Aviation remains one of the most difficult sectors to decarbonize. However, with accelerating risks of climate change, the UK public is supportive of demand-management options such as limits on flying.

The aviation sector has provided significant benefits to society: not only in terms of the expansion of global trade but also in boosting people’s happiness as holidays to diverse geographies have become more affordable and accessible. The sector has also enabled people to seek work or visit family in different countries. However, the high-emitting countries of the G20 that have most benefitted from aviation have failed to deploy low-cost, low-carbon technologies with sufficient speed across all sectors of the economy, resulting in accelerating risks of climate change and threats to the quality of life for all.

Climate scientists fear that runaway climate change could occur if global temperatures increase by more than 2°C. Current global warming sits at around 1.2°C above pre-industrial levels, CO₂ and other greenhouse gas (GHG) emissions continue to remain stubbornly high, and the COVID-19 pandemic and associated lockdowns have had little impact on long-term emission reductions.

The historical lack of decarbonization action, combined with the political disdain for constraining demand for high-carbon products and energy services, has led to a growing reliance on the use of technology to remove CO₂ from the atmosphere in the future, commonly termed ‘negative emissions’. This approach embodies very significant risk. The shift away from straightforward reduction targets, towards combined reductions and removals targets, has galvanized more countries to pledge and legislate for more ambitious climate action. While this should be applauded, societies also need to step back and scrutinize proposed methods of reaching net zero, across all sectors of the economy, inclusive of aviation.

As the world wrestles with the reality of failing to decarbonize the global economy with sufficient speed, and a risky, large overshoot of carbon budgets looks increasingly likely, sectors that have historically been deemed ‘difficult to decarbonize’ are under growing pressure to develop pathways towards net zero emissions. The Intergovernmental Panel on Climate Change (IPCC) has highlighted that the level of decarbonization ambition varies across sectors, with ‘emission reduction aspirations in international aviation and shipping lower than in many other sectors (medium confidence)’.

International efforts to reduce CO₂ emissions are dangerously off track, inclusive of the aviation sector. Global aviation emissions account for around 2.5 per cent of CO₂ emissions, but a higher proportion of effective radiative forcing – a more accurate measure of the aviation sector’s impact on global warming.

Not only is the aviation sector lacking decarbonization ambition, but along with agriculture it is one of the most difficult sectors to decarbonize based solely on supply-side solutions. Many decarbonization options remain either at the R&D phase; are taking many years to be deployed within a sector with sticky, long-lasting and costly current assets; have yet to be scaled to the levels required; or have significant externalities.

This paper investigates the balance between reliance on future supply-side decarbonization (such as fuel efficiency measures and negative emissions) and demand management (reducing passenger-km flown), and also examines the role of near-term demand management in reducing the risk of reliance on future action. All within the context of a ‘fair share’ of carbon budgets for the UK’s aviation sector. The allocation of a fair share of the UK’s carbon budget to the aviation sector is quantified and discussed in section 2.4. The modelling in this paper does not consider the cost of mitigation measures and is not intended to be a lowest-cost optimization study in any way.

The remainder of this chapter highlights the possible impacts of climate change and discusses the potential for demand management in a general sense to swiftly reduce emissions. Chapter 2 presents an overview of the model developed to explore the balance between aviation supply-side decarbonization and demand mechanisms, carbon budgets (and consequently how much time is left to avert the risks of climate change), and the UK government’s Jet Zero Strategy high-ambition decarbonization scenario for the aviation sector. Chapter 2 also presents a summary of the generated scenarios from the modelling. This approach of presenting the results upfront has been adopted as a means of guiding the reader through the various scenarios.

Chapter 3 presents the various supply-side decarbonization options, sequentially questioning how much reliance and hence risk is placed on each. For the main supply-side options, an optimistic and potentially high-reliance risk scenario has been generated, alongside a lower risk, more realistic scenario. Furthermore, Chapter 3 quantifies how demand may need to change as reliance on these supply-side technologies alters. Chapter 4 then proposes a risk-minimization approach of increased demand management in the near term and considers the economic benefits of flying against the social cost of carbon as well as potential policy measures. Finally, Chapter 5 presents conclusions and recommendations.

1.1 What are the impacts of climate change that global society is trying to avoid, and how near are we to that point?

The balance between relying on future emissions mitigation and greater near-term action, such as demand-reduction measures, needs to be assessed based on the severity and time frame in which climate risks could manifest, and their likely probability of occurrence.

The emissions gap for a limited-overshoot 1.5/2°C scenario is ever widening. In late 2021 the IPCC defined various carbon budgets for a given chance of avoiding different levels of global warming. For a 67 per cent chance of staying below 1.5°C – the target set out by the Paris Agreement – the world can emit 400 gigatonnes of CO₂ (GtCO₂) between the beginning of 2020 until net zero CO₂ emissions are reached. The UN Environment Programme (UNEP) emissions gap report illustrates that to stay on course for a limited-overshoot 1.5°C scenario, global emissions would need to be 12–14 GtCO₂/yr lower in 2030 than current nationally determined contributions (NDCs) imply. Interrogation of the emissions gap shows that aggregate emissions over the 2020s would need to decline by an equivalent of more than two years of current global emissions. Net zero targets are a manifestation of this widening gap, and an acknowledgment that there is not enough time to decarbonize if demand grows unchecked.

Clearly the impacts of climate change are already a reality, as has been witnessed in recent years with increased extreme weather, flooding, heatwaves and droughts. Unless decarbonization efforts across the entire energy sector are dramatically increased, many of the worst climate impacts are likely to be locked in by 2040, and could become so severe that they go beyond the limits of what nations can adapt to. Moreover, many of the potential impacts of climate change may turn out to be conservative estimations of the risks, unless efforts are made to radically reduce emissions before 2030, as critical tipping points could be reached at lower levels of temperature increase than previously thought. The IPCC estimates that under a moderate emissions scenario (SSP2-4.5), the world could pass the 1.5°C objective in 2030. It should be noted that many of the negative emission technologies being considered under net zero targets are only likely to be deployed post 2030. As such, there may well be an overshoot in the 1.5°C temperature limit before negative emissions kick in, but by this time these tipping points may have already been triggered. This indicates the primary risk of relying on supply-side CO₂ removal technologies. It is within this climate risk context that the speed of supply-side decarbonization of the aviation sector should be assessed, and indeed the potential need for demand management.

1.2 Demand-side measures can be enacted swiftly to buy time for supply-side solutions

As citizens are increasingly impacted by climate change, they are likely to call for swifter climate action. Given that demand-side emission reductions can be implemented quickly, with little lead time, demand-side responses are likely to be the only fast-acting policy measure left at our collective disposal to avoid disastrous climate impacts. Developing demand-side policy measures that can be deployed as the climate emergency deepens will be critical to ensure there are viable mechanisms to retain future cooperative international climate action pathways:

Within the context of Russia’s invasion of Ukraine and high energy prices, the need for short-term demand management has had increased political and policy attention. The European Commission set a voluntary 15 per cent gas consumption reduction target, inclusive of encouraging households to turn down their thermostats, and the International Energy Agency (IEA) published an extensive set of least-disruptive options to reduce oil and gas consumption. As part of these demand-side recommendations, the IEA encourages EU citizens to take high-speed trains as a high-quality substitute for flying.

High oil and gas prices are already resulting in inflation-driven energy demand reduction. Consequently, there is a clear win-win scenario whereby a greater focus on the demand side could offer a means to reduce reliance on Russian fossil fuels, lower geopolitical risks and benefit citizens suffering under the cost-of-living crisis, while also reducing climate risks.

In 2022, the IPCC highlighted that the demand side has a significant contribution to make in reducing emissions; and that decent living standards can be maintained while reducing demand for high-emission goods and services:

- ‘Demand-side measures and new ways of end-use service provision can reduce global GHG emissions in end use sectors by 40–70% by 2050 compared to baseline scenarios, while some regions and socioeconomic groups require additional energy and resources. Demand side mitigation response options are consistent with improving basic wellbeing for all (high confidence).’

- ‘Decent living standards, which encompasses many SDG dimensions, are achievable at lower energy use than previously thought (high confidence). Mitigation strategies that focus on lowering demand for energy and land-based resources exhibit reduced trade-offs and negative consequences for sustainable development relative to pathways involving either high emissions and climate impacts or pathways with high consumption and emissions that are ultimately compensated by large quantities of BECCS.’

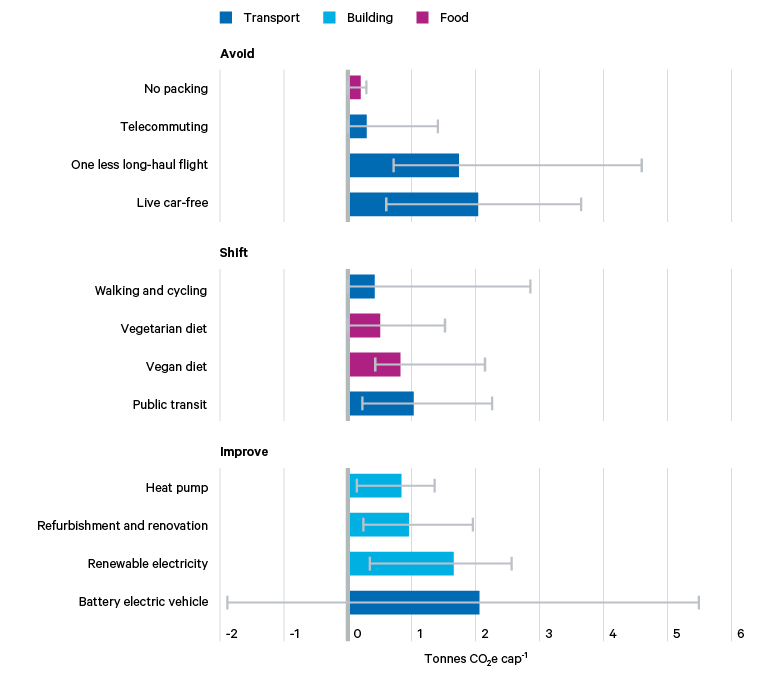

The IPCC also highlighted that COVID-19 policies led to a global decline in CO₂ emissions of around 5.8 per cent in 2020 relative to 2019, and that international aviation emissions declined by a staggering 45 per cent. The IPCC classify future emissions reduction mitigation strategies from the demand side into ‘avoid’, ‘shift’ and ‘improve’ options. As can be seen in Figure 1, one of the greatest avoid potentials for individuals comes from reducing long-haul aviation, which can save slightly more than 1.7 tonnes CO₂ per person.

To balance the severity and time frame of climate risks, and reduce the emissions gap, a near-term focus on the demand side could buy time to develop supply-side solutions, while minimizing the risks of relying on yet to be commercialized and scaled options, such as sustainable aviation fuels (SAFs), zero-emission aircraft and greenhouse gas removals (GGRs). In essence, a new framing is required – focusing on the potential of the demand side in the near term – to enable supply-side solutions to catch up, without baking in over-reliance risks on the supply side, particularly in relation to GGRs.

While undoubtedly politically challenging in any sector, the focus on demand management is gaining traction. In December 2022, the European Commission gave France the green light to ban short-haul domestic flights between cities linked by train journeys of less than 2.5 hours. The French transport minister, Clément Beaune, has said that the measure will come into effect ‘as quickly as possible’. Furthermore, within the Committee on Climate Change’s sixth carbon budget (CB6), the widespread engagement scenario shows passenger demand declining by 15 per cent in 2050, relative to 2018.