Significant changes in how cement and concrete are produced and used are urgently needed to achieve deep cuts in emissions in line with the Paris Agreement on climate change.

Chatham House report

Published 13 June 2018

Updated 14 December 2020

ISBN: 978 1 78413 272 9

Significant changes in how cement and concrete are produced and used are urgently needed to achieve deep cuts in emissions in line with the Paris Agreement on climate change.

This chapter explores how to overcome barriers to the diffusion of clinker substitution and novel-cement technologies. It looks at a combination of existing and proposed policies and approaches, from carbon prices and new standards to leveraging public procurement and encouraging new, more service-oriented, business models. It also considers opportunities for digital disruption in the cement sector – a shift that could bring new opportunities for emissions reductions.

To achieve a steep decarbonization trajectory, a portfolio of these approaches will be needed, and these will have to be tailored to different markets. Each section below, therefore, discusses where a given solution can best be deployed, whether with respect to a specific location, technology or type of application.

Achieving an average global clinker ratio of 0.60 by 2050, as set out in the 2018 Technology Roadmap, would require roughly 2 billion tonnes of clinker substitutes to be consumed in 2050,215 almost 40 per cent more than the quantity consumed today.216 At the same time, the global availability of traditional clinker substitutes – fly ash and blast furnace slag – is likely to decline to around 16 per cent of cement production by 2050.217 This would mean that 1.2 billion tonnes will need to come from alternative sources.218 Increasing the supply and utilization of traditional and non-traditional clinker substitutes will therefore be critical for meeting emissions mitigation targets.

This section focuses primarily on the potential to address scarcity of raw materials for clinker substitutes rather than of those for novel cements. Geopolymers and alkali-activated binders largely depend on the same materials as clinker substitution. Any potential to increase the availability of clinker substitutes should also benefit geopolymers and alkali-activated binders. Several of the other novel cements discussed do not face material supply constraints; those that do face such constraints require further R&D in the first instance to overcome this issue.

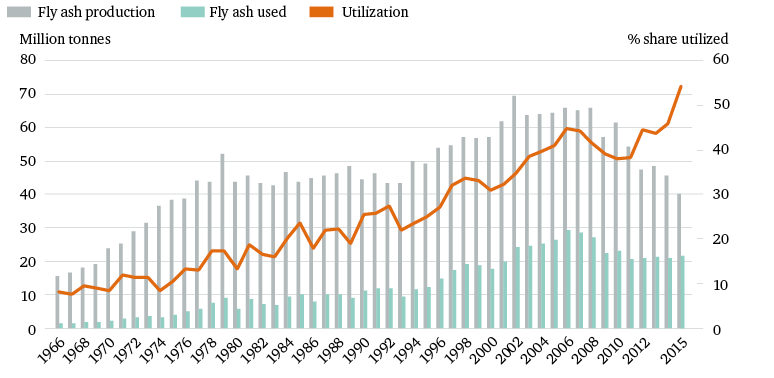

There is scope to increase the availability of traditional clinker substitutes in the short term through targeted regulation. The supply chain for clinker substitutes is heavily influenced by regulation. In the wake of an accident in 2008, for example, the US Environmental Protection Agency (EPA) considered reclassifying fly ash as hazardous waste.219 Although the EPA ultimately opted not to do so in 2010, the regulatory uncertainty led to drops in fly ash use in the US (see Figure 19).220 Conversely, in the Netherlands, the use of clinker substitutes has been facilitated by bans on waste disposal for fly ash and sewage sludge, as well as by a ban on the disposal of concrete waste in landfills. This has encouraged producers of these waste materials to collaborate with cement companies on waste management.221

Regulation is unlikely to substantially improve the availability of fly ash and blast furnace slag in Europe and the US, where overall supplies are decreasing due to shifts in the power and steel sectors.222 However, policy could play a role in encouraging the screening, testing and reprocessing of fly ash and blast furnace slag from older disposal sites. This would increase supplies in the short term while mitigating environmental concerns about those sites.223

Regulation could play a substantial role in increasing the availability of clinker substitutes in the largest concrete-producing countries: China and India

In contrast, regulation could play a substantial role in increasing the availability of clinker substitutes in the largest concrete-producing countries: China and India. Both are projected to have large supplies of fly ash and blast furnace slag,224 even under ambitious emissions reduction scenarios, and neither is currently making the most of this supply. Under the IEA’s B2DS, China and India are expected to reach clinker ratios of 0.55 and 0.50 respectively by 2060.225

Official statistics in China suggest that the country’s fly ash utilization rates are higher than 60 per cent, but a recent analysis by Greenpeace suggests the figure is around 30 per cent.226 Regulation of fly ash takes place largely at the local level, with no specific national regulations.227 The main reason for the deficit seems to lie in the lack of enforcement of existing environmental regulations.

In India, fly ash use has increased steadily, but around 40 per cent remains underutilized.228 A recent paper analysing 16 Indian states suggests that 13 of the states studied require additional support to increase utilization – in the form of adjustments to tax regimes to encourage recycling, as well as better training and access to information.229 In 2016, Maharashtra became the first Indian state to adopt a fly ash utilization policy.230

Trade in clinker substitutes can help overcome local shortages. Cement is cheap but heavy, making it uneconomic to transport very far. As a result, producers have tended to serve local markets within a 200–300 km radius.231 Similar transport distances have applied to clinker substitutes.

However, this is increasingly changing. Although the volume traded still only amounts to a fraction of annual volumes used, trade in blast furnace slag and fly ash has risen almost 166 per cent since 2000.232 Japan is the largest exporter.233 The US and South Korea are among the top five importers.

Blast furnace slag is generally more cost-effective to ship over long distances than fly ash, as it has less volume.234 Moreover, it is typically classified as a product, while fly ash is often classified as a waste material, requiring additional permits to trade.235

From a climate perspective, the benefits of trade in clinker substitutes need to be weighed against the carbon footprint of the transportation involved. However, potential increases in emissions are likely to be small relative to the potential gains from reducing the clinker content per tonne of cement: transporting cement by ship currently emits around 0.010 kg of CO2 per tonne-kilometre.236

Trade may thus allow the likes of the US and Europe to supplement their decreasing domestic stocks of clinker substitutes with supplies from abroad. As importers increasingly look to China and India, a key difficulty will be establishing the necessary distribution networks and supply chain channels in these more fragmented markets.237 In China, for example, there is a mismatch between fly ash utilization in the east of the country, where supplies are high and the construction sector competes for supply with exporters, and low utilization in less developed regions in the west.238

In the medium to long term, fly ash and blast furnace slag availability is likely to decline as the use of coal in the energy sector is reduced and as secondary steel takes a growing share of the steel market. Increasing clinker substitution will therefore require alternative sources of clinker substitutes. Scaling these up needs to start immediately. In this context, there has been a rise in patenting around volcanic rocks and ash and calcined clays for use as clinker substitutes.

Volcanic rocks and ash will become important in regions where these materials are plentiful. Their use depends on local environmental conditions and legislative frameworks.239 They also present a raft of technical difficulties,240 including the fact that quality varies considerably.241 Seventy-five million tonnes of these materials are already used as clinker substitutes every year.242

Studies suggest that calcined clays, in particular, present a significant opportunity to increase clinker substitution around the world, but especially in emerging markets.243 Clays are widely available around the world – although reserves are not always easily accessible and not all clays are suitable for clinker substitution. Those containing kaolinite produce reactive materials when heated (calcined) to 700–850˚C.244

Although only used in a few countries so far, calcined clays have been shown to work at scale. In Brazil, for example, they now make up 3 per cent of the cement market.245 Two reasons calcined clays are not more widely used are that they can be energy-intensive to produce relative to traditional clinker substitutes, although less energy-intensive than clinker,246 and that they typically require additional processing facilities for drying, calcination and grinding.247

This discussion of alternative clinker substitutes is by no means comprehensive. Other novel clinker substitutes are also in use, mainly on a smaller scale, and are discussed in detail in other publications.248 Due to the variety of materials and their dependence on local conditions, obtaining and disseminating enhanced data on their availability, quality and technical characteristics will be key to scaling up their use.

This section looks at what could be done to strengthen the business case for deploying high-blend and novel cements. It explores three disruptive shifts: two from within the market in the form of new service-oriented business models and corporate social responsibility (CSR) initiatives; and one external driver in the form of carbon pricing.

At first glance, the ‘servitization’ concept – wherein an input or product is enhanced by the provision of services or even repositioned as a service in itself – might not seem appropriate for a commodity such as cement.249 Prescriptive standards allow for little differentiation in the product sold, and companies mainly compete on price rather than customer service. However, the largest multinational cement producers are increasingly offering a range of services, from speciality cements to intricate delivery services tailored to complex projects.250

A market geared towards service delivery would likely be a friendlier space for innovative products. Brands might seek to differentiate themselves on the basis of a range of special cements or by tailoring cements to end-user specifications.251 In this context, a company might promote low-carbon cements on the basis of their durability characteristics as well as their sustainability credentials, for instance.

A shift towards a more service-oriented business model might offer the larger cement players new possibilities for value creation during a period in which market conditions have been challenging, and in which the financial performance of firms has been at best mixed.252 Slowing economic growth in China has created a global cement glut. In Europe, there has been an imbalance between high production capacity and low market demand in recent years. At the same time, major cement producers are increasingly facing competition from high-performing regional players in emerging markets.253

Investors are increasingly expecting companies to be transparent about their exposure to climate change risks and how they are managing these

A lot can also be achieved by working closely with companies in the sector to engender disruption from within their organizations. Investors are increasingly expecting companies to be transparent about their exposure to climate change risks and how they are managing these. The cement sector is not immune to this trend and has developed reporting guidelines for climate-risk disclosure. However, a number of the largest firms do not follow them. The continued lack of clear targets for reducing emissions also makes it hard for investors to understand whether cement emissions will in fact decline in line with international targets.254

Firms are also increasingly subject to the demands of local communities. The environmental impacts of limestone mining and cement production in terms of air pollution and soil and water contamination have, for example, led to quarry and production site closures in the Netherlands.255 The scandal surrounding the Lafarge plant that was kept running in Syria during the early stages of the civil war also underlines the increasingly global nature of maintaining a ‘licence to operate’.256

In response to these trends, the Cement Sustainability Initiative (CSI) has brought together major cement producers on a decarbonization platform, most notably improving transparency in respect of progress on different emissions mitigation levers.257 Nine major cement and concrete producers from around the world recently launched the Global Cement and Concrete Association, which intends to promote innovation throughout the construction supply chain.258

There are still large differences between cement producers in terms of emissions intensity, innovation capacity, how ambitious they are in the targets they set, and how supportive they are of regulatory measures to cut emissions.259 LafargeHolcim and HeidelbergCement, for example, already use internal carbon prices of $32 per tonne and $23 per tonne respectively.260 In 2016, Italcementi committed itself to setting a science-based emissions target.261 In contrast, Taiheiyo Cement of Japan and Italy’s Cementir have highly emissions-intensive production processes and their emissions reduction targets are relatively low.262

Although market forces are putting pressure on cement majors to reform policies and operational practices, whether changes are actually likely without firmer regulation remains an open question. Carbon pricing has long been seen as vital for the cement and concrete sector, and policymakers have used it as a tool to create incentives for more action on sustainability.

In Europe, however, most stakeholders agree that the EU Emissions Trading Scheme (ETS) so far has fallen short of its ambitions, particularly with regard to the cement sector.263 Two main problems are generally cited. The first is that carbon prices have been too low to trigger meaningful action. Prices have generally fluctuated between €4/tonne and €8/tonne since the beginning of Phase III in 2013, although 2017 saw prices rise to more than €10/tonne.264 This has been too low to adequately compensate for price differentials between low-carbon cements and conventional Portland cements.265 BYF clinkers, for example, would currently struggle to compete due to higher material costs, but they may be able to compete at a carbon price above €20–30/tonne.266

The second, related, issue is that the supply of free emissions allowances has been too high and has created perverse incentives.267 Critics argue that this has slowed the transition to a low-carbon cement sector by subsidizing the emissions of the largest cement producers in particular: raising their profit margins, locking in existing emissions-intensive production processes and distorting competition.268 Free allocation is supposed to protect domestic industries from being undercut unfairly by those located abroad that are not subject to carbon pricing. The extent to which the cement sector needs this protection has been the subject of considerable negotiation during each phase of ETS reform.269

Against this background, 2017 saw the agreement of Phase IV (2021–30) of the EU ETS. Positive changes have been made, including reforms to make sure allocation levels more closely track actual output; a reduction of the emissions cap by 2.2 per cent every year; and the introduction of an innovation fund to support the deployment of breakthrough technologies.270 However, proposals to end free allocation to cement companies and establish a ‘border carbon adjustment’, whereby European importers of clinker and cement would have to buy carbon allowances, were ultimately rejected by the European Parliament.271

The failure of these latter proposals has contributed to a general perception that the EU ETS is unlikely to bring about meaningful changes in the cement sector, at least in the short term. Member states that are more ambitious in this area, including the Netherlands, Portugal and France, are considering carbon floor prices, following the UK’s approach, which could still affect the sector.272

In the meantime, however, there are lessons for other countries and regions that might hope to promote low-carbon cement through carbon pricing.273 These include the following:

Elsewhere, China approved the first phase of its own emissions trading scheme, which will focus on the power sector, in December 2017.279 Cement will likely be included in the next phase along with a raft of other industrial sectors. The government’s 13th Five-Year Plan (2016–20) also has ambitious targets for cutting overcapacity in the building materials sector.280 These targets may have a larger impact on emissions from the sector than any plans for the emissions trading scheme. In India, the main trading initiative so far has been the Perform, Achieve and Trade scheme, which has already achieved results in the cement sector.281 Significant carbon prices are unlikely in India in the short to medium term.

This section looks at how technical characteristics that hold back the adoption of high-blend and novel cements might be overcome. These characteristics include the following:

These impacts vary considerably depending on the decisions made by those producing cement and concrete. Advances in the understanding of the nanoscale structures of cement are opening up new ways to improve the performance of concrete. For example, many high-blend and novel cements display slower early-stage strength development than Portland cement but achieve higher compressive strength and superior durability later on. Using nanotechnology, researchers are experimenting with modifying particle size and distribution through grinding and packing to enhance early-stage strength development.284

Chemical admixtures can also be used to influence the technical characteristics of low-clinker and novel concretes. Dispersants such as plasticizers and superplasticizers help with ease of application by lowering the amount of water needed to make concrete flow well and enabling higher levels of clinker substitution. Admixtures can also address durability concerns.285 Moreover, decisions taken when mixing concrete (which aggregates to use, what size and in what proportion) can mitigate impacts.286

Using several clinker substitutes in combination in ternary cements can also improve overall performance.287 Combining limestone filler and fly ash, or limestone filler and blast furnace slag, can result in a high-durability concrete.288 With advances in this area, clinker substitution increasingly becomes not just a cost-saving or sustainability measure but also a means of optimizing performance and outperforming traditional concrete.

However, this type of optimization is currently only practical in advanced production settings – i.e. in plants where additional grinding equipment can be used, and where workers have access to chemical admixtures and have the requisite skills and knowledge to take these decisions. The vast majority of concrete production in emerging markets is done on site by workers who lack training and specialist knowledge.289

This is an area in which digitalization will have an important role to play. Digital tools could be used to disseminate best practice for optimizing a particular concrete mix consisting of locally available materials, or to allow a worker on site to quickly call up details on the compatibility of a given SCM with a given admixture. Better dissemination of know-how will be a key factor in facilitating the use of higher-blend and novel cements in emerging markets.

There may not be a single low-carbon cement that provides all the functions that Portland cement does. However, given the advances in optimizing the properties of concretes, and given the range of different applications for cement – from mortar and concrete blocks to reinforced concrete – a single cement that provides all of these functions may not be needed.

Prescriptive standards require that novel products match the characteristics of Portland cement for the majority of applications, even when this might not be necessary

The current ‘one size fits all’ approach poses a considerable barrier to the use of alternative cements; prescriptive standards require that novel products match the characteristics of Portland cement for the majority of applications, even when this might not be necessary. Carbonation, 290 for example, is only a problem for a subset of concrete applications – the 25 per cent of concrete used in reinforced concrete – but most standards require the majority of cements to be carbonation-resistant.291

This approach also precludes flexibility in accommodating local differences in climate and soil conditions, variances that make novel compositions more or less viable in some locations. In Japan, for instance, where buildings have to withstand earthquakes, strength and durability are particularly important.292 In Scandinavia, structures have to withstand extreme temperatures in winter.293 Conversely, in places unlikely to have to endure regular tremors or extreme temperatures, more buildings could be built using high-blend or novel cements.

In this context, stakeholders have called for a shift away from prescriptive standards towards those that focus instead on whether a cement can demonstrate a performance sufficient for a given application in a given context. Belite-rich clinkers, for example, have been used in large concrete dam projects in China where strength gain after a few days is not as important as it might be on a typical construction project.294 Ideally, solutions would allow the lowest-carbon cements to be matched to their most viable use-cases, with higher-carbon cements reserved only for those applications where they might still be needed.

Application-oriented, performance-based standards in cement would need to be complemented by equivalent standards for concrete, as well as by changes in construction and infrastructure codes (and vice versa), as such rules provide separate but interlinked levels of certification. According to industry stakeholders, concrete standards generally pose a greater barrier than cement standards to the use of high-blend cements.295 In Norway, for example, CEM I (>95 per cent Portland clinker) is the only cement allowed in most concrete applications.296

The degree to which prescriptive standards are considered a barrier to innovation in the composition and production of cement depends on the low-carbon cement in question, and whether one believes that a specific cement could be used for mainstream applications or will remain a niche product.

Application-specific flexibility already exists for some niche products, as certain applications do not require standards. CCSC cements, for example, are currently restricted to precast concrete articles, which can be sold under local technical approvals and do not necessarily require standardization at national level.297 In Europe, the European Organization for Technical Assessment route allows manufacturers to put forward novel products not covered by existing standards to be independently assessed and validated.298 Finally, if a construction company needs a niche type of cement for a given application or simply wants to use it, the firm can generally acquire special permission to do so.299

More fundamental barriers prevent high-blend or novel cements from becoming mainstream products everywhere; the most notable is the lack of local availability of raw materials (see sections 2.3 and 3.1). For example, if CSA clinkers are not deployed at scale due to their cost and the limited availability of bauxite, and if they can be used in niche applications in certain places regardless of this, then it may prove less important to develop national standards for their use.

Given the shift towards a more service-oriented business model, it is reasonable to ask whether there will even be such a thing as a mainstream cement product in the future. A more diversified cement market, no longer dominated by Portland cement but instead made up of a broader set of bespoke products, would require a paradigm shift in standardization. Moreover, as explored in the next chapter, structural shifts in practices in the construction sector could result in the emergence of completely new requirements for building materials. For example, would early-stage strength development be more or less important in a building site populated by robots? On the one hand, a company may be better able to afford irregular working shifts and longer gaps between shifts if it is using robots rather than paying workers’ salaries, and safety concerns may be diminished. On the other hand, construction work may speed up with the ability to work through the night, and waiting longer to demould concrete may be even less viable than it is today.

One of the main challenges for performance-based standards is the current lack of rapid and accurate tests to predict the performance of novel concretes over their lifetime.300 In many cases, high-blend and novel cements have not been in use for long enough to have accumulated the decades of in-service data to ‘prove’ their durability; at the same time, predictive models are treated with scepticism.301 However, advances in material analytics, nanotechnology and characterization techniques (including atomic force microscopy, scanning and x-ray diffraction) are transforming the understanding of the chemistry of concrete formation.302 In addition, standards bodies are developing faster testing methods specifically for high-blend cements.303

Building up trust in the durability of new materials will also require a shift to greater in situ testing of materials and monitoring of structures throughout their operational life cycles.304 Developing user-friendly diagnostic tools, and field-based detection tools that provide rapid results, will be key. Increased collection and dissemination of data on in-service performance could dramatically speed up the understanding of novel products and their impact on concretes, allowing the improvement of existing tools and the development of new ones to accurately predict the properties of concretes. Similar developments in the water industry have led to a move away from sample-based water quality measurement to in-line continuous measurement, i.e. measurement where sensors or instruments are situated in a water flow-through system.305

Finally, the traditional route of pilot/demonstration projects will remain an important way to build confidence in novel products. Most of the innovative products considered above are moving through the typical steps from early use in non-structural, low-risk applications to large-scale demonstration in structural applications.306

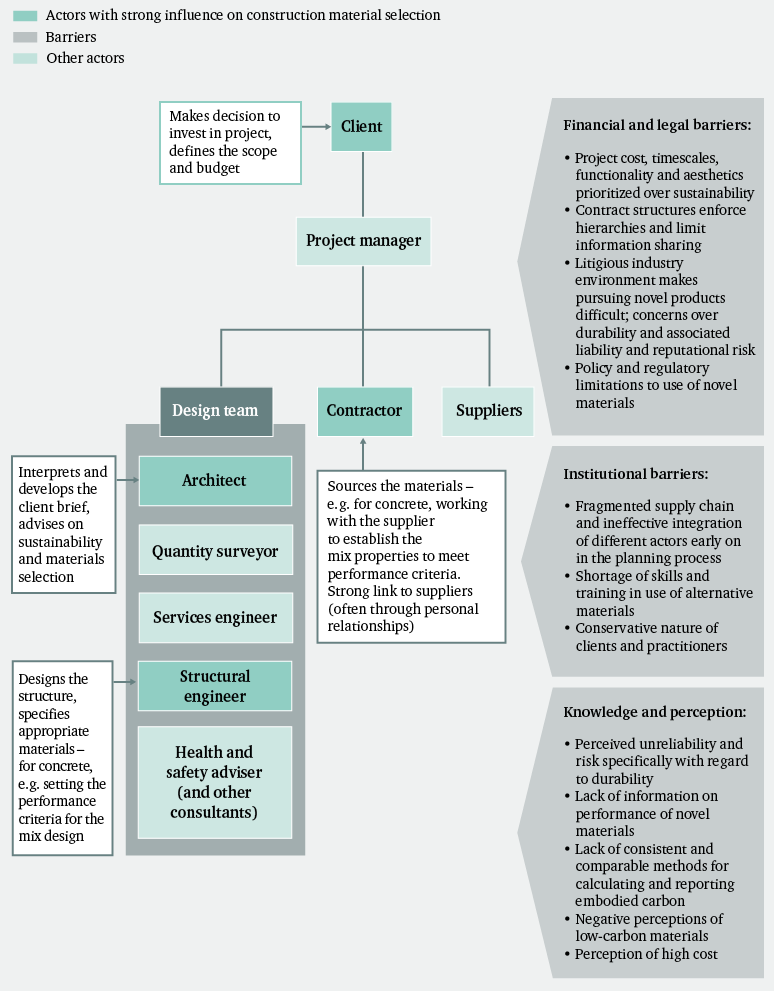

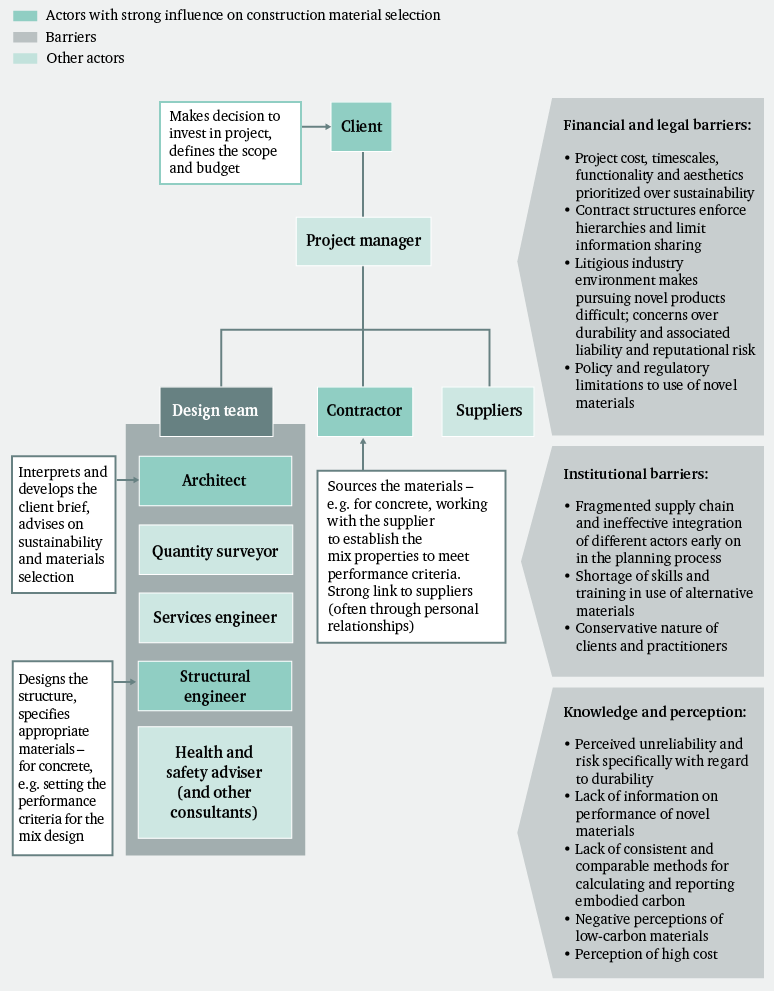

To overcome customer resistance to high-blend and novel cements, buy-in is needed across a range of stakeholders: from the client who commissions a project to the design team that implements it to the end-user who inhabits or works in a given building. However, four sets of actors have a particularly strong influence over material selection in construction projects: architects, clients, structural engineers and contractors (see Figure 20).307

This section therefore focuses on shifting the preferences and incentives of these groups of actors through three entry points: the development of better indicators, alongside stricter regulation; enhanced coordination through digitalization; and endorsement and activism by early-mover consumer groups.

As will be discussed in Chapter 4, a wide variety of sustainable material options exist outside of the cement and concrete paradigm. This section, therefore, more broadly addresses the need to increase demand for innovative building products and does not limit the discussion to low-carbon concretes.

Enhanced information could be key to enabling more sustainable approaches. Addressing knowledge and perception barriers, for instance, depends on access to good-quality information on lower-carbon materials. A commonly cited concern is the lack of simple and consistent indicators to compare different construction materials based on their embodied carbon.308

The number of tools for calculating and comparing embodied carbon levels has proliferated in recent years.309 In the Netherlands, the Milieu Kosten Indicator expresses the economic cost associated with the environmental impacts of a material.310 More broadly, Environmental Product Declarations (EPDs) communicate information about the life-cycle environmental impact of products.311

However, there are still huge inconsistencies in the data used and the outcomes of different assessments.312 Although several national EPD databases exist, these are largely voluntary and there is a lack of globally comparable benchmarks for materials.313 Credible benchmarks are difficult to establish as projects are extremely site-specific.

Developing good indicators will require more robust data gathering over years. The following steps could help speed this along:

Legislation can play an important role in shifting stakeholder approaches. In the UK, for example, the focus of building regulations on operational efficiency320 – i.e. the energy use of a building over the course of its lifetime – has helped shift the concept of operational-carbon metrics from a niche consideration to a mainstream one.321

Better information and tools are only the first step towards sustainability becoming a widely established factor in material selection

Policymakers may also pursue stricter regulatory options by, for example, limiting the embodied carbon allowed in the construction of certain types of buildings. Local authorities could make planning permission contingent on a building design meeting certain targets on embodied carbon. Regulation also has an important role to play in shifting the industry’s financial incentives. Tax cuts or business-rate reductions for buildings that meet a given embodied-carbon grade, or cuts in value-added tax (VAT) for low-carbon materials, could help change the financial calculus of those using these materials.

The choice of materials for a project is highly site- and application-specific. Given this, it is important to ensure that regulations are not too prescriptive. Instead, they need to guide consumers towards choosing more sustainable options while allowing them to find the most appropriate option for a given project. Rather than taxing a particular material, for example, clients might be incentivized to comply with a maximum embodied-carbon threshold for a given structure. Ultimately, the design of such policies will be subject to local conditions. However, improvements in data sharing and the lessons learned from this process will be a global effort.

Better information and tools are only the first step towards sustainability becoming a widely established factor in material selection. A further key barrier to tackle is the fragmented nature of the supply chain.322

Reflecting this, there has been growing interest in software tools such as building information modelling (BIM), which allows users to build a data-rich, computer-generated model of a building. Structural engineers and architects are using BIM to explore the optimal design and materials for a given building at the very beginning of a project.323 BIM also helps to communicate decisions to the client, the contractor and suppliers.

Although BIM is not directly aimed at promoting low-carbon materials, it may help to challenge perceptions of, and guide decisions about, the use of novel materials.324 Integrating embodied-carbon calculations into BIM, for example, could allow architects and structural engineers to see how their design is performing against similar buildings and how their choice of materials is affecting the embodied carbon of their design. This would also help to build familiarity with these metrics.

In order to be effective, however, BIM has to be used by a wide set of stakeholders at different points along the value chain. Questions have been raised as to whether BIM is likely to achieve widespread acceptance beyond design teams. In theory, manufacturers of materials can also link into BIM platforms, receiving data about product specifications and also uploading embodied-carbon data for their own products (in order to compete for contracts on the basis of those data). However, evidence suggests that uptake in the concrete sector has been slow.325

Improving BIM to offer the right kind of services to material suppliers and accelerating its uptake will be part of the solution. But addressing weak links in the supply chain will require more traditional forms of stakeholder engagement in the meantime: for example, training sessions to encourage design teams and contractors to work directly with material producers to better understand their products and overcome concerns about performance and costs.326

In the absence of strong regulatory and financial drivers, motivated groups of clients who are in a strong position to innovate or possess strong agenda-setting power have a particularly important role to play in setting targets at a regional and global level, as well as in demanding more innovative solutions from their suppliers. This section considers two such groups: governments; and companies with ambitious CSR commitments.

Governments spend a huge amount on construction every year, and are in prime positions to drive the development of markets for low-carbon building materials.327

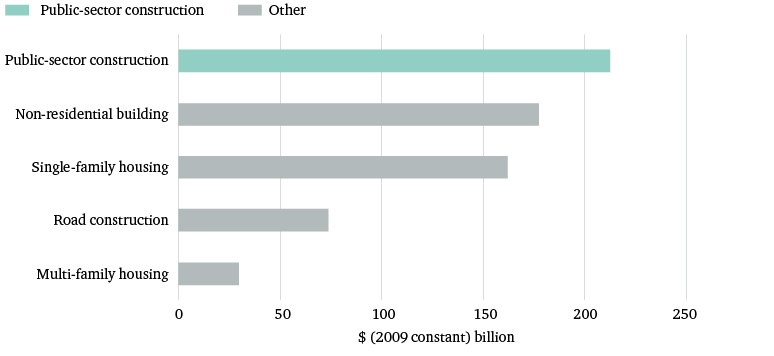

The public sector’s share of construction spending varies considerably by country. In the US, it made up 32 per cent of the total in 2014 (see Figure 21). In the UK, it accounts for around 40 per cent per year.328 In China, approximately 20 per cent of all construction spending involves public-works projects, and the central government and regional governments are responsible for the majority of infrastructure spending.329

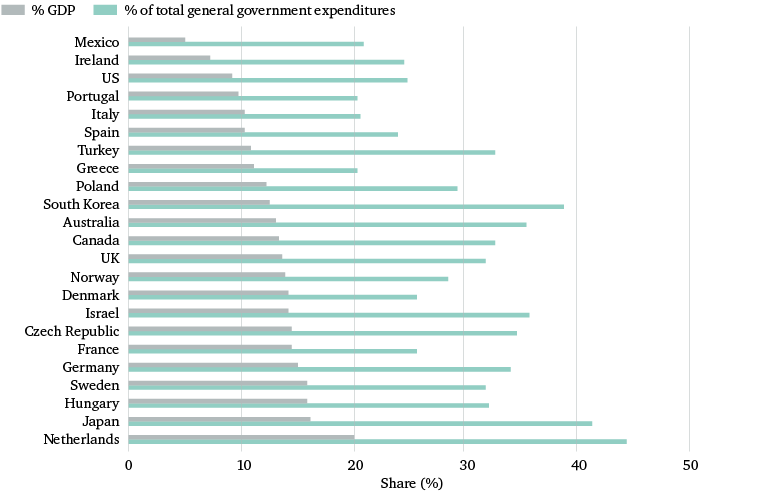

Given the spending power of the public sector, there has been an increasing focus on public procurement of low-carbon building materials.330 In the Netherlands, for example, where public procurement is comparatively high (see Figure 22), the government uses a tool called DuboCalc that gives suppliers a reduction in the price of their bid based on how ‘clean’ it is. Proposals with lower environmental impacts will have a competitive advantage over other proposals.331 This has increased demand for low-carbon cement among local authorities and housing corporations.332

Moreover, the embodied-energy and -carbon indicators and digital tools discussed above can be integrated into public procurement strategies. Governments can set maximum embodied-energy and -carbon levels in public tenders or set targets for public agencies to meet.333 Since May 2015, the United Arab Emirates has required all major infrastructure projects to use cements that contain at least 60 per cent blast furnace slag or fly ash.334 In the UK, a requirement to use Level 2 BIM on centrally procured public projects has been in place since April 2016.335

Although it is widely accepted that public procurement is a valuable tool, it is not always easy to implement. The amount of money involved and the financial interests at stake mean that corruption is a common problem in construction-related public procurement, even in developed economies.336 This can be exacerbated in cases where sustainability is integrated into the process, as the more complex a process is, the more vulnerable it becomes to manipulation and corruption.337 Good governance, fair and transparent procurement procedures, and clear practices regarding the prosecution of corruption are all key to establishing a corruption-resilient procurement environment.338

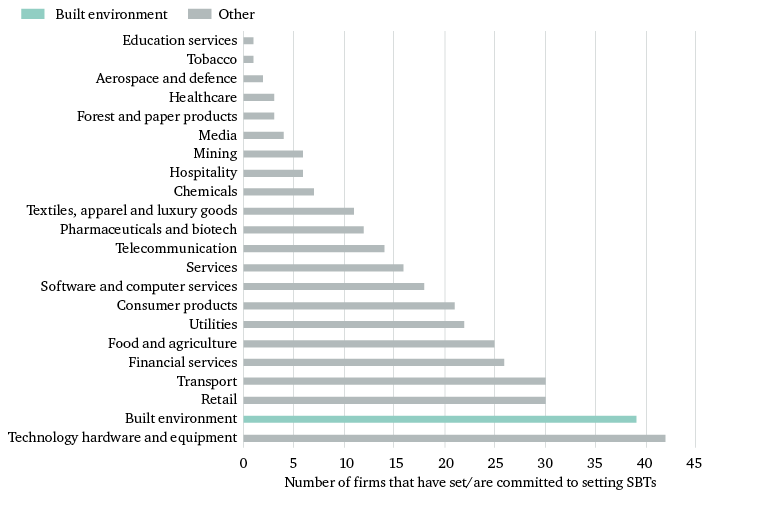

The second group of early-mover consumers consists of commercial clients motivated by CSR commitments. There are now 39 built-environment firms that have either set or committed to setting science-based targets (SBTs) (see Figure 23).339 Landsec’s SBT, for example, commits the UK-based property developer to reducing greenhouse gas emissions by 40 per cent per square metre by 2030 on 2014 levels. It also requires the firm to encourage contractors to set SBTs so that the embodied carbon of key materials can be reduced.340

A growing number of construction clients are also setting carbon-intensity targets for their projects and supply chains. There is huge potential for more firms to adopt such targets voluntarily, as well as for targets to be introduced through regulatory means. Major companies could also band together, along the lines of the RE100,341 to set commitments to lower the embodied carbon of the construction materials they use or procure. Given the collective purchasing power of these companies, this could generate significant market appeal for low-carbon products.

Although the cement and concrete sector is only at the early stages of digital transformation,342 there is growing interest in the role that digital tools could play in overcoming barriers to low-carbon innovation. Many of the barriers discussed above require action that involves matching solutions to local conditions, and improving coordination and communication – areas where digital technologies have significant advantages. Throughout this chapter there are examples of digital tools already starting to play an important role.

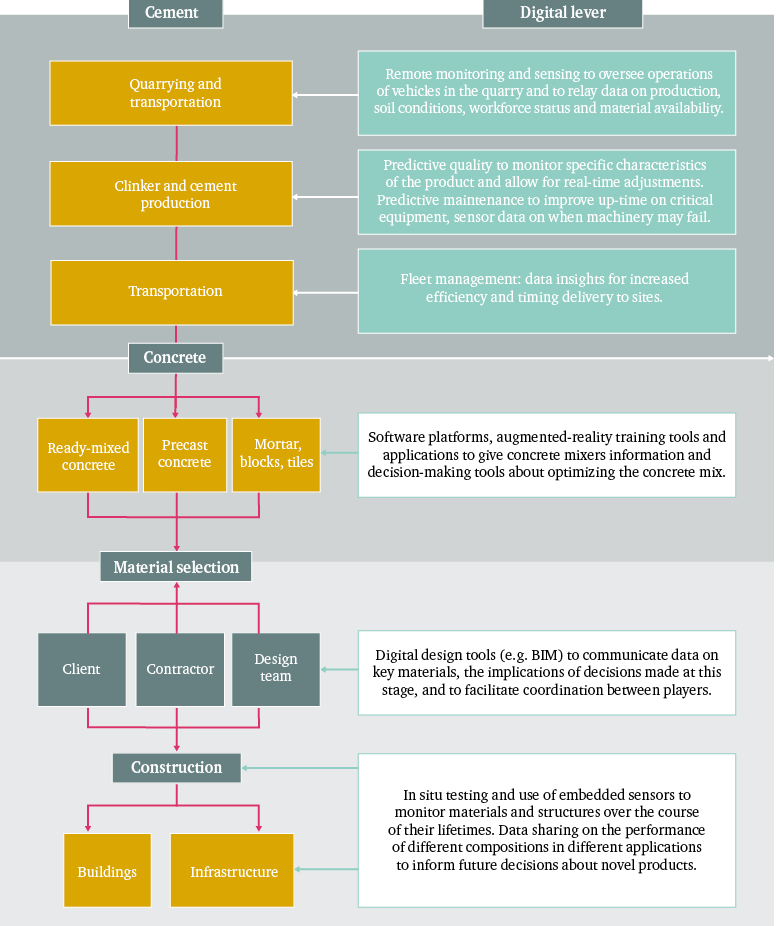

Figure 24 summarizes these examples and introduces new cases, some of which are more ground-breaking than others. The turquoise shading indicates examples already likely to be in place for most industrialized cement producers – for example, for modern quality control and fleet management. The areas shaded in white indicate examples where digital solutions are not yet widespread.

Digital disruption could help disparate and apparently incremental changes across the cement and concrete sector to deliver system-level optimization and deep decarbonization. For instance, analytics could be used to predict product characteristics for a given mixture in a given climate and for a given use (the number of factors involved and the need for very-fine-tuning suggest that machine learning is well suited to tackling this problem). Remote sensing could help track and record the performance of different concretes over time. Augmented-reality and information-driven decision tools, when used on site, could enable an individual worker mixing concrete to make the best decisions for a given context.343

There are many entry points for innovative practices and materials, but all depend on better data collection and, crucially, on making the data available to a range of market participants, including new players. The importance of digital disruption will also depend on the degree to which it reshapes the largest cement markets: China and India.

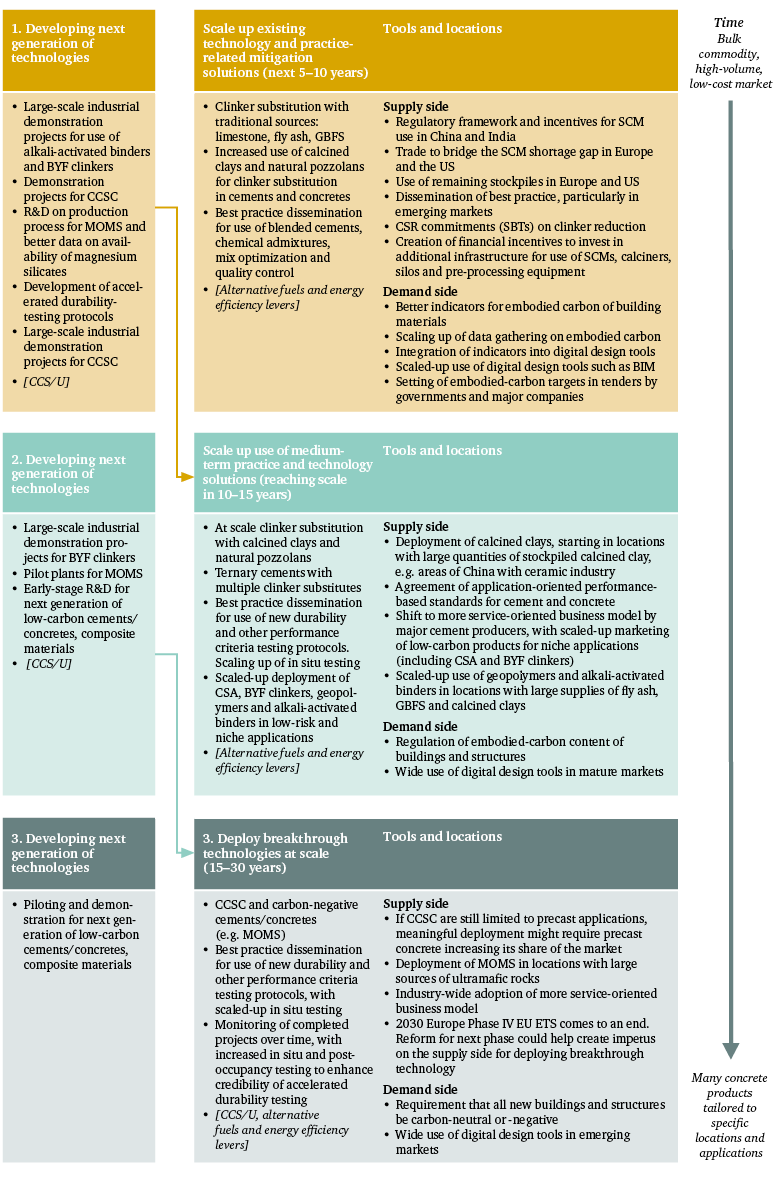

This chapter has highlighted the potential of several solutions to overcome the current barriers to wider deployment of clinker substitution and novel-cement technologies. It has also set out the conditions under which different solutions might be more or less valuable, and over what time frame their uptake within the industry might occur. In this context, three factors are important to consider: the interplay between different technologies considered in this report, the interplay between the solutions set out above, and the key locations that need to be targeted for deep decarbonization to occur.

Early action is needed on readily available mitigation options to maximize their emissions-reduction potential

Early action is needed on readily available mitigation options to maximize their emissions-reduction potential, and to bridge the gap until more innovative early-stage technology options are available.344 In practice this would mean scaling up clinker substitution by using the materials available today, improving distribution networks for them, and optimizing the use of these networks. It would also require expanding the use of alternative fuels and adding to improvements in energy efficiency.

However, a short-term focus on the solutions currently available should not delay long-term efforts to advance potential breakthrough technologies such as novel cements and CCS. The challenge is that there may be limited incentive for cement makers to invest in novel cements while approaches such as clinker substitution still have a lot to offer and are cheaper and quicker to bring to market. Similarly, progress on alternative fuels and clinker substitution could reduce the total amount of CO2 from cement production available for capture relative to the capital cost of CCS, with the result that investing in CCS may seem less worthwhile.

Even clinker substitution may reach the limits of its commercial and practical viability relatively quickly, particularly with fewer traditional sources available. Moreover, the use of alternative fuels is likely to become increasingly expensive.345 In this context, and given the importance of deep decarbonization in the sector, industry-wide adoption of novel cements and CCS would still be worthwhile. A parallel track, therefore, will be needed to accelerate the development and commercialization of technologies such as novel cements and CCS.

The timing of policy solutions relative to one another is also a key factor. Uptake of application-oriented, performance-based standards depends on the development of improved and accelerated durability-testing protocols. The introduction of digital tools that familiarize stakeholders with the methods for assessing embodied-carbon metrics would be an important, though not essential, precursor to setting regulations limiting embodied-carbon content in infrastructure.

Finally, it is important to think about where the biggest markets will be, and thus where novel technologies and solutions are likely to have the greatest disruptive and decarbonization potential. As China, India and other emerging markets will continue to make up the bulk of future demand for cement,346 it is essential that low-carbon innovations are cheap and easy to use, and that relevant players in those markets have access to the requisite information to make use of new products.

Figure 25 introduces a staged approach to the introduction of these different technologies and solutions. It highlights how we might move from the current bulk, high-volume, low-cost commodity market to one characterized by tailored solutions with the potential for increased value added through ‘cement as a service’ offerings.