Significant changes in how cement and concrete are produced and used are urgently needed to achieve deep cuts in emissions in line with the Paris Agreement on climate change.

Chatham House report

Published 13 June 2018

Updated 14 December 2020

ISBN: 978 1 78413 272 9

Significant changes in how cement and concrete are produced and used are urgently needed to achieve deep cuts in emissions in line with the Paris Agreement on climate change.

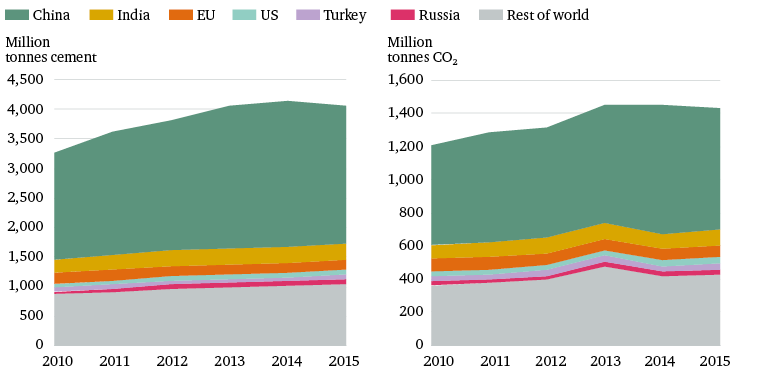

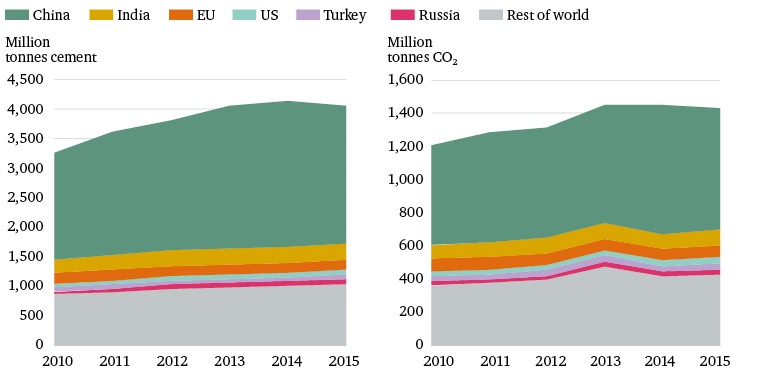

Cement is a key input into concrete, the most widely used construction material in the world. Every year, more than 4 billion tonnes of cement are produced. The chemical and thermal combustion processes involved in the production of cement are a major source of CO2 emissions, contributing around 8 per cent of annual global CO2 emissions.13 Moreover, cement production is expected to grow. The total global building floor area in 2016 was around 235 billion square metres (m2).14 This is projected to double over the next 40 years – equivalent to adding the total building floor area of Japan to the planet every year to 2060.15

The bulk of this growth is expected to happen in emerging markets. While China’s cement production – a key driver of the market in recent years – may have peaked,16 urbanization in other industrializing countries such as India and Indonesia is likely to continue to boost global demand.17 Some estimates project a threefold to fourfold increase in demand from developing countries in Asia by 2050.18

The Global Commission on the Economy and Climate estimates that $90 trillion will be invested in infrastructure through to 2030, and that two-thirds of this investment will be in developing countries

A substantial expansion of the built environment is needed to meet the SDGs. Expanding access to clean water and energy depends on replacing old and building new infrastructure.19 The Global Commission on the Economy and Climate estimates that $90 trillion will be invested in infrastructure through to 2030, and that two-thirds of this investment will be in developing countries.20 It also projects that, if developing countries expand their infrastructure to current average global levels, the production of the required materials alone will cumulatively emit 470 GT of CO2 by 2050.21

Yet this potential expansion would take place during a critical period for global decarbonization. Greenhouse gas emissions need to fall by around half by 2030 to meet the Paris Agreement goal of keeping global warming to well below 2°C above pre-industrial levels, and to pursue efforts to limit the temperature increase even further to 1.5°C.22 This scenario is even more demanding for the built environment. It will require carbon-neutral or carbon-negative construction everywhere from 2030 onwards, which implies the need to rapidly scale up the use of building materials with zero or negative emissions in the next decade.23

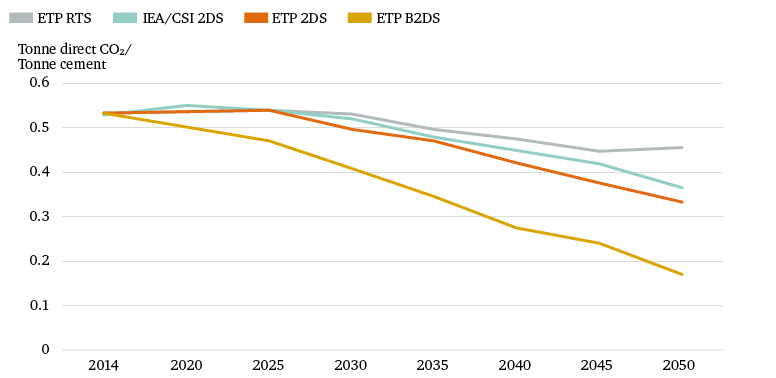

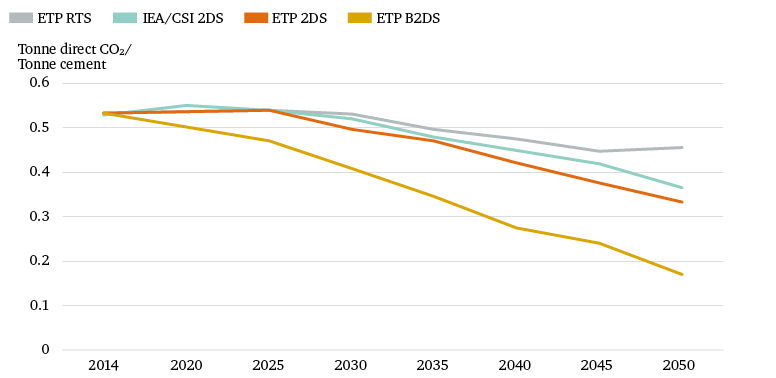

The urgency of early action implied by ‘well below’ 2°C is demonstrated by the scenarios shown in Figure 3. According to the IEA’s ‘Beyond 2°C Scenario’ (B2DS) articulated in its Energy Technology Perspectives 2017 (ETP),24 a 24 per cent reduction in direct emissions per tonne of cement produced by 2030 is required, relative to 2014 levels (equivalent to a 16 per cent absolute reduction in direct emissions).25 The 2°C scenario (2DS) in the IEA’s ETP suggests a reduction of 7 per cent by 2030, and the 2018 roadmap a reduction of 4 per cent over the same period.

In this context, the cement and concrete sector faces a considerable challenge: how to increase production to help roll out infrastructure services and tackle a growing global housing shortage while also achieving emissions reductions in line with global targets.

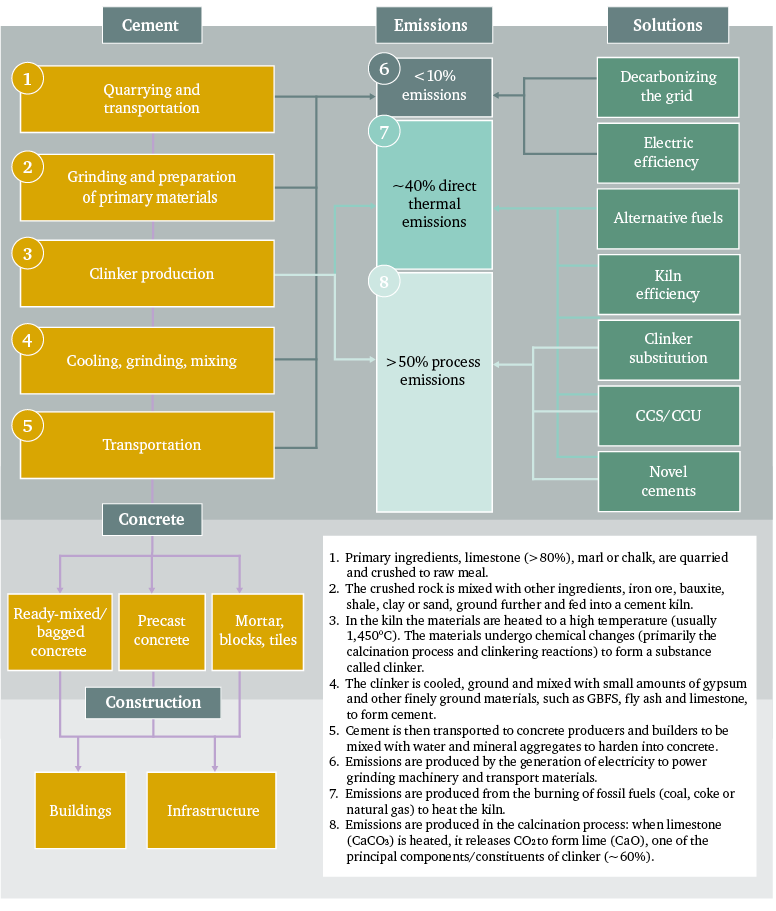

Cement comes in different forms, but it is generally made up of the following key elements: Portland clinker, gypsum, supplementary cementitious materials (SCMs) and fillers. SCMs and fillers include fly ash, granulated blast furnace slag (GBFS) and limestone. Portland clinker is the main ingredient in cement and accounts for the majority of the sector’s emissions. More than 50 per cent of the sector’s emissions are released from the calcination of limestone to produce Portland clinker.26 These are known as ‘process emissions’. A further 40 per cent are generated in the burning of fossil fuels to heat cement kilns to high temperatures for that process.27 Figure 4 highlights emissions and mitigation solutions at different stages along the cement production chain.

The ‘embodied emissions’ of cement – the sum of greenhouse gas emissions associated with its production – are contingent on how much Portland clinker is included, the efficiency of the equipment used, the fuel used and the energy mix in a given location. The production of 1 kg of Ordinary Portland Cement (OPC), the most common type of cement used, with >90 per cent of its composition made up of Portland clinker, results in 0.93 kg of CO2 on average. By comparison, a high-blend cement, i.e. one with a low share of Portland clinker and a high share of SCMs and fillers, can have an embodied-carbon figure as low as 0.25 kg CO2/kg.28

The amount of Portland clinker that can be displaced depends on the type of substitute material used and the grade of concrete required for a given application. As Figure 4 indicates, cement has a variety of end uses. Reducing the Portland clinker content of cement may affect the properties of the final concrete product. Moreover, each clinker substitute has different characteristics and is therefore suitable for different applications.29 Some clinker substitutes can improve the strength development and durability of concrete.30 Cement and concrete standards therefore dictate the Portland clinker content required for a cement or concrete to fulfil criteria for specific applications.

Although blended cements are already widely used in Europe, the global market is still dominated by high-clinker cements. Portland cement, which tends to be made up of >75 per cent Portland clinker,31 is used in more than 98 per cent of concrete produced globally today.32 There are good reasons for this: it is cheap, it produces a high-quality concrete, it is reliable and easy to use, and the raw materials needed to produce it (limestone, chalk and marl) tend to be abundantly available and co-located.33 Maybe most importantly, it has an almost 200-year track record of being used as a construction material, giving engineers and builders confidence in its performance and long-term durability.34

Portland cement, which tends to be made up of >75 per cent Portland clinker, is used in more than 98 per cent of concrete produced globally today

The global cement market is dominated by a few large producers: LafargeHolcim (the product of a 2015 merger between Lafarge of France and Holcim of Switzerland), HeidelbergCement (Germany), Cemex (Mexico) and Italcementi (an Italian firm in which HeidelbergCement has a 45 per cent stake).35 While Chinese companies are leading players in terms of production volumes, they largely continue to operate in their domestic market. Globally, cement firms tend towards vertical integration, producing their own concrete in downstream operations. The capital intensity of cement production36 reinforces this concentration, making it difficult for smaller actors to enter the market and compete with larger firms.

In contrast, the global concrete market is much more fragmented than the cement market, and is built on many smaller companies serving local areas.37 The key differences between concrete producers lie in how they deliver concrete to the end-user: ready-mixed, bagged or precast.38

Every year more than 10 billion tonnes of concrete are used – which, according to some sources, makes it the second-most consumed substance on Earth (after water).39 Given the environmental costs involved, why do we use so much concrete (and as a result cement) as opposed to other construction materials? Few materials have the versatility, resilience, ease of production, low cost and durability of concrete or can resist environmental extremes in the way concrete can. Its high thermal mass and low air infiltration help reduce the energy required to heat and cool buildings.40

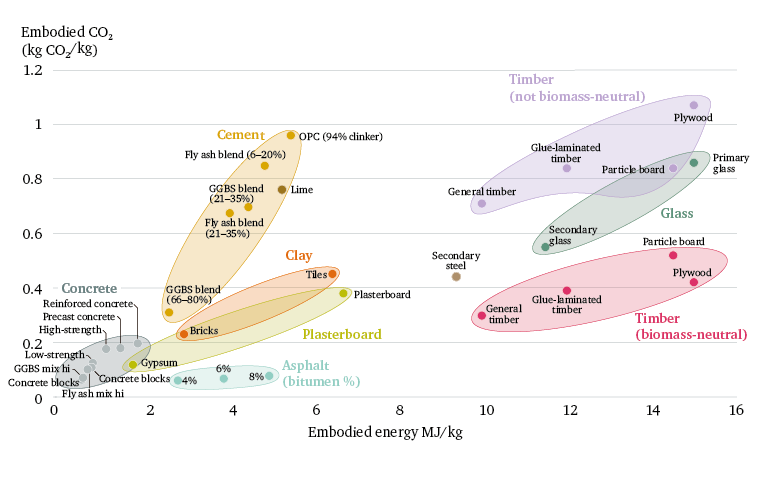

Moreover, alternative materials often come with a higher carbon footprint.41 Figure 5 shows embodied carbon values for cement, concrete, timber, glass, plasterboard and asphalt in the UK (note: aluminium, plastic and steel products are largely omitted from Figure 5, for reasons of space and clarity as their values for embodied energy and CO2 emissions are greater than 16 MJ/kg and 1.2 kg CO2/kg respectively). The obvious conclusion is that cement and concrete have relatively low embodied emissions on a per-kilogramme basis compared to other materials.

This comparison, however, misses some important dimensions and interactions. First, it does not distinguish between how much of each material is needed for a given application or performance level. Second, some of these materials can be substituted for concrete, but typically only for some applications. Third, materials are often best understood in combination: for instance, the strength offered by a combination of steel and concrete. The scope for doing more on the substitution front is explored in Chapter 4.

Finally, Figure 5 also highlights the large variation in embodied carbon levels across different types of cement. Given the vast quantities of concrete and cement consumed annually, it remains critically important to make these materials more sustainable.

The cement industry has pursued strategies to reduce CO2 emissions since the 1990s. In particular, the major producers have worked together under the Cement Sustainability Initiative (CSI), and have devoted substantial effort to introducing mitigation solutions. Policymakers have also sought to encourage enhanced efficiency and accelerated decarbonization. These efforts have focused on four main levers:42

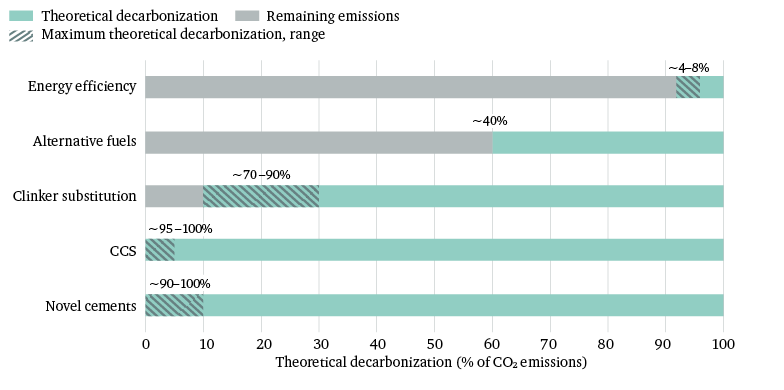

The first lever involves upgrading kilns and equipment so that less energy is needed to produce cement. Changing plant design, shifting towards higher-efficiency dry kilns, upgrading motors and mills, and using variable-speed drives can make a big difference to energy consumption and costs.43 Firms are increasingly employing ‘smart’ devices to track and monitor operations, as well as machine learning to improve process control in their plants.44 Optimizing the recovery of waste heat has been shown to reduce cement factories’ operating costs by between 10 per cent and 15 per cent.45 More efficient grinding processes can offer electricity savings, also benefiting overall energy efficiency.46

Although the industry has invested heavily in optimizing production processes, an efficiency gap remains. Producing cement using the current best available technology (BAT) and practice results in thermal energy consumption of around 2.9 GJ/tonne of clinker.47 By comparison, the global average in 2014 was 3.5 GJ/tonne of clinker.48 The efficiency gap largely reflects the use of older equipment in Europe and the US. Meanwhile, the Indian cement industry is one of the most energy-efficient in the world, with average thermal energy consumption of approximately 3.0 GJ/tonne of clinker.49

The second lever consists of switching from fossil fuels to alternatives such as biomass and waste. Coal has been the main fuel used historically,50 but cement kilns can safely burn biomass and waste instead of fossil fuels as the high processing temperature and the presence of limestone clean the gases released.51 The type of alternative fuel used, however, depends on local availability and the quality of alternatives, which are often outside the control of cement producers.

The use of alternative fuels in cement production is most prevalent in Europe, making up around 43 per cent of fuel consumption there compared to 15 per cent in North America, 8 per cent in China, South Korea and Japan, and around 3 per cent in India.52 This indicates that a lot can still be achieved by simply increasing the use of alternative fuels, particularly in emerging markets such as China and India.53 There is even scope for improvement in Europe, where the average cement plant could substitute around 60 per cent of its fuel with alternatives; some European producers are already running on >90 per cent waste fuel for extended periods.54

The third lever consists of reducing the amount of Portland clinker used by substituting it with clinker substitutes such as fly ash, GBFS and limestone. The IEA estimates that around 3.7 GJ and 0.83 tonnes of CO2 can be saved per tonne of clinker displaced.55 How much clinker substitute can be blended into cement or concrete depends on the type of clinker substitute and the grade of concrete required, but some substitutes – e.g. GBFS – theoretically allow for substitution levels of over 70 per cent,56 potentially reducing emissions from production by over 60 per cent.

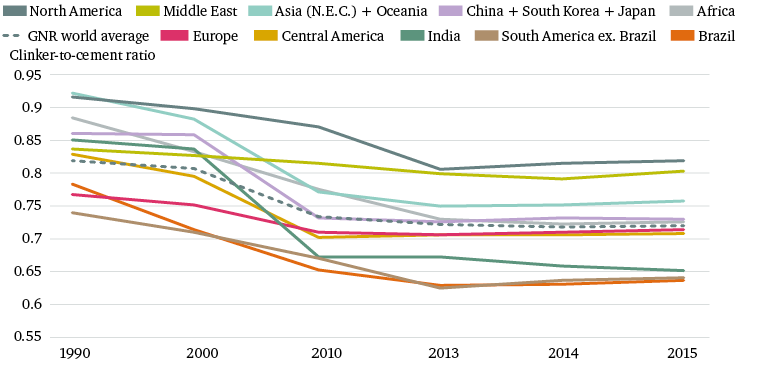

To date, clinker substitution has contributed on average to a 20–30 per cent decrease in CO2 emissions per tonne of cement produced, compared to the 1980s.57 The average clinker ratio was around 0.65 in 2014.58 While the reduction in clinker use has been substantial, clinker ratios have recently levelled off (see Figure 6) and there is still considerable scope for improvement in most regions, as evidenced by the target set by the 2018 roadmap of reaching an average global clinker ratio of 0.60 by 2050.59 This is considerably more ambitious than the target of 0.71 by 2050 set in the original 2009 roadmap.60 The main constraints on clinker substitution tend to be the availability and cost of clinker substitute materials, which vary considerably by region, consumer acceptance and the barriers imposed by standards and regulations.61

The fourth lever consists of capturing the emissions from a cement kiln, and then securing and storing these. CCS is particularly attractive for cement producers, as the process emissions from heating limestone to produce clinker cannot be avoided by simply switching fuels and improving energy efficiency. Even with large-scale substitution of Portland clinker, emissions from the portion of clinker that would still be produced would continue to present a challenge.62

This is reflected in the emphasis on CCS in technology roadmaps. In the 2009 roadmap, CCS accounts for 56 per cent of the planned direct emissions reduction to 2050, compared with 10 per cent for clinker substitution, 24 per cent for alternative fuels and 10 per cent for energy efficiency.63 The ETP 2017 B2DS relies on CCS for 83 per cent of cumulative emissions reductions in the cement sector.64

The cement industry has engaged in several projects to develop CCS.65 However, as in other sectors, development has been slow. Most CCS technologies are still at the basic research or demonstration stage.66 One of the main barriers so far has been cost.67 Several countries also lack an adequate legal framework for CO2 storage.68 Finally, the lack of geographic clustering is a problem. Most cement plants are too small to justify by themselves the construction of the necessary distribution infrastructure for captured CO2.69 This is not a problem where they are clustered with other industrial sources of CO2, but many may not be suitably located.

These levers – with the exception of CCS – have delivered an 18 per cent reduction in the global average CO2 intensity of cement production since 1990.70 There have been even more impressive reductions in certain countries and regions: for example, Poland recorded a 42 per cent decrease in the same period.71 Progress on each of the levers has also largely been in line with the 2015 indicators set in the 2009 roadmap.72

These levers – with the exception of CCS – have delivered an 18 per cent reduction in the global average CO2 intensity of cement production since 1990

But these gains have been more than matched by increasing demand. There has been an almost 50 per cent increase in the sector’s gross emissions at the global level since 1990.73 Moreover, the new scenarios set out by the 2018 roadmap and the 2017 ETP are more ambitious than the 2009 roadmap, especially for clinker substitution and CCS.74 The cement sector has to not only continue to deploy all of these options but also do so faster, especially if it is to meet B2DS.

There are a number of reasons why the sector has not moved quickly in the past. The capital intensity of cement production relative to revenue means that it can take several years to recoup investments in infrastructure.75 This can make producers reluctant to shift to new approaches that might ‘strand’ existing assets. There has been a lack of financial incentives for the sector to adopt mitigation solutions.76 Finally, the broader construction sector, within which the cement and concrete sector is embedded, tends to be risk-averse.77 Safety is naturally an overriding priority, leading to a strong preference for sticking with practices and products with proven track records.

There are also limits to what existing approaches can deliver in terms of deep decarbonization:

Reaching a clinker ratio of 0.60 by 2050, as set out by the 2018 Technology Roadmap, will also present a significant challenge – implying regulatory and technical changes, as well as innovation throughout the cement and concrete sector and across regions. It will depend on the viability and availability of clinker substitutes at a time when traditional sources (slag and fly ash) are on the decline. Even if the 0.60 target is achieved, there will be residual process emissions from the share of Portland clinker that continues to be produced.

In short, the relatively easy decarbonization gains have largely been made. Given the increased ambition and urgency required to shift to a Paris-compatible pathway, the next phase of decarbonization will be technically and economically more challenging than efforts to date unless a new wave of innovation redraws the landscape.

Against this backdrop, there has been considerable interest in innovations that could steeply reduce overall emissions by introducing changes to cement composition. Low-carbon cements, or ‘novel cements’ as this report refers to them, are substances made from alternatives to Portland clinker that mimic the properties of conventional Portland cement but that can be produced using less energy and release fewer emissions in production. Some novel cements even enhance the properties of concrete.81

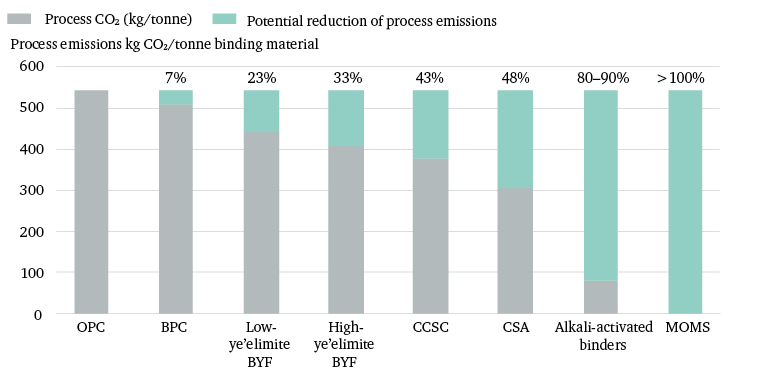

A decade ago, a British start-up called Novacem announced breakthroughs in carbon-negative cement.82 More recently the buzz has been around companies such as Solidia Technologies, Blue Planet, CarbonCure and Skyonic, which are developing concretes that absorb and store CO2. Solidia, a US firm now in a partnership with major cement producer LafargeHolcim, claims that its low-clinker-content CO2-cured concrete reduces CO2 emissions by 70 per cent compared with OPC.83 LafargeHolcim itself has developed Aether, a belite ye’elimite-ferrite (BYF) clinker that has a lower limestone content than OPC and requires a lower production temperature,84 resulting in CO2 emissions reductions of 20 per cent or more per unit of clinker in cement.85

By altering the raw materials used (in most cases reducing the share of limestone), these clinkers can reduce process emissions from limestone calcination and thermal emissions from fuel combustion. For example, carbonatable calcium silicate clinkers (CCSC) of the kind used in Solidia concretes may lower process emissions by 43 per cent (see Figure 7). Magnesium oxides derived from magnesium silicates (MOMS), the technology promoted by Novacem, could in theory be made from materials that contain no carbon.86 Geopolymer or alkali-activated binders can have embodied energy and carbon footprints that are up to 80–90 per cent lower than those for Portland cement.87 Both CCSC and MOMS can be hardened by carbonation (using CO2 rather than water) – meaning that they could absorb and contain more CO2 than is emitted in the manufacturing process, making them ‘carbon-negative’.88

So far, however, these novel cements and concretes have failed to penetrate the market significantly.89 Many of these products face resistance from consumers.90 Almost all standards, design codes and protocols for testing cement binders and concrete are based on the use of Portland cement, making it difficult to experiment with and scale up the use of novel products.91 Not all of these novel binder technologies have reached a level of maturation to be deployed at scale. Finally, there can be difficulties extending stakeholder participation beyond the manufacturers of novel cements and concretes.92

Given the rapid emissions savings needed for a climate-compatible cement and concrete sector, understanding the potential for disruption in the sector – i.e. breaking through the barriers outlined above – is vitally important.

The sector will need to move on two broad fronts:

Moreover, to decarbonize cement and concrete, it is necessary to look beyond the sector itself and consider the wider built environment, and even to examine assumptions around how we will live in the coming decades. Although a full examination of this is beyond the scope of this report, our analysis looks at key areas that could affect the decarbonization of cement and concrete, shape future demand, or unlock barriers to scaling up innovative technologies.

In this context, it needs to be remembered that the cement and concrete sector will not be immune to broader disruptive trends stemming from digitalization and new business models. Enhanced connectivity, remote monitoring, predictive analytics, 3D printing and urban design are already combining to transform traditional supply chains within the construction industry, as well as the interaction and management of actors along those chains.95

Another reason for looking at the wider context in which innovation in low-carbon cement and concrete must develop is that countervailing trends in politics society and the workforce are reshaping the future of the built environment.96 If the decarbonization of the energy and transport sectors accelerates as expected, cement and concrete producers could find themselves next in line in terms of facing demands for radical change. Those that fail to adapt to public and consumer expectations around deep decarbonization and sustainability could find their licences to operate under threat. The urban landscape and infrastructure developments will be the battleground in which such issues play out.

The ability of decision-makers in business, government and civil society to encourage and accelerate decarbonization in cement and concrete will rely on greater clarity around the most promising technologies and on opportunities for radical new approaches. Innovation trends are also critical for informing investment into research and development (R&D) and as an input into low-carbon industrialization strategies for policymakers.

The ability of decision-makers to encourage and accelerate decarbonization in cement and concrete will rely on greater clarity around the most promising technologies and on opportunities for radical new approaches

The report examines three questions:

It draws on nine months of research on low-carbon innovation in the cement and concrete sector, including a patent-landscaping exercise conducted by Chatham House and CambridgeIP (an innovation and intellectual property consultancy); 10 expert interviews; and two workshops held to discuss methodology, findings and recommendations, in which 10 companies were represented.

Patent landscaping involves creating databases of patents for individual sectors or ‘technology areas’. It is used to measure innovation, as well as to understand systems of innovation – for instance, by revealing geographical trends and changes in innovation patterns over time.97

There are several advantages to using patent data as a proxy for innovation. Patents provide a large amount of information on the nature of the invention, the inventor(s) and the applicant. The data are available, quantitative and discrete.98 As a result, patents can be aggregated and compared using common metrics.

However, patent data provide an imperfect picture of innovation. First, the data can be incomplete. Second, non-technological innovations are not patentable. Third, even among innovations that can be patented, some may not be patented as companies may not wish to reveal their technology in an open document. Finally, patent data alone reveal little about the potential importance or impact of an innovation.

To understand the drivers of and barriers to innovation, as well as which innovations present truly transformative steps, analysis needs to go beyond simple patent identification. We therefore overlay the trends derived from the patent analysis with additional analysis of key factors that affect the deployment of low-carbon cements. These will be explored in Chapter 3.

We focus the patent search on technologies and processes to do with ‘clinker substitution and replacement’. One of the key reasons for this is the potential of this particular lever to contribute to deep decarbonization (see Figure 8). Clinker substitution and replacement can lower thermal emissions, as well as significantly reduce and potentially eliminate process emissions from cement production. Such approaches also potentially present relatively inexpensive routes to decarbonization.99 Scaling up clinker substitution does not generally require changes in equipment or fuel sources.100 Similarly, some of the novel cements discussed above can be produced in conventional cement kilns.101 By contrast, most CCS technologies require substantial investment in new kilns.102 Finally, increased ambition by the cement industry around clinker substitution (reflected in global targets) suggests that this is an area with further potential and where efforts will need to be increased.

The term ‘clinker substitution’ generally refers to lowering the Portland clinker content of cement by blending in alternative materials.104 The patent search area also includes novel cements and concretes in order to capture the more radical innovations emerging in this area. The search area is defined as: products and processes to do with lowering or entirely replacing the Portland clinker content of cement and concrete. This includes two categories in particular:

As a shorthand, the report refers to this technology area as ‘clinker substitution and replacement’, to SCMs and fillers collectively as ‘clinker substitutes’, and to alternative-clinker technologies as ‘novel cements’. For a full list of subcategories and definitions of technologies included, see Appendix 1.

Chapter 2 sets out the focus and findings from the patent analysis, highlighting geographic and organizational patterns of innovation as well as the extent of technology diffusion thus far. China emerges as a key player in innovation. The chapter also explores the barriers holding back the commercialization and widespread deployment of low-carbon cements.

Chapter 3 explores the potential to overcome the barriers to the deployment of low-carbon cements and concretes. Possible solutions include higher carbon prices, as well as alternative strategies around product standards, the leveraging of public procurement, or new business models. The chapter also argues that the cement sector may not be immune from digital disruption, which could bring new opportunities for emissions reductions.

Chapter 4 highlights the potential for disruptive shifts in the built environment that could radically change how cement and concrete are used, or could open up the use of alternative materials. These areas could help to deliver deep decarbonization, but the scale of this opportunity is only just starting to come into focus. Moreover, a climate-safe pathway would need to combine these new opportunities with the strategies described in Chapter 3.

Chapter 5 provides conclusions, recommendations and practical suggestions on ways to move forward.

Cement is a powder used in construction made by grinding clinker together with various mineral components such as gypsum, limestone, blast furnace slag, coal fly ash and natural volcanic material. It sets usually by reaction with water, hardens and sticks to other materials such as sand, gravel or crushed stone, and binds them together to form concrete or mortar.109

Clinker is an intermediate product in cement production. Conventional clinker (also referred to as Portland clinker in this report) is a greyish substance, consisting of granules the size of a small marble, formed from heating limestone and other materials in a cement kiln.110

Alternative clinkers or binders are made from different materials or via different processes from those associated with the production of traditional clinker. They generally consist of natural or man-made materials (ideally from a carbon-free raw material base) that, once ground to a fine powder, are capable of reacting rapidly with water and/or CO2 to form a hardened mass that can be used as a binder.111

Clinker substitutes are materials added to cement or concrete to lower the share of clinker. They include:

Cementitious is a term used to refer to materials that have a similar nature to cement, i.e. ‘of the nature of cement’.114

Portland cement is the most common type of cement used worldwide. Different standards around the world allow for the designation ‘Portland cement’ to apply to products containing varying shares of Portland clinker. For example, European cement standard EN 197-1 defines two main types of Portland cement: CEM I >95 per cent clinker and CEM II Portland-composite cement 65–94 per cent clinker.115 Today, the proportion of clinker substitutes in Portland cements is generally around 20 per cent of the whole mix (i.e. making them >75 per cent clinker).116

Ordinary Portland Cement (OPC) is a common type of cement consisting of >90 per cent ground Portland clinker and about 5 per cent gypsum. OPC is often referred to by different names: Portland cement or CEM I in Europe, PI or PII in China, and Portland cement Types I to V in the US.117

Composite and blended cement are cement types with a lower share of clinker than OPC (i.e. <90 per cent).118

High-blend cements are cements with >50 per cent clinker substitutes as a share of the cement mix.119 This report sometimes also refers to these as low-clinker cements.

Low-carbon cements contain less or no Portland clinker, and therefore release fewer CO2 emissions in production and may require less energy to produce.

Ternary cements or concretes are mixtures including three different cementitious materials – e.g. a ternary concrete might be made up of a combination of Portland cement, GBFS cement and fly ash cement.

Concrete is cement mixed with water to form a paste and filled with mineral aggregates such as sand and gravel.120 Concrete has characteristics that vary according to the concrete mix and are influenced by the cement used. These differences are reflected in the different grades assigned to varying mixes.

Low-carbon concrete is concrete with fewer embodied CO2 emissions than conventional Portland-cement concrete. This can mean that it contains less Portland cement and more clinker substitutes, or that it contains alternative-clinker cement.

Carbon-negative concretes are concretes that capture and store more CO2 than is released during their production. These concretes are hardened by carbonation (using CO2) instead of hydration (using H2O) – i.e. they absorb CO2 as they harden.

Aggregate is inert filler, e.g. sand, gravel or crushed stone, within a concrete mix.121

Chemical admixtures are chemicals added to a concrete mix immediately before or during mixing to modify the properties of the mix.122

Embodied carbon is the sum of the carbon requirements associated, directly or indirectly, with the delivery of a good or service. In the context of building materials, it is the sum of CO2 equivalent or greenhouse gas emissions associated with the production of the material.

Operational carbon is the sum of the carbon requirements associated, directly or indirectly, with the operation of a good or service. In the context of buildings, it is the sum of CO2 equivalent or greenhouse gas emissions associated with the operation (heating, cooling, powering) of a building.

Direct emissions are emissions of greenhouse gases from sources owned or controlled by the reporting entity. Examples include the emissions from cement kilns, company-owned vehicles, quarrying equipment, etc.123

Indirect emissions are emissions that are a consequence of the reporting entity’s operations but that occur at sources owned or controlled by another entity. Examples include emissions related to purchased electricity, employee travel and product transport in vehicles not owned or controlled by the reporting entity, and emissions occurring during the use of products made by the reporting entity.124

Process emissions are defined as the portion of CO2 emissions from industrial processes that involve chemical transformations other than combustion. In the context of cement, these are CO2 emissions released by limestone as it is calcined in a cement kiln.125

Calcination process refers to changing the chemical composition of a material by a thermal process. In clinker production, limestone is calcined (i.e. heated) to form lime, one of the principal components of clinker.126

Note: Throughout this report we refer to ‘Portland cement’ or ‘traditional Portland cement’ to signify a set of cements with a Portland clinker content generally >70 per cent. This, therefore, encompasses, OPC, CEM I and most of the CEM II cements. When we refer to OPC, we specifically mean cement with a Portland clinker content >90 per cent. Throughout this report we refer to traditional cement clinker, i.e. clinker made in a conventional way with a high share (>60 per cent) of calcium silicates, as ‘Portland clinker’.