Delivering on climate goals will require a rapid halt to deforestation, and reforestation and afforestation at scale. But it will also require a secure and sustainable supply of minerals and materials for green technologies and sustainable infrastructure. Many of these commodities are found in critical forest landscapes, placing forests at increased risk as demand for minerals increases. This paper explores the mining sector’s impacts on forests, and the potential for ‘forest-smart’ mining policies and practices to support deforestation-free mineral supply chains.

4. Forest-smart approaches

There are several areas of opportunity to better address the impacts of mining on forests. These range from interventions that directly address forest risks and impacts, to those that support the wider conditions for forest-smart approaches and the wider transition to more sustainable, zero-carbon mining and minerals supply chains. This section signposts these areas of opportunity at country, company and sector level.

Country level

Effective governance remains the first line of defence against mining-induced forest loss and degradation. Ensuring that existing legislation and regulations are enforced is crucial, yet this remains a real challenge for many countries with limited resources, weak institutions and wavering political will, particularly where environmental protection and climate commitments are perceived as being in opposition to urgent economic development needs. The full value of forests in socio-economic and ecosystem terms is rarely recognized or factored into decision-making around the sector. Where conflicts between protecting forests and supporting mining are evident, high-value mineral resources tend to win out.

Mining and forest governance frameworks

Where mining presents forest risks, a reassessment of the policy and regulatory frameworks that guide the sector is warranted. These frameworks should address the mining sector’s forest impacts (and the emissions and biodiversity implications of those impacts) throughout the project cycle. Particular attention should be paid at the beginning and the end of the project cycle, where some of the greatest opportunities for forest protection, reforestation and afforestation are likely to arise. Bilateral donors and MDBs should explore how their policy and technical assistance can help.

As noted in Section 2, forest-smart approaches will be most effective when they are designed into projects from the outset. Relatively few large mines came online in the years following the commodities price crash of 2014, and those that did were often in ‘safe haven’ OECD jurisdictions. More recently, the development of mega-mines such as the Simandou iron ore project in Guinea has resumed, and despite relatively low exploration budgets, investor interest in ‘rest of the world’ locations (ex-Canada and Australia) is increasing, including in many forest-rich developing countries such as the DRC and Ecuador.41

Declining ore grades across the sector may lead to an expansion in mining and, in turn, the scale of land-use change and forest impacts. Such declines may also incentivize exploration and mine development in forest landscapes where there is a prospect of discovering and developing higher-grade ores. This suggests the need to review regulatory frameworks and licensing practices for new mines in forest landscapes, including strengthening ESIAs and ensuring that the value of forests is recognized, and that forest risks (and the full costs of avoiding, minimizing, restoring and offsetting them) are internalized in economic assessments. It also suggests the need for higher-level, strategic impact assessments that can coordinate ESIAs in mining and other sectors, and that can support integrated approaches at landscape, national and regional level.

Where mines have been in operation for decades, and where they were not designed with forest preservation in mind, opportunities to implement tools at the upper end of the mitigation hierarchy will naturally be limited, as well as more expensive and technically challenging. However, the decommissioning, rehabilitation and restoration of mine sites may still present significant opportunities for reforestation and afforestation, and in some instances the opportunity to repurpose mine sites for alternative socio-economic uses. Many large-scale mines are due to be decommissioned in the coming decades, yet the forest potential of mined land does not typically feature in minerals governance regimes where these relate to mine closure requirements. The regulatory and policy regimes that guide the mining sector should consider the forest potential of mined land and how locally appropriate reforestation or afforestation measures could be incorporated into the design of mine closures.

National climate commitments and SDGs

Situating mining sector development within the wider context of national climate and sustainable development planning is crucial. Moving beyond project and sector approaches will be particularly important where the indirect and cumulative impacts of mining are concerned. Such approaches will require the coordination and financing of integrated, landscape-level planning, potentially through REDD+ and other forest finance mechanisms where locally appropriate. Securing the requisite political commitment for such approaches remains challenging, especially where the economic value of forests appears relatively low compared to that of mineral resources. NDCs and long-term national emissions reduction strategies to 2050 can help reinforce the value of forests, and provide a clear mandate for governments to avoid mining-linked forest loss and degradation, as well as setting targets for reforestation and afforestation. National sustainable development plans may also help raise awareness around the varied ecosystem services and socio-economic roles that forests play, and the value of protecting and investing in them. Key questions include the following:

- What is the likely impact of mining and its associated infrastructure on the delivery of NDCs and long-term strategies to 2050, given the sector’s emissions (including those associated with deforestation and forest degradation)?

- Could climate targets for the mining sector – ensuring no net loss of forest carbon or ensuring net gain, alongside the wider decarbonization of mining activities – be incorporated within NDCs and national sustainable development plans?

- What policy and regulatory frameworks (particularly those relating to minerals and forest governance) and institutional capacities are required to implement such commitments at national and subnational level?

- Where are the investment gaps for forest-smart mining and for NDC and SDG delivery more broadly, and where are the entry points for companies and private sector investors, including through REDD+ and emerging green and forest finance mechanisms?

Countries with a high dependency on mining and a high vulnerability to forest impacts would benefit from national roadmaps for more sustainable mining. Some of these countries, such as the DRC, Guinea and Zambia, account for a significant or growing share of global production of certain minerals. Potentially, these countries have the international profile to become model examples of forest protection through the integration of land-use change and forest impacts into mining policy. At both national and subnational levels, integrated planning and enhanced monitoring can help minimize forest loss and degradation resulting from mining and economic drivers. Such processes may also support jurisdictional approaches to forest finance, which may help address any residual forest impacts, and aggregate these impacts into REDD+ and other mechanisms with the potential to attract private as well as public finance.42 Where critical forest landscapes overlap national borders, as in the Amazon, West Africa and the Congo Basin, for instance, collaborative approaches may be required to monitor mining activity and safeguard forests both within and between jurisdictions.

Company level

Companies are facing increasing demands from their shareholders and other stakeholders to disclose climate-related risks under the TCFD, and to set out how they will transition to a Paris-aligned business model. Demonstrating credible progress will be important to the mining sector’s continued social licence to operate. Emissions relating to deforestation are not part of standard climate disclosures under the TCFD, and mining companies have yet to draw direct links between their climate commitments and their forest impacts at the operational level. Better understanding of the sector’s forest impacts and associated emissions will be crucial to effective investor engagement. Assessments should incorporate both the loss of forest carbon stocks due to mining and linked infrastructure and the gains through reforestation and afforestation. The Greenhouse Gas Protocol is developing standards and guidance for corporate reporting of land-use change and carbon removals, which may assist in this.43 Mining and consumer companies should also consider aligning offsets with their impacts, and investing in forests in the country or region of operation.

Progress on the disclosure of impacts on biodiversity and other areas of natural capital, such as land and water, lags by comparison. Where particularly valuable or vulnerable ecosystems are concerned, the relative impact of mining on biodiversity may be far greater than its impact on climate change. Yet incorporating biodiversity into policy development and decision-making at the corporate level remains difficult, given the bottom-up nature of assessments, the context-specific nature of impacts, and the relative absence of reporting frameworks for nature-based disclosures. Momentum for the development of both climate- and nature-related financial disclosures is now growing rapidly, particularly in the EU,44 and a Taskforce for Nature-related Financial Disclosures (TNFD) is being developed ahead of COP26 by a coalition of NGOs, banks and governments.45 Where the economic value of carbon offsets is relatively higher than that of biodiversity offsets, there may be opportunities for REDD+ and other forms of forest carbon finance to generate revenue streams that contribute to the protection of local ecosystems and the delivery of biodiversity targets. Such approaches may also help ensure that forest impacts are addressed at project and jurisdictional level, rather than offset elsewhere.

Wherever mining has an impact on forests, the principles of good corporate policy should include clear commitments to no net loss of forest cover, no net loss of biodiversity, and net-zero GHG emissions (or even net removals, for example through reforestation and afforestation).

Wherever mining has an impact on forests, the principles of good corporate policy should include clear commitments to no net loss of forest cover, no net loss of biodiversity, and net-zero GHG emissions (or even net removals, for example through reforestation and afforestation). The development of integrated frameworks for assessing climate, forest and other impacts could aid assessment of the mining sector’s progress against such commitments in a more comprehensive way. With most mining companies accepting responsibility for direct forest impacts, and many now reporting and setting targets for scope 1 and 2 emissions, there is already a solid foundation on which to build the links between forest impacts at project level and associated emissions at the climate policy level. One obvious entry point is the incorporation of land-use change and net forest carbon losses/gains in GHG reporting. As companies begin to address their scope 3 emissions, there should also be scope to incorporate indirect forest impacts, such as those relating to infrastructure, and to consider the partnerships and mechansims that would be required to address them.

Sector level

Analysis of the concentration of supply and demand in certain mineral markets and each country’s vulnerability to forest impacts could help identify supply chains and countries in need of further attention. A 2014 paper by Chatham House found that most minerals production (by volume) is concentrated in just 11 countries: four OECD countries (Australia, Canada, Chile and the US) and seven emerging markets (Brazil, China, India, Indonesia, Peru, Russia and South Africa). For some supply chains, this concentration of production is pronounced: Australia and Brazil account for more than 70 per cent of global iron ore exports, the DRC for more than 80 per cent of cobalt exports, and Chile for more than one-third of copper exports. Among the developing countries that have received large-scale greenfield mining investments in recent years, only Zambia and Guinea were projected to become ‘major’ producers providing more than 5 per cent of world supply (for copper and iron ore respectively).46 Several of the major producers, as well as Zambia and Guinea, are among the highest-risk producer countries for forest impacts.

With OECD companies and Chinese enterprises accounting for most global mining investment, efforts to address mining’s forest impacts will need to resonate with a wide range of stakeholders. While this paper focuses on the options for companies and countries in terms of reducing forest impacts, and for investor and consumer engagement to encourage this, it acknowledges the limitations of such an approach. For SOEs and more strategic actors, the disclosure and management of mining’s forest impacts (alongside wider land, water, climate and biodiversity impacts) will likely be affected by more direct mechanisms, including the development of legislation, regulation and case law, and by the implementation of standards and mechanisms that affect access to finance (see Box 2). There is also a need to engage smaller, ‘junior’ mining companies that explore for, discover and develop mineral deposits in the earliest stages before selling them on, as such firms do not have the same capacities as the major miners. Both cases reinforce the need for robust policy and regulatory frameworks in host countries and markets, and for the institutional capacity to enforce them.

Box 2: China’s role in global mining and minerals governance

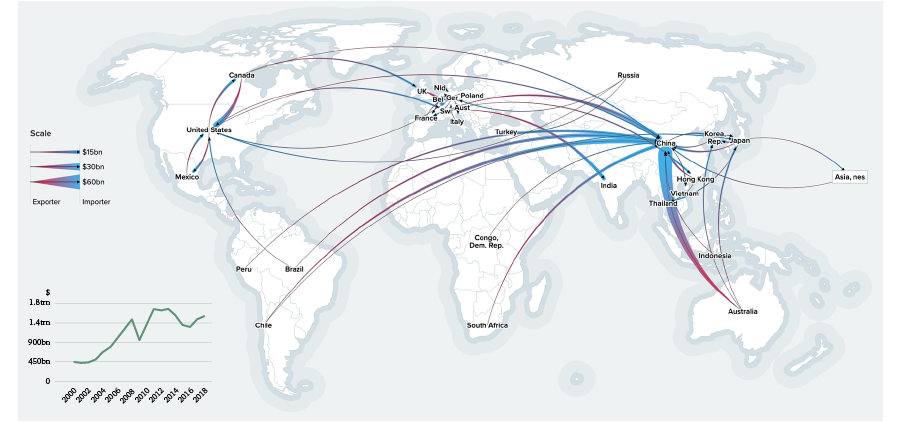

Few challenges in the mining sector can be addressed without China’s engagement. Global metals and minerals trade almost doubled in weight – from 1.8 billion tonnes to 3.5 billion tonnes – between 2000 and 2018, and quadrupled in value from $450 billion to $1.5 trillion over the same period (see Figure 3).47 China’s rising demand was the primary driver of this growth, and was reflected in the emergence of sizeable trade flows of iron ore from Brazil, nickel from Indonesia and the Philippines, and copper from Chile, among others. China now accounts for around half of all metals and minerals trade and consumption, as well as being a major minerals producer in its own right, particularly of rare earth elements (REEs). As the world’s largest producer of renewable energy and other clean technologies, China is importing growing volumes of the metals and minerals required to manufacture them. Long-standing concerns about security of supply have driven significant Chinese investments in overseas mining projects, including cobalt mines in the DRC, copper mines in Zambia, and bauxite and iron ore mines in Guinea.48

While environmental governance of the mining sector within China has strengthened, discussion of the sector’s climate impacts remains limited. Since the 2000s, new environmental regulation has been implemented and environmental impacts have become a factor in financing. For domestic finance, the introduction of the China Banking Regulatory Commission (CBRC)’s Green Credit Guidelines in 2007 created a voluntary framework for ESG reporting. For foreign direct investment (FDI), guidance for outbound investments in the mining sector and due diligence guidelines for responsible minerals supply chains have been developed by the China Chamber of Commerce of Metals, Minerals & Chemicals Importers & Exporters (CCCMC).49 Guidance on forest impacts has focused on soft commodities, particularly palm oil and rubber.50 Chinese mining companies increasingly consider ESG reporting part of good risk management and a precondition for access to finance, but reporting remains voluntary and does not typically include GHG emissions or the emissions associated with forest impacts.

China has also taken a leading role in the development of green finance. China’s central bank – the People’s Bank of China (PBC) – established green finance systems within China and put green finance on the G20 agenda in 2016. China’s green finance market has grown to become the world’s largest, yet there remain concerns that emerging green finance mechanisms lack clear definitions and metrics of success. They are often designated by sector – such as electric vehicles or batteries – with the aim of increasing capital allocation to green sectors as well as supporting China’s economic restructuring towards lower-emission, higher-quality growth. According to the PBC’s 2018 national report, the standards, metrics, disclosure and accreditation required for green finance products are still in development. So, too, are the related policies for overseas investment, including in countries involved in China’s Belt and Road Initiative (BRI).51 Ongoing efforts to harmonize sustainable investment and finance standards for the BRI, including through indicators of company ‘climate performance’ such as emissions reporting and shadow carbon pricing, may help in this regard.52 Efforts to address life-cycle emissions and the impacts of China’s green sectors and their mineral inputs will be crucial to ensuring that emissions and other environmental impacts are not simply outsourced along China’s supply chains.

Engagement with the concept of green supply chains may also help address the mining sector’s forest impacts. Since the 2000s, Chinese research and policy dialogues have expanded their focus from green production and procurement within government, to green public production and consumption, and most recently to green life cycles and supply chains. The China Council for International Cooperation on Environment and Development (CCICED) began exploring the use of green supply chains almost a decade ago, and the report of its taskforce on China’s role in greening supply chains in 2016 cited evidence of pollution from Chinese-operated copper mines in Peru and Myanmar causing severe environmental and social impacts. It noted that such impacts can undermine the social licence of companies to operate and can damage China’s reputation as a trade and investment partner. It recommended greater engagement with international guidelines for sustainability in the mining sector, the development of incentives for compliance with standards such as those of the CCCMC, and the scaling up of recycling to reduce primary demand.53 The CCICED’s attention has now turned to zero-deforestation supply chains, including those for beef, soy, palm oil, and pulp and paper. The consideration of mineral supply chains by the CCICED and other advisory bodies could raise the profile of mining’s forest impacts, and encourage the development of green mineral supply chains.

Source: Based on Chatham House research and stakeholder engagement with government, international organizations and NGOs in Beijing in late 2019.

Figure 3: Global metals and minerals trade, by value, 2018

Figure 3: Global metals and minerals trade, by value, 2018

Source: Chatham House/UN Comtrade (2020), www.resourcetrade.earth. Note: The map shows all metals and minerals trade flows over $15 billion in 2018. The inset figure shows global metals and minerals trade between 2000 and 2018, by total value traded.

Deforestation-free supply chains

Greater awareness of the forest risks associated with certain minerals and producer countries could incentivize commitments to deforestation-free mineral supply chains. Consumer concerns about the environmental and social impacts of mineral supply chains have already driven supply chain and market reforms, the best known of which relate to conflict and child labour. These include the US Dodd-Frank Act, the EU Conflict Minerals Regulation and the CCCMC’s Due Diligence Guidelines. The European Commission has now committed to developing legislation that will introduce mandatory human rights and environmental due diligence for companies across all sectors. At the same time, there are numerous commodity- and issue-specific standards and initiatives, from Responsible Steel to the Global Battery Alliance. Concern among consumer companies about the supply chain risks associated with cobalt from the DRC prompted the London Metal Exchange (LME) to develop its Responsible Sourcing Policy.54 The LME is now planning to launch a platform to trade low-carbon aluminium, in response to growing consumer concerns about the climate impact of metals.55 Apple, for example, is moving towards 100 per cent recycled products and has committed to becoming carbon neutral by 2030, including its scope 3 footprint through supply chains, which will necessitate working with suppliers.56 Apple has already supported a joint venture between Alcoa and Rio Tinto to produce the world’s first carbon-free aluminium.57

Many of the supporting conditions required for forest-smart mining and supply chains will also form the basis of a decarbonized and more sustainable mining sector.

Moving beyond single-issue standards and towards more integrated standards can help. Many of the supporting conditions required for forest-smart mining and supply chains will also form the basis of a decarbonized and more sustainable mining sector. These conditions range from comprehensive, comparable emissions reporting and the expansion of carbon pricing to the development of ‘green’ metals products and clear signals of demand for them from consumers and investors. Direct and indirect forest impacts and their emissions implications are among several variables – including life-cycle energy, carbon and water intensity, for instance – that will need to be incorporated in supply chain standards and market mechanisms if the full cost of mining and metals production is to be accounted for. The development of credible responses here, and in turn of demand and price signals, would build a clear strategic and commercial case for producer countries and companies to ensure that they develop the most sustainable and low-carbon mining sector possible.

Raising the profile of forest-risk mineral supply chains – and making this information publicly available – may encourage consumers, investors and civil society to call upon governments and companies to support more sustainable mining practices and the development of low-carbon, low-impact metals and minerals supply chains. Better understanding of the trade-offs associated with mining in forest landscapes is crucial to informed decision-making. These trade-offs will depend on a range of factors, from the types of minerals to be produced (and whether these are critical inputs for clean technologies or more widely available/substitutable commodities) to the types of forest affected (particularly where tropical forests with great significance for emissions mitigation, ecosystem services and sustainable livelihoods are concerned). Where particularly vulnerable areas are identified, the establishment of ‘no go’ zones may be the only appropriate response. While the next steps will ultimately be a sovereign decision, clear signals from investors and consumers, particularly in the major consumer markets of the OECD and China, could encourage responsible decision-making.

S&P Global Market Intelligence (2020), World Exploration Trends, March 2020, https://pages.marketintelligence.spglobal.com/rs/565-BDO-100/images/World%20Exploration%20Trends%20Report%202019-final.pdf (accessed 1 Jun. 2020).

This reflects the wider trend away from project-level REDD+ schemes towards comprehensive, government-led jurisdictional approaches to forest and land use at state or sub-state level and potentially ‘nested’ approaches, where REDD+ projects can contribute and where the risk of carbon leakage can be minimized.

Greenhouse Gas Protocol (2019), ‘New Greenhouse Gas Protocol Standards/Guidance on Carbon Removals and Land Use’, 15 October 2019, https://ghgprotocol.org/blog/new-greenhouse-gas-protocol-standardsguidance-carbon-removals-and-land-use (accessed 12 May 2020).

See, for example, Climate Disclosure Standards Board (2020), ‘Enhancing nature-related financial disclosures in mainstream reports across Europe and beyond’, https://www.cdsb.net/what-we-do/enhancing-nature-related-financial-disclosures-mainstream-reports-across-europe-and (accessed 12 May 2020).

Global Canopy (2020), ‘Bringing Together a Taskforce on Nature-related Financial Disclosures’, Global Canopy, UNDP, UNEP-FI, WWF, 21 July 2020, https://tnfd.info (accessed 31 Jul. 2020).

Kooroshy, K., Preston, F. and Bradley, S. (2014), Cartels and Competition in Minerals Markets: Challenges for Global Governance, Research Paper, London: Royal Institute of International Affairs, https://www.chathamhouse.org/sites/default/files/field/field_document/20141219CartelsCompetitionMineralsMarketsKooroshyPrestonBradleyFinal.pdf (accessed 12 May 2020).

The value of trade peaked at $1.7 trillion in 2012–13, prior to the commodities price crash. See data at Chatham House/UN Comtrade (2020), www.resourcetrade.earth (accessed 12 May 2020).

Preston, F., Bailey, R., Bradley, S., Changwen, Z. and Wei, J. (2016), Navigating the New Normal: China and Global Resource Governance, a joint report of Chatham House and the Development Research Centre of the State Council, https://www.chathamhouse.org/publication/navigating-new-normal-china-and-global-resource-governance (accessed 12 May 2020).

See China Chamber of Commerce of Metals, Minerals & Chemicals Importers & Exporters (CCCMC) (2014), Guidelines for Social Responsibility in Outbound Mining Investments, http://www.cccmc.org.cn/docs/2014-10/20141029161135692190.pdf (accessed 30 May 2020); and CCCMC (2015), Chinese Due Diligence Guidelines for Responsible Minerals Supply Chains, http://www.cccmc.org.cn/docs/2016-05/20160503161408153738.pdf (accessed 30 May 2020).

CCCMC (2017), ‘Official release of the Guidance for Sustainable Natural Rubber in Ho Chi Minh City, Vietnam’, 3 November 2017, http://en.cccmc.org.cn/news/cccmcinformation/72549.htm (accessed 12 May 2020).

PBC (2018), Summary of the China Green Finance Development Report 2018, http://www.gov.cn/xinwen/2019-11/20/5453843/files/b61d608674b04494b3ae1aef76dd7b13.pdf (accessed 30 May 2020).

China Development Bank and UN Development Programme China (2019), Harmonizing Investment and Finance Standards towards Sustainable Development along the Belt And Road, http://www.un.org.cn/uploads/20191108/bbb5cee285b9e35d7de574f4e9e4f6df.pdf (accessed 14 May 2020).

See China Council for International Cooperation on Environment and Development (CCICED) (2016), China’s Role in Greening Global Value Chains, CCICED Special Policy Study Report, CCICED 2016 annual general meeting, 6–7 December 2016, http://www.cciced.net/cciceden/POLICY/rr/prr/2016/201612/P020161214521503400553.pdf (accessed 12 May 2020).

LME (2019), ‘LME sets out responsible sourcing requirements’, press release, 25 October 2019, https://www.lme.com/News/Press-room/Press-releases/Press-releases/2019/10/LME-sets-out-responsible-sourcing-requirements (accessed 12 May 2020).

Sanderson, H. (2020), ‘London Metal Exchange plans ‘low-carbon’ aluminium trading’, Financial Times, 5 June 2020, https://www.ft.com/content/e11cdc46-fda3-445d-a323-69e4f9c6012b (accessed 5 Jun. 2020).

Apple (2020), ‘Apple commits to be 100 percent carbon neutral for its supply chain and products by 2030’, press release, 21 July 2020, https://www.apple.com/uk/newsroom/2020/07/apple-commits-to-be-100-percent-carbon-neutral-for-its-supply-chain-and-products-by-2030/ (accessed 31 Jul. 2020).

Apple has pledged to end reliance on mining and make all products from recycled or renewable materials, and has supported the development of zero-carbon aluminium. See Nellis, S. (2019), ‘Apple buys first-ever carbon-free aluminium from Alcoa-Rio Tinto venture’, Reuters, 5 December 2019, https://uk.reuters.com/article/uk-apple-aluminum/apple-buys-first-ever-carbon-free-aluminium-from-alcoa-rio-tinto-venture-idUKKBN1Y91RH (accessed 1 May 2020).