This paper recommends a framework for strengthening US–EU trade relations and achieving successful trade talks in the current era of protectionism.

Which Way Forward?

Research paper

Published 8 March 2019

Updated 14 December 2020

ISBN: 978 1 78413 313 9

This paper recommends a framework for strengthening US–EU trade relations and achieving successful trade talks in the current era of protectionism.

Less than a fortnight before agreeing the trade truce with Juncker, Trump had called the EU a ‘foe’ of the US for ‘what they do to us in trade’.24 He has since also claimed that the EU ‘was formed in order to take advantage of us on trade’.25 While these statements are both incendiary and factually incorrect, some concrete concerns raised by the Trump administration have a kernel of truth.

President Trump has prioritized reducing the US trade deficit and tackling unfair trade practices. He blames the EU for the US’s trade deficit with the bloc and with certain of its member states.

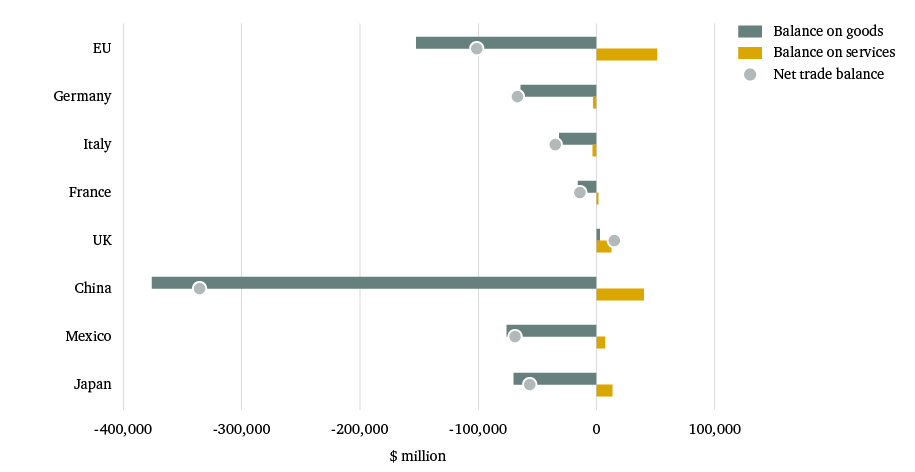

The US’s overall trade deficit with the EU has widened since 2009. In 2017 it stood at $101.2 billion – with the trade deficit in goods ($152.6 billion) partially offset by the trade surplus in services ($51.4 billion).26 The trade deficit with the EU as a bloc is the US’s second largest after China ($335.7 billion in 2017). A key driver is the US’s trade deficit in goods with Germany, which reached $64.1 billion in 2017; the overall deficit with that country being $66.7 billion, or nearly two-thirds of the EU total.27

President Trump is highly critical of Germany over trade, and has repeatedly taken to Twitter to denounce the country’s trade surplus. Other EU member states – notably Italy and France – with which the US runs overall trade deficits have so far largely remained off Trump’s radar.

President Trump is highly critical of Germany over trade, and has repeatedly taken to Twitter to denounce the country’s trade surplus.28 Other EU member states – notably Italy and France – with which the US runs overall trade deficits (see Figure 1) have so far largely remained off Trump’s radar. When bemoaning the trade deficit, Trump is usually focused solely on merchandise trade. He ignores the overall US trade surplus in services. However, in the case of Germany (and also Italy), the US runs a trade deficit in both goods and services.

Most economists agree that while global trade imbalances matter, Trump’s focus on the bilateral trade deficit is misplaced. The US trade deficit is not driven by a specific country’s (or bloc’s) trade policy, but by macroeconomic forces related to national savings and investment. Thus, attempting to alter the trade deficit through bilateral efforts without addressing the underlying macroeconomic issues is unlikely to lead to the desired outcome.

It is important to note here that there are valid concerns regarding Germany’s global trade surplus, which stood at 7.6 per cent of the country’s GDP in 2017.29 This issue has been raised for years by the IMF and many G20 countries, as well as within the EU itself. For instance, the chief economist at the IMF warned in August 2018 that Germany’s reluctance to reduce its structural trade surplus was contributing to trade tensions.30 In other words, despite many flaws – and lack of rhetorical nuance – in Trump’s trade logic, the administration is right to single out Germany for criticism. To alleviate global concerns, but also to support its own long-term outlook, Germany needs to further boost domestic demand and investment, for example by increasing spending on public infrastructure, education, and research and development. This would not only help to reduce global economic imbalances, but also boost the country’s economic growth and competitiveness in the long term.31

A related source of tension between the US and Germany is the Trump administration’s claim that Germany ‘exploit[s]’ a ‘grossly undervalued’ euro to gain an unfair trade advantage.32 Since 2016, the Department of the Treasury has included Germany on its Monitoring List of trading partners.33 The Trump administration recognizes that ‘Germany does not exercise its own monetary policy’,34 and that the independent European Central Bank (ECB) conducts monetary policy for the eurozone. The overall weakness in the euro vis-à-vis the dollar has in part been driven by the divergence between monetary policy in the US and that in the eurozone, with the US Federal Reserve raising interest rates gradually since 2015 while the ECB has kept rates low. It is right to state that German exporters have benefited from an undervalued euro in their country, which the IMF estimated in July 2018 to be 10–20 per cent weaker than it should be.35 However, this is not the result of a deliberate currency manipulation; rather, it is due to mechanisms such as tight controls on the labour market, which have prevented real wages from keeping pace with productivity, that amount to an internal devaluation and help Germany’s international competitiveness. Thus, the US – and others, including the IMF – are essentially correct when they argue that if Germany took steps to let wages move in line with improvements in productivity, and also increased its domestic demand, higher wages and prices would appreciate Germany’s real effective exchange rate.

The current US administration seems to be unwilling to acknowledge that EU automotive companies operate factories in the US – with Mercedes, BMW and Volkswagen together directly employing more than 20,000 US workers.

Trump has complained about German cars on the streets of New York City since the 1990s. He regards the transatlantic trade in automobiles and automotive parts as unbalanced. As president, he has repeatedly criticized disparate tariff levels: the EU imposes tariffs of 10 per cent on US- and other foreign-built cars, while the US levies a 2.5 per cent tariff on cars built in Europe. However, he ignores the fact that the US has higher trade barriers for trucks: the EU tariff is 22 per cent, as against the US tariff of 25 per cent.36

It is unclear what the Trump administration’s ultimate goal actually is when it comes to automotive tariffs. In August 2018 the president rebuffed an offer by the EU to eliminate tariffs on cars, deeming this ‘not good enough’, because European ‘consumer habits are to buy their cars, not to buy our cars’.37 Moreover, the current administration seems to be unwilling to acknowledge that EU automotive companies operate factories in the US – with Mercedes, BMW and Volkswagen together directly employing more than 20,000 US workers.38 If the Trump administration was to go ahead with additional tariffs on imported automobiles and automotive parts under Section 232 of the Trade Expansion Act of 1962, there is the risk that European companies might reduce investment and cut their workforce in the US.39 It remains to be seen what the Department of Commerce has found in its investigation, and what course of action it recommends. But most commentators – including leading Republicans in Congress, such as the recently retired chairman of the Senate Committee on Foreign Relations, Senator Bob Corker – do not regard the national security provisions as a valid justification for the introduction of automotive tariffs.40

The jury is still out on the question of whether the imposition and threat of tariffs is a means to an end or the end per se. Larry Kudlow – the current director of the National Economic Council and a former television host with critical views of tariffs generally – has argued that President Trump has a vision of ‘free and open trade’.41 Wilbur Ross, the Secretary of Commerce, has similarly made the case that the president’s objective is to ‘reduce tariffs, reduce trade barriers and make an open level playing field for U.S. companies all around the world’.42 Trump has, notably, credited the successful renegotiation of the North American Free Trade Agreement (NAFTA) to the US’s imposition of steel and aluminium tariffs, as well as to its threat of introducing automotive tariffs.43 This suggests that the Trump administration is using tariffs as a negotiating tactic to press other countries into making concessions. However, the Trump administration’s refusal to revoke the steel and aluminium tariffs on Mexico and Canada immediately after signing the new United States–Mexico–Canada Agreement (USMCA)44 in November 2018, as well as Trump’s self-designation as ‘Tariff Man’ in a tweet lauding the positive impact of tariff revenues for the US, shortly after reaching a 90-day tariff truce with China,45 suggests that the current US administration is prepared to impose and maintain tariffs for some time yet.

The Trump administration’s practice of going back and forth in its trade talks – asking the EU to eliminate its automotive tariffs and then snubbing its offer to do so, or officially putting new tariffs on hold but continuing to hint at their possible imposition, to some extent reflects the fact that President Trump likes to keep the opposition around the negotiating table ‘off balance’. But it also reflects the reality that there are various factions within the administration that have different views on trade.

There are broadly two camps within President Trump’s trade team. The first includes National Economic Council Director Larry Kudlow and Secretary of the Treasury Steven Mnuchin as the voices in the current administration that are, relatively speaking, the most in favour of free trade – although both have backtracked on their previous commitment to free trade and internationalist principles since joining Trump’s team. The other camp comprises President Trump’s trade adviser Peter Navarro and USTR Robert Lighthizer, whose stance on trade is more protectionist and hawkish. Navarro (who serves as the Assistant to the President and Director of the Office of Trade and Manufacturing Policy) is concerned with the US industrial base, and favours a decoupling of the US and Chinese economies. Lighthizer – a long-standing critic of China’s trade practices – might be prepared to strike a deal with Beijing if it addresses some of the issues at stake. Meanwhile, Commerce Secretary Wilbur Ross oscillates between these two camps, but often sides with the latter group. He is best described as a more old-fashioned protectionist, under whose leadership the Department of Commerce has made more aggressive use of traditional – but also rarely used – trade remedies (such as self-initiating the first anti-dumping and countervailing probes in decades, or initiating the Section 232 national security investigations).

Although leaders in other countries know that ultimately it is President Trump who calls the shots on trade, it is important for them to know who within the administration has the president’s ear. For the Europeans, the main interlocutor is USTR Lighthizer, who is the US lead on the US–EU Executive Working Group. Lighthizer’s primary target has been China’s practices regarding forced technology transfer, intellectual property theft, and perceived efforts to dominate future technology sectors. European officials thus believe that Lighthizer is more amenable to collaborating and forming a united US–EU front against China.46

Another major point of contact for European officials is Wilbur Ross. As Commerce Secretary, his primary goal is more narrowly focused on the US trade deficit and on trying to increase US exports to the EU. Because of the Department of Commerce’s determination that steel and aluminium tariffs are a threat to US national security – which ultimately led to the imposition of tariffs affecting the EU and other allies – the relationship between Ross and EU officials seems more fraught. This was evident in a tense meeting between Ross and European Commissioner for Trade Cecilia Malmström, in October 2018, during which Ross emphasized that President Trump’s ‘patience was not unlimited’ and his EU counterpart accused Washington of deliberately delaying the negotiation process.47

President Trump has repeatedly emphasized that he favours bilateral deals over mega-regional or multilateral agreements. Because the European Commission has exclusive competence over the EU’s trade policy, a deal between the US and the EU would technically fit with this preference. However, Peter Navarro has previously criticized TTIP as being a ‘multilateral deal in bilateral dress’.48 Since then, Trump has reportedly offered France a bilateral trade deal with better terms than those available to the EU as a whole – on condition that the country pulls out of the bloc.49 So far, the EU and its member states have been unanimous in emphasizing that any negotiations must take place at the EU level and not with individual countries.

The Trump administration has also adopted an approach that is much more transactional in nature than those of its predecessors. Notably, it has conflated trade and defence issues, linking concerns over the US’s trade deficit with the EU to frustration over some EU member states’ failure, thus far, to meet the NATO pledge (agreed at the alliance’s 2014 summit in Newport, Wales) of increasing defence spending to 2 per cent of GDP by 2024.50 While this approach has alienated the US’s allies, the EU has been able to react with remarkable unity.51

Given the US government’s concerns over both the country’s trade deficit with the EU and what it has framed as Germany’s manipulation of the euro to its own advantage, the EU and its member states are a primary target of the Trump administration’s trade rhetoric and actions. At the same time, the EU has since early 2018 been caught in the crossfire of the trade war between the US and China, and may suffer collateral damage.

Compared with the impact of the steel and aluminium tariffs on the European economy, new unilateral US tariffs on automobiles and automotive part imports from the EU would have much more severe economic effects. The US measures on steel and aluminium affect EU exports worth €6.4 billion, but the EU’s exports of cars and automotive parts to the US are worth more than €50 billion annually.52 Germany – given the importance of its car manufacturing sector and its exposure to the US market – would be especially badly hit by automotive tariffs. However, the complexity of supply chains means that the impact of US tariffs would be felt in Europe more broadly. A recent report by five renowned German economic institutes, commissioned by the German government, found that an escalation of the trade conflict would be likely to trigger a severe recession in Germany and more widely in Europe.53

Compared with the impact of the steel and aluminium tariffs on the European economy, new unilateral US tariffs on automobiles and automotive part imports from the EU would have much more severe economic effects.

Even if the transatlantic tariff dispute does not intensify, a further deepening of the US–China trade war would have adverse consequences for EU economies. The US currently imposes tariffs on imports of Chinese steel and aluminium in the name of national security. It has also imposed tariffs on $250 billion worth of Chinese products, based on Section 301 of the Trade Act of 1974.54 China has raised retaliatory tariffs on $110 billion worth of US products. Despite the 90-day ‘ceasefire’ agreed between President Trump and President Xi in early December 2018, and Trump’s subsequent decision, in late February 2019, to defer a tariff increase,55 a further escalation of the trade dispute cannot be ruled out, as both sides will find it difficult to address long-standing issues around China’s trade practices. Thus, the Trump administration may yet carry out its threat to impose tariffs on a further $267 billion worth of Chinese imports. The indirect effects of this tit-for-tat US–China trade war on the EU and its member states could be significant. It would disrupt global supply chains and, in all probability, would lead to a slowdown in global trade and economic growth.56

It should also be borne in mind that while the current US steel and aluminium tariffs are aimed at China, they miss the mark because they do little to address the real issue of China’s excess steel capacity. China is not among the leading 10 supplier countries for US imports of steel. Rather, US steel imports come primarily from Canada, Brazil and South Korea.57 However, these three countries received initial exemptions from the tariffs, with the latter two having secured a permanent exemption by agreeing to a quota.

On the matter of trade, the Trump administration sees the EU as both adversary and potential ally. The EU has become a primary target of US trade action, and is also vulnerable to collateral damage in the US’s trade war with China. At the same time, the US recognizes the EU as a potential partner against China’s trade practices, and in pressing for reform of the global trading system.

The US and the EU share concerns regarding China’s overcapacity in the steel sector, market-distorting subsidies to industry, the role of state-owned enterprises, policies on forced technology transfer and theft of intellectual property. While initially it seemed as though Trump’s trade wars, on multiple fronts, were pushing the EU and China closer together and strengthening their economic ties, more recently the US and the EU have signalled their intention ‘to join forces to protect American and European companies better from unfair global trade practices’.58

Moreover, the US and the EU, along with Japan, have intensified their discussions on tackling shared concerns about China’s trade practices, as well as on reforming the WTO, and have issued a number of joint statements since 2017.59 While neither the 2018 Trump–Juncker agreement nor the joint US–EU–Japan statements make direct reference to China, these efforts suggest that the US and the EU may be willing to overcome their trade dispute and work together to stand up to China’s trade practices.

To sum up, on the matter of trade, the Trump administration sees the EU as both adversary and potential ally. The EU has become a primary target of US trade action, and is also vulnerable to collateral damage in the US’s trade war with China. At the same time, the US recognizes the EU as a potential partner against China’s trade practices, and in pressing for reform of the global trading system.