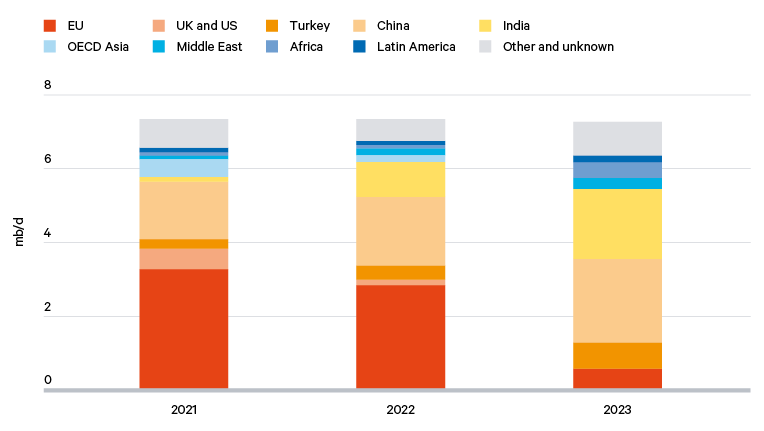

Russian oil export volumes in 2023 remained stable at 7.5 million barrels per day (b/d). A slight decline in crude oil exports was offset by a corresponding increase in oil product exports. Overall exports to the EU, the US the UK and OECD Asia dropped 4.3 million b/d below pre-war levels. However, exports to India, China and countries in the Middle East almost entirely made up for exports lost due to sanctions (see Figure 2).

Nevertheless, Russia’s monthly average revenue from commercial oil exports in 2023 fell by $4.2 billion compared with the previous year. This decline was due to price caps implemented by G7 countries and increased discounts on Russian crude more broadly.

From the European perspective, through the 2022 energy crisis, a combination of diversification policies, along with the switch to US LNG, reliable Norwegian supplies, sanctions, more renewable capacity, industrial gas demand declines, increased gas storage and a mild winter, shifted the bloc’s dependence on Russian gas from around 40 per cent per year in 2020–21 to around 12 per cent in 2023.

In 2022, EU countries together spent around €390 billion on energy subsidies, compared with €216 billion in 2021 and €200 billion in 2020. The UK, for its part, spent around an additional £60 billion on gas, and in excess of £50 billion on subsidies in 2022/23. In July 2023, Bruegel estimated that some €651 billion had, since September 2021, been allocated and earmarked across EU countries, along with the UK and Norway, in order to minimize the impact of rising energy costs on consumers.

Following the 10-fold increase in European gas prices, and the sharp fall back to near pre-war levels, LNG markets are fundamentally changed. One of the chief reasons for this is that the market has become more globalized, with increased demand for LNG and competition between Europe, China and other markets in Asia for US LNG, which is a product of the shale oil and gas boom in the US. Over the period 2018–23, US LNG exports have quadrupled, and the EU’s share has increased from an average of 28 per cent in the four years prior to 2022 to more than 60 per cent in 2022 and 2023.

Tensions remain acute in the Middle East, with recent heightened exchanges between Iran and Israel compounding fears that the widening of the Israel–Hamas conflict could lead to regional instability, and jeopardizing the crucial Strait of Hormuz, via which one in every five barrels of global daily petroleum is transported. During an emergency session of the UN Security Council in April 2024, Secretary-General António Guterres warned of the Middle East being at risk of full-scale conflict, and stating – ‘neither the region nor the world can afford more war’. The IMF also warned at this time of the increased risk that oil prices could rise sharply.

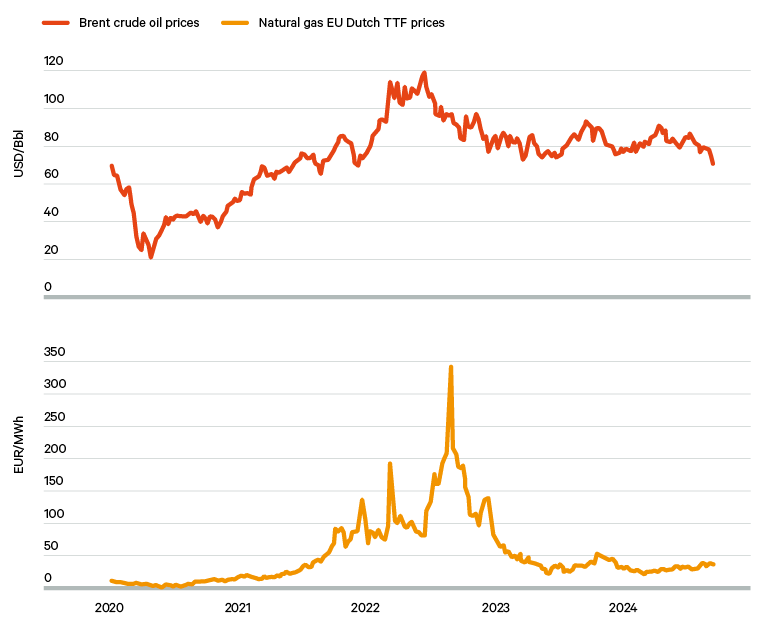

While oil and gas prices have declined from their highest point in the early months of Russia’s war on Ukraine, indications from forward markets are that for the foreseeable future prices in Europe will remain elevated compared with those in the US and China.

Future oil and gas price rises cannot be ruled out, and many market analysts anticipate ongoing price volatility. Even without considering a further escalation of Russia’s military activity, along with wider Middle East tensions, and if the US can maintain its LNG export capacity, Russia has faced refining difficulties, and at the beginning of 2024 Ukraine targeted Russian refineries, leading to production declines.

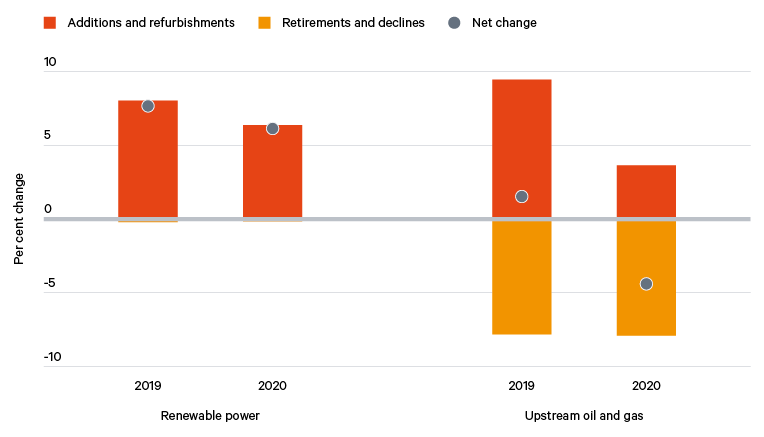

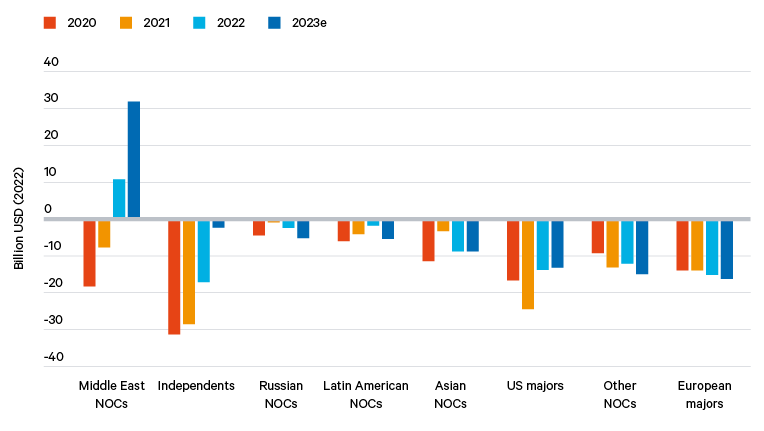

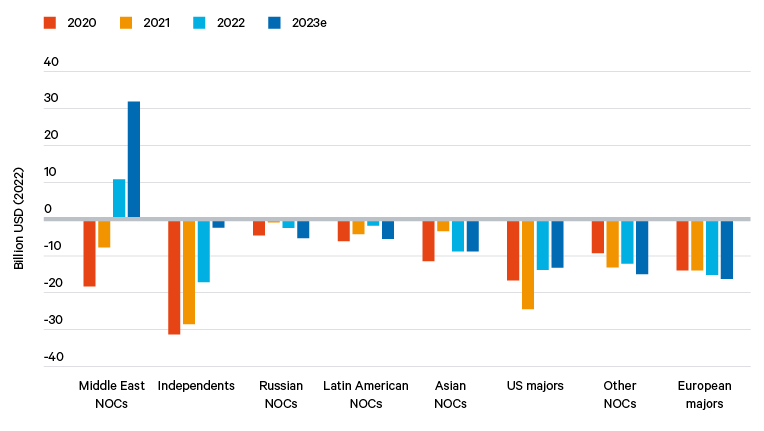

Historically low investment in upstream oil and gas means there is a structural inflationary trajectory of fossil fuel prices

Arguably, the shale oil and gas boom in the US has been one of the major drivers of the shifts in geopolitics over the last decade, as shale drilling techniques have helped the US become the world’s largest producer of oil, consistently pushing Saudi Arabia into the second spot from 2017 onwards, and meaning the US is less reliant on supplies from the Middle East. It has been this production revolution in the US that has prevented global oil prices going even higher during the war in Ukraine, and as the escalation of the Israel–Hamas conflict has fuelled wider instability in the Middle East. The scale of US output has also enabled record LNG exports to Europe, and has shielded European countries from otherwise even higher gas price inflation.