It is also heavily interconnected within the EU. A Brexit could therefore jeopardise UK growth prospects as well as global financial stability. Here a Chatham House international economics expert explains how.

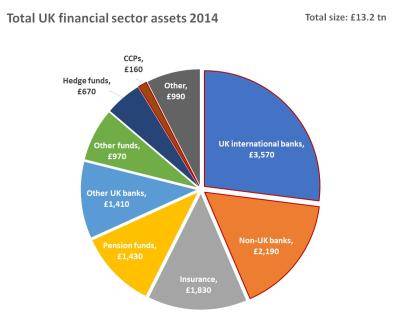

Includes all financial assets held on bank balance sheets excluding derivatives. Assets in billion British pounds.

Source: Bank of England

- UK international banks and non-UK banks — the two largest subsectors — will be most directly affected by a Brexit vote. The majority of non-UK banks’ assets, representing over £1tn, are EEA based. Currently EEA banks can ‘passport’, which means that they can operate in a unified manner across borders within the EEA. Leaving the EU would end passporting rights (unless the UK joins the EEA) making the UK operations of EEA banks and European operations of UK banks significantly harder to conduct.

- The trading of derivatives, currencies and other commodities is a significant proportion of financial activity worldwide. This activity is mediated through institutions known as Central Counterparties (CCPs), which provide a central platform to co-ordinate trades — a process known as ‘clearing’. Four of the largest CCPs are based in London but 21% of their members’ assets are EEA-based outside the UK. If the UK were to leave the EU, much of their clearing activities denominated in Euros would likely have to move to the Eurozone, meaning the UK’s CCPs would either have to move or downsize. Relocating such complex activity (and building the associated regulatory frameworks) would introduce significant uncertainty into the financial system.

- Barring a negotiated agreement after Brexit, non-bank sectors such as insurance and the funds sector would lose access to the single market. Being cut out of the single market, and from Europe’s capital markets union as that initiative moves forward, could make the British financial industry less competitive in the long term.

- London will see its global prominence as the world’s leading international financial centre considerably diminished after a Brexit vote. Many of London’s functions — such as euro-related clearing activities — are likely to be transferred to other financial centres in Europe while more global activities will be relocated to New York.