches maturity, and as artificial intelligence manages grid congestion in increasingly smart ways.

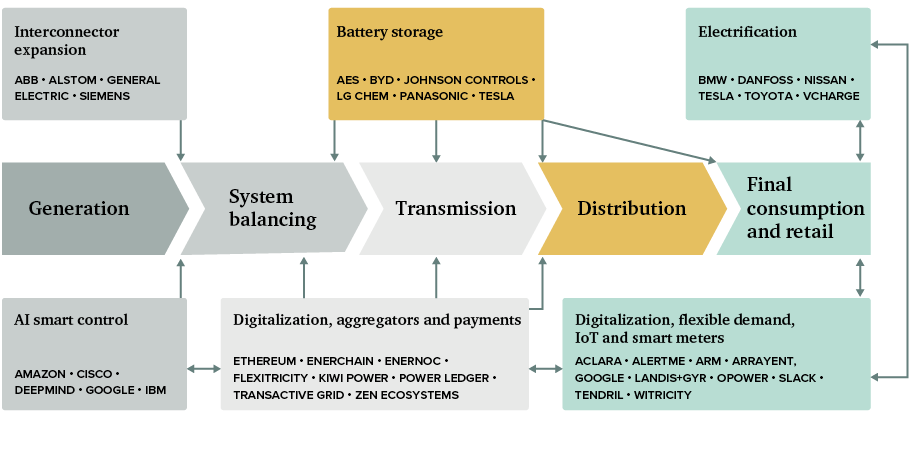

While many traditional utilities are seeking to rapidly reform their business models, the companies leading the second phase of transformations are often those new to the power sector. These challengers to incumbent players are creating services and business models that take advantage of the new technologies. The new companies vary considerably in size, ranging from small, innovative start-ups to some of the largest companies in the world – the latter including car manufacturers and internet firms benefiting from massive customer bases, strong brand recognition and, in many cases, signficant capital assets. These new market actors are encroaching on the business models of the established utilities, and reducing their generation revenues, customer bases and market control. Figure 20 shows how new technologies and associated companies are beginning to enter the electricity sector during this second phase of transformations.

Figure 20: The new market players in the electricity sector, under each aspect of the second phase of transformations

Figure 20: The new market players in the electricity sector, under each aspect of the second phase of transformations

Energy service provision by new market facilitators

Traditional utilities already face a vast number of new competitors (or potential competitors) in flexible-demand markets. Google and Amazon, for example, are in talks with regulators to introduce time-of-use tariffs to enable flexible demand.216 In order to keep pace, utilities are acquiring and investing in start-ups – for instance, the UK’s Centrica paid £65 million in 2015 for AlertMe, a home energy management system that enables communication between a central control hub and wirelessly connected devices and appliances. A contrasting example is the case of Tendril, a US company that has remained private and has attracted nearly $150 million in investment, principally from Siemens, GE and ENGIE. Tendril provides ‘home energy reports that [combine] behavioral science and physics-based home simulation to give customers actionable data on how they use energy’.217 Potentially one of the biggest market disrupters of the future is Opower, which was acquired by Oracle in 2016 for $532 million.218 Opower already provides services to 100 traditional utilities globally, such as Pacific Gas & Electric (PG&E), Exelon and National Grid, helping them to deliver digital services to consumers by analysing more than 600 billion meter reads from 60 million end-users.219

As regards capacity markets, traditional utilities are failing to win flexible-demand contracts. In December 2016, the Ontario Independent Electricity System Operator held its second flexible-demand capacity auction. As with many similar auctions across various jurisdictions, new players won the tenders, leaving traditional utilities struggling to participate. EnerNOC and Enershift won the largest contracts.220 Both companies are what are termed ‘aggregators’ – new and necessary market players in flexible-demand provision. The ability of these new players to capture market share was demonstrated in June 2017, when Enel Green Power North America (a subsidiary of Italy’s Enel) acquired EnerNOC to enter the flexible-demand market.

Box 12: Aggregators – the new intermediaries

Aggregators enable the intelligent control of millions of devices connected to the Internet of Things (IoT) and to smart meters. This is a critical role given the huge potential of the flexible-demand sector. Without aggregators, the volume of data and complexity of the system would be unmanageable for system operators.

Another dimension to this complexity comes from consumers. As more distributed energy resources (DERs) such as solar photovoltaics (PV), batteries, smart meters, IoT-connected devices, smart electric vehicle (EV) charging facilities and even vehicle-to-grid EVs are adopted, a growing number of electricity consumers could become ‘prosumers’, selling power and flexibility services back to the grid in an intelligent manner. But these potential prosumers are currently locked out of the market. Having millions of flexible-demand households communicating simultaneously with the wider system is technically challenging due to the volume of data that require processing in real time.221 This is where aggregators such as VCharge, a US firm recently acquired by Ovo Energy of the UK, come in, acting as intermediaries between electricity end-users and DER owners on one side and power system participants on the other.222

VCharge’s business model revolves around the aggregation of small distributed demand, in the form of residential electric heating, and the selling of balancing services. VCharge is looking to expand flexible balancing services to battery dispatch and EV charging. Ovo now offers a reduced residential tariff to EV owners.223 With National Grid forecasting the need for 2 GW of flexible demand in 2020 in the UK, this type of bundled tariff offering could become more commonplace. EVs are also stimulating the creation of new tariffs in the US, with 25 electricity suppliers now offering bespoke EV tariffs that are up to 95 per cent cheaper at night.224

As the 2016 Ontario Independent Electricity System Operator capacity market auction showed, aggregators are nimble new market entrants. While current flexible-demand markets and their associated aggregators are engaged with non-domestic consumers, the business model of VCharge points to a looming transformation. By aggregating many small-scale DERs that would otherwise struggle to enter the market, aggregators working within the domestic market could begin to buy and sell flexibility services.

In the UK, two traditional utilities, E.ON and EDF, won 14 per cent of the contracts in last year’s £14 million capacity market auction, which concluded on 22 March 2017. The biggest share (47 per cent) went to non-domestic aggregator companies EnerNOC and Kiwi Power. Smaller aggregators and large industrial entities such as Tata Steel won the remaining contracts.225 In California, Pacific Gas & Electric anticipated losing 7.3 per cent of demand to community-owned aggregators during 2017 alone, and 21 per cent by 2020.226 These aggregators buy power from the power utilities on behalf of their members, enabling them to negotiate better rates. Since early 2017, half of the 58 counties of California, and 300 cities, had a dedicated community aggregator.227

As the number of domestic DERs grows, the influence and transformational impact of flexible demand on the business models of traditional utilities will grow too. As the results of the capacity market auctions indicate, the traditional utilities appear to be lagging behind non-domestic aggregators.

However, as smart metering and the IoT start to enable greater volumes of flexible demand, the household flexible-demand market will present a new opportunity for traditional utilities. In a world awash with data, and with the ability to control appliances in functionally smarter modes, utilities could offer more comprehensive service-based packages to households, creating new value in a system where traditional business models are becoming obsolete.

New transactions, blockchain and peer-to-peer electricity trading

Certain traditional utilities are transforming payments and tariffs to capture the benefits of flexibility on the demand side. The big three Californian utilities – San Diego Gas & Electric (SDG&E), PG&E and Southern California Edison (SCE) – are in the process of finalizing time-of-use tariff structures before they switch the majority of customers to such pricing in 2019.228 In the UK, similar transformations are under way, for instance in Ovo’s new tariff offering (see Box 12). Green Energy UK offered the first time-of-use tariff in January 2017.229

The growing numbers of DERs and aggregators, meanwhile, are providing opportunities for new payment and transaction methods to emerge – methods that could prove to be even more disruptive to utilities than the rise of renewables and low growth in demand, in the sense that more players and competition will enter the market. One of these potentially disruptive trends is the rise of peer-to-peer transactions, facilitated by blockchain technology, which could partially replace the role of the electricity supplier as broker between producer and consumer.

As a secure system for payments and transactions, blockchain is potentially disruptive for electricity trading. It could enable peer-to-peer transactions in which trusted intermediaries such as banks or traditional utilities are partially displaced or no longer needed.230 Blockchain consists of a distributed list of data records, called blocks, that continually grows. Blocks are verified by a distributed network of encrypted computers. To modify a previously verified block, each node on the network needs to be simultaneously modified, as each node is continuously verifying the others.

Ethereum is a blockchain protocol that offers greater functionality and speed than previous protocols, such as Bitcoin. This new functionality includes smart contracts to facilitate and administer contracts between peers.231 Blockchain applications are beginning to emerge within the energy sector. These applications broadly fall within three categories:232

- Facilitation of energy bill payments – in this application, the utility still plays the central role of structuring the tariff and receiving payment.

- Handling of transactions for energy generation when the physical location of the generator is known. With this type of transaction, blockchain enables a household with a DER to sell power to a neighbour, potentially without the need for a utility. However, this requires smart-contract functionality.

- Incorporation of big data and predictive task automation within the blockchain, enabling flexible balancing services.

An example of the first application is BlockCharge,233 a joint project between Slock.it and the German utility Innogy. By incorporating a ‘smart plug’ with the Ethereum protocol, BlockCharge aims to provide universal charging of EVs from any public charging point, negotiating the charging price and facilitating the payment process. Europe’s biggest utilities are also trialling blockchain EV charging using a protocol called Enerchain.234 In other developments, pilot projects are under way in which DERs sell power directly to consumers, via peer-to-peer payments facilitated by Ethereum smart contracts, without the need for a utility as an intermediary. Predictive task automation also remains an area of development for blockchain protocols, and could enable greater penetrations of renewables in the future power system.

At the more disruptive end of the spectrum of blockchain applications, where peer-to-peer transactions are facilitated without the need for the utility, is TransActive Grid. In 2016, the US company connected five prosumer homes (in this case, homes that were fitted with solar PV installations) to five consumer households, enabling the latter to buy excess power from the former.235 The homes were connected to a microgrid, so power was not transferred via a utility-owned grid. A similar pilot scheme, called Power Ledger, is happening in Perth, Australia. Such new modes of payment could lead to households partially migrating away from the retail electricity market and instead sourcing power from prosumers.

Although blockchain can facilitate payments for electricity between peers, electricity must still be physically transferred along distribution networks. This poses regulatory and pricing barriers. Regulations will need to be updated for peer-to-peer power transactions. The traditional utilities that own the grid infrastructure will need to ensure payments for their services are captured in the transactions.236 However, proposals are being developed in which aggregators’ services and blockchain peer-to-peer transactions are merged, so that the aggregator acts in effect as the regulatory buffer for the prosumer, with households paying a retail tariff alongside any peer-to-peer payments they make via blockchain.237

If blockchain is to become significantly disruptive, the regulations governing the transmission of power on grids will need to adapt to allow prosumers to sell DERs directly across the grid. Currently regulations prohibit this. If peer-to-peer transactions of this nature were to become a significant component of the electricity market, utilities would lose their ability to capture value in the exchange between generator and consumer. However, grid utilities would still be in a position to charge for infrastructure costs within peer-to-peer transactions. These transformations are only just emerging, but unbundled utilities will need to adapt to market innovations given the fundamental shift that could ensue.

Transforming traditional utilities’ role and business models

Traditional utilities are entering the digital space primarily in order to optimize their existing capital-intensive infrastructure. Since 2010, investment in grid infrastructure by unbundled utilities has remained stagnant at $100 billion per annum. In contrast, their expenditure on digital infrastructure grew by 20 per cent in 2016 alone.238

On the one hand, the emergent digital, flexible smart grid could benefit traditional utilities, as the need to invest in existing, capital-intensive infrastructure may be partially mitigated by digitalized infrastructure. On the other hand, traditional utilities may lose market share as emerging players begin to offer new services to consumers, or even as prosumers begin to use DERs. During the first phase of the sector’s transformations, liberalization and competition opened many retail markets to new players. Service-oriented offerings from new market actors are, however, likely to be far more disruptive. The emergent EV charging tariff is leading the way in terms of offering specific tariffs for specific services – in this case, time-of-day-based charging of EVs. With Google and Amazon backing flexible-demand tariffs, there is the prospect of many more households being offered the service of having appliances controlled remotely, by algorithms in the cloud, perhaps in combination with one of the many new green tariffs now on offer.

It is clear that a new business model is emerging, one that provides energy service platforms for DER-owning prosumers. These platforms consist of networks that connect multiple producers and consumers, providing tools, services and rules to enable participants’ interaction and hence the creation of new marketplaces. Online services in other sectors, such as Uber (transport), Airbnb (lodging) and eBay (online marketplace) exemplify such platform businesses. With the aggregation of the various forms of DERs within marketplace platforms, it is possible to envisage the development of a growing array of new services and packages that are tailored for the owners of DERs. The CEO of Commonwealth Edison, a US utility, has publicly stated her desire to transform the business by shifting from a utility business model to an energy platform model.239

The services offered on these platforms might also include the prosumer model of households being able to choose locally produced solar PV power. These platforms could also help DER owners comply with regulations (which currently inhibit households selling power directly to the grid), perhaps even using blockchain-based smart-contract protocols for transactions. Platforms would derive their revenues from a range of business models, including traditional consumer or supplier charges, transaction fees, advertising and premiums.

Such platforms already exist within the electricity system. Non-domestic flexible-demand aggregators are prime examples. Kiwi Power, EnerNOC and Flexitricity are aggregator platforms to which commercial and industrial electricity consumers grant third-party control of their systems in order to participate in flexible-demand markets. Many existing electricity suppliers are in a prime position to use their established relationships with households – such as in the setting of retail tariffs – to create some of the first energy service platforms.

Across jurisdictions, transmission and distribution networks are currently operated by various entities. The distribution networks tend to be operated by so-called distribution network operators (DNOs), which themselves are often subsidiaries of unbundled utilities. Traditional utilities therefore have valuable experience in distribution network operation and maintenance.

Importantly, for those traditional utilities that currently operate distribution networks, energy service platforms are likely to require the formation of what have been termed ‘distribution system platforms’ (DSPs) or ‘distribution system operators’ (DSOs).240 The difference between DNOs and DSOs is subtle but important. DNOs are responsible for overseeing connection of DERs, but they generally do not oversee or facilitate dispatch and coordination.

To ensure the ability of DSOs to create efficient and fair markets, new regulations and accountability to an independent regulator will be needed, perhaps requiring an independent or even not-for-profit DSO.

Many conceive of future DSOs as facilitating platforms that will provide such coordination services;241 the DSO backbone would be essential to enable competition between various platforms within one distribution network, while maintaining interoperability. One utility might form the DSO, enabling regulated utilities as well as independent and unregulated energy service platform providers to meet the service needs of electricity consumers and prosumers. The DSO would also need to provide open and transparent system access, and operate market mechanisms developed by the platforms, alongside performing the essential duties of maintaining system safety and reliability, currently undertaken by the DNO.242

The model of multiple and competing energy service platform providers, facilitated by the DSO platform, is not dissimilar to that of telecommunication networks. For instance, in the UK, Openreach – a subsidiary of BT – operates the fibre-optic cables that are the backbone of the system. On top of this platform, BT and other internet and communication providers and their various platforms compete to offer services to consumers. To ensure the ability of DSOs to create efficient and fair markets, new regulations and accountability to an independent regulator will be needed, perhaps requiring an independent or even not-for-profit DSO.243

Pilot projects such as Australia’s Decentralized Energy Exchange (deX) offer insights into how an energy service model enabled by platforms and DSOs might function.244 Sponsored by the Australian Renewable Energy Agency (ARENA), deX attempts to bring together DERs in a competitive market structure. DSO-type functionality is provided by GreenSync software in collaboration with network operators United Energy and ActewAGL. Bids and offers from multiple DERs are aggregated from solar PV, batteries and flexible demand within individual deX households, to provide the DNO with the least-cost balancing mechanisms it requires. In essence, the GreenSync software provides the DNO with the same software functionality that a full DSO would provide. As such, the pilot project is a step along the path towards a DSO model that enables a platform marketplace of services.245 The GreenSync system also allows transactions to be effected via digital wallets, an arrangement one step away from blockchain peer-to-peer payments.

Modern economies are built on a series of interacting platforms, the most successful of which tend to enable the greatest number of participants to compete in a given marketplace. In many regards electricity grids are natural infrastructural platforms, enabling traditional utilities to compete within the grid platform. The rise of a variety of small-scale flexible DERs within the distribution grid, enabled by digitalization, is creating the need for a new layer of energy platform business models and service offerings that extend to the prosumer. To take advantage of the opportunities this presents, traditional utilities will need to reconceive their role still further, moving away from business models based around ownership of capital-intensive generation infrastructure. Thus, rather than using digital infrastructure to optimize their existing asset bases, they will need to build entirely new infrastructure-light business models, platforms and services.

Regulating transformations

Digital infrastructure and technologies that increase the flexibility of the electricity system are currently disadvantaged, compared to traditional generators and network infrastructure, when it comes to financial valuations. Currently, electricity prices do not fully capture the spatial and temporal differences between supply and demand. Consequently, demand flexibility, location-specific congestion management and the ability to install batteries in a modular, distributed manner are not appropriately valued in the market.

Reforms of electricity markets are required to create efficient market signals for these new forms of smart flexibility and congestion management, as well as for DERs. Locational marginal pricing – in which electricity prices reflect the physical limits of the network as well as the difference in value between locations – offers a potential alternative to reduce network congestion, although it is politically unpopular as it can cause electricity costs to rise in areas of high demand. Equally, scaling up transmission investment to enable greater flows of renewable power from regions of high supply to regions of high demand is costly. The European Commission’s clean energy package of 2016 attempts to ensure that network operators are rewarded based on investments (such as in digital infrastructure) that minimize the need for capital-intensive projects, as costs are passed on to consumers via tariffs.

In the UK in 2017, the Energy Networks Association began the Open Networks Project, aimed at exploring the transformation of DNOs into DSOs, supporting flexibility and providing platforms for new markets and services for customers. The UK regulator, government and nine DNOs are participating in the project.

New York’s Reforming the Energy Vision (REV) is perhaps the most all-encompassing set of reforms to attempt to move traditional utilities from a cost-of-service business model to a ‘service platform’ model in which providers create marketplaces, sell system data, charge transaction fees and create flexibility. REV differs from reforms in other US states. For instance, California has set specific targets, such as for storage and EVs, whereas REV has taken a system-wide approach that targets the transformation of the actors underpinning and operating the electricity system itself.

REV provides for incumbent utilities to continue as distributors of energy even as they become marketplace operators. The DNOs themselves become DSPs – that is, providing the platform between suppliers and consumers of energy. REV reforms recognize that ‘macrogrid’ entities serve a public good in decentralizing the energy system.246 Since its formation in 2014, REV has stimulated innovation and experimentation. Not all projects have been successful. ConEdison began implementing a ‘virtual power plant’, consisting of 300 households, that was supposed to integrate DERs such as solar PV and storage. But the project ran into difficulties and was suspended in April 2017.247 Of 17 REV projects, five principally involve utilities creating market and service platforms. Central Hudson Gas & Electric’s CenHub Marketplace also integrates product and service offerings with advice to households on consumption patterns.248 Meanwhile, Connected Homes, by ConEdison in partnership with Opower, attracted almost 129,000 unique visitors to its marketplace platform in the third quarter of 2017.249

REV’s aim of integrating more DERs presents increased cybersecurity challenges. If thousands of small DERs communicate via the internet with a DSO, this increases the number of connections vulnerable to cyberattack. REV and its associated DSPs recognize the need to strengthen protocols to prevent such attacks; the DSPs are responsible for ensuring that the DERs communicating with their platforms are safe.250

Box 13: Government engagement and ownership

The trend in the power sector over the past decade has been one of liberalization and privatization, albeit implemented to various degrees in different parts of the world. This trend, along with the establishment of independent regulators, has led to shrinking state involvement in the power sector, particularly as governments have relied on the market to deliver national policy objectives concerning power supply.

However, a significant proportion of global power generation remains in full or partial public ownership. In the US, 48 million citizens get their electricity from public-sector companies. In the EU, many of the largest power generation companies, including EDF (France), Vattenfall (Sweden), Enel (Italy) and RWE (Germany), are fully or partially owned by national or regional governments. Many of the power giants in Asia similarly are under partial or total government ownership; these firms include KEPCO (South Korea) and most of the conventional Chinese generators.

In some countries, the number of power companies in public ownership is increasing. For instance, in Germany the number of municipally owned power companies has increased over the past decade.251 Globally, there is a mix of public and private ownership of networks – the Chinese State Grid remains state-owned and, as of 2018, is the second-largest company in the world by revenue, behind Walmart.252 In the UK, National Grid is run as a private company operating the gas and electricity transmission networks; it also has significant operations in North America.

As demonstrated by the 2015 Paris Agreement on climate change, there is political acceptance at national and international levels of the need for rapid and near-total decarbonization if the most serious consequences of climate change are to be avoided. However, this commitment needs to be backed up by strong policy interventions. In market-based systems, an array of mechanisms have been used to try to stimulate or discourage certain technologies – for example, feed-in tariffs have been introduced in an effort to stimulate low-carbon renewables, while emissions performance standards have sought to discourage high-emission generators. However, market interventions, especially when required to deliver rapid change, can have unintended consequences for other market actors, potentially necessitating government intervention in other areas. This can sometimes conflict with policy objectives. For example, capacity mechanisms, with their associated financial assistance, in the UK are given to fossil fuel generators, including coal plants, to help ensure security of supply, even though clear targets exist to reduce the use of carbon in the sector.

This has already raised questions about the efficiency and ability of the electricity market to deliver decarbonization.253 As greater flexibility is introduced into the system, it is likely that where market systems dominate, they will fragment further, possibly requiring a further suite of government market support mechanisms. This may reduce market efficiency to such an extent that direct or indirect government ownership of the grids would be economically more beneficial.254

As EV deployment rates accelerate and battery costs fall, flexibility is likely to increase, enabling greater penetration of renewables while avoiding increased SIC. This will herald the entrance into the electricity sector of a new wave of market players that are likely to use innovative technologies to offer new services to consumers. It is, however, the broader set of digitalization technologies that may truly revolutionize flexibility.

Among various aspects of digitalization occurring in the sector, those likely to prove the most disruptive for the traditional utilities are applications of flexible digitalization that create new services and fragment old ones. These new services range from creating the means to aggregate household consumption and open up residential flexible-demand markets to creating new modes of transactions and connecting millions of DERs to platforms of interacting prosumers. The power landscape will undoubtedly shift. The traditional utilities will need to ensure that they capitalize on the opportunities these new technologies bring, by developing new energy services to prevent further erosion and fragmentation of their business models.