This paper focuses on the strategic direction of EITI and its implementing countries. Its findings may also help inform debate as governments and their development partners seek to support a recovery in line with a ‘well below 2°C’ world.

Research paper

Published 15 June 2020

Updated 19 November 2021

ISBN: 978 1 78413 402 0

This paper focuses on the strategic direction of EITI and its implementing countries. Its findings may also help inform debate as governments and their development partners seek to support a recovery in line with a ‘well below 2°C’ world.

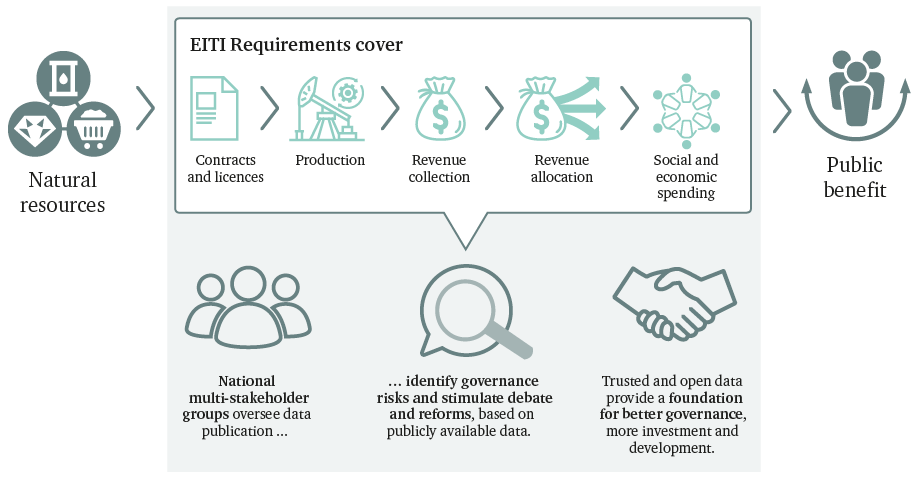

There are several entry points for the discussion of transition within the existing EITI Standard and its Requirements. This chapter explores first, where there may be ‘quick wins’ by asking new questions of the data and disclosures EITI already generates, such as those relating to revenues and contracts; and second, where there may be a case for EITI to encourage the consideration of additional data or disclosures. Some, like greenhouse gas emissions and carbon prices, may already be known and available elsewhere, and could usefully be linked to EITI data. Others, such as the cost of production, may be known but may not be widely or publicly available, and EITI could encourage or require their disclosure. This approach reflects the strategic and capacity concerns noted above, and is intended to encourage stakeholders to address transition as a cross-cutting issue, rather than an additional agenda.

Some of the data and disclosures that EITI generates may already be relevant, when viewed through a transition lens.

The public policies and financial flows that guide the extractives sector can all help shape the supply and demand of extractive resources. Accordingly, they have the potential to either support or undermine transition over time, depending on how they are designed and implemented. The scope of EITI’s Requirements for implementing countries are set out in Figure 1. Some of the data and disclosures that EITI generates may already be relevant, when viewed through a transition lens. For example:

Across the areas outlined above, EITI provides three levels of guidance for implementing countries. The distinction is important, as each implementing country undergoes a process of Validation every three years, where a country’s compliance with the EITI Standard and its Requirements is assessed.

There are mandatory areas that countries must, should or are required to report. These issues will be accounted for in country Validation and the EITI Board’s assessment of a country’s compliance. There are expected areas where countries are expected to or should consider, documenting their discussions and their rationale for disclosure/non-disclosure (including barriers to disclosure). These issues and their documentation are considered in Validation. Finally, there are optional areas – areas that countries are recommended to, are encouraged to, may wish to or could consider. These are documented in Validation, but do not form part of the assessment of country compliance.

In some cases, existing data and disclosures could support analysis and dialogue, if linked to contextual information and guidance. In other cases, such analysis and dialogue would require additional country or project information, which could require the ‘upgrading’ of an existing Requirement, or the expansion of the scope of the data and disclosures required by the 2019 EITI Standard. These areas of analysis and dialogue are summarized in Table 1, and introduced in turn below.

|

Issue |

Relevant EITI Requirements |

Questions for MSGs |

Additional data needs |

|---|---|---|---|

|

Revenue resilience |

5.3 Revenue management and expenditures (part C) |

|

Contextual information

Additional data and disclosures

|

|

6.3 Contribution of the extractive sector to the economy |

|||

|

Project viability |

4.1 Comprehensive disclosure of taxes and revenues |

|

|

|

5.3 Revenue management and expenditures |

|||

|

Distribution of risk |

2.1 Legal framework and fiscal regime |

|

|

|

2.4 Contracts |

|||

|

Public finance at risk |

2.6 State participation |

|

|

|

4.5 Transactions related to SOEs |

|||

|

5.1 Distribution of extractive industry revenues |

|||

|

6.3 Contribution of the extractive sector to the economy |

|||

|

Carbon pricing |

6.1 Social and environmental expenditures by extractive companies |

|

|

|

Emissions reporting |

6.4 Environmental impact of extractive activities |

|

|

|

Subsidies |

5. Revenue allocation |

|

|

|

6.2 Quasi-fiscal expenditures |

|||

|

6.3 Contribution of the extractive sector to the economy |

|||

|

6.4 Environmental impact of extractive activities |

|||

|

Fossil fuel phase-out |

4.6 Subnational payments |

|

|

|

5.2 Subnational transfers |

|||

|

6.2 Quasi-fiscal expenditures |

|||

|

6.3 Contribution of the extractive sector to the economy |

Source: Chatham House analysis of the 2019 EITI Standard, not exhaustive.

The inclusion of contextual information can help set the scene for country discussions relating to climate change and energy transition. Many EITI stakeholders are considering the potential for energy scenarios to provide some wider context for national discussions about transition. Mainstream scenarios, such as those produced by the International Energy Agency (IEA) and the International Renewable Energy Agency (IRENA), for example, can help countries understand the likely evolution of supply and demand under different transition pathways, and test the resilience of their extractive sector plans under these assumptions. However, in a side event at EITI’s Global Conference in 2019, many EITI stakeholders expressed their need for a better understanding of these scenarios, as well as of their implications for demand, prices and investment. Germany’s experience may be helpful here. Its MSG commissioned a study on future demand for metals, and included a descriptive chapter on the share of RE in the domestic energy market in its EITI reporting (see Box 2).

Germany is one of the world’s largest importers and consumers of mineral resources, and a significant producer of lignite (brown coal) for use in its domestic energy system. Energy transition is high on the political agenda, particularly where the scaling of renewables and the phase-out of coal-fired power generation is concerned. Germany has been an EITI implementing country since 2016, and its MSG has explored several issues relating to energy transition – particularly the relationship between RE and future demand for raw materials. This work has included the following:

There are concerns about the MSG’s expertise and resources to cover the field of energy transition and climate change, and the best way to link EITI and energy transition. There are also overlaps with other governance processes such as the Commission on Growth, Structural Change and Employment, which holds discussions on issues relating to the phasing out of power generation from lignite and the related extraction of lignite. While acknowledging these challenges, the MSG remains interested in exploring new areas related to energy transition, and particularly in reporting on the process of phasing out coal, in legal and economic terms.

Based on: Country presentation at the expert workshop Climate Change, Energy Transition and the EITI, convened by Chatham House on 17 January 2020.

Another option would be to expand EITI’s focus from extractive resources to energy systems. Many EITI-implementing countries suggest that EITI could engage with domestic energy and power reforms (see Appendix). Some EITI supporters have also suggested that it may be more natural for EITI to expand to include fiscal flows relating to RE, rather than to include non-fiscal flows relating to extractives.13 While the inclusion of contextual information on energy transition may add value to MSG dialogues, the inclusion of RE reporting presents challenges. Extractives tend to generate large, centralized financial flows, while RE markets are characterized by smaller, decentralized financial flows. This makes them very different to extractives in terms of both the ‘rent’ they offer elites14 and the feasibility of project-level reporting, given the far greater number of actors and payments involved. Germany has explored this (see Box 2).

While the inclusion of contextual data may help set the scene for national discussions relating to energy transition, more granular country- and project-level analysis and reporting will be required to build a fuller picture of a national exposure to transition risks and preparedness for low-carbon opportunities. The following eight areas emerged from research and dialogue, and provide a starting point for engagement with transition.

There is a strong case for producer countries to undertake scenario analysis and stress-test their economies under different transition pathways.

The impact of transition on resource revenues over time is perhaps the single most important question for producer countries. EITI already requires countries to further public understanding and debate, including around the sustainability of revenue collection and allocation. EITI Requirement 5.3 encourages countries to consider ‘projected production, commodity prices and revenue forecasts arising from the extractive industries and the proportion of future fiscal revenues expected to come from the extractive sector’.15 There is a strong case for producer countries to undertake scenario analysis and stress-test their economies under different transition pathways.16 MSGs could help encourage this by exploring the demand and price assumptions that underpin national forecasts, and asking governments to explain how these assumptions compare to those that underpin more rapid transition scenarios. At a high level, such discussions could shine a light on the resilience of revenue forecasts under a range of transition scenarios. They could also call into question the sustainability of sector-linked debt, including infrastructure investment and resource-backed loans.

While top-down assessments can give some indication of the resilience (or vulnerability) of revenues, building a more comprehensive picture of national exposure to climate-related risks will require a granular, bottom-up assessment. With its focus on project-level reporting, EITI is well placed to support assessments of the commercial viability of existing and proposed projects. The vulnerability of any project to being stranded (or of any resource being left undeveloped) can be inferred from its position on a wider cost curve of production. Put simply, projects with a higher cost of production will be more vulnerable to stranding. There are two key metrics here: first, a project’s break-even price (or shut-in price, if it is already online), and second, how this price compares to those of other projects along the cost curve. The think-tank Carbon Tracker has shown how all the major international oil companies (IOCs) sanctioned projects in 2018 that conflict with the long-term goal of the Paris Agreement and represent capital at risk in a ‘well below 2°C’ world, based on their cost of production.17

EITI could help make the data that are required to assess project viability publicly available, or at a minimum, highlight barriers to doing this.

IOCs and their investors have access to commercial data, including estimates of the price of production and sophisticated cost curves. Country stakeholders – including governments, civil society organizations and citizens – often struggle to obtain comparable information. This can lead to unrealistic expectations about both the commercial viability of projects and the potential for the domestic use of fossil fuel supply for power generation and in industry. Cost audits were raised as a ‘missing item on the transparency agenda’ by Oxfam America at EITI’s 2019 Global Conference.18 By expecting the disclosure of data on the cost of production, EITI could help make the data that are required to assess project viability publicly available, or at a minimum, highlight barriers to doing this. Barriers to this are likely to include the fact that the cost of production is not static,19 and that these data may expose the share prices of IOCs to scrutiny.

Encouraging comparative analysis and peer learning between implementing countries could help build a wider discussion around project viability and the risks of stranded assets. EITI data and disclosures typically inform analysis and debate at a country level, and there is limited comparative analysis. The EITI International Secretariat could consider restructuring EITI summary data to support such analysis.

The legal and fiscal regimes that guide the extractive industries and the contracts that define the terms of any given project all have a bearing on the cost of production and the commercial viability of a project. They also determine how the balance of risk and reward is distributed between the state and the private sector, and between a country and its international partners. Striking the right balance here is crucial to the perception of a ‘fair share’ of wealth from extractive resources, and to the sector’s social licence to operate. Many of the assumptions underpinning these regimes and contracts, including the overall time frame for production, will be challenged by transition. There is also the risk of a ‘race to the bottom’ among fossil fuel producers if countries try to bring reserves to market rapidly before demand and prices decline (the so-called ‘green paradox’).20 Similar pressures may be evident for prospective minerals producers too, as they compete with established producers for investment.

Many of the assumptions underpinning these regimes and contracts, including the overall time frame for production, will be challenged by transition.

EITI has a unique opportunity, with all implementing countries being required to disclose contracts and amendments in real time from 2021. First, EITI could encourage analysis of existing contracts for clauses that present transition risks. For example, where the overall share and timing of revenues to a country are concerned, these revenues may be compromised where the time frame for production is shorter than anticipated, and where country returns are scheduled after those of companies. ‘Take-or-pay’ clauses to supply production to the domestic market – where the host country must take supply or pay a penalty – may present substantial economic risk where this fossil fuel supply (and the infrastructure required to utilize it) becomes more expensive than clean alternatives. Second, EITI could explore whether the real-time disclosure of contracts – and amendments to them – could help provide early warning of material deviations to fiscal or contractual terms. The drivers of these deviations could then be explored, including whether a country’s approach is exhibiting signs of a ‘race to the bottom’, and how that might affect the relative risks and rewards from the sector.

A considerable share of extractive revenues is channelled through SOEs and reinvested in the extractive industry. National oil companies (NOCs) can be particularly powerful actors, receiving and retaining large percentages of revenues, accumulating large assets and taking on large debts, with limited transparency or accountability. For example, data from the Natural Resource Governance Institute (NRGI) show that in 2015 the Nigerian National Petroleum Company (NNPC) retained revenues worth over five times as much as Nigeria’s annual healthcare budget. The Ghana National Petroleum Corporation (GNPC) has received around one-third of Ghana’s oil revenues to date. Colombia’s Ecopetrol and Indonesia’s Pertamina carry long-term liabilities worth 3.8 times and 1.8 times total annual oil and gas revenues to government, respectively. In total, NRGI defines at least 25 countries – including seven EITI-implementing countries – as ‘NOC-dependent’, meaning that the NOC collected more than 20 per cent of total government revenue.21

Assessments of ‘capital at risk’ of stranding have helped shareholders to engage IOCs on their management of climate-related financial risks. There remains no comparable assessment of ‘public finance at risk’ …

In recent years, assessments of ‘capital at risk’ of stranding have helped shareholders to engage IOCs on their management of climate-related financial risks.22 There remains no comparable assessment of ‘public finance at risk’ or mechanisms for stakeholder engagement with NOCs. EITI would be well placed to explore this, with its existing Requirements for disclosures on the distribution of extractive industry revenues, state participation in the sector and transactions related to SOEs, including the publication of balance sheet information. Building on these data and encouraging MSGs to estimate the full scale of public finance at risk under different scenarios could help encourage SOEs to develop corporate climate governance, and governments to consider the risks associated with reinvesting in the sector. This could fill an important gap in awareness and accountability at national level, as well as contributing to a more comprehensive assessment of systemic risk at international level.23

Carbon price assumptions are another key variable where the commercial viability of projects is concerned. EITI already requires disclosure of the fiscal regimes guiding the sector and encourages the disclosure of social and environmental expenditures. These could include carbon price regimes and tax payments, although only nine EITI countries currently implement carbon price regimes.24 By contrast, most companies and many MDBs apply internal carbon pricing in their economic analysis and decision-making, and some disclose their carbon price assumptions through their annual reports and mechanisms such as CDP.25 For national decision-makers, the disclosure of carbon prices used by investors – and scrutiny of them in comparison to those used by others – may help support sound decision-making in the sector, and provide an indication of the relative preparedness of operating partners. Such disclosures may also help encourage the development of domestic carbon price regimes and national carbon accounting capacities within the sector, especially in SOEs, and in linked power and industry.

There is growing international scrutiny of the emissions associated with the production of extractive resources. The oil and gas sector is under increasing pressure to address its upstream emissions, especially flaring and fugitive non-CO2 emissions like methane (due to leakage and venting).26 The mining sector must also decarbonize if its contribution to transition is to be sustainable, and progress is now being made on the electrification and the integration of RE in mining activities.27 While many companies disclose greenhouse gas emissions through their annual reports or mechanisms such as CDP, few disclose these data at national or project level (whereas EITI disclosures are made at the project level).

For many producer countries, the extractive sector will be among the largest sources of national emissions. Building national emissions-reporting capacity is important, as the Paris Agreement comes into effect. Countries such as Trinidad and Tobago are already exploring how they might integrate emissions into their EITI reporting (see Box 3), and others have also voiced their interest.28

Efforts to address upstream emissions may also generate financial flows, which would benefit from transparency. Governments have a range of fiscal tools available to them, including disincentives such as carbon taxes or environmental penalties, and incentives such as the desire to recoup revenues (which would otherwise be lost where there is methane leakage, for example) and to access carbon markets (where upstream emissions reductions are packaged into carbon offsets, and traded in return for carbon finance). Carbon finance often flows directly to NOCs, and would benefit from scrutiny.29

Trinidad and Tobago (T&T) is a resource-rich small island state and one of the world’s largest exporters of liquefied natural gas (LNG). It has a long history of large-scale oil and gas production, and small-scale mining, and joined EITI in 2011. Despite being a vulnerable island state with urgent climate adaptation needs, political and societal awareness of the implications of climate change and energy transition remain low. A 2016 survey found that less than 5 per cent of the population and less than 3 per cent of industry (including the extractive industry) saw climate change as a major challenge facing the country. At the same time, successive governments have been unwilling to take the perceived political risk of reducing energy subsidies.

TTEITI has been successful in improving the availability of data around the extractive industries and in being a credible, independent voice. TTEITI believes it has an important role to play in developing public awareness around climate change and energy transition, and the MSG has begun reassessing the elements of ‘good governance’, including beneficial ownership and contract transparency. TTEITI is making progress in encouraging civil society to look beyond financial reporting, and towards the wider environmental and social impacts of the extractive industries. It has been an active advocate of environmental reporting within EITI, including CO2 emissions, and notes the incorporation of environmental reporting in the 2019 EITI Standard as a milestone in this regard.

TTEITI has established an environmental subcommittee with the responsibility of furthering a work programme on environmental reporting, although CO2 emissions are not part of EITI’s environmental reporting requirements. While there are no statutory systems for emissions monitoring in T&T, a pilot programme has been implemented by the Ministry of Planning and Development for the monitoring and verification of emissions. TTEITI has now developed a voluntary template for reporting resource impacts – including electricity, water usage, CO2 and methane – as well as statutory requirements related to air and water pollution. The subcommittee’s long-term aim is to move towards the incorporation of environmental and climate impacts in the sector, including a natural capital approach,30 in conjunction with the Central Bank of Trinidad and Tobago and other agencies, in order to support a broader approach towards the good governance of natural resources.

Based on: National MSG presentations at the expert workshop Climate Change, Energy Transition and the EITI, convened by Chatham House on 17 January 2020.

There may also be value in disclosing the carbon intensity of production. Carbon intensity may provide an indication of a supply chain’s climate-resilience and competitiveness over time, and it varies considerably between countries.31 For minerals producers, the primary concern will be the CO2 emissions associated with extraction, processing and transport, and the availability of options to reduce the emissions associated with these processes and ultimately decarbonize them. For fossil fuel producers, upstream emissions mitigation may significantly improve carbon intensity, but the embedded CO2 in the fuel that is produced and ultimately burned will be the primary driver of carbon intensity.32 Investors and consumers of both minerals and fossil fuels are increasingly looking to carbon intensity as a comparative measure between producer countries and companies. As a metric, carbon intensity will almost certainly increase in prominence as the EU and others consider the introduction of carbon border adjustment mechanisms. Carbon intensity may also add to the overall cost of production if it is considered alongside carbon pricing and internalized, and may bring a project’s commercial viability into question. National governments should have a strong interest in data and analysis on the carbon intensity of their production, as it may enable them to reduce the carbon intensity (and enhance the competitiveness) of their exports and their domestic energy sector, as well as informing their discussions with the EU and other trading blocs.

The allocation of resource revenues to spending (through the national budget) and to savings and investments (through sovereign wealth or strategic development funds) may help support sustainable, low-carbon areas of the economy and ‘crowd in’ international climate finance. However, the presence of production and consumption subsidies acts as a barrier to sustainable investment. Fossil fuel subsidies effectively raise the cost of bringing energy efficiency and RE to the market, as such technologies must be subsidized to compete with fossil fuels, even where they are at price parity (or even ‘subsidized twice’, where they are not).

Fossil fuel subsidies also obscure the real contribution of the extractive industries to the economy. EITI already encourages countries to disclose quasi-fiscal expenditures and to consider the net contribution of the extractive industry to the national economy, and the consideration of subsidies may materially change this picture (see Box 4).

The quantification and disclosure of ‘unseen’ subsidies to the sector could support a more comprehensive assessment of the sector’s net contribution to economic development, and of the trade-offs associated with developing and producing extractive resources.

There are various ways to quantify subsidies, further explored in the next chapter. While some focus purely on the economic costs, others include ‘externalities’ such as the cost of environmental and public health damages. EITI already encourages MSGs to report on the social and environmental impacts of extractive activities. The quantification and disclosure of ‘unseen’ subsidies to the sector could support a more comprehensive assessment of the sector’s net contribution to economic development, and of the trade-offs associated with developing and producing extractive resources. Disclosures on social and environmental expenditures, considered alongside those on social and environmental impacts, could support estimates of the social cost of carbon and encourage natural capital accounting approaches.33

A growing number of countries have now made commitments to phase out coal, and commitments to phase out oil and gas may follow in time. As of June 2020, the national governments of 33 countries have committed to phasing out coal consumption, and some cases, linked domestic coal production.34 Germany has committed to ending coal-fired power generation and to closing its coal mines by 2038 at the latest, at a cost of €40 billion. Several EITI-implementing countries face declining oil and gas production in the coming years, and there will be important discussions to be had around the subnational impacts of this transition. Whether the phase-out of fossil fuels is policy- or market-driven, support for a managed and equitable decline will be crucial. Indeed, the need for a ‘just transition’, which addresses the impacts of transition on fossil fuel dependent countries, regions and communities, is enshrined within the Paris Agreement.

Early consideration of the implications of transition – including how resilient revenues are likely to be throughout transition and how vulnerable assets are to stranding – may help governments anticipate the economic and social impacts of transition, and develop plans to support affected regions and communities. In this respect, the areas outlined above can all contribute to a government’s ability to manage the inevitable decline of the sector. Ensuring that packages of support for fossil fuel-producing regions are transparent in their design and delivery will be crucial to society’s support for transition at national and international levels. This support may include subsidies, compensation and other public financial flows which could, in theory, be considered within many of EITI’s existing Requirements, including subnational payments, transfers and quasi-fiscal payments. Germany is exploring the potential for this (see Box 2). Data on the contribution made by the extractive sector to the economy, including employment, may also help inform planning for an orderly and equitable decline.

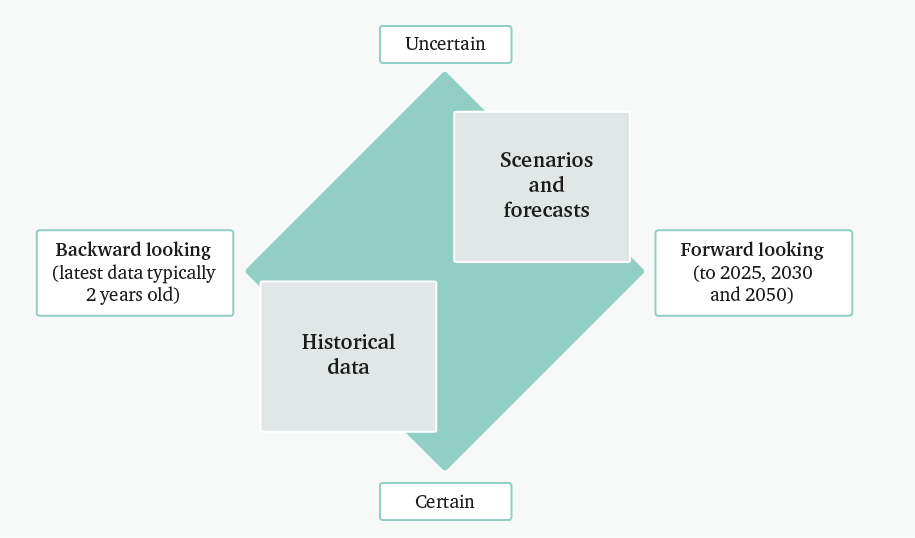

Despite the opportunities outlined above, there remain practical questions about how the data and analysis introduced above might integrate with existing EITI Requirements. Some stakeholders note a tension between EITI’s need for precision and its focus on historical data, and the inherent uncertainty and forward-looking nature of forecasts and scenarios.35 These tensions will be familiar to those working on the disclosure of climate-related financial risks. However, there is an important distinction to be made between forecasts, which represent a projection of current trends, and scenarios that are designed to ‘stress-test’ forecasts under a range of credible pathways and inform planning, policy and investment. As outlined above in Figure 2, below, EITI already encourages the disclosure of forward-looking data in several areas, including government forecasts for production and revenues.

The consideration of forward-looking data and analysis – and of the assumptions that underpin it – appears well aligned with EITI’s mission and Requirements. As EITI’s founding principles state: ‘We recognise that a public understanding of government revenues and expenditure over time could help public debate and inform choice of appropriate and realistic options for sustainable development.’36 In this context, the purpose of analysing EITI data through a transition lens, and considering additional disclosures where appropriate, is to shine a light on the assumptions that underpin decisions being taken today and to allow stakeholders to assess which data are driving those assumptions and whether these data are appropriate and up to date. The next chapter considers how these data, disclosures and dialogues can contribute to improved national and international governance.