In parallel with the requirement for government to share royalties with landowners, companies are required to provide benefits to communities through the establishment of SRAs. These set out the services or materials that companies will provide to communities, and these should be equivalent in value to 5 per cent of stumpage fees.

Over the last decade, implementation of SRAs has been reported to have improved markedly, the result of reforms instigated by the VPA process, although data is limited. Based on unpublished data compiled by Civic Response, IPE Triple Line reported a high level of compliance by companies with the requirement to establish SRAs during 2017–19. Across 11 of the 36 districts in the high forest zone, 141 timber companies (representing three-quarters of those operating) had done so by the end of this period.

The evidence from Liberia

In Liberia, the land rental fee is disbursed to the subnational level (counties) and to forest communities. In addition, holders of forest concessions – forest management contracts (FMCs) and timber sales contracts (TSCs) – are required to pay a fee to affected communities as part of their social agreements.

Subnational counties receive 30 per cent of the land rental fee. This money is divided equally between each county and paid into County Forestry Development Funds. However, there is little publicly available information on these disbursements or on how counties use these funds. The EITI report for the financial year 2018/19 states that the government ‘did not report to us the total amount being paid to sub-national entities’.

A further 30 per cent of the land rental fee should be paid into a dedicated account for redistribution to communities living near to forest concessions. The account is managed by the National Benefit Sharing Trust (NBST) to which Community Forestry Development Committees (CFDCs) submit applications for community projects.

The first time such payments were made was in 2015 and in the period up to 2017, a total of $2.6 million was paid into the NBST. A further payment of $200,000 was made in 2021.

The total funds paid remain far short of the 30 per cent of the land rental fee received that is due to communities. Forest Trends estimated that just one-third of the funds due had been transferred to the NBST, leaving a shortfall of more than $5 million. Communities are also not receiving all the revenues they are due because of the arrears in land rental fees. According to the government, in 2020, $3.8 million was owed in area-based fees, of which $1.14 million was due to communities.

To address the failure of the government to transfer revenues as required by law, the government, forest communities and civil society agreed on a new system for disbursing funds in September 2021. This will entail the establishment of an escrow account into which the land rental fee will be paid, rather than directly to the government. From this account the proportion due to communities must be paid to the NBST within 24 hours. In addition, as a longer-term solution, an amendment to the National Forest Reform Law of 2006 has been proposed that would enable companies to pay the 30 per cent community share directly to the NBST.

Of the land rental fee for use of community forests by third parties, 55 per cent is due to communities.

Logging in community forests has become an important source of timber. Data from LiberTrace reports show that community forest management agreements (CFMAs) accounted for less than 5 per cent of log production in 2014, and over 50 per cent by 2019. The extent to which the revenues due from such activities are being paid to communities was not explored in this research, but reports from civil society indicate that to date there has been weak implementation of this provision.

With respect to the requirements for benefit-sharing by companies, the holders of timber concessions (FMCs or TSCs) are required to enter into social agreements with communities bordering their concession areas. These agreements include both cash and non-cash benefits such as road maintenance and social infrastructure. For the cash benefits, a minimum of $1 per cubic metre of timber harvested should be paid into a dedicated account held by the company for disbursal to community representatives.

Publicly available data on these agreements are limited. In LiberTrace, the existence of social agreements for a concession is registered, but the agreements themselves are not publicly accessible; and the Forestry Development Authority’s website has no information on social agreements.

That said, a list of signed agreements made by companies is given in the EITI reports. In recent years, these latter reports have included more detailed data on the payments being made, as reported by companies. Such reporting began in financial year 2012/13, and since 2016/17, the payments have been disaggregated by type (Table 4).

|

|

|

|

|

|---|

|

|

|

|

|

|

|---|

|

2012/13

|

–

|

–

|

–

|

–

|

52,271

|

|

2013/14

|

–

|

–

|

–

|

–

|

0

|

|

2015/16

|

53,221

|

750,000

|

0

|

581,400

|

1,384,621

|

|

2016/17

|

114,450

|

0

|

0

|

0

|

114,450

|

|

2017/18

|

0

|

0

|

21,840

|

12,073

|

33,913

|

|

2018/19

|

33,000

|

0

|

11,000

|

14,000

|

58,000

|

Source: LEITI annual reports, https://www.leiti.org.lr/publications/document-type/leiti-reports.

Note: Mandatory payments are those to be made under social agreements with communities, these include the cubic metre fee.

How these payments relate to companies’ obligations as set out in their social agreements is not clear. The National Union of Community Forestry Development Committees (NUCFDC) has reported that implementation of these agreements is weak. From their monitoring visits to 11 communities with active social agreements in 2018–19, the required cash payments had only been made for one-third of the agreements.

The evidence from the Republic of the Congo

In the Congo, the area tax is disbursed to subnational departments. Regarding benefit-sharing arrangements for communities, companies are required to establish social contracts and also to pay into a local development fund.

With respect to the area tax, 50 per cent of this should be allocated to the country’s subnational departments. The funds should be paid into a special account held by the treasury and then split equally between the departments for the purposes of development.

However, there are limited publicly available data on these revenues. In the EITI reports, for the years 2016 and 2019, it is stated that no transfers were made into this account, while for the years 2017 and 2018, the government did not provide any data on the amounts paid into this fund. Based on the area fees reported to EITI, however, the total amount that should have been paid for the four years is approximately $7.8 million (Table 5).

|

|

|

|---|

|

|

2,625,473

|

1,312,737

|

|

|

3,007,531

|

1,503,765

|

|

|

5,764,929

|

2,882,464

|

|

|

4,254,693

|

2,127,346

|

|

|

15,652,625

|

7,826,313

|

Source: Republic of the Congo EITI annual reports, 2016–19, https://eiti.org/republic-of-congo#eiti-reports-and-other-key-documents.

These typically entail the construction of infrastructure such as roads, hospitals or schools. Under the 2000 Forest Law, these agreements were made between companies and the government, but this was changed under the 2020 Forest Law and negotiations are now required to be held directly with communities.

In addition, concessionaires are required to establish local development funds to support community projects, through payment of a royalty. This was previously only required for certain concessions (13 of the 51 concessions operating in the country) but since the 2020 Forest Law it has become mandatory for all. As of early 2021, just eight local development funds had been established.

Since 2017, the EITI reports have included data on the ‘social payments’ made by companies, as reported by these companies (Table 6). How this relates to compliance with their legal requirements is not clear because the agreements are not systematically published. NGOs have reported this to be weak, however, with many communities receiving few benefits either from social contracts or local funds.

|

|

|

|

|

|---|

|

|

|

|

|

|

|

|

2017

|

2,212,794

|

41,800

|

264,542

|

0

|

2,519,136

|

|

2018

|

1,746

|

0

|

326,063

|

0

|

327,808

|

|

2019

|

320,706

|

402,295

|

97,580

|

0

|

820,581

|

Source: Republic of the Congo EITI annual reports, 2017–19, https://eiti.org/republic-of-congo#eiti-reports-and-other-key-documents.

Key findings

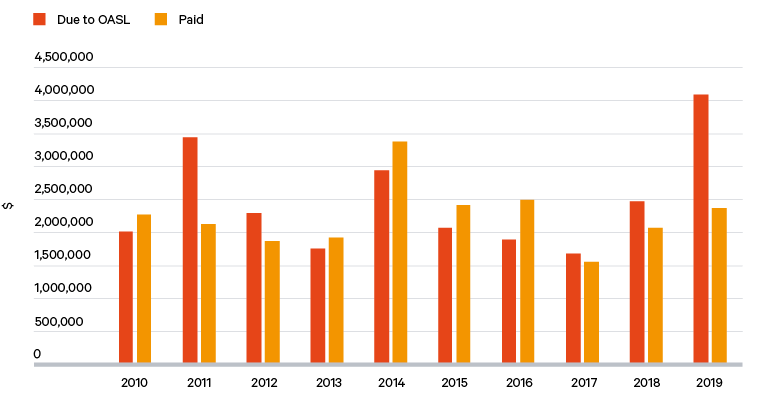

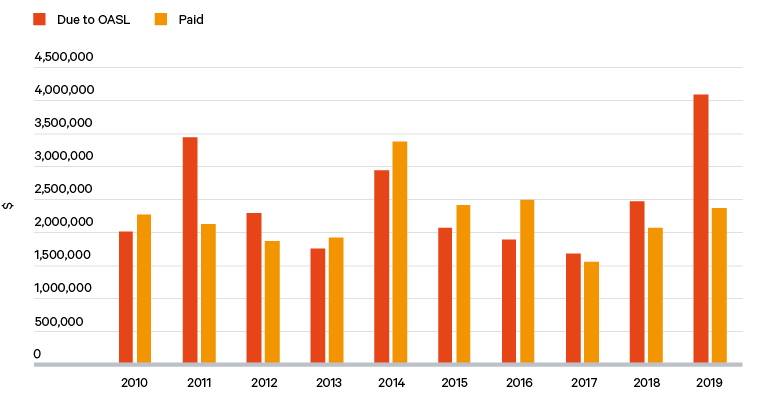

The extent to which revenues are being disbursed to subnational institutions, as required by law, is opaque. In Liberia and the Congo, there is little information available on whether revenues are being paid into subnational development funds. In Ghana, disbursement of revenues to the OASL is taking place largely as required, although there remain historical arrears. Further investigation is required to determine whether the OASL is disbursing the funds to the beneficiaries as required.

There is more transparency regarding benefit-sharing arrangements with communities and the available evidence suggests that compliance is improving on the part of both government and companies in Ghana and Liberia. Increased access to fiscal data in concert with reforms of the policy mechanisms for benefit-sharing have been helping to drive the improvements seen. In the Congo, compliance remains weak but recent reforms are expected to help improve compliance.

Clearly, the improvements seen remain far from adequate and communities are still owed significant revenues. Communities are losing out not just because of the failure to disburse revenues, but also because the revenues due are not being collected. The latter is also impacted by government decisions to provide tax breaks, which in both Liberia and the Congo, have amounted to millions of US dollars.