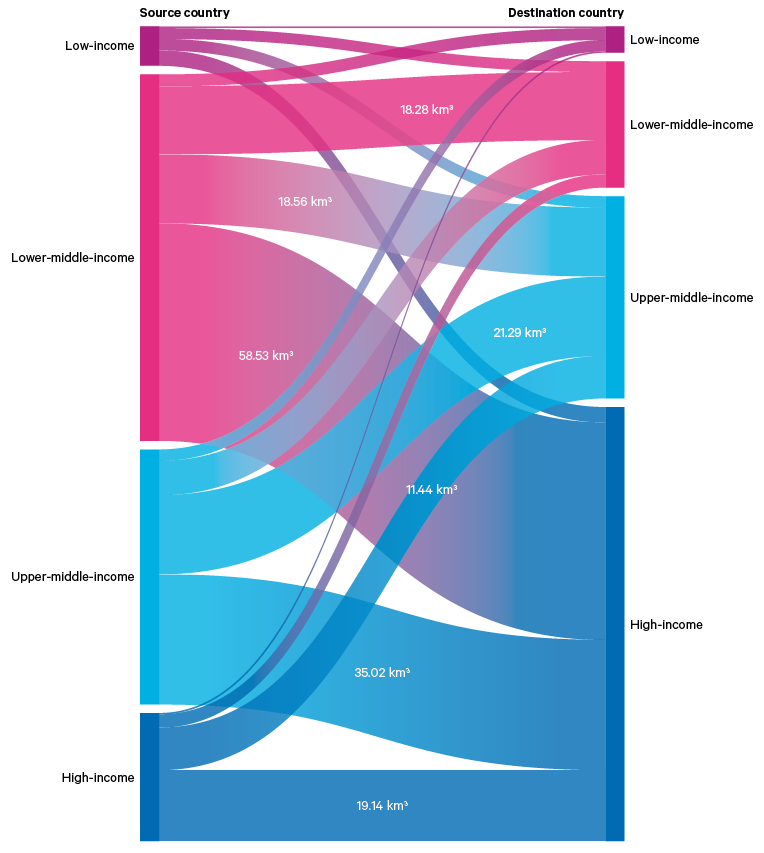

To illustrate the asymmetries in the flows of virtual water in global agricultural trade, 81 per cent of so-called ‘blue water’ embedded in this trade is associated with consumption in upper-middle-income and high-income countries. Virtual water flows from lower-middle-income countries to high-income countries are particularly significant (Figure 2). Consumption in the 19 countries of the G20 is responsible for 55 per cent of the blue water embedded in all international trade involving agricultural commodities.

These dynamics are both exacerbating water stress in producer regions and creating significant geopolitical and supply-chain risks. Although producer countries benefit by receiving income from export crops, they are also negatively affected by water pollution, diversion and depletion, all of which reduce societal resilience to the climate and biodiversity crises. This is by no means limited to developing countries. In Spain, for example, more intense and frequent heatwaves and water shortages are affecting the stability of the agribusiness sector, with knock-on consequences for Spain’s trading partners – as was illustrated by empty supermarket shelves in the UK following a 2022–23 Spanish drought. In some countries, an increase in agricultural exports has driven deforestation, contributing to increased flooding and erosion.

These environmental factors are interacting with turbulent geoeconomic dynamics – including export restrictions, supply-chain fragmentation and the use of tariffs. Increasing protectionism can restrict the flow of food products to international markets at the same time as droughts, floods and competition for water reduce harvests and worsen food security. Export restrictions in response to societal or political pressure to improve local food security can push up international prices, as was seen in many countries when food-price inflation surged owing to concerns around grain supplies following Russia’s full-scale invasion of Ukraine in 2022. Similar inflationary and supply issues are beginning to be realized as the US and Israeli conflict with Iran disrupts shipping through the Strait of Hormuz, triggering a global fertilizer crisis.

Such crises tend to deepen global inequalities, while creating conditions for political upheaval and broader geopolitical tension as countries with greater fiscal capacity potentially wield their economic influence and soft (or even hard) power to exploit other countries’ natural resources, including water.

Sector spotlight: critical minerals, advanced electronics and virtual water

As developments in the artificial intelligence (AI) sector progress rapidly, there is growing scrutiny of virtual water’s role in advanced electronics. The direct operational water use of data centres has attracted attention, as it visibly affects and creates tensions with local communities and nearby industrial and agricultural water users. However, advanced electronics of all kinds also carry significant indirect globalized water footprints from water use in the supply chain. A wide range of products – consumer electronics, advanced weapons systems, electric vehicles (EVs), green technology infrastructure – are all reliant on, and pollutive of, water at various stages of raw-material extraction and manufacturing.

Multiple water-intensive supply-chain stages often leave significant per-product water footprints in the electronics sector. Supply chains in this sector are characterized by their complexity, as they can involve hundreds of regionally clustered suppliers – each using and degrading water in their own operations as well as inheriting the water use in upstream extraction, processing and fabrication stages. Such supply chains can start with water-intensive mining for critical raw materials in arid, potentially water-stressed countries or regions (such as parts of the US, Australia, South Africa and India). Sixteen per cent of critical mineral deposits and mines are located in highly water-stressed areas. Lithium – used in both EV batteries and solar panels – is particularly water-intensive. Over half of the global reserves of lithium are found in South America’s ‘lithium triangle’, a region experiencing severe water stress. Impacts from mining operations can include contamination from hazardous materials, for example through acidic mine drainage or stored tailings (waste material) that leach into groundwater due to improper treatment.

Mining operations can threaten local needs, including basic access to water and sanitation. In the Democratic Republic of the Congo (DRC), which has the world’s largest reserves of cobalt but where basic water and sanitation access is low, poor water quality around mining sites has sometimes led to higher prevalence of disease including diarrhoea, hepatitis and cholera. (Cobalt is essential to many industrial processes, and to production of batteries for the green transition.) Mining operations in the DRC have sometimes contaminated groundwater and soil, affecting the supply of clean water for local populations.

The centrality of these industries to the global economy creates potentially significant supply-chain dependencies and geopolitical tensions around the geographic concentration of resource extraction and processing capabilities. The US’s aggressive statements in early 2026 in relation to Greenland are one such example, and may have been motivated by a desire to access the Danish territory’s abundant critical minerals as a counter to China’s status as the majority supplier of the world’s rare earth minerals.

The semiconductor sector (see also Box 2) illustrates some of these challenges. High volumes of water are used in advanced electronics manufacturing, due to the need for ultrapure water (UPW) to ensure high manufacturing standards. Given massive global demand for sophisticated semiconductors, we can expect the electronics sector’s consumption of water generally, and UPW specifically, to increase further in the future.

Water use by data centres is also a concern. Over 40 per cent of such facilities are projected to face high or extremely high water stress between 2030 and 2040. Moreover, with investment in AI skyrocketing, the global number of data centres in operation, planned or under construction is rising dramatically.

While security of water supply may not currently be a significant factor in the geopolitical jockeying of countries to control electronics supply chains, the sector’s high consumption of water, the geographic concentration of resources and processing capacities, and the growing climate change impacts and water stressors associated with electronics manufacturing suggest that sustainable water use deserves to be a more central consideration throughout the value chain. The water-intensive stages of critical-mineral and semiconductor supply chains are intersecting with strategic competition over technological leadership, industrial resilience and raw-material security. As countries adjust their geo-economic strategies and diversify or onshore water-intensive production, water risk – hitherto often underacknowledged – will become an increasingly important factor shaping national resilience and global economic stability. This linkage between industrial policy, resource security and geopolitical fragmentation is examined further in Chapter 3.