It is important for policymakers in the EU to control the types of biomass feedstock used – and supported by policy frameworks – in order to limit negative impacts on the climate.

Demand and Supply in Selected EU Member States

Research paper

Published 7 June 2018

Updated 14 December 2020

ISBN: 978 1 78413 267 5

It is important for policymakers in the EU to control the types of biomass feedstock used – and supported by policy frameworks – in order to limit negative impacts on the climate.

In 2016 (the latest year for which figures are available), the countries analysed in this paper were nine of the 11 largest consumers of energy from solid biomass for power and heat in the EU.234 Between them they accounted for 75 per cent of EU28 electricity generation, and 71 per cent of EU28 heating and cooling consumption, from biomass. Their experiences so far, and the prospects for the future development of biomass energy in these countries, thus provide a good indication of how EU consumption of biomass energy as a whole is likely to develop.

As discussed in chapters 3–11, all of these countries provide government support for energy from woody biomass, among other renewable technologies, through a mixture of feed-in tariffs or premiums, quota obligations on energy suppliers, tender or auction schemes for contracts at above-market prices, fiscal incentives such as grants or tax breaks (particularly in Scandinavian countries with energy and emissions taxes), and support for grid connections and installations. This mixture of measures, and frequent policy changes in many of these countries, make it extremely difficult to calculate exactly how much support, in monetary terms, has been delivered in practice, and how this compares with the support given to other renewables, but a rough idea can be gained from the growth rates in tables 16 and 17 below, particularly when compared with growth in renewable electricity and heat across all technologies. The UK in particular has seen a rapid growth in the use of biomass for both power and heat (Romania has seen the fastest rate of growth in electricity generation, but from an extremely low base).

Table 16 summarizes, for the EU28 and each of the nine countries analysed in this paper, electricity generation from solid biomass in 2009 and 2016, its average annual rate of growth over that period, and the proportion of total electricity and of renewable electricity generation it accounted for in 2009 and in 2016.

In each of these nine countries, except Sweden, biomass provided a larger proportion of total electricity generation in 2016 than it did in 2009. This is because the consumption of renewable electricity as a whole has increased, in line with countries’ efforts to meet their Renewable Energy Directive targets. In five of the nine countries, however, and in the EU28 as a whole, biomass provided a smaller proportion of renewable electricity in 2016 than it did in 2009, and in three countries (Finland, France and Romania) only a slightly higher proportion. Only the UK has seen a substantial increase in the generation of electricity from biomass both in absolute terms and as a proportion of electricity from renewable sources.

|

Electricity from biomass |

Biomass as share of total electricity (%) |

Biomass as share of renewable electricity (%) |

|||||

|---|---|---|---|---|---|---|---|

|

2009 (Mtoe) |

2016 (Mtoe) |

Av. annual growth 2009–16 (%) |

2009 |

2016 |

2009 |

2016 |

|

|

EU28 |

5.22 |

7.86 |

6.0% |

1.9% |

2.8% |

10.0% |

9.5% |

|

Denmark |

0.17 |

0.30 |

8.3% |

5.4% |

9.8% |

19.2% |

18.2% |

|

Finland |

0.72 |

0.91 |

3.4% |

10.1% |

12.1% |

36.5% |

36.7% |

|

France |

0.11 |

0.26 |

13.9% |

0.2% |

0.6% |

1.6% |

3.1% |

|

Germany |

0.82 |

0.93 |

1.9% |

1.6% |

1.8% |

9.5% |

5.7% |

|

Italy |

0.24 |

0.35 |

5.5% |

0.8% |

1.3% |

4.5% |

3.7% |

|

Poland |

0.42 |

0.59 |

5.0% |

3.3% |

4.1% |

56.5% |

30.8% |

|

Romania |

0.00 |

0.04 |

72.8% |

0.0% |

0.8% |

0.1% |

1.8% |

|

Sweden |

0.87 |

0.84 |

-0.5% |

7.2% |

6.8% |

12.3% |

10.4% |

|

UK |

0.31 |

1.69 |

27.2% |

1.0% |

5.5% |

14.5% |

22.5% |

Source: Eurostat SHARES database, http://ec.europa.eu/eurostat/web/energy/data/shares.

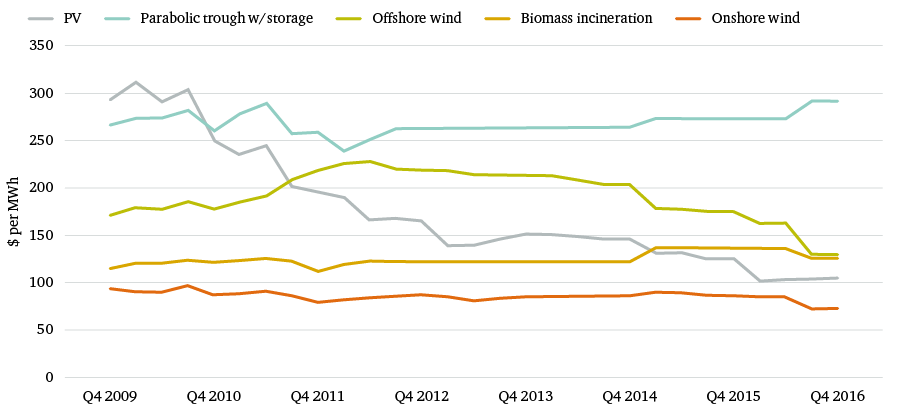

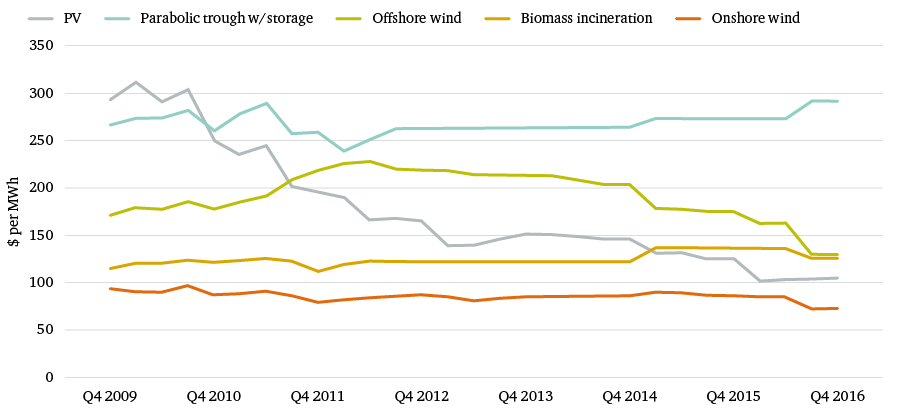

The main reason behind this slower growth of biomass power than of renewable electricity overall is the significant falls in the costs of competing renewable technologies, particularly solar PV and wind. While, on a global scale, in 2014, the levelized costs of electricity from biomass were slightly lower than those of solar PV and roughly the same as onshore wind, biomass combustion technologies are relatively mature, and therefore have a lower cost reduction potential. In 2016, the International Renewable Energy Agency (IRENA) projected a possible reduction in biomass costs of 10–15 per cent by 2025; in contrast, it anticipated a 59 per cent fall for solar PV, and 26 per cent for onshore wind, by the same date.235 Like most forecasts of the costs of renewables, these latter two figures now seem certain to be underestimates. During 2016 alone the cost of solar PV fell by 17 per cent, onshore wind by 18 per cent and offshore wind by 28 per cent (see Figure 32).236

In September 2017, the UK’s second Contracts for Difference auction saw two offshore wind contracts agreed at a strike price less than half the average price delivered by the industry in the first auction just two years earlier, and close to the market price of electricity (i.e. close to being free of subsidy).237 In April 2017, DONG Energy won two contracts in a German auction for offshore wind at a subsidy rate of zero (though this excludes some of the costs of connecting to the grid, which are included in the UK contracts). In June 2017, Bloomberg New Energy Finance projected the cost of offshore wind to decline by a further 71 per cent by 2040.238

Although biomass is being out-competed, in cost terms, by other renewable technologies, it has the advantage over solar and wind of being dispatchable: i.e. it is a source of electricity that can be dispatched at the request of power grid operators or of the plant owner. Biomass plants can adjust their power output according to need (while stopping and starting a biomass power plant is a costly and inefficient process, adjusting the power output of an operating plant upwards or downwards is much less so); solar, wind (and hydro, apart from pumped hydro storage) are there or not, depending on the conditions. The role of biomass in balancing the renewable energy system may become more important as countries steadily increase the share of solar and wind in their energy mix – though there are of course alternatives, including a greater degree of interconnection with other countries’ grids, battery storage (where costs are also falling sharply) and other storage technologies. This question will be examined in more detail in the forthcoming Chatham House paper, Woody Biomass for Power and Heat: Global Demand and Supply.

Table 17 summarizes, for the EU28 and each of the nine countries analysed in this paper, heat consumption from solid biomass in 2009 and 2016, its average annual rate of growth over that period, and the proportion of total heat and of renewable heat consumption it accounted for in 2009 and in 2016.

Across the EU as a whole, and in every one of the nine countries analysed here, the share of biomass has risen as a proportion of total heat consumption. As with electricity, this is because of the general expansion of renewable energy encouraged by the Renewable Energy Directive targets. Throughout the EU biomass still dominates renewable heat; the smallest proportion of consumption from biomass in these nine countries is 67 per cent, in Germany, and it is over 90 per cent in Finland, Poland and Romania. Unlike the situation with electricity generation, alternatives to biomass for renewable heat have tended to be less well commercialized, at least to date. In addition, in many countries biomass has always been an important source of heating, particularly in rural households, even before the introduction of policies supporting renewable energy. Furthermore, in several of these countries, particularly Finland and Sweden, an important part of biomass heat consumption is accounted for by the production and consumption of black liquor in the pulp and paper industry.

However, alternatives to biomass for renewable heat – mainly heat pumps, solar thermal and biogas – are now beginning to find wider markets, which helps to explain why, in both the EU as a whole and in all nine countries analysed here, biomass fell as a share of renewable heat between 2009 and 2016, though in most cases by a relatively small amount. (The largest proportionate fall, in the UK, is a reflection more of the lack of development of all renewable technologies before 2009 than of any move away from biomass; in fact the UK has also seen the fastest rate of growth of heat consumption from biomass of any of these nine countries, though from the lowest base.) This is a slow development, however, so for all the reasons outlined above, biomass is likely to remain the dominant source of renewable heat throughout the EU; other technologies will expand faster, but from a much lower base. The implementation of energy efficiency improvements in buildings may also reduce the demand for heating from all sources.

|

Heating and cooling from biomass |

Biomass as share of total heating & cooling (%) |

Biomass as share of renewable heating & cooling (%) |

|||||

|---|---|---|---|---|---|---|---|

|

2009 (Mtoe) |

2016 (Mtoe) |

Av. annual growth 2009–16 (%) |

2009 |

2016 |

2009 |

2016 |

|

|

EU28 |

66.88 |

77.91 |

2.2% |

12.6% |

15.0% |

84.6% |

78.4% |

|

Denmark |

1.72 |

2.35 |

4.5% |

22.3% |

31.1% |

75.5% |

74.5% |

|

Finland |

5.34 |

6.90 |

3.7% |

40.6% |

48.8% |

94.1% |

91.0% |

|

France |

8.28 |

9.82 |

2.5% |

12.4% |

15.7% |

81.9% |

74.4% |

|

Germany |

7.22 |

9.57 |

4.1% |

6.9% |

8.7% |

74.5% |

67.2% |

|

Italy |

7.79 |

7.12 |

-1.3% |

12.6% |

12.8% |

76.5% |

67.6% |

|

Poland |

4.11 |

5.17 |

3.3% |

11.3% |

13.9% |

98.1% |

94.5% |

|

Romania |

3.75 |

3.47 |

-1.1% |

26.3% |

26.5% |

99.3% |

98.8% |

|

Sweden |

7.11 |

7.85 |

1.4% |

51.9% |

54.7% |

81.6% |

79.8% |

|

UK |

1.22 |

2.86 |

12.9% |

2.1% |

5.1% |

90.7% |

73.1% |

Source: Eurostat SHARES database, http://ec.europa.eu/eurostat/web/energy/data/shares.

A possible inhibiting factor, however, is the concern increasingly being expressed over the impacts on local air quality and human health of the use of biomass for household heating and other purposes. A study published in 2018, for example, estimated that exposure to smoke from domestic biomass use caused, among other impacts, at least 40,000 deaths across the EU28 in 2014, together with more than 130,000 cases of bronchitis, more than 20,000 respiratory and cardiac hospital admissions and 10 million working days lost.239 More than 1,300 deaths a year were linked to air pollution from 27 biomass burning power stations across the EU. This topic is not considered in this report, which focuses on the impacts of biomass use on emissions of carbon dioxide and thus on climate change (though particulate emissions, or ‘black carbon’, also accelerate climate change), but should be borne in mind when considering future demand for biomass.

EU member states’ National Renewable Energy Action Plans, drawn up in response to the 2009 Renewable Energy Directive, projected that bioenergy would account for 12 per cent of total European energy consumption by 2020, more than half of the 20 per cent target set for energy from renewable sources.240 This implies continued rapid growth between 2016 and 2020, but according to projections published by the European Commission in November 2016, accompanying the new draft Renewable Energy Directive, further significant growth beyond 2020 seems less likely, due mainly to the fall in price of competing renewables and anticipated improvements in energy efficiency.241 One of the models used by the Commission, the Price-Induced Market Equilibrium System (PRIMES), projected a 27 per cent increase in bioenergy use between 2015 and 2020, followed by a 4 per cent increase between 2020 and 2030. Another model, Green-X, had a somewhat different trajectory suggesting that total bioenergy demand will be lower than the level projected by PRIMES in 2020, but would increase by 17 per cent between 2020 and 2025, and then remain flat until 2030.

Nevertheless, as can be seen from the country analyses, further growth in biomass use for energy can be expected at least until 2020, under the current policy framework. Projections of the EU’s ability to meet this continued growth in demand from its own forests are uncertain, depending on, among other factors, the future development of industries that compete for raw materials (such as the construction industry) and the potential for increased use of wood, agricultural residues and waste wood as well as the growth of energy crops. All three models used by the Commission to estimate supply projected increased use of roundwood and increased harvesting rates in forests (alongside growth in the use of agricultural residues); this is consistent with the country analyses in this paper. One study estimated that, if the EU was to achieve its aim of providing 27 per cent of its energy consumption from renewable sources by 2030, the amount of biomass it would need was equivalent to the total EU wood harvest for all purposes in 2015.242

All projections also assume a growing role for imports, particularly from North America and Russia, but also potentially from non-EU Europe (e.g. Belarus, Bosnia and Herzegovina, and Ukraine) and from Latin America. This also depends on demand for woody biomass in those countries, for energy and for other purposes, and pressure on land use. As noted in Chapter 11, a 2017 analysis of the availability of biomass feedstock to the UK concluded that 70–90 per cent less biomass was likely to be available from imports than had previously been projected, partly because of limited global availability of land for biomass and competition for biomass supplies.243 Imports may thus be less significant – and future growth in supplies more constrained – than the estimates above suggest. This topic will be discussed in more detail in the forthcoming Chatham House paper, Woody Biomass for Power and Heat: Global Demand and Supply.