The direction and pace of growth in the meat analogue industry will depend upon numerous factors affecting prospects both for commercially viable production systems at scale and for acceptance and demand among target consumer segments. Despite increasing consumer awareness of the environmental and animal welfare impacts of eating meat and the growing market for reduced-meat diets, the degree of consumer acceptance of meat analogues is uncertain, as is the likely level of support from Europe’s civil society groups. The role of the incumbent industry in supporting or hindering the growth of meat analogues is also unclear: while some major players in the meat industry are investing in meat analogue innovations themselves, others are actively resisting the up-swell of start-ups marketing their products as meat substitutes.

This chapter explores the ways in which consumer perceptions, civil society and incumbent industry responses, technical challenges and meat consumption trends may influence the growth of the meat analogue industry in the EU before considering, in Chapter 4, the complexities of the regulatory questions to which meat analogues give rise.

Consumer perceptions of meat analogues

Producers of meat analogues actively target their products at meat-eaters. They have aligned their marketing with that of conventional meat products – emphasizing the taste and experience of eating meat through carefully chosen language and imagery – while innovators in cultured-meat products emphasize their ability to deliver meat ‘as we know it’, without the negative environmental and welfare impacts. The mission statement of San Francisco-based Memphis Meat encapsulates this concept, with the slogan ‘Better meat, better world’. Deep-set personal preferences for meat in Europe are nevertheless expected to present a significant obstacle to generating widespread demand for plant-based ‘meat’ and cultured meat. A number of studies undertaken into consumer attitudes to meat analogues specifically, and plant-based diets more generally, indicate that those already seeking to reduce their meat consumption are the most likely to purchase plant-based meat alternatives, while so-called ‘meat-believers’ – those who regularly consume meat and who do not display any active intention of shifting their diets – are less likely to be tempted by new meat substitute options.

Those already seeking to reduce their meat consumption are the most likely to purchase plant-based meat alternatives, while so-called ‘meat-believers’ are less likely to be tempted by new meat substitute options.

Familiarity, sensory attractiveness and the prevalence of food ‘neophobia’ are all likely to play a role in strengthening or dampening public interest, particularly among meat-eaters at whom novel meat analogues are aimed. The cultivation of recognizable whole cuts of meat – as opposed to muscle cells that can be used in minced-meat products (sausages, burgers, etc.) – in a way that is economically viable at scale remains a long-term goal. The technological process involved in producing a steak in vitro, for example, requires culturing a more complex tissue, including multiple cell types, and considerable progress is needed to achieve a steak or similar whole-cut of meat that achieves the colour, flavour and nutritional profile of meat harvested from an animal – and to do so in a manner that is economically viable is even more challenging, and therefore significantly further from market. Even with further technical breakthroughs, consumer concerns over the ‘naturalness’ of cultured meat are expected to be a major obstacle to the future widespread adoption of cultured-meat products. Early research indicates that cultured meat can evoke feelings of disgust and strangeness – often referred to as the ‘yuck’ factor – and that many consumers may view in vitro products as ‘freakish’.

The (perceived) nutritional quality of meat analogues and their safety compared with conventional meat is also likely to be an important factor in their uptake. Relative to the conventional processed meat products that they are intended to replace (including burgers, sausages, nuggets, and so on), plant-based ‘meat’ products tend to contain lower levels of saturated fat, cholesterol and calories, and often contain higher levels of micronutrients such as zinc, iron and calcium. Beyond Meat and Impossible Foods both report that their burgers have a protein content comparable to that of an average conventional beef burger. Some studies have nevertheless demonstrated that individuals are worried about the production process and ingredients involved in manufacturing – for instance, over processing and high use of salt and genetically modified organisms (GMOs) – while others perceive meat analogues to be lacking nutritionally as compared with conventional meat.

In the case of cultured meat, the controlled conditions for production raise the possibility of meat that is free from food-borne disease and that is at low risk of contamination. Furthermore, tightly controlled production procedures obviate the need for antibiotics while creating new opportunities for the addition of desirable vitamins and the reduction of fat and fatty acid content. Perceptions of the health impacts of consuming cultured meat vary considerably, in part due to a high degree of uncertainty among the public surrounding both the relevant technology and the production processes. While studies have indicated that some consumers acknowledge the potential health benefits and increased food safety of cultured meat compared with conventional meat, others argue that there persist several ‘unknowns’ about the long-term side-effects of eating cultured meat. Such arguments place particular emphasis on the risks of developing cancer and of catching food-borne diseases such as zoonoses (infectious diseases that are transmitted naturally between animals and humans). Another study demonstrated that those individuals with a greater degree of concern for the environmental impacts of meat consumption were more likely to express an interest in eating cultured meat.

Support among environmental and animal welfare groups

Public attitudes to meat analogues, and particularly to cultured meat, will be shaped to a significant degree by civil society narratives. Civil society has played an important role in raising awareness among citizens about the impacts of their diets, and environmental groups in particular are deemed one of the most helpful sources of public information in Europe relating to meat consumption and the climate. The growing number of meat reduction campaigns, such as ‘Meat Free Monday’ and ‘Veganuary’, among others, have also been influential in raising awareness of the benefits of eating less meat and fostering the consumption of more plant-based meat alternatives. Yet past experience of civil society-led public discourse on GMOs in Europe, and its influence on low public acceptance of GM technologies in the EU, is indicative of the power of NGOs to shape both public opinion and public policy and regulatory responses.

Plant-based ‘meat’ and cultured meat present a dilemma to NGOs advocating a shift in meat-eating habits. For the most part, NGOs active on this issue promote messages of step-wise changes in diets, encouraging a flexitarian lifestyle and/or the substitution of ruminant meat (beef, lamb) for monogastric meat (chicken, pork). Few organizations – principally those concerned with animal welfare – are openly supportive of a shift to meat-free diets. Most NGOs, in shaping their campaigns around meat consumption, aim for moderate messaging that is accessible and appealing to mainstream audiences, and that avoid creating a perception of the organization as radical in its mission. Manufacturers and marketers of meat analogues are, in their own way, promoting a shift away from conventional meat but the means of their production and the way in which they are marketed raise certain questions for environmental and animal welfare groups (see below). In addition, there are concerns that the promotion of cultured meat may yield an ‘addition effect’ (also known as the ‘Jevons Paradox’) in which these new products do not replace conventional meat but instead contribute to even higher levels of total meat consumption (cultured and conventional combined).

Early assessments indicate that meat analogue production is significantly less resource-intensive than conventional meat production: based on current projections, a 50 per cent replacement of meat products by cultured meat, imitation meat (plant-based ‘meat’) and insects could be expected to yield a 38 per cent reduction in agricultural land demand. In the case of cultured meat, the concentration of resources on producing only muscle tissue that will be eaten – and therefore avoiding the energy-, resource- and time-intensive production of waste or by-products – is one of its most important attributes, according to advocates. Life-cycle assessments (LCAs) of the most well-known plant-based meat analogues indicate that plant-based ‘meat’ is, on the whole, significantly less emissions-intensive than conventional meat. The relative environmental impact of cultured-meat production compared with conventional-meat production is more uncertain. Cultured-meat production is expected to be less land- and energy-intensive than beef production, however, land requirements are anticipated to be similar to those of poultry production while direct energy inputs will be significantly higher.

Until such time as cultured meat is being produced at scale in industrial bioreactors it is not possible to assess fully the resource intensity of production.

LCAs of cultured meat at this stage are, however, highly speculative and are based on modelled rather than actual production methods. Until such time as cultured meat is being produced at scale in industrial bioreactors – at which point it may be assumed that cultured meat will have been approved under EU regulation and investments will have been made in the necessary infrastructure – it is not possible to assess fully the resource intensity of production. In addition, while assessments of actual production methods are possible with plant-based ‘meat’, producers have retained a degree of secrecy around the ingredients and techniques that achieve their unique degree of mimicry, meaning that the precise resource intensity of their production – embedded land use, for example – remains uncertain.

The ‘clean’ nature of meat analogues has also been questioned by civil society in response to the use of GMOs in certain plant-based ‘meat’ products and cultured-meat processes. In the US, civil society groups – including Friends of the Earth, ETC Group and PETA – have voiced concerns over the use of genetic engineering processes in the creation of the Impossible Burger and in certain cultured-meat production methods, and over the degree of processing involved in producing both plant-based ‘meat’ and cultured-meat products.

Among the animal welfare and animal rights communities, the prospect of ‘slaughter-free’ meat has garnered considerable support for the nascent cultured-meat industry: in 2008, the US-based animal welfare NGO People for the Ethical Treatment of Animals (PETA) announced a $1 million prize for the first research team to produce commercially viable in vitro chicken cells; more recently, in early 2018 Humane Society International/India launched a partnership with India’s Centre for Cellular and Molecular Biology to encourage both an expansion in production and a growth in demand for cultured meat in India; and other organizations, including Compassion in World Farming and Mercy for Animals, have publicly voiced their support for the scaling-up of cultured-meat production and consumption as a means of reducing the number of animals slaughtered each year for meat (estimated at 7.5 billion animals each year in the EU, and 9.1 billion in the US). The two longest-standing cultured-meat companies in Europe, Mosa Meat and Cellular Agriculture Ltd., currently harvest cells at the point of slaughter, however, and so are not ‘slaughter-free’. The continued use of foetal bovine serum (FBS) by many of the major cultured-meat companies is also likely to present a barrier to generating support among the animal welfare community, owing to the effects on the calf foetus in the process of its extraction, although serum-free media are already in use or in development by others in the sector.

Economics of production

Currently, cultured-meat production is highly labour intensive. In shifting from the laboratory to industrial-scale bioreactors, cultured-meat producers should be able to achieve economies of scale, but tissue engineering to this extent is both unprecedented and unproven. The price of production will need to fall dramatically if the end product is to be affordable and appealing for consumers: the start-up Aleph Farms recently announced it had been successful in producing a small strip of beef steak for $50 – compared with the $330,000 it cost to produce the first cultured-meat burger in 2013 – while cultured minced meat also remains costly to produce at $11 per hamburger. Technical breakthroughs will be needed before prices drop further: today, 80 per cent of the costs of the final product result from the need for expensive growth factor proteins. Scale-up would also require associated investments in infrastructure and logistics, the cost and resource efficiency of which have yet to be examined. Sector stakeholders anticipate that it will be between five and 10 years before industrial-scale cultured-meat production is possible.

Industrial-scale production of plant-based ‘meat’ and cultured meat could bring fundamental changes to today’s food system. Growth in demand for plant-based ‘meat’ will generate greater demand for plant protein crops such as pea and wheat, creating an incentive for some livestock producers to transition away from industrial animal farming. While new jobs would be created with the scaling up of cultured-meat production, they would likely be far fewer in number with much of the production process automated, and those that are created may be located in the industrial heartlands of Europe rather than in its agricultural regions. Power balances among industry players may see less change, however: while it is predominantly start-up companies and universities leading innovation in the meat analogue industry, several major agribusinesses are moving to buy stakes in the ‘disruptor’ companies and to invest in in-house innovation in plant-based ‘meat’ and cultured meat.

Responses from industry incumbents

As in many sectors of the economy, incumbent meat industry has an important role to play in either accelerating or dampening innovation, depending on whether it views that innovation as a risk or opportunity. Lessons from other sectors, including the energy and utilities sectors, show that the response of industry incumbents to innovation can influence to a large extent its nature and success, particularly when market power is concentrated (as it is in the food sector) and when those incumbents take active steps to influence laws, regulations and public discourse.

On the one hand, the rise of plant-based ‘meat’ and cultured meat poses a risk to conventional meat producers, and to processors, marketers and logistics operators along the supply chain: increased demand could prompt a shift among consumers away from conventional meat and could either incentivize more localized meat production or relocate production, all with potentially adverse implications for meat industry incumbents. On the other hand, meat analogues offer an opportunity for businesses in the meat industry to diversify their offering and spread their risk: early investment in meat analogue start-ups and in research and development (R&D) for proprietary meat alternatives could offer a means of hedging against future demand shifts. In 2016, a coalition of institutional investors, with assets worth a collective $5.3 trillion, called on meat companies to diversify the protein products they sell and invest in plant-based alternatives, outlining the multiple and growing investment risks associated with factory farming. Analysts have also noted the relatively stable prices of meat alternatives compared with conventional meat, as they are less reliant on seasonal supply fluctuations and offer opportunities for (potentially) longer shelf-life and easier storage.

Major players in the meat and food industries have already invested in plant-based ‘meat’ and cultured-meat start-ups – including Tyson Foods (with investments in Memphis Meats, Beyond Meat), Cargill (with investments in Memphis Meats), PHW (with investments in SuperMeat), Unilever (with investments in the Plant Meat Matters consortium and Vegetarian Butcher) and Jan Zandbergen (the company recently signed a distribution agreement with Moving Mountains) – though their investments remain small as a share of their overall R&D activities. Others in the industry have

taken a more defensive approach to the rising number of meat analogue companies: some industry incumbents in the US have lobbied for a clarification of legal definitions of meat and for more stringent regulation of meat-alternative labelling.

Meat consumption trends

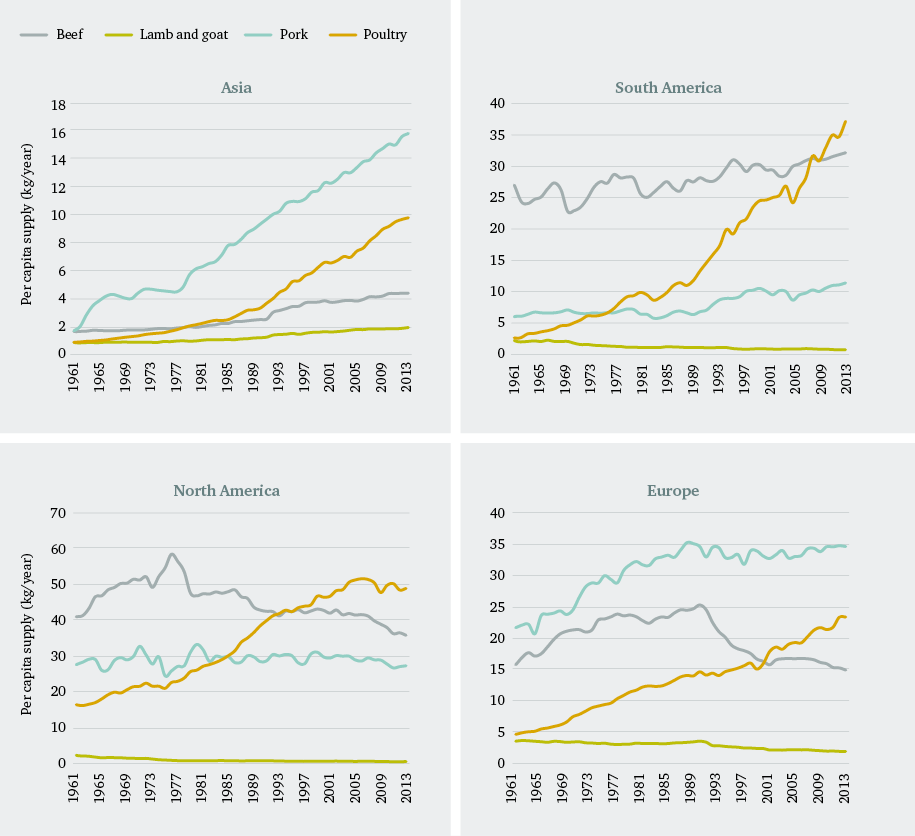

Another likely factor in determining the scale of the future meat analogue industry lies in current trends in meat consumption, not only in Europe but globally. Since the 1960s, global patterns of meat consumption have shifted significantly. Worldwide demand for meat has steadily increased over this period, a trend that is expected to continue: the International Panel on Climate Change (IPCC) stated in a 2018 report that in the absence of proactive policy interventions to reduce meat consumption, ‘prevailing trends are for increasing rather than decreasing demand for livestock products at the global level’. This growth in overall consumption has been driven primarily by a rapid surge in consumption of poultry – the average per capita intake of which increased more than fourfold between 1961 and 2013 – with consumption of pork also showing a strong upward trend. By contrast, per capita consumption of meat from ruminants such as cattle, sheep and goats, plateaued over the same period.

Worldwide demand for meat has steadily increased since the 1960s, a trend that is expected to continue.

Change over this period has looked very different from region to region. In Asia, per capita meat consumption grew significantly, driven principally by a surge in demand for pork and poultry. In South America, overall consumption has risen modestly but there has been a dramatic shift in demand from beef to poultry. In Europe and North America, poultry also took a growing share of total per capita meat consumption by the end of the 1961–2013 period, with a marked downturn in overall consumption occurring in North America from 2007 onwards (see Figure 2).

Total demand for meat in Europe has not dramatically changed in recent years although there has been a discernible shift away from the more resource-intensive ruminant meats (beef and lamb) and towards less resource-intensive monogastric meats (poultry and pork). In light of the reluctance of meat-eaters to shift to meat analogues, widespread growth in demand for plant-based ‘meat’ and cultured meat among target audiences may depend on a broader shift in social and cultural norms towards acceptance of flexitarian lifestyles and towards a food environment in which plant-based options are both more visible and more appealing. For those EU companies looking to export their products, booming markets in South America and Asia present a promising opportunity, with growth in total consumption expected to remain strong and, in some countries (China and Singapore, for example), growth in the meat analogue industry is already underway. An increasing preference for poultry in these markets is also likely to create more favourable market conditions for cultured-meat manufacturers; chicken and duck meat are expected to be the first cultured meats to be market ready.