The role of circular economy finance and transition funds

Investments in new infrastructure are crucial to making the transition to a circular economy happen. The financial sector has a key role to play in connecting action on climate change, minimizing waste and pollution, and advancing inclusive development pathways. At COP24, in 2018, more than 120 institutions with a combined $6 trillion in assets under management made a public commitment to support a just transition. Large institutional investors are now beginning to offer thematic circular economy funds as a way for investors to tap into the circular economy trends. An important question that arises in the context of distributive justice is: Who will benefit from these investments?

How to finance just transitions has until recently been missing from the majority of climate investment, and even more so from circular economy investments. In the context of climate change, a global framework for investor action on the just transition has been developed to mobilize investors to pursue a just transition as part of their core operating practices. These frameworks can be tailored to the circular economy transitions to integrate concepts and solutions for zero-waste, circular value chains, or product-service systems.

Part of financing just circular transitions will include the creation of funds for affected sectors and communities to support the economic redevelopment of affected regions and communities. Tax reforms that promote better environmental practices and reform of environmentally harmful subsidy schemes for fossil fuels and other non-renewable resources can create an important source of revenue for just transition funds. Planning for the transfer of funding from industry subsidies that encourage the use of non-renewable resources to transition funds is an important starting point, and should be considered in long-term policy and financing strategies.

In Indonesia, for instance, where national fuel subsidies were reformed in 2015–16, the removal of major energy subsidies cut government subsidy spending, for which some $22.6 billion had been allocated in 2012, to $8 billion in 2015, and then to $4 billion in 2016. Although the overall impacts of the reforms are as yet difficult to evaluate, the reallocation of Indonesia’s fuel subsidies is considered a major step forward in improving public expenditure. Money not disbursed as a result of the phasing-out of subsidies has been used to finance increases in social protection and transfers to villages, and poverty reduction programmes. Although the diverted finance did not reach all vulnerable groups, and the fuel price increases resulting from the reduction in subsidies gave rise to public protests, the reform overall is considered to have generated positive social outcomes. In particular, it improved the efficiency of social welfare policies by replacing indiscriminate fuel subsidies (whereby a disproportionate share of subsidies went to the wealthiest households) with the Bantuan Langsung Tunai (BLT) Cash Transfer programme targeted at low-income households. The challenge for the future will be sustaining these reforms once political and international market conditions change, in particular as regards energy prices.

Just transition funds have some similarities to ecological compensation funds, but their objectives are different. Ecological compensation is a mechanism to protect biodiversity and ecosystem service by counterbalancing ecological damage caused by infrastructure developments in a specific region. In China, for example, ecological compensation schemes have been in place since 1998, with a value to date of approximately $150 billion. Such mechanisms include not only direct payments for environmental services, but also an array of comprehensive measures taxes, fees, subsidies, funds and compensation payments. The aims are to resolve issues resulting from unequal development, imbalanced and ecological economic interests, and unequal distribution of ecological assets.

The aim of dedicated just transition funds, in contrast, is to help affected communities withstand the impacts of industrial restructuring, and to build strong, resilient and diversified new economies. They can create economic opportunities and industrial restructuring in places hardest hit by the energy transition, and help scale community-based transition efforts. In 2019 the European Parliament issued the call for the creation of a new €5 billion ‘Just Energy Transition Fund’, the objective of which would be to ‘address societal, socio-economic and environmental impacts on workers and communities adversely affected by the transition from coal and carbon dependence’. Relevant funds and investment plans have since been included under the Just Transition Mechanism of the European Green Deal, and are also highlighted in the new European Circular Economy Action Plan. The mechanism currently focuses chiefly on local energy transitions, but as implementation progresses it will need to include additional considerations beyond energy and support other industrial sectors to reduce resource consumption and waste generation.

In 2019 the European Parliament issued the call for the creation of a new €5 billion ‘Just Energy Transition Fund’, the objective of which would be to ‘address societal, socio-economic and environmental impacts on workers and communities adversely affected by the transition from coal and carbon dependence’.

As well as support for large industries during the transition, investing in SMEs will also be critical to making the circular economy happen. In 2019 the European Investment Bank (EIB) and five major European national banks launched a Joint Initiative on Circular Economy (JICE) to provide loans, equity investment and guarantees to eligible circular economy projects, including for SMEs. This and similar initiatives point to the development of innovative financing structures for public and private infrastructure, municipalities, and private enterprises of various sizes, as well as for research and innovation projects. However, as most value chains have global dimensions and involve many suppliers in lower-income countries, it is important also to consolidate and streamline existing and new development and climate finance outside Europe. Only if this happens can the circular economy be successful globally.

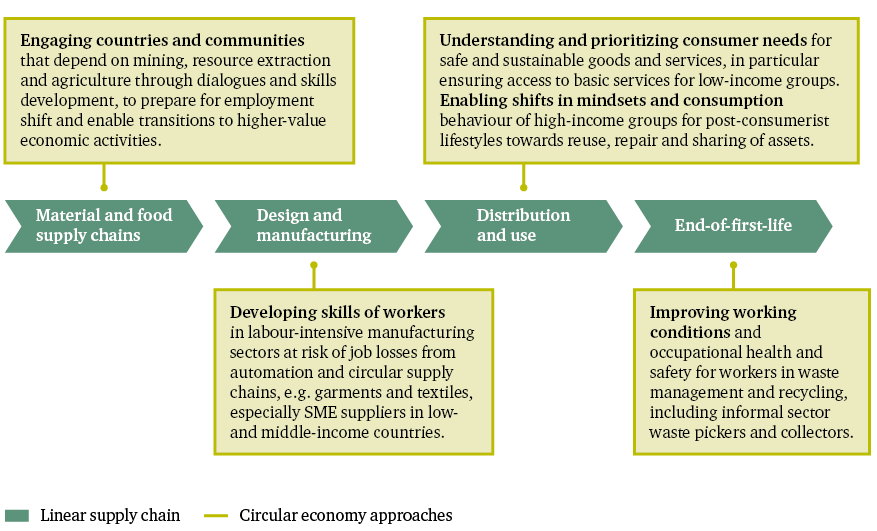

Furthermore, investments are also needed to formalize the waste management and recycling sectors in low-income countries. Donor agencies and NGOs should invest supporting the creation of more formal and equitable work structures for waste pickers, specifically in contexts where formal associations currently do not exist or are weak. The process of integrating waste pickers requires governments and the private sector to understand the complexities of this work, as well as willingness to think creatively in order to facilitate inclusion, the development of higher-value employment opportunities, and better livelihoods.

The role of multilateral cooperation for trade

High levels of public awareness of the issue of marine plastic pollution are among factors that have contributed to greater engagement in thinking about current problems in the trade of waste plastics. China’s 2018 import ban on certain types of low-grade plastic waste highlighted the injustices in the current global trade in waste and recycling value chains, the lack of transparency and accountability in the international waste trade, deceptive practices such as the mislabelling of waste shipments as recyclable materials, and low levels of law enforcement and customs inspections, all of which have facilitated the proliferation of illegal waste trafficking under the guise of recycling. Notably, it had an immediate impact in disrupting trade flows in plastic waste – in some cases directing plastic waste from consumer societies like the UK to low- and middle-income countries with inadequate waste management infrastructure, in many cases illegally.

Issues of power, corruption, marginalization, and unequal distribution of burdens and access to resources are all in strong evidence in the current global trade in waste. Effective governance mechanisms to regulate waste trade will be required to reduce tensions between high- and lower-income countries in all these respects, as well as to make equitable use of the circular economy opportunities associated with the hundreds of millions of tonnes of waste generated each year. One example of these trade tensions between exporting and importing countries can be seen in the issue of plastic scrap import bans and plastic waste shipments that violate the newly amended Basel Convention. In 2019 parties to the Convention adopted a legally binding framework to regulate and enhance transparency in the global trade of certain plastic waste streams. Notably, the new hazardous waste classification for certain plastic waste streams prohibits participating countries from accepting shipments of these kinds of waste from non-parties, such as the US. It also prohibits shipments of hazardous waste without the consent of the importing country. To give one example of the scale of the challenge, Malaysia’s imports of plastic waste from its 10 biggest country sources – including the US, the UK, Japan, Spain and Australia – reached 456,000 tonnes in January–July 2018, up from 316,600 tonnes for the whole of 2017, after China’s ban on imports of plastic scrap and other waste entered effect at the beginning of 2018. With the adoption of the amendment to the Basel Convention, the government of Malaysia began sending non-recyclable plastic back to its country of origin.

The momentum of the circular economy offers the opportunity to energize discussions on the environment and trade, including on a new role for the World Trade Organization (WTO) in tackling plastics pollution. In particular, the WTO’s Aid for Trade initiative, which aims to assist developing countries to overcome constraints to engaging in international trade, could help support paradigm shifts in trade relations for waste and secondary resources. New trade-related programmes could support the circular economy, improved trade performance and reduce poverty. As a strategic priority, these programmes would focus on development needs along with the environmental and economic interests of developing countries.