Sisi’s debt to his Gulf Arab backers

The route of Abdel-Fattah el-Sisi to power came via a campaign of popular protest against the Morsi government during the first half of 2013. This culminated in mass demonstrations at the end of June and a palace coup on 3 July, carried out by Sisi himself as defence minister and commander of the Egyptian armed forces. The rebellion against Morsi was orchestrated by figures with ties to the Egyptian military, and was, to varying degrees, supported by the US, Israel, the UAE and Saudi Arabia, on the basis of their deep misgivings about the Muslim Brotherhood being in charge of such an important regional power as Egypt.

Saudi Arabia and the UAE were quick to declare their approval of Sisi’s action, and underlined this with generous financial transfers. A powerful UAE delegation led by Crown Prince Mohammed bin Zayed visited Cairo at the start of September, just two weeks after an estimated 1,000 people had been killed when the security forces stormed protest encampments set up by supporters of the ousted president.7 The alacrity with which the Emirati and Saudi leaderships announced their backing for Sisi prompted the question of whether they had played a part in enabling the coup – which has since been officially termed the ‘30 June Revolution’. According to recordings subsequently leaked from the Egyptian Ministry of Defence and to confidential testimony from US officials, it is highly likely that the UAE provided funds to support the activity of Tamarrod, the movement that organized the mass petition against Morsi.8

The rebellion against Morsi was orchestrated by figures with ties to the Egyptian military, and was, to varying degrees, supported by the US, Israel, the UAE and Saudi Arabia, on the basis of their deep misgivings about the Muslim Brotherhood being in charge of such an important regional power as Egypt.

Sisi’s own connections to the Gulf went back to his stint as defence attaché in the Egyptian embassy in Riyadh in the final period of the Mubarak presidency – he had been recalled to Cairo in early February 2011 to take up the post of head of military intelligence, replacing Murad Mowafi, who in turn took over as head of the General Intelligence Service from Omar Suleiman, one of Mubarak’s closest aides. As part of the promotion, Sisi had become a member of the SCAF, the army’s supreme council, which ruled Egypt until Morsi’s eventual assumption of the presidency. Morsi himself had also shaken up the military hierarchy early in his presidency, in August 2012, choosing Sisi as the new defence minister and army commander (replacing Field Marshal Mohammed Tantawi) and promoting another relatively young SCAF member, Sedky Sobhi, to the position of chief of staff of the armed forces (replacing Sami Anan).

As mentioned, the subsequent ousting of Morsi in mid-2013 prompted immediate financial support from several Gulf Arab states. In the days following the coup, Saudi Arabia, the UAE and Kuwait announced a $12 billion aid package, half of which would consist of long-term, low-interest deposits with the Central Bank of Egypt, with the remainder being provided as grants, mainly in the form of supplies of petroleum products. The initial transfers, including $2 billion each from the UAE and Saudi Arabia during July, were reflected in a rise in long-term deposits within the central bank’s quarterly tally of external debt, from $3 billion at the end of June 2013 (comprising placements by Saudi Arabia and Libya) to $9 billion in September (reflecting placements of $2 billion each by Saudi Arabia, Kuwait and the UAE). Offsetting some of these inflows, the remaining short-term deposits and medium-term bonds from Qatar were subsequently paid off as they reached maturity over the following two years, while the $2 billion deposited by the Central Bank of Libya was paid back by mid-2018.

Table 1: Long-term deposits by Gulf Arab creditors (as of December 2018)

|

Date of placement |

Amount |

Interest rate |

Maturity |

|

|---|---|---|---|---|

|

Kuwait |

24/09/2013 |

$2 billion |

12-month Libor |

20/09/2019 |

|

21/04/2015 |

$2 billion |

2.5% |

22/4/2019, 23/4/2019, 22/4/2020 |

|

|

Saudi Arabia |

09/05/2012 |

$1 billion ($500 million outstanding) |

3-month Libor |

09/05/2019–09/11/2020 |

|

19/07/2013 |

$2 billion |

3.0% |

19/07/2019 |

|

|

22/04/2015 |

$2 billion |

2.5% |

22/04/2019, 22/04/2020, 22/04/2021 |

|

|

23/09/2016 |

$2 billion |

4.5% |

01/07/2019 |

|

|

16/05/2017 |

$1 billion |

4.5% |

01/07/2019 |

|

|

UAE |

17/07/2013 |

$1 billion |

3.0% |

15/07/2021 |

|

17/07/2013 |

$1 billion |

3.5% |

17/07/2023 |

|

|

22/04/2015 |

$666.7 million |

3.0% |

20/04/2021 |

|

|

22/04/2015 |

$1.333 billion |

2.5% |

22/04/19, 22/04/2020 |

|

|

13/05/2016 |

$1 billion |

2.5% |

30/05/2019, 30/05/2020, 30/05/2021 |

|

|

31/08/2016 |

$1 billion ($900 million outstanding) |

4.0% |

31/08/2022 |

|

Totals |

||||

|---|---|---|---|---|

|

Principal |

Interest |

Total |

||

|

Kuwait |

$4 billion |

$100.4 million |

$4.14 billion |

|

|

Saudi Arabia |

$7.5 billion |

$218.2 million |

$7.72 billion |

|

|

UAE |

$5.9 billion |

$525 million |

$6.43 billion |

|

|

Total |

$17.4 billion |

$843.6 million |

$18.24 billion |

|

Source: Central Bank of Egypt (2013), Quarterly Report Volume 64: External Position of the Egyptian Economy, https://www.cbe.org.eg/en/EconomicResearch/Publications/Pages/ExternalP… (accessed 16 Mar. 2020).

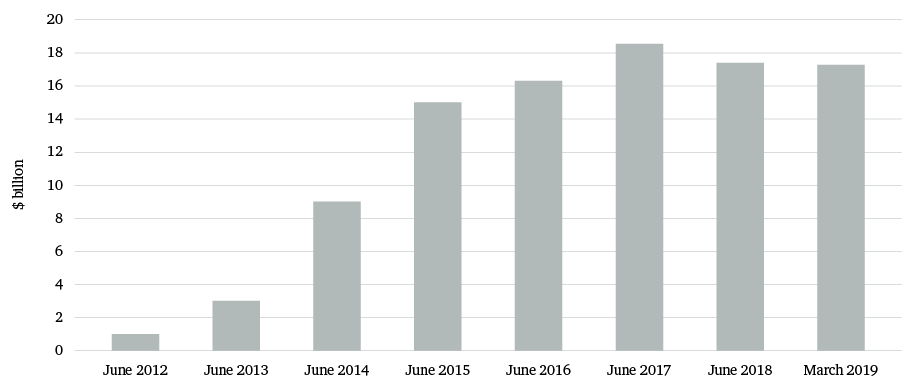

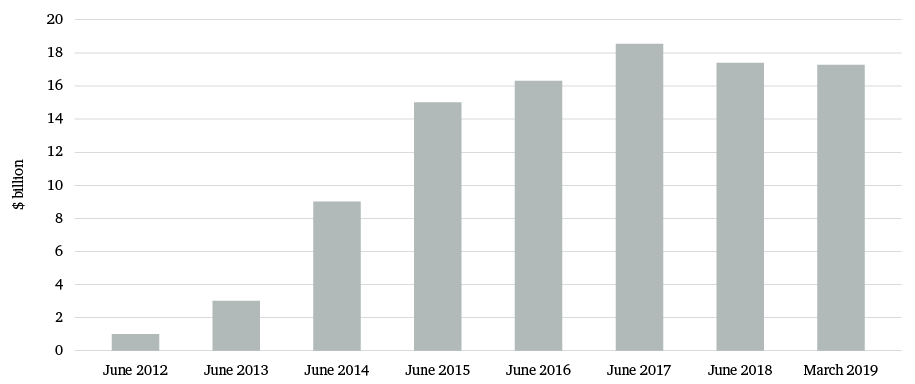

Figure 1: Long-term deposits with Central Bank of Egypt, $ billion

Figure 1: Long-term deposits with Central Bank of Egypt, $ billion

To compensate for the withdrawal of funds by Qatar, there was a second set of deposits of $2 billion each from the UAE and Saudi Arabia in April 2015. These two core Gulf allies deposited a further $5 billion in total in 2016 and 2017, in a move designed to complement a $12 billion extended fund facility that Egypt signed with the IMF in November 2016 (see below).

As a result, according to details provided by the Central Bank of Egypt in its quarterly bulletins on the country’s external financial position, the total amount of deposits peaked at just over $18 billion in mid-2017. This came down to $17.4 billion in 2018, following the repayment of the final instalments to Libya. The most recent bulletin available as this research paper was being written covered the period up to the end of 2018. This showed that $10.4 billion was due to be repaid (mainly comprising principal) to the UAE, Saudi Arabia and Kuwait during 2019. Based on monthly central bank figures for Egypt’s net international reserves up to January 2020, it appears likely that some, if not all, of these maturities have been extended, although there have not been any official announcements. Typically, the central bank inserts a note in its monthly reserve update to explain any significant change resulting from a debt repayment. Foreign exchange reserves (excluding gold) remained stable at about $40 billion during 2019, with no exceptional payments noted. Roughly half of the total due in 2019 was scheduled to be paid to Saudi Arabia in July, redeeming deposits of $2 billion and $3 billion, but the central bank’s reserve figures do not give any indication that payments of that magnitude were made during that month. More clarity on the status of the deposits should come once external debt and balance-of-payments data for the whole of 2019 are published.

The Gulf deposits have played an important part in the increase in Egypt’s total external debt to $106 billion as of March 2019, up from $43 billion in June 2013. However, these deposits are not classified as part of the government’s public debt (of which the external component stands at about $50 billion), according to the Ministry of Finance’s definition.9

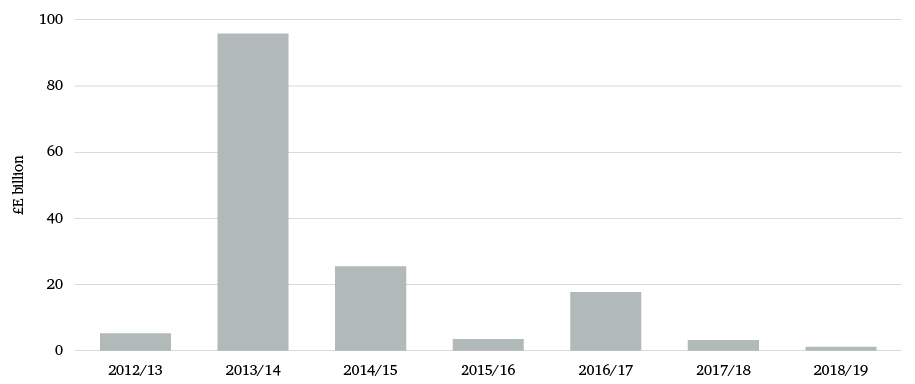

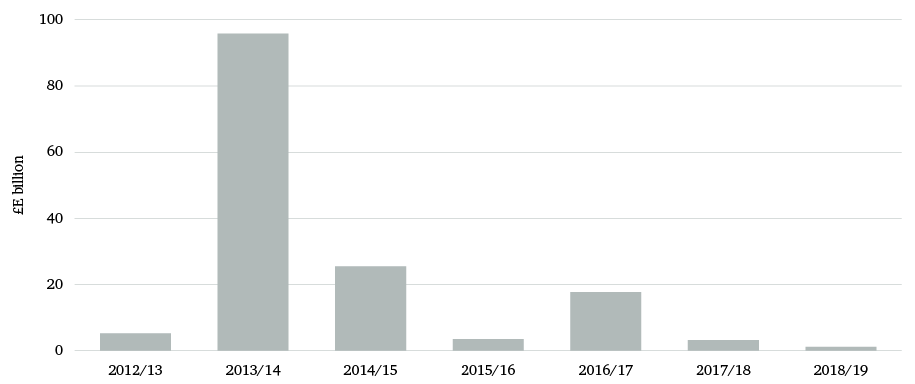

The other main source of documented Gulf aid to the Sisi administration has been grants and supplier credits to finance the import of petroleum products. The bulk of the grants came in the two years following Morsi’s overthrow. In the 2013/14 (July–June) fiscal year, such grants totalled £E95.9 billion ($13.7 billion at the then prevailing exchange rate), and in the following year they reached £E25.4 billion ($3.4 billion), with part of the reduction stemming from the fall in oil prices. The value of grants fell sharply thereafter as the financing for fuel supplies switched to supplier credits – although there was a rise to E£17.7 billion (about $1 billion at the average exchange rate following devaluation) during 2016/17, reflecting capital grants from the UAE to finance investment projects, according to the Ministry of Finance.10

However, budgetary support from the Gulf donors came with some conditions. The UAE, in particular, sought to ensure that the aid would enable the Egyptian government to achieve financial sustainability through enacting economic reforms. (This was similar to the efforts of the same donors to put pressure on the Sadat administration in the mid-1970s to rein in wasteful budget spending, after they had provided grants and loans to support Egypt in the aftermath of the October 1973 war with Israel. Their attempts to push the government towards embracing an IMF-backed package of fiscal reforms had caused some resentment within Egypt.)11 The aid to Sisi’s administration was accompanied by a reform package drawn up for the UAE government by Lazard investment bank and Strategy& (formerly Booz Allen). The package was overseen by Sultan al-Jaber, a minister of state in the UAE government who was later appointed chairman of the Abu Dhabi National Oil Company.

Figure 2: Grants to Egypt from Gulf Arab donors, £E billion

Figure 2: Grants to Egypt from Gulf Arab donors, £E billion

Egyptian officials sought to play down suggestions that the UAE was seeking to impose a kind of shadow IMF programme. An unnamed Egyptian official was quoted by the Financial Times as explaining: ‘It is more a reform attitude rather than a programme: more like, how can we help you reform or study certain things like, for instance, the investment environment? Or how can we reduce the oil companies’ debt?’12 The active involvement of Sultan al-Jaber did help some UAE-based companies to resolve problems that they had faced following the departure of Mubarak. One such company, Dana Gas, explicitly acknowledged the UAE official’s role in the conclusion of a deal in which the company committed itself to new investment in return for the settlement of arrears on payments due from the Egyptian government for sales of natural gas.13

However, the deposits and grants from the Gulf donors in the three years following the removal of Morsi provided only brief respites, as each infusion of funds was deployed in a vain effort to defend a heavily overvalued exchange rate. Egypt’s foreign exchange reserves stood at $11.2 billion in June 2013, on the eve of Sisi’s coup (having fallen to just below $9 billion earlier that year, before Qatar stepped in with its final tranche of aid). The initial round of post-Morsi Gulf deposits pushed reserves up to about $15 billion, but these slipped back to $11.6 billion at the end of 2014. Another round of deposits lifted reserves to $16 billion by April 2015, but again they slipped back to $11 billion within 12 months. Sisi and his central bank governor, Tarek Amer, concluded by mid-2016 that Egypt had little choice other than to seek support from the IMF.

In August 2016, the IMF announced that it had reached a staff-level agreement on a $12 billion extended fund facility – the amount to which Egypt was eligible had been increased at the start of the year as part of a global adjustment of IMF quotas. There were two implicit preconditions for the final approval of this programme. One was devaluation, couched by the IMF in terms of improving ‘the functioning of the foreign exchange markets’. The other was for the Gulf donors to provide another tranche of finance: ‘It would also be very helpful for Egypt’s bilateral partners to step forward at this critical time,’ the IMF statement said.14

The UAE obliged with a $1 billion deposit later in August, and Saudi Arabia transferred $2 billion in September, with a further deposit of $1 billion in May 2017. These were the final instances of overt financial aid from Sisi’s Gulf supporters. The central bank went ahead with the flotation of the Egyptian pound on 3 November 2016, leading to a 50 per cent devaluation of the currency, and the IMF board approved the loan programme eight days later.

By early 2018, Egypt’s foreign exchange reserves had reached a plateau of about $40 billion, providing a comfortable cushion of six months’ cover for imports of goods and services. By this metric, Egypt’s balance-of-payments position is now relatively secure, and there is no immediate requirement for additional financial support from the Gulf Arab donors. Moreover, under the stewardship of the IMF programme, the government has brought its fiscal deficit down to a manageable level; the deficit had peaked at about 17 per cent of GDP (excluding the Gulf grants) in 2013/14. Gross public debt, while still high at around 90 per cent of GDP, is on a downward path. Despite these improvements, there is no guarantee that Egypt will not need financial support from its Gulf allies in the future, in particular in the event of a major external shock – such as the COVID-19 pandemic, which has already forced Egypt in effect to close down its tourism sector and is also likely to hit remittances as Egyptian workers in the Gulf and Europe are laid off.