China’s lending to Africa peaked in 2016 and has since been in decline. While these loans have contributed to Africa’s debt vulnerability, they are not the only factor. China is a critical component in finding effective solutions to African debt distress.

Public debt has doubled in Africa since 2010, reaching 65 per cent of GDP in 2022. Creditors have also diversified: by 2022, Paris Club members and non-members (notably China) accounted for 37 per cent and 17 per cent, respectively, of African countries’ total external debt. Looking more broadly, combined private and public external debt in Africa increased more than fivefold between 2000 and 2020 to $696 billion – of which Chinese lenders accounted for 12 per cent.

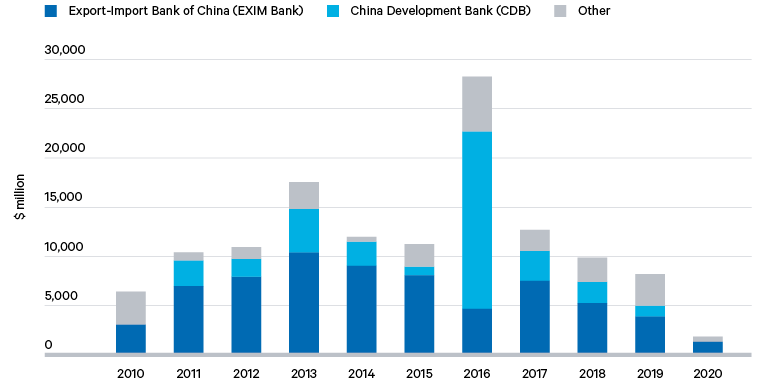

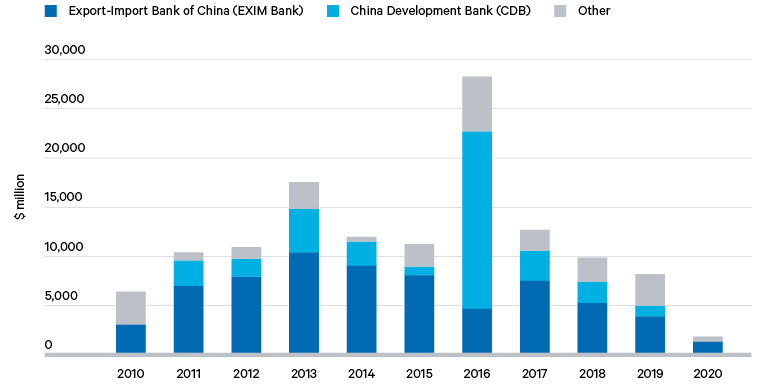

Over the last 22 years, Chinese finance has contributed to an infrastructure boom in many African countries. However, the pace of lending slowed after 2016 as commodity prices and GDP growth rates declined, with Chinese loans to African governments dropping from a peak of $28.4 billion in 2016 to $8.2 billion in 2019, and falling again to just $1.9 billion in 2020 (although the latter in part reflected the exceptional circumstances of the pandemic). China has built a large stock of debt across the African continent, and now faces the challenge of managing these investments amid economic woes linked to the legacy of the COVID-19 pandemic and the war in Ukraine, which have heightened the prospects of default in some African nations. The IMF and World Bank consider 22 low-income countries in Africa to be either in debt distress or at high risk of debt distress as of 30 November 2022. The IMF defines debt distress as when a country is experiencing difficulties in servicing its debt.

In considering policy responses to African debt distress, it is important to avoid slipping into narratives of predatory Chinese ‘debt-trap diplomacy’ and fears of asset appropriation, which minimize the agency of African actors in shaping the nature and impact of Chinese investment. These perspectives also disregard the marked heterogeneity of Chinese approaches and motives. At times, Chinese investment in Africa has been implemented in an unplanned and uncoordinated manner by competing lenders with links to different elements of the Chinese state. The logic of Chinese investment has also ranged from simple profit-seeking to politically contingent geostrategic calculations, depending on location and political context.

It is also clear that the impact of Chinese debt varies widely across the continent and that Chinese loans play a critical role in only a subset of Africa’s 54 countries (and not in three of Africa’s major economies – Egypt, Nigeria and South Africa). A lack of transparency makes it challenging to unpack and quantify the total outstanding public debt stock owed to China, the extent of repayments and its composition in terms of commercial or official bilateral loans.