|

|

|

|

|

|

|

|

|---|

|

China

|

36

|

45

|

24

|

66

|

2

|

52

|

18

|

|

Malaysia

|

35

|

19

|

13

|

25

|

20

|

19

|

38

|

|

Thailand

|

71

|

55

|

75

|

48

|

9

|

73

|

31

|

|

Sri Lanka

|

61

|

76

|

49

|

72

|

59

|

68

|

39

|

|

Vietnam

|

77

|

103

|

54

|

103

|

22

|

83

|

62

|

|

Pakistan

|

105

|

67

|

47

|

93

|

41

|

70

|

99

|

Source: WEF, Global Competitiveness Report 2019.

Note: Rank out of 141. Quality of roads, efficiency of train services, efficiency of air transport services and seaport services are derived from an opinion survey; air connectivity represents the IATA airport connectivity indicator, which measures the degree of integration of a country within the global air transport network; electricity supply quality is measured using electric power transmission and distribution losses as a percentage of domestic supply.

|

|

|

|

|

|

|

|

|

|---|

|

Southern Expressway (ongoing, started construction in 2011)

|

Loan (4)

|

1,545

|

Fixed Rate – 2%

|

EXIM

|

Road Development Authority

|

CCC

|

- 48% of total expressways.

- Commute to Galle from Colombo has halved from 3 hours to 1.5 hours.

- Better infrastructure has allowed the southern coast to develop as a tourist hotspot.

|

|

Outer Circular Highway Project (ongoing, started construction in 2014)

|

Loan (1)

|

494

|

Fixed Rate – 2%

|

EXIM

|

Road Development Authority

|

Metallurgical Corporation of China Ltd

|

- 5% of total expressways.

- Easier commute to Colombo from suburbs.

|

|

Colombo Katunayake Expressway (completed in 2013, started construction in 2009)

|

Loan (1)

|

248

|

Fixed Rate – 6.3%

|

EXIM

|

Road Development Authority

|

China Metallurgical Group Corporation

|

- 15% of total expressways.

- Reduced commuting time to airport from 2 to 1.5 hours from Central Colombo.

|

|

Hambantota International Airport project (completed in 2013, started construction in 2010)

|

Loan

|

190

|

Fixed Rate – 2%

|

EXIM

|

Airport & Aviation Lanka Limited

|

CHEC

|

- Emergency landings possible with 2nd airport.

- Saved Sri Lanka $1.5 M per flight, if diverted to Southern India during an emergency.

- Increased national passenger capacity, reducing congestion at Colombo Airport.

|

|

Hambantota

Port Development Project (completed, started construction in 2007)

|

Loan (3)

|

1,335.7

|

Fixed (2–6.5%) and Variable Rates

|

EXIM

|

Sri Lanka Ports Authority

|

CHEC

|

- Industrial zone will bring in more primary industries.

- Diversified port operations through the addition of value-added services.

|

|

CICT Colombo Terminal

(completed in 2014, started construction in 2011)

|

Investment

|

500

|

N/A

|

CMPH

|

Sri Lanka Ports Authority

|

CMPH

|

- Currently the only deep-water terminal in South Asia equipped with facilities to handle the largest vessels afloat.

- CICT has helped the Port of Colombo to move up the Drewry’s Port Connectivity Index to be ranked the 11th best connected port in the world in 2018.

|

|

Norocholai power station (completed in March 2011, started construction in 2006)

|

Loan (3)

|

1,346

|

Fixed Rate – 2%

|

EXIM

|

Ceylon Electricity Board

|

China Machinery Engineering Corporation

|

- Accounts for 31% of total installed capacity of CEB-owned power plants.

- Accounts for 33% of Sri Lanka’s total power generated in 2018.

|

|

Colombo Port City (ongoing, to be completed in 2042, started construction in 2014)

|

Investment

|

1,300

|

N/A

|

CHEC

|

N/A

|

CHEC

|

- Adding 1.5 million units of A-Grade office space (tripling total office space in Colombo).

- Would improve Sri Lanka’s ease of doing business rankings.

- Likely to attract high tier financial services.

|

|

Lotus Tower

(completed in September 2019, started construction in 2012)

|

Loan

|

88.6

|

|

EXIM

|

Telecommunications Regulatory Commission of Sri Lanka

|

China National Electronics Import & Export Corporation

|

-

Improve telecommunications infrastructure.

- Reduce the number of downtime incidences.

-

Provide leisure activities to public.

|

Source: Calculations based on data provided by the Central Bank of Sri Lanka, Department of External Resources, Ministry of Finance, Sri Lanka; Board of Investments, Sri Lanka, and various interviews with key persons.

Notes: EXIM: Export-Import Bank of China; CMPH: China Merchant Port Holdings; CHEC: China Harbour Engineering Company; CCC: China Communications Construction Company Limited.

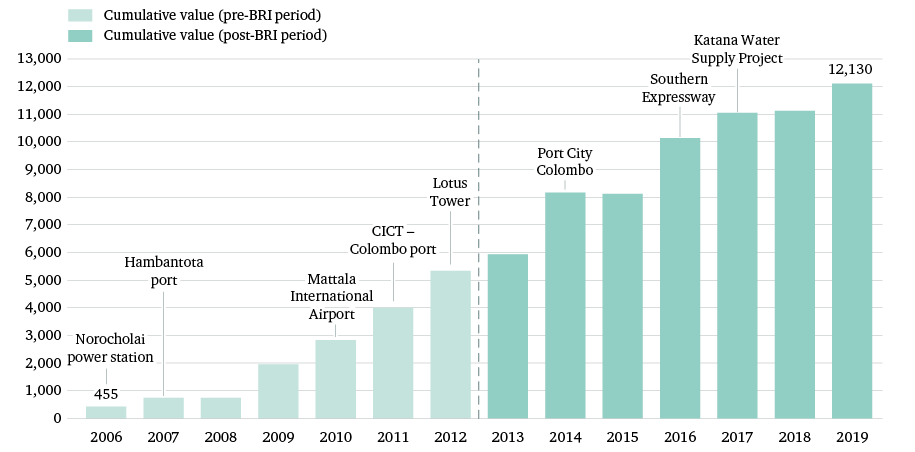

Studies have attempted to quantify unmet infrastructure needs across South Asia and provide indicative estimates of current infrastructure gaps. In 2014, a World Bank report on infrastructure in South Asia conservatively estimated that Sri Lanka requires as much as $36 billion (at current prices) to close its infrastructure gap. This works out at a staggering 40.5 per cent of Sri Lanka’s 2018 GDP.

Taking into account existing Chinese investment commitments, Sri Lanka’s present infrastructure financing requirement is estimated to be around $23.9 billion. Chinese infrastructure investment alone is insufficient to close Sri Lanka’s infrastructure gap. Cumulative Chinese infrastructure investment commitments, since 2006, amount to approximately 33 per cent of the estimated figure needed. Sri Lanka faces the difficult task of raising significant amounts of additional finance from other sources (international capital markets, general taxation and other donors) for its unmet infrastructure needs.

What are the expected economic benefits of Chinese investments?

One way to assess the expected economic benefits of Chinese infrastructure investments is to look at the effects of specific projects on Sri Lanka’s infrastructure development. Table 2 provides details of major Chinese projects including financing, actors and expected economic benefits.

Roads and expressways are the largest subsector for Chinese investment in Sri Lanka. Since 2009, investment from China has built an estimated 116.1 km or 68 per cent of the length of all expressways in Sri Lanka. Three major expressway projects – the Southern Expressway, the Colombo–Katunayake Expressway, and the Colombo Outer Circular Highway – have benefited from this investment. These infrastructure projects have significantly contributed to improving national road connectivity, enhancing road safety and reducing journey times. These investments have the potential to help Sri Lanka attain the same quality of roads seen in other upper-middle-income economies like Malaysia.

Roads and expressways are the largest subsector for Chinese investment in Sri Lanka. Since 2009, investment from China has built an estimated 116.1 km or 68 per cent of the length of all expressways in Sri Lanka.

For example, the 126-km Southern Expressway, linking Colombo with the major cities of Galle and Matara, has opened up southern Sri Lanka, halved journey times from Colombo to Galle to 1.5 hours, and improved road safety. Four loans from the Export-Import Bank of China (EXIM Bank China) totalling $1.6 billion between 2014 and 2017 supplemented start-up loans that the project received in the early 2000s from the Asian Development Bank (ADB) and the Japan Bank for International Cooperation. China Harbour Engineering Company, China State Construction Engineering Corporation and China Aviation International Engineering Company constructed the Chinese-financed sections of the Southern Expressway.

Ports are the second-largest subsector for Chinese investment, for example building the fourth terminal at Colombo port and constructing the new Hambantota port in Southern Sri Lanka. Investments in port capacity, and the ability to handle containerized cargo from mega container ships, have enabled Sri Lanka to leverage its strategic geographical location in the Indian Ocean and become a regional trading hub. In 2018, about 79 per cent of Colombo port’s throughput was for transhipment purposes in response to demand from a rapidly growing Indian market.

A major part of the success of the Colombo port is due to an initial Chinese investment of $500 million in 2011 by China Merchant Port Holdings Company in the CICT. This is the only state of the art deep-water terminal in South Asia, which can handle ultra large container carriers (ULCC) or more than 20,000 twenty-foot-equivalent-unit (TEU) vessels. Commencement of CICT operations in 2014 was critical in Sri Lanka, consolidating its position in regional transhipment trade over the last few years. With the geographical coverage of these services and high frequency of mainline liner service connections, CICT has helped the Colombo port become the 11th best connected port in the world.

Another key project was the transhipment port at Hambantota in the early 2000s, which was expected to become the country’s second-largest port after Colombo port. It was financed by three fixed interest rate loans from EXIM Bank China amounting to $1.4 billion. Two Chinese state-owned enterprises (SOEs), China Harbour Engineering and Sinohydro Corporation, constructed the port. However, the project took longer than expected to come on stream and incurred financial losses putting a strain on Sri Lanka’s public finances. Some have seen this as an example of unprofitable infrastructure investment and China’s so called ‘debt-trap diplomacy’.

To stem financial losses, in 2017, the coalition government of President Sirisena agreed to give Chinese SOEs a controlling interest in managing the port under a 99-year lease. In accordance with a risk-sharing agreement, Sri Lanka received $1.12 billion, which was used to bolster the country’s foreign exchange reserves. Furthermore, the management of the Hambantota port moved to a Chinese SOE, China Merchant Port Holdings Company Limited. This global port operator is not only developing Hambantota port and the adjacent industrial zone but also working to diversify the range of available port related services (e.g. ship repairing and bonded warehousing and distribution). Once Hambantota port becomes fully operational over the next few years, container traffic through Sri Lanka has the potential to double to some 16 million TEUs. The adjacent industrial zone is expected to attract new foreign investment and create jobs.

Non-renewable energy generation is the third-largest sector for Chinese investment in Sri Lanka. In the early 2000s, Sri Lanka suffered from unreliable electricity supply and periodic power cuts that hampered the economy. A temporary solution of commissioning 10 diesel power plants did little to alleviate the electricity supply problem and exacerbated the high dependence on imported diesel fuel and high electricity prices.

Eventually, the Norocholai power station in northwest Sri Lanka – also known as the Puttlam power plant – emerged as a longer-term solution to the country’s electricity supply problems. It was co-financed by three EXIM Bank China loans amounting to $1.4 billion, with additional financing from the government of Sri Lanka. The China Machinery Engineering Corporation began construction on the project in 2007 and built it in three phases – each with a 300-megawatt capacity – over a seven-year period. The Norocholai power station is now the largest power station in the country and a significant contributor to the country’s electricity supply. The power plant made up 31.1 per cent of the total installed capacity of Ceylon Electricity Board-owned power plants and accounted for 33 per cent of total Sri Lankan power generation in 2018.

Urban development in the form of the Port City Colombo project is the fourth subsector for Chinese investment. It is a new city built on 269 hectares of reclaimed land as an extension of Colombo’s central business district.

Along with water and sanitation, urban development in the form of the Port City Colombo project is the fourth subsector for Chinese investment. It is a new city built on 269 hectares of reclaimed land as an extension of Colombo’s central business district. An international financial centre lies at the heart of this project along with residential and retail developments. CHEC Port City Colombo (Pvt) Ltd, which is a wholly owned subsidiary of China Harbour Engineering Company (CHEC), whose parent company is China Communications Construction Company, is the main developer and has initially invested $1.3 billion. The Port City is expected to be a game changer for modern service development in Sri Lanka, made up of financial, ICT and professional services along the lines of Dubai International Financial Centre and the Gujurat International Financial Tec-City. On completion in 2042, the development is expected to add 1.5 million units of A-grade office space to Colombo, tripling the current office space capacity. Furthermore, assuming the Port City is 60 per cent operational, it will generate 122,000 jobs and bring in FDI close to half a billion dollars. Even higher numbers are predicted during the construction phase of the project.

Assessing the political and economic costs of Chinese investment

Some aspects of Sri Lanka’s experience of Chinese infrastructure investment are portrayed as a cautionary tale for other developing countries. Three negative aspects or economic costs associated with Chinese infrastructure investment in Sri Lanka are analysed below: 1) the Chinese debt trap; 2) a trade deficit with China; and, 3) limited domestic spillovers from Chinese investments.

Has Sri Lanka fallen into a Chinese debt trap?

One widely held interpretation of China’s approach to Sri Lanka is that it uses commercial loans to advance its economic and geostrategic interests in the country. This view has been expressed by US Vice President Mike Pence, billionaire financier George Soros, the New York Times and think-tanks in Delhi and Washington DC. Their argument is that the BRI has extended large commercial loans for infrastructure projects in Sri Lanka without the strict conditionality normally imposed by multilateral development banks. Consequently, projects that were not commercially viable, particularly the Hambantota port, sustained losses. As a result, Sri Lanka became entangled in a debt trap that resulted in the country conceding majority control in national assets like Hambantota port and made the country vulnerable to Chinese influence.

However, cross-country macroeconomic analyses of Sri Lanka’s debt dynamics do not support this argument. Hurley et al. assessed the likelihood of debt problems in a sample of 68 countries that received BRI investment from China but did not include Sri Lanka in the eight countries they identified as being of particular concern. Similarly, another study of debt sustainability in 25 countries in Asia with exposure to BRI projects reported that Sri Lanka is at low-to-medium risk of BRI-related debt problems. Mongolia, Kyrgyz Republic, Tajikistan, Laos and the Maldives are all at higher risk.

The IMF’s review of its extended fund facility in Sri Lanka reported that China has become an important provider of commercial loans to Sri Lanka for infrastructure projects and that these loans amounted to about $5 billion (15 per cent of external debt) at the end of 2018. Sri Lanka faces a general foreign debt problem, but this has little to do with Chinese loans. Such macroeconomic analyses may not be regarded as conclusive as they only provide estimates of Sri Lanka’s debt position and China’s role in it. Furthermore, these studies make little mention of the critical issue of the debt sustainability of Chinese loans.

Based on data from the Ministry of Finance and the Central Bank of Sri Lanka, Table 3 provides information on Sri Lanka’s total external public debt by holder and the ratio of debt service to exports. The data on Sri Lanka’s total external debt and debt sustainability suggests that Sri Lanka may be at risk from a general external debt problem. In 2018, Sri Lanka’s total external public debt rose to $34.7 billion and its debt service ratio increased to 15 per cent.

|

|

|

|

|---|

|

Total external public debt (a) – $ billion

|

23.7

|

28.6

|

34.7

|

|

Of which is held by:

|

|

|

|

|

China (b)

|

2.2

|

4.8

|

5.0

|

|

Japan

|

4.3

|

3.4

|

3.4

|

|

Other bilateral lenders (c)

|

3.3

|

2.3

|

2.2

|

|

Multilateral lenders (d)

|

6.6

|

7.3

|

7.9

|

|

Financial markets

|

7.0

|

10.8

|

16.2

|

|

Other (e)

|

0.3

|

0.1

|

0.1

|

|

External debt service to exports of goods & services (f)

|

12.3%

|

12.0%

|

15.0%

|

|

Of which is held by:

|

|

|

|

|

China

|

0.8%

|

2.3%

|

2.5%

|

|

Japan

|

2.5%

|

1.3%

|

1.2%

|

|

Other bilateral lenders

|

1.7%

|

1.8%

|

2.5%

|

|

Multilateral lenders (World Bank, ADB etc.)

|

2.0%

|

1.9%

|

2.3%

|

|

Financial markets (g)

|

5.2%

|

4.8%

|

6.6%

|

Source: Central Bank of Sri Lanka & Department of External Resources, Ministry of Finance Sri Lanka.

a) Total external public debt is calculated as external debt of the central government plus external debt of SOEs and public corporations.

b) Includes central government debt held by the Chinese government, China Development Bank, and the EXIM Bank China, as well as Chinese loans to SOEs.

c) Comprises of other external debt of SOEs for which the ownership is not published.

d) Bilateral lenders include India, US, Germany etc.

e) Multilateral lenders include World Bank, ADB etc.

f) Does not include debt service of foreign loans to SOEs.

g) Financial markets include: International sovereign bonds and foreign currency term financing facility.

The value of Sri Lanka’s external public debt to China doubled from $2.2 billion to $5 billion between 2012 and 2018 with a significant spike in debt occurring between 2012 and 2014 (see Table 3). As a percentage of GDP, Sri Lanka’s external debt to China rose from 3.2 per cent to 5.6 per cent between 2012 and 2018. However, Sri Lanka owes less to China than it does to other foreign creditors. In 2018, external public debt owed to financial markets (e.g. holders of international bonds issued in Sri Lanka) accounted for as much as 18.2 per cent of Sri Lanka’s GDP, while the amount owed to multilateral lenders stood at 8.9 per cent and bilateral lenders accounted for 6.3 per cent of external public debt. This compares with 2012 figures of 10.2 per cent owed to financial markets, 9.7 per cent to multilateral lenders and 11.1 per cent to bilateral lenders. This is indicative of a shift in Sri Lanka’s foreign financing and debt dynamics during the transition to upper-middle-income status. A higher per capita income has meant that the country is graduating from concessionary aid towards more reliance on bilateral commercial loans and financial markets.

Debt sustainability – the ability to service external debt (principal plus interest) – is perhaps more indicative of a country’s macroeconomic well-being than its level of total external debt. This is usually presented as a ratio to export earnings. From a low base, the cost of Sri Lanka’s external public debt service to China quadrupled from $104 million to $498 million between 2012 and 2018. However, Sri Lanka’s ratio of external debt service to China to export earnings only saw a modest rise from 0.8 per cent to 2.5 per cent over the same period (see Table 3). Sri Lanka’s burden of servicing debt to financial markets and other lenders is greater than that to China. For instance, in 2018, Sri Lanka’s ratio of external debt service to financial markets to export earnings was 6.6 per cent and to bilateral lenders was 3.7 per cent of exports. Meanwhile, debt service to export ratios to multilateral lenders (2.3 per cent) was on par with the debt service ratio to China.

Have Chinese investments increased Sri Lanka’s trade deficit with China?

Chinese infrastructure projects in Sri Lanka have relied heavily on imported capital goods and intermediate goods from China. For instance, the Southern Expressway was built using significant imports of Chinese road construction equipment and road construction materials. This reflects several factors including (i) established long-term buyer–seller relationships between Chinese SOE contractors in Sri Lanka and SOE suppliers in China, (ii) heavy state subsidies to highly protected SOE suppliers and private companies in China and hence artificially low prices for exports, and (iii) the lack of a capital goods industry in Sri Lanka.

The data show that Sri Lanka’s imports of capital goods and intermediates from China have surged since 2006, linked to an increase in Chinese infrastructure investment. Before the announcement of the BRI, Sri Lanka’s capital imports from China accounted for around 17 per cent of Sri Lanka’s total capital goods imports in 2006–12, which rose to 27 per cent in 2013–17. Meanwhile, Sri Lanka’s intermediate goods imports from China rose from 58 per cent of the country’s total intermediate goods imports to 62 per cent over the same period. The import surge destined for Chinese infrastructure projects in Sri Lanka, coupled with a small base of Sri Lankan exports to China, translated into a growing trade deficit between the two countries. Sri Lanka’s overall trade deficit with China (as a share of Sri Lanka’s GDP) rose from -2.6 per cent in 2006–12 to -4.3 per cent in 2013–19.

Are there domestic spillovers from Chinese investment?

FDI is regarded as a crucial vehicle for economic development particularly for economies in the process of industrialization like Sri Lanka. Among other benefits, FDI tends to result in a diffusion of technology and management practices to domestic firms, which improves their productivity and competitiveness. Studies often distinguish between direct spillover effects of FDI (specific firm-to-firm knowledge transfers) and more indirect spillover effects from FDI (increased FDI presence, productivity improvements and industrialization). However, project-level data gaps make it more challenging to analyse direct spillover effects.

The available data suggest that there were limited indirect domestic spillovers in terms of sectoral shifts, exports and employment from Chinese infrastructure investment since 2009. Information on sectoral shifts show that Chinese infrastructure investment has dominated Chinese FDI into Sri Lanka since 2009, accounting for 88.7 per cent in 2009–12 and rising to 99.4 per cent in 2017–18. This occurred at the expense of Chinese FDI into manufacturing and services, which saw significant declines over the same period. Not surprisingly perhaps with low-level FDI support, Chinese firms in manufacturing and services have made little contribution to either exports or employment in Sri Lanka. They accounted for less than 1 per cent of the exports of all firms that work with the Board of Investment, Sri Lanka’s investment promotion agency, in 2009–18 and about 1 per cent of employment of those firms in the same period.

Conclusion

While Sri Lanka became an upper-middle-income economy in 2019, its overall infrastructure performance remains well below the expectations for similar economies. The cumulative value of Chinese infrastructure investment into Sri Lanka, which amounted to $12.1 billion between 2006 and July 2019, was insufficient to close Sri Lanka’s huge infrastructure investment gap. The expected economic benefits to Sri Lanka from Chinese investment varies across sectors and projects with some sectors and projects generating greater economic benefits than others. While Sri Lanka is often portrayed as having been engulfed by a Chinese debt trap as a result of public investment finance, the evidence suggests that Sri Lanka has a general debt problem rather than a specific Chinese debt problem. Other challenges include a growing trade deficit with China and limited domestic spillovers from Chinese investment. The economic analysis in this chapter suggests that Sri Lanka should put in place more effective foreign debt management strategies, implement a strong investment promotion and export push towards the Chinese market and encourage greater domestic linkages from Chinese projects.