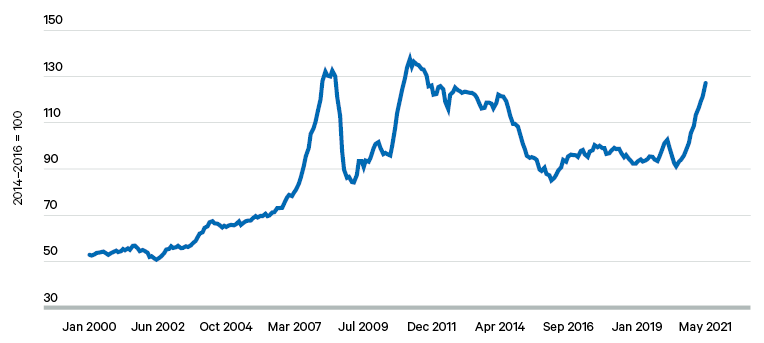

In part, global food price rises have been driven by lower-than-expected maize production in the US, dry weather in South America affecting maize and soy production, and substantial maize purchases on the part of China, which has been seeking to restore its grain reserves as it restructures its agricultural sector following the devastating 2018/19 outbreak of African swine fever.

The COVID-19 pandemic is also starting to have an impact on global food supplies, with many import-dependent countries similarly moving to rebuild national stores of staple crops including cereals, oilseeds and sugars, in the face of uncertainty and declines in global grain inventories.

Global lockdowns in early 2020 left many empty shipping containers stranded in Europe and the US, creating bottlenecks and driving up shipping prices when Western consumer demand for Asian goods recovered in the second half of the year. These impacts and port congestions have latterly spilled over to affect dry-bulk food freight as well.

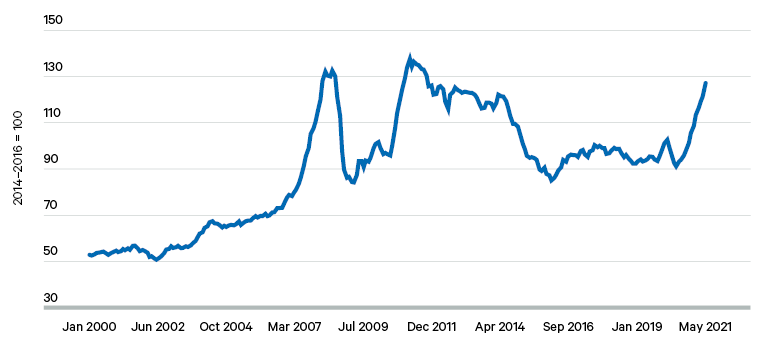

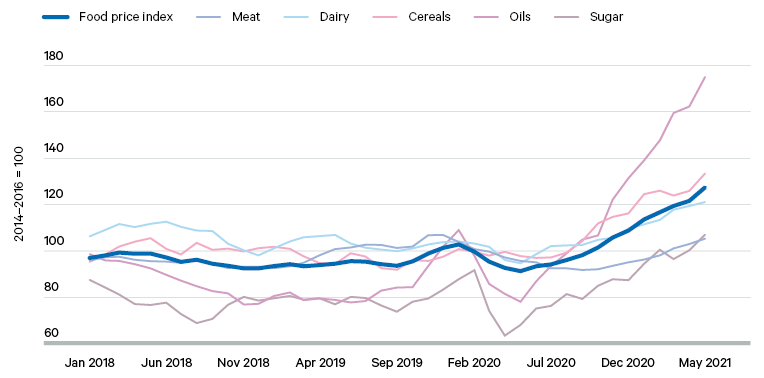

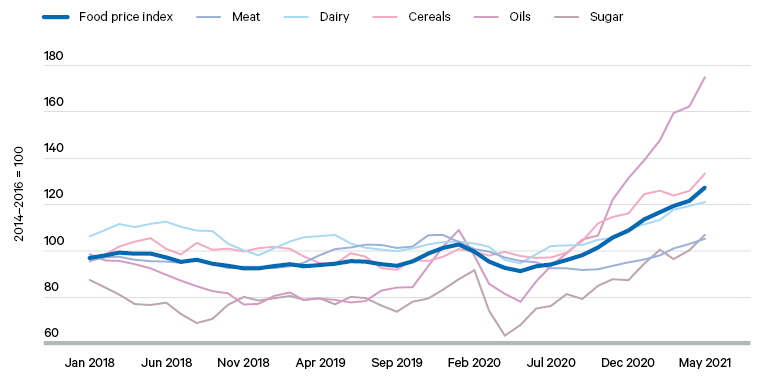

Broader factors related to economic recovery are also at play, including the impacts of stimulus packages, rising oil prices (and forecasts) and positive sentiment in equity markets, as well as a weak US dollar. Increasing demand from the biodiesel sector has also directly contributed to the rise in vegetable oil prices, as shown in Figure 16. AMIS, in its June 2021 ‘Market Monitor’, asserts that ‘[although] inflationary tendencies might appear to be driving commodity food prices higher, the evidence points more to the unique supply and demand conditions that unfolded over the past year’, with fundamental factors driving prices higher. This is likely to persist, given tight market expectations for 2021/22, but in the absence of any large production shock, international food prices could yet fall back.

Global lockdowns in early 2020 left many empty shipping containers stranded in Europe and the US, creating bottlenecks and driving up shipping prices when Western consumer demand for Asian goods recovered in the second half of the year.

Price volatility to date also remains less concerning than a decade ago. As measured by the Excessive Food Price Variability Early Warning System, a tool developed by the International Food Policy Research Institute (IFPRI), only hard wheat, rice and sugar, among the major staple commodities, experienced an excessive number of days of extreme futures prices in 2020. In the case of wheat, during the second quarter of 2020 this was largely due to unfavourable weather in Europe, whereas rice price volatility between April and August 2020 was more likely to have been related to disruptions resulting from the COVID-19 pandemic. Both commodities subsequently returned to low volatility even as prices rose, with only maize prices exhibiting excessive volatility in 2021 (in the second quarter).

Prices on domestic markets have generally been more volatile from the outset of the pandemic. In a number of Asian countries, prices of rice and wheat have risen significantly. In Syria, prices for staple foods were reported to have risen by 40–50 per cent following the outbreak of the coronavirus in March 2020; in Laos and Thailand, retail prices for rice rose by 20 per cent on average each month between January and April 2020, compared with the corresponding month in 2019. In India, Mongolia, Pakistan and Sri Lanka, increases averaging between 10 and 20 per cent were observed in the same period. On average, in mid-2020 the World Bank calculated that food price rises of at least 12 per cent were being experienced across the most food import-dependent countries in the Middle East and north Africa, sub-Saharan Africa, Latin America and the Caribbean.

Responses

Many governments have moved to introduce measures to encourage and facilitate trade, for example through temporary tariff reductions, VAT exemptions and accelerated customs procedures. Some governments have adopted measures to facilitate the continued distribution of both inputs and agricultural produce, such as the ‘green channels’ introduced in China, and the expedited border crossing checks, or ‘green lanes’, introduced in the EU. The UK government and major supermarkets introduced the ‘Vulnerable Supply Chains Facility’, to strengthen retailers’ global supply chains by supporting workers in developing countries during the pandemic. Measures have also been introduced to provide direct support to smallholders: in South Africa, for example, the Department of Agriculture, Land Reform and Rural Development established an additional assistance programme for small-scale farmers; in Brazil, an emergency credit line has been set up specifically for smallholders; in Germany, monthly grants are being issued to small and medium-sized enterprises (SMEs) to cover their operating costs; and in Côte d’Ivoire, the government has introduced a public guarantee scheme for credit provided to informal businesses.

Several major IGOs have established programmes specifically targeting SMEs and smallholders and their access to key inputs, markets and credit. The International Fund for Agricultural Development, for example, has established a multi-donor Rural Poor Stimulus Facility with the specific aim of providing basic inputs to crop, livestock and fishery producers, facilitating continued market access, offering financial support, such as flexible debt repayment plans, and facilitating the use of digital services to improve producers’ access to key weather and market information.

In comparison, the FAO has launched a four-year programme to boost resilience to the crisis among smallholders, including through insurance and credit schemes, cash transfers and technical support.

IGOs have also launched a range of response and recovery programmes to minimize interruptions to global, national and local food trade networks. Another FAO initiative launched in response to the crisis is a four-year trade facilitation project which will include a ramping-up of regular trade policy assessments, the convening of multi-stakeholder forums to encourage trade policy coordination and discourage distortive trade measures, and the provision of technical assistance in areas such as food safety control systems and the digitization of trade documents and bureaucratic procedures.

Retail, markets and provisioning

Impacts

The temporary closure of hospitality businesses in many regions around the world has harmed the seafood and livestock industries, but government support measures have dampened losses. Seafood producers have experienced a dramatic fall in demand with the shutting down of restaurants. Indeed, global shrimp production was expected to fall by 30–50 per cent in 2020 compared with 2019.

In major livestock-producing countries like the US, the slumping of demand from the restaurant and food services sectors has resulted in significant waste at the farm gate, with producers dumping milk and eggs – something that also happened in the UK – and, in some cases, culling livestock herds, to get rid of excess supply.

The temporary closure of hospitality businesses in many regions around the world has harmed the seafood and livestock industries, but government support measures have dampened losses.

Global dairy exports were, by June 2020, predicted to fall by 4 per cent relative to 2019 volumes, marking the most significant year-on-year reduction in three decades.

Horticultural producers have also been forced to dump huge volumes of produce in response to the closure of hospitality and food services.

Responses

A number of governments around the world have introduced policies to generate demand and mitigate oversupply in the wake of widespread hospitality closures. In the US, the federal Department of Agriculture ramped up the public procurement of fresh produce, dairy and meat products to compensate for the loss of demand from the hospitality sector. In the EU, the European Commission allowed governments to offer private storage aid to those in the meat and dairy supply chains. This will allow producers to claim support for the storage of products such as cheese, butter and beef for periods of two to seven months, with the aim of avoiding oversupply on European markets and subsequent drops in prices.

A handful of other countries, including Egypt, India and Saudi Arabia, also ramped up public procurement and stockpiling as a means of supporting producers and protection against food shortages.

Economic access

Impacts

Food access, i.e. the capacity of individuals to acquire the foods needed for a nutritious diet, has continued to be the dimension of food security most affected by the COVID-19 pandemic and related restrictions – particularly through the impacts of income losses and macroeconomic shocks, although isolation and shielding restrictions have also played a part. However, it is not yet clear where the converging impacts of COVID-19’s economic effects, rising food import bills and other supply and demand factors are most likely to result in deteriorating food security outcomes in the short term, nor the degree to which potential price increases will transmit to markets serving the marginally food-secure.

Nonetheless, rates of household poverty and nutrition insecurity have risen across many countries, primarily as the result of lost employment. Although global cereal production has remained strong, the effects of a global recession and of the loss of employment – together with a significant reduction in remittances – among low-income households and informal workers are expected to lead to reduced nutrition security as economic access to nutritious diets falls – a trend also observable in the UK., Even before the pandemic, it is estimated that around three billion people worldwide were unable to afford a healthy diet in 2019. By April 2020 the WFP was warning the UN Security Council that it would be projecting that 130 million additional people would be facing acute food insecurity by the end of 2020, nearly doubling the total from 135 million in 2019 to 265 million in 2020.

The World Bank has been conducting high-frequency telephone surveys to monitor the impacts of the pandemic in developing countries. These show that as of December 2020, on average one-half of all households in the poorest countries had an adult skipping at least one meal due to lack of resources in the 30 days before the survey.

Furthermore, in 16 per cent of households across all surveyed countries, at least one adult had gone without food for a full day in the week before the survey. The extent to which this is directly attributable to the impact of the COVID-19 pandemic is not clear, but in almost all countries, food insecurity is more frequently reported in households that had suffered job losses following the pandemic. The coronavirus has proved to be a compounding factor to conflicts, extreme weather events and pests in driving global food insecurity. According to the FAO, this was the case for many of the 45 countries assessed as being in need of external food assistance at the end of 2020 (up from 42 at the end of 2019).

Globally, 148 million more people are thought to have experienced severe food insecurity in 2020 than in 2019. The prevalence of moderate or severe food insecurity in 2020 was 10 per cent higher among women than men (up from 6 per cent in 2019). In total, the number of people facing chronic hunger increased (by around 120 million) to 10 per cent of the global population – the first significant change in the last five years.

Responses

By April 2020, 181 countries had either introduced social protection programmes to support vulnerable households, or had announced plans to do so. In India, for example, the government made an early announcement of a $22.6 billion relief package which included both cash and food transfers.

Among the 181 countries, 26 country programmes were specifically aimed at informal workers. In the Philippines, for example, temporary employment opportunities in sanitation services were offered to informal workers, and in Indonesia the government provided subsidized vouchers to workers in this category to support upskilling and reskilling training programmes.

MDBs and IGOs are working independently, in concert with each other and in collaboration with national governments in order to mitigate the effects of the pandemic on food and nutrition security. In the Democratic Republic of the Congo, the government and the World Bank are monitoring food price and consumption data in order to inform the design and roll-out of social protection and emergency response measures. In Pakistan, the World Bank is providing direct livelihood support to 18,000 households – the majority of them female-headed – in the form of kitchen garden development and extension services to support small-scale livestock rearing and agricultural activities.

The WFP has adapted existing food provision programmes to meet the needs of vulnerable households, for example through shifting school meal programmes to take-home rations, and has scaled up its emergency food distribution by 17 per cent (in comparison with 2019 levels) to meet growing demand.

The impact of the COVID-19 pandemic on global food systems

The COVID-19 pandemic is clearly contributing to new and deeper segments of vulnerability in food systems around the globe. Certain supply chains have had acute moments of significant impacts, and many communities have evidently experienced worsening food and nutrition security, largely due to income reductions associated with the deep economic crises resulting from the pandemic and at risk of being exacerbated by rising food prices. Responses that have been implemented have tended to be piecemeal rather than the result of proactive coordination across states, supply chains, or food environments, and it is likely that between 120 million and 150 million more people have become food insecure because of the pandemic. Yet the situation could have been even worse. The systemic shocks that were initially feared have not yet materialized, and there have been few significant trade disruptions. This can be largely attributed to two factors: the fact that the outbreak of COVID-19 generated a primarily demand-side shock, and the existence of plentiful global food stocks at the onset of the pandemic. Although the worst-case scenario has not materialized, it would be misguided to conclude that global food systems are resilient.