Interpretations that emphasize the geopolitical strategic aspects of the BRI are dominant because it is easier to see the project as part of a wider narrative about declining Western power, and the ‘rise of China’, than to examine its more complex economic drivers. While President Xi Jinping clearly aims to signal China’s great-power status through the BRI, it remains a plan mainly aimed at addressing deep crises within the Chinese economy. The Chinese government launched the BRI primarily in order to help address these systemic problems by unlocking overseas demand for Chinese industry, construction projects and loans.

China’s growth model in crisis

China’s annual rate of economic growth has slumped from an average of around 10 per cent during the 2000s to less than 7 per cent since 2015, reflecting the increasing exhaustion of its investment-, infrastructure- and export-led growth model. Fundamentally, Chinese growth was produced by debt-fuelled infrastructure investment, which enabled export-oriented industrial clusters to form, generating export surpluses that repaid the original debt and allowed the cycle to repeat. Historically, in other countries this growth model has always yielded diminishing returns, as the domestic economy cannot absorb additional investment productively or efficiently, causing falling rates of return. In China, this problem was exacerbated by decentralization, with local governments creating new industries in competition with each other, generating irrational duplication and vast surplus capacity (Zhou, 2010: Ch. 7). By 2008, China’s western regions already experienced ‘oversupply of infrastructure’, thanks to the BRI’s forerunner, the Great Western Development Campaign (GWDC), which stimulated growth through financing local and cross-border infrastructure projects (Qin, 2016: p. 213). The problem was exacerbated by Beijing’s introduction of a RMB 4 trillion ($586 billion) stimulus package following the 2008 global financial crisis – 38 per cent of which fuelled further infrastructure spending (Qin, 2016: p. 204). With demand for Chinese exports also falling, surplus capacity increased to 20–30 per cent in most basic industries (European Union Chamber of Commerce in China, 2016).

The early 2010s saw a slump in profitability. The rate of return on domestic infrastructure projects fell to 3.1 per cent in 2012, below capital costs (Leutert, 2016: p. 89). By 2015, every RMB 5 of investment generated just RMB 1 of economic growth (Arase, 2015: p. 32).

This situation has compounded related crises of overaccumulation and indebtedness. Persistent export surpluses and high savings generated domestic deposits of $5.14 trillion and foreign reserves of $4 trillion by 2014 (IMF, 2019; World Bank, 2019). Collapsing domestic profitability compounded financial institutions’ struggle to find productive outlets for this capital. Perversely, indebtedness has also risen sharply, thanks to debt-fuelled stimulus spending. From 2008 to 2016, local government debt rose from RMB 5.6 trillion ($864 billion) to RMB 16.2 trillion ($2.5 trillion), while corporate debt – 60 per cent of which is held by state-owned enterprises (SOEs) – grew from $3.4 trillion to $12.5 trillion between 2007 and 2014 (McMahon, 2018: Chs. 2, 3).

BRI to the rescue

For the Communist Party of China (CPC), whose legitimacy rests heavily on continuous economic growth, these structural problems within the economy represent an existential crisis. The BRI is intended to address these issues by stimulating external demand for Chinese goods, services and capital.

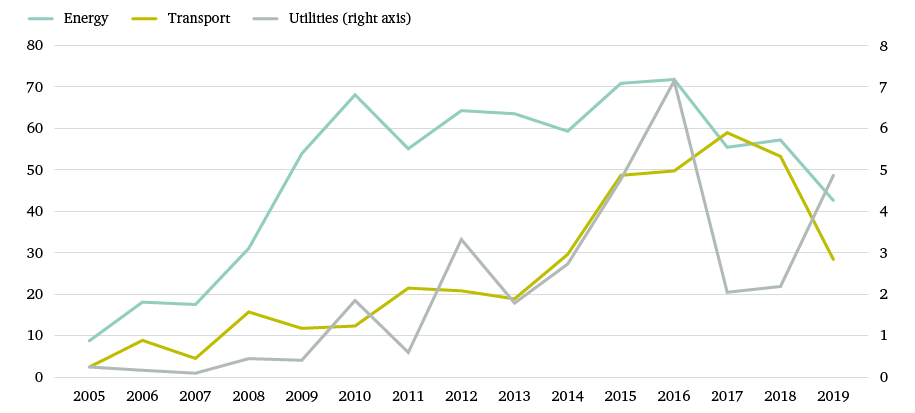

Externalizing domestic problems is a well-worn Chinese strategy. In 2000, Beijing’s ‘Go Out’ policy encouraged SOEs facing dwindling domestic resources and markets to seek opportunities overseas – which oil companies and hydropower dam-builders had already been doing. The GWDC spurred road- and rail-building companies to follow suit, followed by firms in the energy, logistics and other infrastructure-related sectors, generating steady increases in overseas investment and contracting (see Figure 1). The BRI simply scales up this strategy, repackaging and rebranding many existing projects and supporting new ones.