The third main type of forest tax is the timber rights fee (TRF). This was introduced in 2003 with the establishment of a process for competitive bidding for the allocation of timber rights. Initially it provided an important source of forest sector revenues for the government – 50 per cent of these revenues at its peak in 2007 – but contributions subsequently dropped to very low levels, accounting for less than 1 per cent of forest sector revenues over the following decade. This was because the majority of operating companies refused to pay as they disagreed with it being applied retrospectively. In 2017, partly as a solution to this situation, the TRF was changed from an annual to a one-off payment. By the end of 2021, most companies had agreed to this and had applied to convert their existing leases to timber utilization contracts (TUCS) that, once approved, would require payment of this fee.

The evidence from Liberia

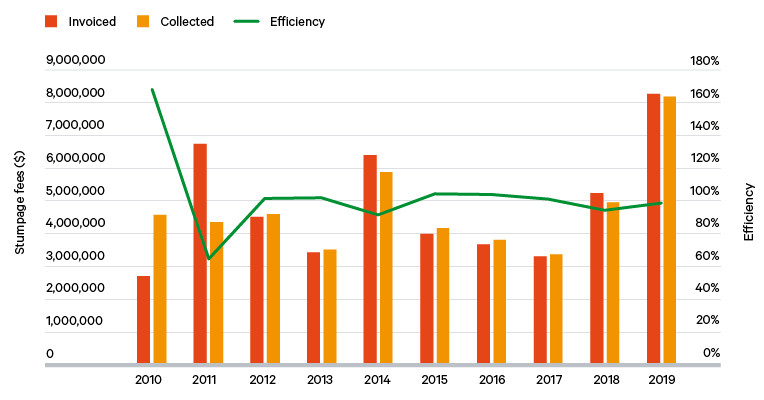

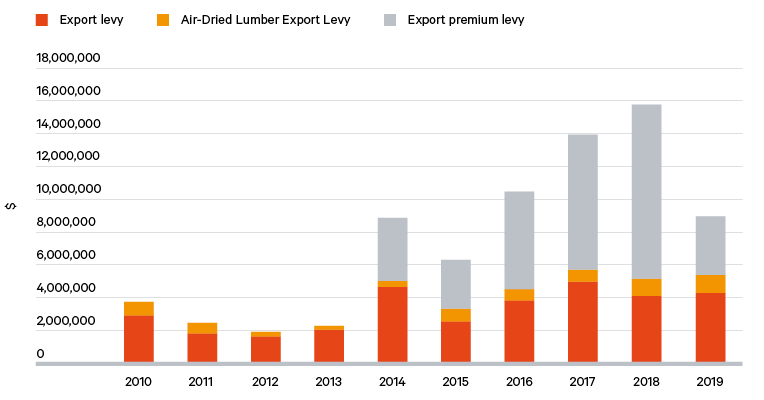

In Liberia, the current main sources of forest sector revenue are stumpage fees, land rental and export taxes; prior to 2013, the land rental bid premium was also an important source of revenue.

Unpaid forest taxes have been a persistent problem in Liberia since commercial logging was formally resumed. This restarted after the UN sanctions on timber exports from the country were lifted in 2006. These were imposed three years earlier because of the role that the timber sector had played in the civil war.

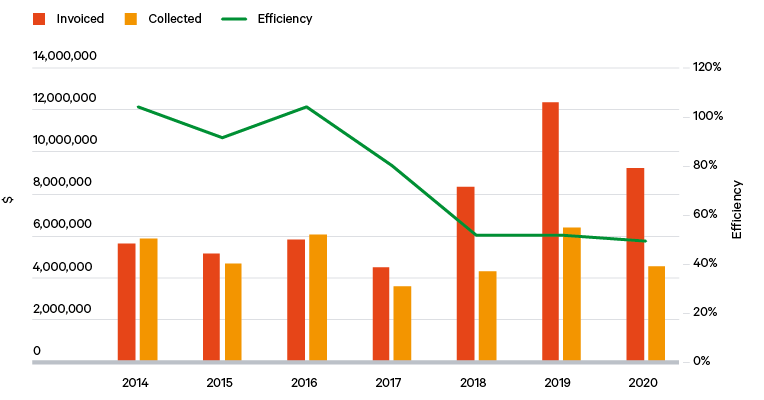

Analysis of the country’s annual EITI reports by Forest Trends indicated that over the 2007–15 period, the government collected $74 million in revenues from the sector, with $49 million in arrears.

A significant proportion of the arrears accumulated prior to 2013 was due to the non-payment of the land rental bid premium – an annual fee that had been established as part of the bidding process for forest concessions (see Table 1). The bid premium accounted for more than 70 per cent of the $49 million arrears in 2015. Companies had been refusing to pay this as they claimed that they had understood this to be a one-off fee, and it was abolished in 2013.

The government has sought to recoup these historical debts. The 2013 act that abolished the bid premium stated all arrears for this fee accrued up to the fiscal year 2011/12 were due to be paid within three years, or as agreed with the government. However, $11.7 million of these arrears were reported as outstanding as of July 2019. New payment schedules were negotiated with companies for some of these arrears (as well as those for other taxes), however, compliance with these has been reported to be low.

In 2017, legislation was passed allowing companies to write off their arrears through investments in wood-processing facilities made in the period 2016–20. However, the extent to which this mechanism has been used by companies is unclear because it has not been systematically documented. The LiberTrace report for March 2019 notes that one company was issued a tax credit and so only paid 15 per cent ($95,126) of the total land rental due, and in the 2018/19 LEITI report, two projects were reported for which a tax credit had been granted, valued at $3.9 million in total. The government also noted to the VPA Joint Implementation Committee in 2020 that two further tax credits had been issued with a total value of $5.1 million.

Tax collection rates have also worsened in recent years (Figure 3). Data from LiberTrace indicate that of the $51 million invoiced for the period 2014–20 (up to October 2020), $35.5 million in revenues had been collected, leaving $15.5 million in arrears. The bulk of this debt has been accumulated since 2018, and is mainly due to arrears in land rental fees.