This report examines the common economic factors that continue to drive conflict in Iraq, Libya, Syria and Yemen. It also makes specific recommendations to Western policymakers addressing these types of sub-economies in detail.

Chatham House report

Published 25 June 2019

Updated 18 October 2023

ISBN: 978 1 78413 332 0

This report examines the common economic factors that continue to drive conflict in Iraq, Libya, Syria and Yemen. It also makes specific recommendations to Western policymakers addressing these types of sub-economies in detail.

Analysis of conflict economies to date has mostly focused on state-level dynamics, while academic studies have also indicated that national conflict economies are inextricably linked to transnational or regional conflict economies.74 Less attention has been paid to the development of conflict economies at the subnational level. This chapter focuses on conflict sub-economies that are location-specific but similarly integrated into regional and transnational flows.

Comparative analysis of Iraq, Libya, Syria and Yemen reveals the existence of three distinctive types of conflict sub-economy: capital cities; transit areas and borderlands; and oil-rich areas. The value and types of rents extracted, and the types and intensity of violence associated with such rents, vary by sub-economy. In capital cities, rents are derived from controlling state institutions and treating the state as a resource – one that offers an assortment of assets, revenue streams and patronage postings. In transit areas and borderlands, rents centre around arbitrage opportunities and the taxation of goods and people. In oil-rich areas, rents are collected through oil sales (usually as taxes upon the sale of oil products, in the case of armed groups) and are contingent on physical control of the area (although the level of taxation achievable depends on the extent to which various actors control points along often-fragmented supply chains).

This chapter explores how the three types of conflict sub-economy condition local economic activity in different ways and determine whether violence is used. Through comparative analysis, we show that each type has a distinct set of characteristics and operating dynamics. Rather than conducting subnational comparisons of conflict economies within a single MENA country – as is common in both the scholarly and policy worlds – we argue that cross-national comparisons across sub-economy types are more likely to reveal generalizable patterns that can be applied to other MENA countries, and perhaps to other conflict-affected countries. For example, our analysis shows that the dynamics of Baghdad’s conflict sub-economy have more in common with that of Tripoli in Libya than with that of al-Qaim (a border town) in Iraq. The conflict sub-economy of al-Qaim, in turn, has more in common with al-Mahra in Yemen than al-Mahra does with the national capital, Sanaa.

Despite political, economic and social fragmentation in Iraq, Libya, Syria and Yemen, physical control of the capital city in each country remains the most prized asset. In Iraq and Libya, such control is equivalent to controlling the state, owing to the extent to which oil revenues run through Baghdad and Tripoli respectively. While Damascus and Sanaa do not provide the same opportunities for revenue capture, they are still the hubs of their respective conflict economies – with Damascus providing a means for the legal distribution of patronage, and both capitals enabling the capture of public and private institutions.

Capital cities have symbolic as well as practical significance.75 While the relative strength of the state, the degree of centralization and the history of state consolidation vary across the four capitals, what they clearly have in common is power. Baghdad, Tripoli, Damascus and Sanaa each sit at the centre of control over state institutions, assets and legislative power. They are also the financial sector’s primary interface with international markets. Where forces in control of capital cities have international recognition, their access to external markets is typically enhanced (as is their influence in multilateral organizations such as the UN). Where such recognition is denied, warring actors in control of capital cities have nonetheless found ways to circumvent the constraints placed on their commercial and financial activity.

The more the distribution of resources reflects both the power balance in the city itself and the broader national power balance, the more likely we are to see embedded rather than competitive violence. For example, Baghdad’s resources are divided among a limited elite, sustaining a system of embedded violence. While Tripoli, like Baghdad, is the principal access point for revenues generated from the state’s oil wealth, Libya’s rival forces have not agreed on how power should be divided. As a result, heavy competitive violence is currently under way in a bid for control over the city. Damascus and Sanaa do not have the same degree of largesse to distribute. Yet both the Syrian regime (which controls the government and formal powers of the state) and the Houthis (who have infiltrated Yemen’s state institutions) have used financial institutions and state resources to build their economic capacity in support of their war efforts. In both Damascus and Sanaa, the actions of the dominant forces are underwritten by coercion, sustaining embedded violence.

When a sitting government loses physical control over the capital, competitive violence will continue until a clear winner emerges, after which ‘violence rights’ will be awarded and embedded violence will become institutionalized

The ways in which control over capital cities has played out in these four countries suggest that when a sitting government loses physical control over the capital, competitive violence will continue until a clear winner emerges, after which ‘violence rights’ will be awarded and embedded violence will become institutionalized in the economic life of the city.

Seizing physical control of buildings and territory guarantees access to state budgets and assets in capital cities, enabling control of patronage and revenue distribution. Once physical control is established, ‘violence rights’ are then linked to control over budgets and assets, as well as to access to state benefits and patronage posts. The conflict economy dynamics of capital cities are not unique to the MENA region, but will find easy comparisons with other countries that are mired in war. Undoubtedly, capital cities are central nodes in all government patronage systems, but they play an extra important role in the MENA region because power is comparatively more centralized than in other developing countries. This is particularly the case in Iraq and Libya, where almost all distribution occurs from the political centre. Still, for armed groups in any country, being able to reward loyalists with a stable salary or a regular welfare supplement, or to punish enemies by stripping them of their posts, is a powerful tool.

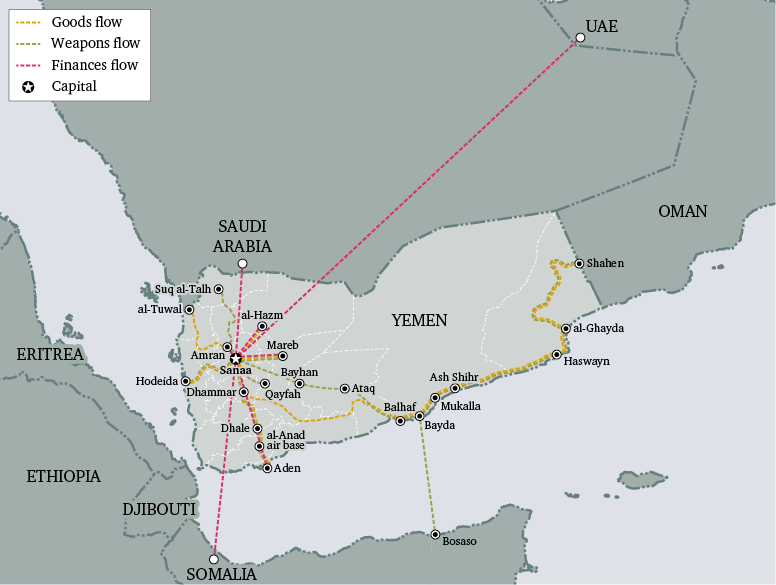

In Syria and Yemen, resources are more broadly distributed. Yet even in Syria, a major proportion of economic activity must pass through Damascus. The same applies to a more limited degree to Sanaa. The 2015 ouster of President Abd Rabbu Mansour Hadi’s internationally recognized government led him to announce that Aden would be the temporary capital of Yemen. Before the war, Sanaa functioned as a clearing house for revenues generated by oil and gas exports from Mareb, Shabwa and Hadramawt, for customs duties collected at ports like Aden and Hodeida, and for receipts from manufacturing in Taiz. The Houthi takeover of Sanaa precipitated a breakaway of these regions from the capital, and an accompanying loss of revenues. In other words, a degree of de facto decentralization occurred.

In Libya, the picture varies again: even though political forces in the east of the country have sought to establish rival state institutions to those in its west, oil revenues continue to be distributed solely from Tripoli. This has allowed Tripoli to retain its pre-eminence in the conflict economy (although at the time of writing the city was under threat from the LNA’s ongoing 2019 offensive, led by Field Marshal Haftar).

Control of Tripoli connotes dominance over the distribution of Libyan state revenues. The system of governance under Gaddafi was characterized by significant centralization: as a result, almost all key state institutions are found within 1 square kilometre in the capital.76 Since the overthrow of the Gaddafi regime, periods of calm have been short-lived.77 The GNA has survived only with the acquiescence of Tripolitanian militias, which coalesced from over 30 groups of varying military significance in 2012 to four dominant groups in 2016: the Tripoli Revolutionaries Brigade (TRB); the Nawasi Brigade; the Abu Slim Central Security Unit; and the Special Deterrence Forces.78

Following this consolidation of power in Tripoli, two of these groups – the TRB and the Nawasi Brigade, along with their networks – used their territorial control to infiltrate state institutions, reducing the need for overt coercive violence. Their presence on or near the premises of state institutions has enabled them to extract rents, control access to buildings, and intimidate staff and visitors. Prior to 2016, armed groups in the capital were able to obtain salaried positions and access to the budgets of state institutions in return for protection services.79 In other cases, armed groups and their networks used their positions and coercive power to sign major commercial contracts from state institutions.80 As this dynamic has evolved, armed groups and their networks have increasingly learned to fill senior positions in order to guarantee their influence. For example, in 2018 the Nawasi Brigade, which controls the headquarters of the Libyan Investment Authority (LIA), sought to violently force the LIA’s management to recruit and employ candidates from the armed group itself. The LIA’s management refused, and was forced to move out of Tripoli for several months. However, a plan to relocate the LIA’s headquarters was blocked by the Nawasi Brigade.81 The group also has influence within the Ministry of Finance. While armed groups’ infiltration of state institutions has reduced the need for overt violence, their influence continues to undermine the institutions themselves and has contributed to the normalization of embedded violence.82

Powerful interests from outside Tripoli have felt excluded from rent-seeking opportunities as Tripoli-based armed groups have consolidated their physical and institutional control. This consolidation of control has provoked further episodes of competitive violence. In August and September 2018, the Tarhuna-based 7th Brigade sought, with a number of allied groups, to displace Tripoli’s militias within the city. The 7th Brigade, also known as the Kani Brigade, sought to characterize the Tripolitanian armed groups as ‘the Daesh of the public finances’. This political line of attack was an effort to curry favour with the local population. It reflected the well-known predatory revenue-generation methods of the incumbent militias in Tripoli. Following the successful defence of their positions in Tripoli, the Tripolitanian armed groups made public shows of taking a less rapacious approach to rent-seeking, perhaps also reflecting their prioritization of institutional infiltration over direct violence. Overall, events in Tripoli demonstrate how volatile the situation is when a limited number of groups are trying to maximize access to rents, while other groups and communities are locked out of revenue-generation opportunities.

Events in Tripoli demonstrate how volatile the situation is when a limited number of groups are trying to maximize access to rents

In Yemen, Houthi-linked administrators and businessmen have adopted a similar strategy of institutional infiltration to dominate economic life in Sanaa through coercive means. Apart from a sudden outbreak of fighting in December 2017 – when the Houthis killed their erstwhile ally, former president Ali Abdullah Saleh, and consolidated their control over the capital – Sanaa has not witnessed significant levels of competitive violence. Yet the Houthis and their affiliates have continued to wage a campaign of institutional capture, underwritten by ‘violence rights’ and an implicit threat of force. Either directly or through their role as a so-called mushrif (supervisor), Houthi affiliates control the CBY, the Ministry of Finance, the Ministry of Oil and Minerals, Yemen Petroleum Corporation (YPC – the state fuel distributor), and tax and customs authorities. While customs revenues are largely collected from customs points at Hodeida, Dhamar and latterly in Amran governorate, the funds are routed to Sanaa for redistribution. Yemen’s main telecommunications firms are all headquartered in Sanaa and mostly controlled by the Houthis. Such a consolidation of power in the capital has enabled the Houthis to integrate the state, the formal economy and the informal economy into a powerful military machine. These tactics have consequently allowed the Houthis and their associates to form a sustainable resource base to fund their military agenda, despite significant international opposition, although the Hadi government has since 2016 attempted to wrest control of the levers of the economy away from Sanaa.

In Iraq, political actors allocate government appointments and exercise control over ministries in order to gain access to state revenues and budgets, representing the prevailing power balance across ethno-sectarian lines. This is one reason why we see less competitive violence in Baghdad. As in Libya, Iraq’s reliance on oil revenue reinforces the significance of the centralization of power in the capital. This process, in turn, makes the centre attractive to all armed groups operating throughout the country. The presence of oil serves as a centralizing force in Iraq’s rentier economy. As a PMU commander told one of this report’s authors, ‘the money we make from checkpoints is minimal compared to money from Baghdad’.83 Yet the connections between elites, political parties and their armed wings are much clearer in Baghdad than in Tripoli. These actors have divided the wealth among themselves. After 2003, Shia, Kurdish, Sunni and other elites all came together to ‘split the national pie’ under the so-called muhassasa (quota) system.84 Every subsequent government formation process in Iraq has involved a negotiation between these groups over government appointments and access to ministries. Ministers have reported to Chatham House that contracts and payment orders are processed by representatives of political blocs connected to political and armed factions, often without the ministers’ consent or knowledge.85

Iraqi ministers have reported that contracts and payment orders are processed by representatives of political blocs, often without the ministers’ consent or knowledge

The balance of power in Baghdad differs from that in Tripoli or Sanaa, as the muhassasa system means that the proceeds from the city’s conflict sub-economy are distributed among an array of actors (from different communities) across the country. Rent-seeking opportunities are more horizontally inclusive. Since 2003, Shia, Sunni, Kurd and minority leaders have become enriched, while their citizens remain poor. Less competitive violence is on display in Baghdad, yet this does not mean that violence is absent. In fact, to hold significant power in the capital, each network must have the capacity to employ coercive force. For example, armed groups control different areas in Baghdad, each exerting influence over the property and businesses in their area. Businesspeople are unable to work in the city without organized backing or protection.86 Armed factions use their presence in the city to control access to the state’s institutions and assets. As the rise of the country’s protest movement has indicated, privileged access to state resources is a driver of embedded violence. In turn, the failure to tackle this problem makes outbreaks of competitive violence more likely.

Control over government ministries also confers the right to assign public procurement contracts. This is one of the most lucrative ways of rewarding loyalists and maintaining coalitions of armed groups. In Syria, the Assad regime operates a highly centralized system of governance through the capital, Damascus. This system is based on a combination of coercion and embedded violence, exercised through core institutions in the security and military services.87 Central Damascus has remained firmly in the grip of the regime. Since the outbreak of the conflict, the government has prioritized control of the capital and other major urban centres, while being more willing to cede other areas. As Syria lacks the scale of oil resources of Libya or Iraq, we also see differences in the dynamics of coercion and patronage. Without being able to rely on the revenues of the oil and gas sector, the regime has instead sought extensive foreign support (military support from Russia, and financial and military support from Iran), and cultivated loyalist elites to maintain its war effort, particularly during periods when vast areas of the country have come under the control of rebel forces.

Lacking the revenues required to keep fighting, the Syrian regime has at times subcontracted parts of its war effort to domestic and international allies.88 This quid pro quo has involved the exchange of privileged access to economic opportunity in return for financial and material support. Contracts and commercial licences have been granted to regime-affiliated figures and businessmen, some of whom fund militias that fight in support of the government. For example, oil supply deals, including import contracts, have been awarded to middlemen such as Baraa Qaterji and Hussam Qaterji, brothers who run a militia in Aleppo.89 Other examples include the extraction of steel and rubble from destroyed towns and cities. Mohammad Hamsho, a magnate who reportedly received the exclusive right to purchase scrap metal collected from destroyed neighbourhoods,90 was also blacklisted by the EU for his funding of regime militias. He is believed by many to serve as a proxy for Maher al-Assad, the president’s brother and commander of the Fourth Division of the Syrian Arab Army.

The regime has used similar tactics to requisition land. Perhaps the most emblematic development is the Marota City project, which is being built on land that once consisted of informal housing settlements but has been forcibly expropriated for development. The area had been a hub for the opposition in the early stages of the conflict. The scheme has attracted half a dozen businessmen as investors, each of whom has clear ties to the Assad regime and has contributed resources to its war effort.91

In a variety of quid pro quo deals, natural resource contracts have been awarded to firms of foreign allies. Licences to extract minerals, including phosphate and salt, have been granted to Russian companies. In a move that perfectly encapsulates the dynamics of the Syrian conflict economy, the government has further committed to devolving control and management of certain oil and gas fields to Russian entities. Yevgeny Prigozhin, a prominent Russian oligarch with close ties to President Vladimir Putin, has reportedly been granted the right to collect 25 per cent of revenues from any oil and gas fields ‘liberated’ by his mercenaries.92 That said, none or very few fields have so far been appropriated in this way.93 In April 2019, the port of Tartous was leased for 49 years to a Russian company.94

Control of the capital city also comes with the ability to make laws and use the legal authorities of the state to legitimize, undermine, fast-track or block particular practices or behaviours. Particularly in Syria and Iraq, armed actors who control the capital can use the legislature to legitimize their actions and patronage decisions through the law. In contrast, in Libya and Yemen – where governance remains split – legal powers are contested.

In Syria, the regime has made full use of its legal authorities to create private militias to support the Syrian Arab Army. From the writing of a new constitution in 2012 to the enactment of laws on real estate and local administration, control of the state bureaucracy via Damascus has enabled the regime to continue to set the rules of the game. In addition to providing privileged access to state assets, legal powers have been used by the state in effect to ‘subcontract’ its war effort in official form. A 2013 law establishing the right of private enterprises to form their own security forces has allowed pro-regime business figures to fund loyalist militias, thus bolstering the forces of the Syrian Arab Army. Prominent examples of the militias formed include the National Defence Forces, supported by the Al-Bustan Charity that was founded by Rami Makhlouf, a cousin of Bashar al-Assad and the owner of a vast businesses empire.

In Iraq, the PMU’s armed groups leveraged their growing military capacity, public profile and political leverage in Baghdad to pressure the Haider al-Abadi government and Iraqi parliament into giving them legal recognition in 2016. This was achieved through allies in parliament. This recognition, in turn, has translated into direct payments to the PMU from the Iraqi state. The PMU emerged in 2014 as an umbrella organization of some 50 paramilitary groups across the country, in response to the rise of ISIS. A key priority for the group was to become financially self-sustaining; as such, its leaders sought to tap into the state’s resources. In October 2016, the Iraqi parliament passed Law Number 40 (2016), which legally recognized the Commission of the PMU. Funding for the PMU was consequently incorporated into the Iraqi state budget, and by the 2019 budget year the group was receiving an equal share of salaries per soldier to that allocated to the Iraqi Ministry of Defence. Despite its official recognition, the PMU remains something of a parallel structure, not fully under the command and control of the state. Like other armed groups and political parties in Iraq, it has access to other forms of revenue outside formal legal parameters, including informal taxation at checkpoints outside the capital. This is illustrative of the multi-pronged approach, discussed later in this report, of combining formal revenue streams from the state (via the capital) with informal revenue streams (via transit areas and borderlands). PMU forces are unlikely to cede their gains to the state despite the military defeat of ISIS. In this sense, PMU groups are both part of the state and in competition with it, perpetuating the presence of extra-state structures.

In Libya and Yemen, the disputed status of the authorities dilutes the potency of legal tools for managing conflict sub-economy dynamics. The governance split between the Tripoli-based Government of National Accord (GNA), headed by the Presidency Council, and the eastern-based House of Representatives (the internationally recognized parliament) means that the route for new legislation, and therefore control over state authorities, is blocked. Legal battles over who has the authority to appoint the leadership of Libya’s institutions, and thus who has the right to control their assets, are ongoing. Particularly notable is the struggle through the international courts for control of the Libyan Investment Authority (LIA), which has assets worth an estimated $67 billion.95 Legal battles for control of assets have become a major feature of Libya’s conflict economy, dovetailing with the trend of institutional capture and infiltration by armed groups. That said, negotiating an accord with whichever armed group physically controls the premises of a given institution can be more important than any legal ruling. During the 2016 legal battle between rival leaderships of the LIA, for example, it was the Nawasi Brigade, rather than the courts, that determined who had access to the building.96

Despite war, and despite efforts to capture, control and destroy the states around them, financial hubs have been resilient, even where political actors have sought to relocate financial institutions. In each of the case studies, the capital city is the predominant node for monetary and financial policy, for transactions involving the private banking sector, and for interactions with the international financial system.

Financial sanctions and a lack of international recognition can significantly impede access to global markets, but even where this has been the case, the four capital cities have retained their financial authority. Centres of financial authority have been remarkably ‘sticky’. This is to say that it is difficult to dismantle or replicate the technical capacity, infrastructure, commercial support systems and human resource networks that are required to sustain a financial centre. It is also a sector that has historically been, by necessity, more rules-based and technocratic. These features have given the state’s financial institutions, and their supporting networks, more room to adapt to the conflict economy.

Iraq’s financial and economic institutions, headquartered in Baghdad, have served as financial conduits for armed actors who are not accountable to the state. For example, armed groups linked to various political elites rely on the state retail bank Rafidain and the Trade Bank of Iraq (TBI) to transfer money around the country and abroad.97 Foreign states have also used these same vehicles to fund armed groups working against the interests of the state. Such arrangements incentivize armed actors to establish their own independent channels to receive money directly from external actors, which creates an accountability relationship between an armed group and a foreign power. From the funding of Sunni awakening (sahwat) groups by Turkey, the US and the Gulf states in 2008–10 to Iran’s financial sponsorship of PMU groups, the transactions underwriting the operations of many of Iraq’s key non-state armed actors have been conducted through Baghdad-based financial institutions.

At the same time, ‘leaks’ in the financial and monetary systems have provided opportunities for other armed actors competing with the state. Between 2014 and 2015, for example, ISIS infiltrated the central bank’s currency auctions in order to launder money, relying on middlemen who worked inside the bank. According to an Iraqi banking source, in 2015 ISIS was earning a minimum of $25 million per month in these auctions.98

Control over a central bank is a powerful lever in any economy. But it is especially powerful in a conflict economy, where access even to sprinklings of financial or monetary information can be monetized without many of the normal restrictions that would be in place during peacetime. In Syria, the regime’s control over the Central Bank of Syria (CBS) is a powerful asset in the conflict economy. Many of the central bank’s operations generate significant profits for well-connected speculators, particularly in the foreign exchange market. A system of multiple exchange rates, including various official rates, enables individuals close to CBS or other regime officials to speculate, buying US dollars at the discounted official rate to resell them in the black market. Another tool of influence is the provision of asymmetric information to financial traders. One example was an unofficial CBS decision at the end of May 2016 to reduce the supply of Syrian pound liquidity in the market. This sudden decision led to a shortage of cash in the market and a temporary jump in the value of the pound.99 Days later, the CBS resumed cash supplies and the pound depreciated again. Between the end of April and the end of May, the black-market value of the US dollar fell by 25 per cent, before rising 20 per cent again in June.100 Analysts in Damascus believe the decision of the CBS was coordinated with several regime insiders, business partners and corrupt actors, helping these parties reap significant benefits.101

In Syria, the regime’s control over the Central Bank of Syria is a powerful asset in the conflict economy

Economic sanctions have not decisively affected Damascus’s role as the hub for money transactions within the country and with the outside world. While Western sanctions do not formally ban financial transactions with all Syrian entities, in practice the country’s banking sector has become largely isolated from international markets as a result of sanctions. Sanctions have increased the cost of financial transactions and have made the processes involved more cumbersome. Even transactions with allies such as Russia and Iran have become more difficult. In early 2019, both countries were still struggling to get around the constraints102 on their financial transactions with Syria. Yet rules and regulations are still issued by the CBS, and the reduced flow of international bank transactions still needs to go through the Syrian capital. That said, Damascus has lost a substantial part of its financial role to Beirut,103 which a large number of traders now use to process payments via third parties.

In Libya and Yemen, rival actors have sought to relocate the state’s resources to temporary capitals as a result of conflict. In Libya, this move has been opposed by the international community. As a result, the Central Bank of Libya (CBL), based in Tripoli, has largely retained its autonomy. International support for the CBL as an entity has, broadly speaking, prevented a rival leadership in the east from engaging with the international financial system, and has kept the east largely dependent on the redistribution of state revenues from the CBL. Eastern-based authorities have succeeded in purchasing banknotes and coinage from Russia to address liquidity issues, but they are unable to access SWIFT codes required to conduct international financial transfers. Their rivals in Tripoli have largely consolidated control over the assets of state institutions.

In Yemen, the Saudi-led coalition supported the Hadi government’s relocation of the headquarters of the Central Bank of Yemen (CBY) from Sanaa to Aden while Western partners such as the US and UK opposed it. The move went ahead, resulting in the loss of SWIFT authorization for international financial transfers until early 2018. The Hadi government has since attempted to incentivize and pressure merchants and banks into working with the CBY branch in Aden, and has been bolstered in these attempts by the provision of a Saudi credit facility of $2 billion. In September 2018, the Hadi government introduced a new decree aimed at forcing importers to work with CBY Aden, while excluding Houthi-affiliated merchants who have emerged since the start of the war. While the Hadi government has achieved a degree of success in taking control of the economy, Sanaa has remained the de facto administrative, financial and commercial centre of gravity in the economy throughout the conflict. Most of Yemen’s most important formal, semi-formal and informal financial institutions, fuel importers, food importers and revenue-gathering state institutions continue to be based in the city, although this could change.

Houthi networks in northern Yemen use a combination of formal banking channels and the hawala system to facilitate the continuation of financial and trade flows. Unlike in Syria, where the regime is able to circumvent international sanctions by operating via brokers who have not been subject to sanctions, the Houthis’ system is centred around a state-run commercial bank (which has become popularly known as the ‘Houthi central bank’) and the hawala money exchange system, which critically does not require any actual transfer of funds (not even electronically). The Hadi government has attempted to revoke the bank’s SWIFT access, but reportedly worked out a deal with the bank’s management not to cut it off entirely. While international recognition and access to multilateral organizations remain important, the Houthis have also illustrated that control of the capital city in a conflict economy can offset the constraints in place.

The Libyan dinar and the Yemeni riyal cannot be traded outside their respective countries. Access to foreign currency therefore requires direct access to foreign markets. Where such access is limited, this creates opportunities for arbitrage reflecting differences between the formal price of foreign currency in local-currency terms and its value on the black market.

At the beginning of 2014, the black-market dinar/US dollar exchange rate in Libya was nearly equivalent to the official exchange rate. Yet a confluence of factors – including the impact of a major oil blockade in the east, a governance split between the east and west of the country, and a lull in global oil price movements – prompted the Central Bank of Libya (CBL) to implement a series of austerity measures. Policies to reduce corruption were also introduced.

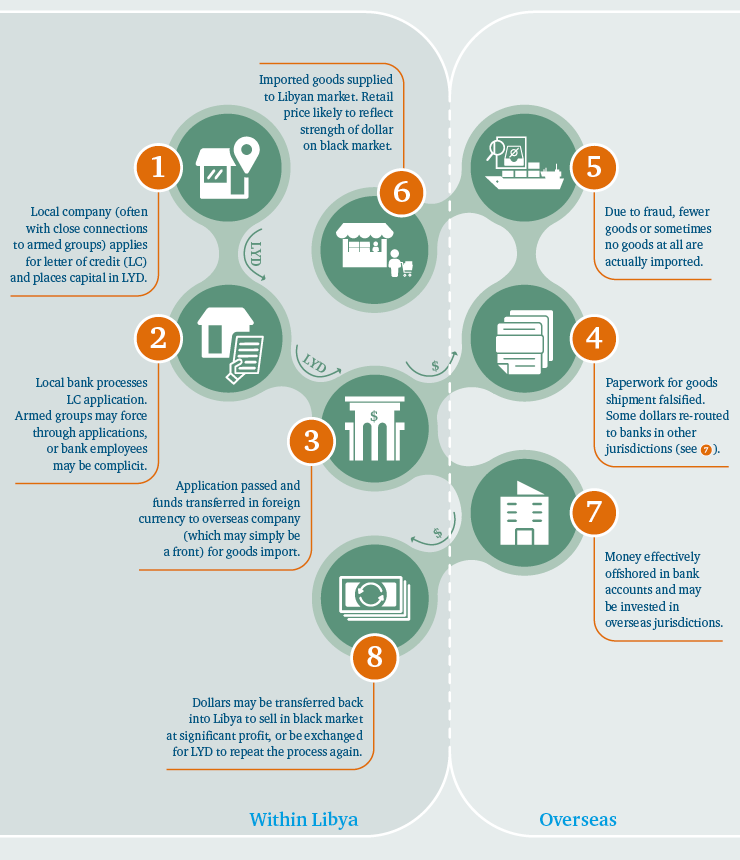

Put together, these measures had the effect of limiting access to foreign exchange, thereby creating a significant spread between the official and unofficial exchange rates. While the official rate held steady at around LYD1.4:US$1, at times the unofficial rate reached LYD10:US$1. This difference in exchange rates created a significant opportunity for anyone able to access foreign currency at the official rate and sell at the black-market rate. Given that Libya is heavily import-dependent, documentary letters of credit supplied for the import of goods became a major source of profit for actors ranging from businessmen to armed groups. The introduction of a fee upon access to foreign exchange in September 2018 has, however, lessened the arbitrage opportunity as the black-market rate for the dinar has fallen. Tripoli’s armed groups have developed significant business interests, setting up companies specifically to obtain letters of credit and divert the money from them. A number of armed groups also offer facilitation services: effectively a tax upon business in return for a guarantee that the letter of credit sought will be obtained.

Import fraud increased after 2013, in particular, when armed groups found it harder to access funding from the ministries of interior and defence. As of end-2016, militias from the Tripoli district of Tajoura were reported to have accessed $1 billion in misused letters of credit via 10 front companies.104 Haithem al-Tajouri, commander of the Presidency Council-affiliated First Central Security Division, has come under particular scrutiny over the affair. His division is in charge of providing security for diplomatic representations established in or visiting Tripoli. Tajouri also heads the Tripoli Revolutionaries Brigade (TRB), a non-state armed group formed during the civil war. After being cited by the UN Panel of Experts for allegedly extorting more than $20 million in letters of credit from CBL employees in 2015, Tajouri appeared to have refined his methods by using front companies. The UN Panel of Experts later reported that two banks had issued dozens of letters of credit to companies owned by an individual thought to have developed business links with Tajouri.105

Tajouri’s control of security at the port of Tripoli provides a means of securing imports and navigating official customs checks.106 The scale of the profits from such activities has raised tensions not only with other armed groups that lack similar access to finance, but also with a local population that feels the effects of the inflation and goods shortages associated with this diversion of resources.

Houthi merchants have been able to create a fuel oligopoly by coordinating with the de facto authorities to restrict rivals’ access to supplies of foreign currency required to import fuel. The income generated from these activities helps, at least in part, to fund the Houthi war effort. With access to much-needed foreign currency closely controlled by a Houthi-led council based in Sanaa, and merchants in the north actively discouraged from using credit facilities in Aden, some businesses have struggled to access foreign exchange. A number of merchants who have crossed the increasingly powerful Houthi traders have found their vessels held at the Hodeida port for days or even weeks, incurring costly fees. They have also had their cargoes inspected more rigorously and overtaxed, and have struggled to convert Yemeni riyals into US dollars – with funds often frozen for weeks or months before being released or converted. This has caused significant financial losses as a result of periods of (at times) rapid currency depreciation.

The concentration of state and financial institutions in capital cities provides unrivalled access to the international financial system, as well as to aid received via multilateral organizations such as the UN. Closely linked to this is the fact that international recognition shapes the conflict economy of capital cities by determining different actors’ access to external forums. In particular, the ability to negotiate the conditions upon which multilateral organizations can and cannot access Syria has provided the regime significant control over aid distribution since 2014. In Yemen, control over the financial sector and local security has enabled Houthi networks to influence aid distribution.

In Syria, the conundrum for donors is that aid capture is instrumentalized by the Assad regime as a means of countering its economic failure, while for the local population it is an important contributor to the coping economy. This allows the government to subcontract some elements of public spending. Despite international opprobrium, the regime’s control of Damascus still provides it with de jure international recognition and a seat in global institutions, including most importantly at the UN. As a consequence, all UN agencies and many international NGOs are based in Damascus, and operate under the rules set by the central government. While cross-border aid provided to northern Syria continues to bypass Damascus, an increasing amount is distributed via the capital as government forces recover more territory. Funds routed through Damascus are likely to amount to more than $1 billion per annum, which is roughly equivalent to around 20 per cent of actual government expenditure.107 This makes foreign aid an important contributor to the Syrian economy.

The de jure status of the Syrian government in Damascus enables the Assad regime to determine which groups and communities receive aid. This allows the government to selectively reward loyalist networks and communities. To receive funds, aid recipients must be registered with the government. Registration is used as an instrument of patronage, and also as a means of generating funds for groups aligned with the regime. These groups, as well as various regime-aligned figures, often use NGOs registered in the names of relatives to win contracts. In other cases, the parties involved benefit indirectly from financial inflows by operating as subcontractors on aid-funded projects. Income from such projects will then partly be used to pay salaries to subordinates and/or affiliates, or to finance other expenses, including in support of the war effort.108

These practices place the UN and international donors in a difficult position. Funds earmarked for aid are clearly buttressing the positions of prominent government-allied actors in the conflict economy. Yet bypassing the government to distribute aid is extremely difficult, if not impossible. Thus far in Syria, international donors have not succeeded in applying conditionality to humanitarian aid to prevent the regime from using it as an income stream.

In Yemen, the use of formal financial networks for aid operations will benefit entrenched elites. The use of informal networks will benefit shadow elites. To pay local staff and procure goods in northern Yemen – where the headquarters of most humanitarian organizations in the country are located – Western donors must either use informal financial systems closely connected to Houthi networks, or go through formal financial systems which are vulnerable to Houthi extortion. As donors cannot access Yemeni riyals outside the country, they are forced to do business with local financial operators. When informal transfers are required, donors must go through banks or money exchange businesses that are largely based in Sanaa and have purportedly strong Houthi links. Further, these businesses are overseen by several different economic councils controlled by the Houthis. It is likely that some of the proceeds from such informal transfers bleed into payment of Houthi fighters.

In Yemen, the use of formal financial networks for aid operations will benefit entrenched elites. The use of informal networks will benefit shadow elites

When using the banking system, aid agencies must work with banks that have branches or correspondent accounts outside the country. These banks have been able to command preferential exchange rates from international organizations, and charge sizeable fees. The Sanaa Center for Strategic Studies, a policy research institute, estimates that in 2017 this system netted a single bank $80 million in profit in an eight-month period.109 Such profits have made the banks a target for extortion by the Houthis, who have forced them to provide international financial services and cheap hard currency. In both Syria and Yemen, the developments outlined above illustrate that funds allocated – typically via capitals – for support to the coping economy cannot be protected entirely from entering the conflict economy.

In all four countries, to differing extents, internal territorial divisions caused by conflict have given rise to market distortions and the emergence of distinct economic units (sub-economies). Transit areas110 sit on the fault lines of these divisions, and have become significant sources of both taxation (i.e. on the movement of goods) and arbitrage (i.e. where actors profit from differences in the prices and availability of goods). As a result, transit areas111 along key trade routes have become prized assets for armed groups and other conflict economy participants.

In most cases, economic activity within transit areas falls outside the control of the state. In some cases, state actors cooperate with armed groups in return for a cut of the profits from transit points, rather than reporting such activities up through their command structure. Similar arbitrage and taxation opportunities are perceptible in ‘borderlands’ – defined here as areas situated on international borders – with the principal difference being that the state actors and economic systems engaged are on the other side of that international border. The relative absence of the state in borderlands lowers the barriers to entry for armed actors.

In the four countries, transit areas and borderlands are major sites of competitive violence. Although these conflicts are at times interpreted as ethno-sectarian or tribal in nature, at their core they represent actors competing for rents. This can create undesirable incentives for the perpetuation of territorial divisions, with a detrimental impact both on local populations and on state-building more broadly.

‘Taxation’ – in a broad sense of the term, often implying unofficial or illegal levies – is a major source of income for armed groups in the conflict sub-economies of Iraq, Libya, Syria and Yemen. It is particularly important for those groups with limited access to funding from the state and/or external patrons. Many of these transit areas are situated along historical trading routes that have always been sources of wealth, and are thus focal points for competition and violence. For national actors, subcontracting the control of transit areas and borderlands to local groups can be a useful strategy. It reduces labour costs, and gives local political or military partners a self-sustaining means of generating revenue. Competition for control of key transit areas, and the taxation opportunities associated with them, is a notable aspect of each of the conflict economies studied here. In addition, armed groups have established checkpoints within their own areas of control to further increase revenues.

One consequence of this pattern of activity is that acquisition of territory has assumed particular economic importance. Insurgent or underground groups, for instance, cannot reap the benefits available to groups that can expand their territorial reach into transit areas. Armed groups are thus incentivized to move away from the ‘underground’ model of resistance and to focus on territorial gains. Sometimes groups will justify income from transit areas as charges for the provision of security, or as a means of addressing funding shortfalls. In Iraq, for example, PMU armed groups have taken over or set up checkpoints in the north of the country ostensibly to raise funds and outsource labour costs (as fighters directly receive money at these checkpoints), despite the fact that PMU forces also receive salaries from the Iraqi state; this further builds PMU patronage networks.

Transit areas have been sites of significant armed clashes – not only because they determine the front lines of territorial control for each side, but also because they are major sites of taxation. In Syria, owing to the emergence of hard territorial divisions, taxation at transit areas has been a dominant form of revenue generation. The key transit areas are borders between territory under the control of the Assad regime and that controlled by rebel factions. Morek, a town northwest of Hama and south of Idlib, is illustrative of such dynamics. It lies on the Aleppo–Damascus motorway and serves as a crossing between regime-held areas and the rebel-held Idlib area. As a result of Morek’s strategic importance, armed groups controlling the town and the roads leading to it are able to generate substantial revenues, which in turn encourages regular competitive violence.112 For example, the expansion of the armed group Hayat Tahrir al-Sham (HTS) in the Idlib area in early 2019, while mainly motivated by a desire to pre-empt Turkish intervention, also had an economic imperative – one dimension of which was to secure control of the main road axis and intersections between rebel-held and regime-held checkpoints. Checkpoint fees are among the main sources of revenues for HTS. Open-source data indicate that HTS levied between $400 and $1,500 per truck transporting Turkish goods into regime-held areas, with the group’s revenues from taxation at the Morek crossing estimated by some at up to $1.5 million per month.113 On the regime side of the transit area, various security agencies, local militias and units of the Syrian army levy transport fees at checkpoints on the route from Hama to Morek. One such fee is called tarfiq, Arabic for ‘accompanying’, because regime militias are supposed to accompany trucks and provide protection until the next checkpoint is reached. The tarfiq, like other fees levied by militias, increases the cost of transport and the end price of the products sold.

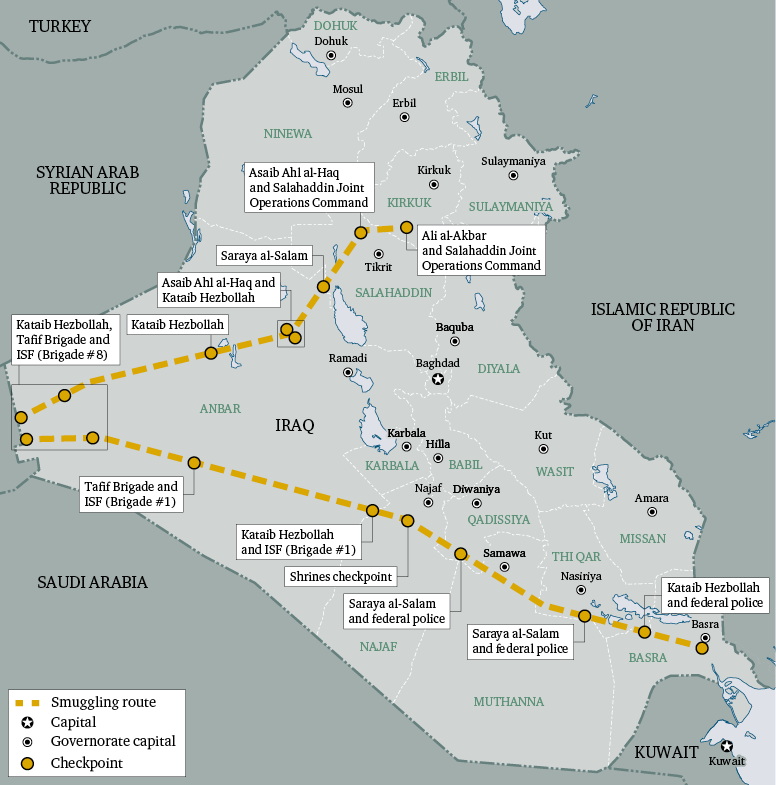

In Iraq, despite the absence of formal conflict, the battle among armed factions for control of informal taxation continues. The Iraqi town of Tuz Khurmatu has suffered major violence in recent years.114 Often, this conflict has been described in ethno-sectarian terms – Shia fighting against Sunnis and Kurds.115 However, the strategic location of the town at the intersection of trading routes to Iran, Syria and Turkey, and its position as a waypoint for oil and gas flows from nearby Kirkuk, reveals an alternative explanation.116 When PMU groups,117 Peshmerga and Shia Turkmen affiliates captured the area from ISIS in 2017, they focused on implementing a checkpoint regime along the main highway from Tuz Khurmatu to Baghdad. The revenues from these checkpoints are critical for armed groups – from the PMU to the Peshmerga – that cannot always afford to pay their fighters but still want to maintain a base and legitimacy in the area. Forces linked directly to the federal government, including local and federal police (the 7th Emergency Force) and the army (the Tigris Operations Command), are either absent from the area or unable to mitigate the competitive violence between armed groups.

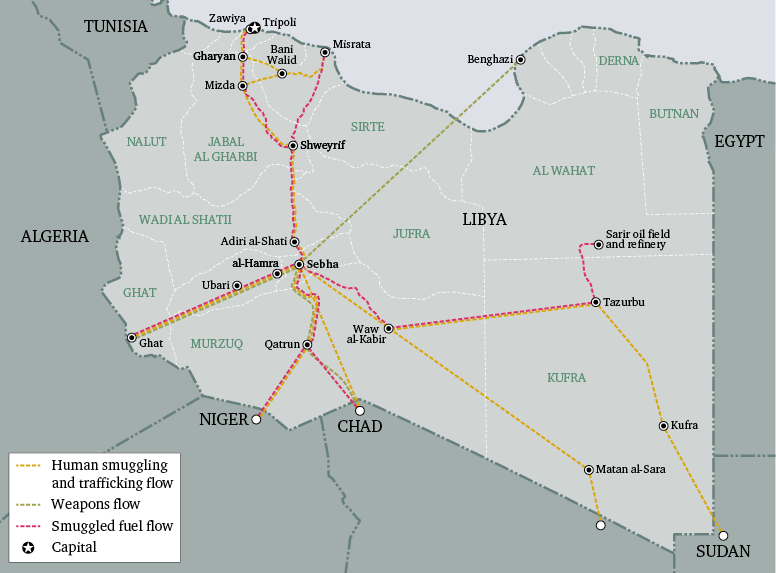

In Libya’s southern region of Fezzan, a lack of access to state resources has meant that informal taxes levied at roadside checkpoints – along with protection fees – constitute the principal source of income for armed groups.118 Competitive violence is ongoing for control of trading routes and taxation opportunities. Under Gaddafi, certain groups were preferred over others as part of a system of divide and rule. The subsequent collapse of the regime’s monopoly on force resulted in the eruption of armed competition in the south of the country. In part, at least, this violence reflected local actors’ efforts to seek control of smuggling routes. The collapse of state services in the south has only reinforced the importance of the informal economy. The problem has been compounded by the fact that many ethnic and tribal groups have limited access to state resources, and in particular to state salaries.119

The road from Sebha, the capital of Fezzan, to the northern coastal cities is the most critical transit area in the region. The road is controlled by a wide range of armed groups connected to local communities. Interviews conducted by Chatham House in November 2018 noted a visible increase in the number of checkpoints between Sebha and Mizda in late 2018. Travellers noted that the journey time from Sebha to Tripoli was now over 14 hours, compared to seven or eight previously. The high tolls that can be levied on smuggled fuel have motivated the establishment of yet more checkpoints, according to one interviewee from the Tebu community who concluded that these revenue-generating activities were aggravating tensions. The informal taxation practiced by groups in the Fezzan region appears to have increased the prices and reduced the availability of goods in the local market, damaging the coping ability of vulnerable local populations – despite the fact that the armed groups hail from, and seek to represent, these communities. This status quo appears set to continue: local forces will continue to find means of funding themselves to protect their interests and generate income.

The informal taxation practiced by groups in the Fezzan region appears to have increased the prices and reduced the availability of goods in the local market

Armed groups have monetized their control of transit areas in Yemen by taxing trade. This trade takes place even where goods that pass through an area controlled by a particular armed group may strengthen the position of its enemies. Merchants who depend on smuggling have ensured that transit routes remain open despite changes in military control of these areas. A clear example is the town of Bayhan in northwestern Shabwa governorate. Nominally controlled by military units loyal to the Hadi government, it sits at the intersection of territories respectively held by Islah-affiliated militias and military units, UAE-backed security forces and the Houthis. Despite Bayhan’s apparent insignificance as an urban centre, the area is known as a transit point for arms and other smuggled goods entering the country from the southern coast and elsewhere. Chatham House interviews indicate that the Shabwa smuggling networks play a crucial role in the continued flow of arms, people, drugs and fuel into the north. This is borne out by repeated attempts by the Yemeni government and UAE-backed forces to close down smuggling networks in Shabwa.120 By maintaining a presence in Bayhan, the erstwhile Houthi–Saleh alliance sustained access to the kondo mountain roads and southern coast. In 2017, the Hadi government initiated attempts to assert its authority in the governorate, including by sending forces from Mareb to Bayhan to fight the Houthis.

The 26 September Brigade, which controls Bayhan, is nominally aligned with the Hadi government. It has allegedly prioritized generating rents over curtailing a key Houthi trading route. The Houthis lost most of their territory in the Bayhan district following Saleh’s death in 2017. Logically, this should have impaired their trading links to Sanaa (which would have been a major setback). Yet within months of the 26 September Brigade’s capture of the territory, supply routes to the north appeared to have reopened. Indeed, the local arms market in Bayhan is now thriving. It is so well supplied that prices are lower there than in other areas of the country, according to two local sources. Thus Bayhan continues to operate as a transit area on a key Houthi trading route, despite the 26 September Brigade’s ostensible support of the government. Moreover, smugglers in southern Shabwa and along the mountain routes were well known to the de facto commander of Yemeni armed forces in Mareb, Ali Mohsen al-Ahmar, as well as to others, even before the change of control in Bayhan. They were thus well positioned to cut deals with all parties early on.121 In short, although the collectors of tax may change, it is likely that trade will continue regardless of who controls Bayhan.

The flow of goods through borderlands depends on the nature of each border and its infrastructure: it is more difficult to enforce border regimes on porous borders – and therefore collect taxes – than on non-porous ones. Borderlands are distinct from transit areas in that they involve direct interaction with the forces of external states. At tightly controlled crossings, this makes the barriers to entry much higher for armed actors in terms of controlling and taxing the movement of goods; the opportunities at more porous border crossings, which are difficult to police, are more readily exploited.

In Iraq, Libya, Syria and Yemen, the weakening of the central state has enabled local forces to control the flow of goods across international borders. For example, the Amazigh city of Zuwara, situated close to Libya’s western border with Tunisia, was long marginalized by the Gaddafi regime. Yet in recent years the city’s forces have developed a high degree of control over the flow of goods through the principal formal border crossing at Ras Jdir. While state customs officials are present at this border post, interviews with smugglers have indicated that the forces of Zuwara have the real leverage to determine what does and does not cross the border.122 In northern Syria, meanwhile, control of border crossings with Turkey has become a significant source of revenue for armed groups (see Box 3).

The extent of the interaction between the occupants of borderlands and external state actors depends on the nature of the area. Some borders – as in western Iraq, Libya, eastern Syria and Yemen – are relatively porous. Others – such as in northern and southern Syria – are much more tightly controlled.

In Syria, Turkey exerts significant control over a territory known as the ‘Euphrates Shield Area’ (ESA). The ESA covers all the land north of Aleppo that was gained by Turkish-backed rebels in an offensive against ISIS and the forces of the Kurdish Democratic Union Party (PYD) between late 2016 and early 2017.

Economic and political developments on the Turkish side of the border have a meaningful impact in the ESA because of the overwhelming importance of Turkish influence, investment and expenditure there. For instance, the depreciation of the Turkish lira relative to the US dollar in the first half of 2018 effectively decreased the earnings of thousands of employees of local administrations and armed groups, as they received salaries in lira from Turkish state institutions. The war has also reoriented the ESA economy towards the Turkish market. The road network, for instance, is now being rebuilt to link towns in the region to Turkey. One example is a new motorway under construction between the al-Bab industrial zone and the al-Rai border crossing.

The financial sector of the ESA is also wholly integrated with the Turkish financial system. While there are no bank branches in the area, the Turkish Post Office has opened several branches. Turkish state-owned commercial banks have also opened ATMs and counters offering financial services. The hawala system is particularly developed in this border area, and is used for money transfers in all types of business transactions.

In Yemen, concentrated conflict around the western ports has increased the importance of the country’s eastern borderlands. Al-Mahra, Yemen’s easternmost governorate, has historically been the most politically and economically marginalized. Since 2015, however, the governorate has become a key transit point for goods being smuggled in and out of conflict-afflicted parts of Yemen, most importantly the Houthi-held northwest, as other routes in south and central Yemen have become less accessible.

As a result, since 2016 an increasingly fraught struggle for control of border posts and ports has emerged involving the governments of Yemen, Saudi Arabia, the UAE and Oman, as well as al-Mahra’s diverse tribes. In order to address the perceived threat posed by flows of money and goods from the governorate, the Saudi military has occupied the Nishtoun port and al-Ghayda airport – key strategic positions. This is despite resistance from a broad spectrum of tribal leaders.

Since 2016 the Saudis have closed off the southern coastal road between Oman and Yemen, and have prevented delivery of Omani fuel to depots in the al-Mahra governorate that were crucial to the movement of tribesmen. They have also prevented Omani aid from entering al-Mahra and other governorates. The power struggle has significantly reduced both licit and illicit trade in al-Mahra. This has further frustrated tribal groups, some of which have become increasingly vocal in their threats to rise up against the Saudi forces stationed in the governorate.123

Profits from arbitrage are generated at the point of sale by traders who are able to access markets on either side of transit areas and borderlands. Traders sometimes leverage their relationships with competing actors to negotiate market access, an activity which is not ostensibly violent in itself, but which supports the maintenance of the status quo. Physical control of transit points and borderlands by armed actors provides further opportunities for armed groups to tax the movement of goods. While taxation is a fee levied on the movement of the goods, arbitrage is a source of revenue generated from the sale of similar goods based on price differences. Market conditions typically vary on either side of transit areas (an internal border dividing two zones of territorial control) and borderlands (the area around an international border). With the exception of formal customs systems on international borders, the arbitrage opportunities available in a border area are often of the same nature as those in a transit area. A key dynamic to note (as also explored in the discussion of supply chains in oil-rich areas) is how conflict entrepreneurs profit from the trade of goods across front lines. This is particularly notable when warring armed groups on either side of a transit point cannot deal directly with the other side.

For people who can access markets on both sides of a territorial division, significant arbitrage opportunities exist

The increased trade friction at transit areas and external borders, while a significant source of revenue for armed actors, distorts markets. Goods available or produced in one area may not be available in another. They may become significantly more expensive as a result of fees on the movement of goods. As noted, entrenched front lines and the emergence of conflict-related governance structures can create new territorial divisions that strongly influence the development of conflict sub-economy dynamics.

Clear territorial and market divisions have thus far emerged only in Syria, although trade has been disrupted to differing degrees within and across Iraq, Libya and Yemen. In Iraq and Yemen, rivalry over local governance has created internal territorial divisions, although the fact that formal and informal trading routes have remained functional has diminished the impact of these divisions. Under its ‘caliphate’, ISIS increased the fees at certain checkpoints; in doing so, it affected the supply of goods on both sides of each checkpoint. In Yemen, shifts in the dynamics of the conflict on the Red Sea coast have impeded goods flows, in turn increasing taxation opportunities along sea and overland trading routes in the east of the country. In Libya, the intensity of the conflict has been considerably lower and territorial divisions are more blurred. Nonetheless, increasing informal taxation and insecurity in the south have detrimentally affected markets in that region. Current fighting around Tripoli has the potential to exacerbate these issues, particularly if goods entering Libya via Misrata are prevented from reaching the eastern and southern markets.

Territorial divisions in Syria have been more dynamic and openly violent than in the other three countries. Over the course of the civil war, entrenched but dynamic front lines have led to the effective ‘cantonization’ of the country, with areas controlled by the Syrian regime physically separated from those controlled by rebel groups. A range of rebel forces have established themselves as governance actors: they include opposition groups (some aligned with the Syrian National Coalition), the Syrian Kurdish-dominated administration of Rojava in the northeast, and proscribed Salafi-jihadi actors such as ISIS and HTS. Yet with the expansion of regime control to larger parts of the country, in particular the Damascus suburb of Eastern Ghouta, Daraa and a pocket north of Homs, territorial divisions have had a lesser impact on the conflict economy. As a result, in 2017 and 2018 countrywide inflation fell to single-digit levels as markets became more integrated again.

While it has been possible throughout the war for goods to move through Syria, hard territorial divisions have transformed market dynamics – this has been manifest in the erection of trade barriers and shifts in supply and demand. The barriers between territories have created price differentials, shortages of certain foodstuffs and much suffering for local populations, as well as opportunities for profit. For example, the so-called ‘siege’ economy in Eastern Ghouta124 had dire consequences for the local civilian population. However, both for the regime and for the rebel Jaysh al-Islam forces that controlled access to Eastern Ghouta, the siege became a major taxation opportunity. Traders who leveraged contacts to buy goods in Damascus and sell them in Eastern Ghouta (after paying the armed groups to allow the goods through) were able to reap massive profits: at one point a kilogramme of sugar could be sold in Eastern Ghouta for 24 times its purchase price in Damascus.125

Unlike transit areas, borderlands connect two formally distinct and separately regulated markets. Borderlands also offer the opportunity for different actors to profit from price differentials. As Box 3 indicates, external states have the power to control flows within more tightly regulated crossings.

The porous Syrian–Iraqi border, connecting two conflict economies, has been the location of a major trading post for Salafi-jihadi forces. One of these trading posts, al-Qaim, came to be known as the last bastion of ISIS forces in Iraq. The town has a history as a base for Salafi-jihadi groups. It was first held by Al-Qaeda in Iraq. Later, ISIS militarily controlled al-Qaim for several years, and in doing so was able to control historic smuggling routes. The al-Qaim border crossing served as a focal point for the smuggling of weapons, fighters and goods. Traders operating in the area benefited – and continue to benefit, post-ISIS – from the arbitrage opportunities between the Syrian and Iraqi markets. While there has been an understandable focus on weapons and fighters transiting the area, local traders have also smuggled licit goods such as sheep into Syria, where sellers could find better prices. Al-Qaim also remains an important point in the cross-border oil and gas trade. Smugglers often bring crude oil and sell it either to a refinery or to the al-Qaim oil market, one of the largest in the region. Buyers and sellers are taxed the equivalent of around US 30 cents per barrel of crude in this market. Given the flow of refugees across the border, the town has also become an important transit point for humanitarian aid in the form of food, water and medical supplies. At times, these supplies have been appropriated by militants and sold in local markets.

For a time, al-Qaim was an economic lifeline for ISIS. This helps explain its strategic importance to ISIS commanders. Following ISIS’s territorial defeat in 2017, armed groups loyal to political parties and paramilitary groups (but not to the state) were the first to fill the local security vacuum, establishing a presence ahead of the Iraqi security forces, which remain relatively weak. As a consequence, al-Qaim has become a contested area in which armed groups seek to profit from the departure of ISIS by establishing a foothold in cross-border trade – a trade which, incidentally, has never ceased to exist despite various armed groups coming and going. Sunni tribes, the PMU and criminal gangs are among the rival forces that have taken over different parts of the city’s informal and black markets and smuggling routes.

Contrary to what Western policymakers may assume, physical control of the oil-producing regions of Iraq, Libya, Syria and Yemen does not automatically confer a commensurate ability to capture revenues from oil sales. This is because there are significant barriers to entering the oil sector. Oil trade involves a complex supply chain that requires infrastructure, expertise and market access if it is to be monetized effectively.

The complexity of the oil supply chain means that armed actors seeking to wrest control of oil-producing areas must cooperate with local actors who have the expertise to operate the associated systems and facilities. As ISIS forces found in Syria, cooperation was required not only with engineers who operated the oil rigs, but also with entities that controlled those parts of the supply chain to which ISIS lacked access, namely refining capacity and tanker fleets. This broad situation – now minus the presence of ISIS forces – persists, providing continued opportunities for middlemen able to deal with armed actors on all sides.

In contrast, where an actor controls all aspects of the supply chain – as in the Yemeni governorate of Mareb – the dynamics of the oil market are determined by refining capacity. In Libya, the international community has prevented sales of crude oil from unrecognized authorities in the east of the country. This has obliged those in control of oil reserves in that region to accept the routing of crude sales via their opponents in Tripoli, in the west. Meanwhile, smuggling routes in Iraq that were originally established under Saddam Hussein to bypass international sanctions in the early 1990s still operate. These smuggling routes offer a means of patronage for those in control of the oil infrastructure in the south of the country, albeit without addressing the inequities of the centralized system of distribution, dealing with which remains a fundamental cost of doing business.

Sustainably controlling oil-rich areas requires cooperation between local leaders and armed actors. For any armed group with a newly established foothold in a particular area, it makes little sense to expel the skilled workers and broader community that have the capacity to operate the oil supply chain. Rather, the incentive will be to cut a deal with the locals. Extracting, moving, refining and selling oil is a complex and labour-intensive process that requires expertise, and a quid pro quo is therefore required. A clear example of this can be seen in northeastern Syria, where ISIS effectively reached an accord over the division of profits with the local tribes that operated the oil infrastructure. In this case, it is believed that the local tribes negotiated terms that were more or less similar to those that existed under the Syrian government, indicating that ISIS operated as a rational economic actor and recognized the necessity of cooperation. Moreover, the battle to control oil resources has not prevented cooperation over sharing them. For example, Kurdish-dominated forces rely, as ISIS forces had done before them, on engineers paid by the Syrian government to operate oil and gas facilities – including the Conoco gas plant located near Deir ez-Zor.

Local populations have maintained a degree of agency in the contest for control of oil infrastructure. Cutting deals translates into lower levels of violence. Libya’s ‘oil crescent’ – which stretches along the coast from Sirte to Ras Lanuf, and extends southwards down to the Jufra district in central Libya – contains something like 70 per cent of the country’s oil reserves and has been subject to significant power struggles. A blockade of the area by the forces of Ibrahim Jadran, a militia leader, from 2013 to late 2016 cost Libya over $100 billion in lost revenues.126 At that point, the ‘oil crescent’ was captured by forces aligned with Field Marshal Haftar’s self-styled LNA in November 2016. In March 2017, Haftar briefly lost the area to the Benghazi Defence Brigades before recapturing it a week later. Then, in April 2018, as Haftar’s forces were concentrated in an offensive on Derna, Jadran was able to recapture the ‘oil crescent’. He held the area for two weeks, before again being ousted by Haftar. The key point, often overlooked, about all these changes in the short-term balance of power is that each was preceded by the conduct of bargains with local communities in the area, with little heavy fighting involved. In other words, competitive violence was limited. This illustrates a degree of quid pro quo. While a limited amount of fighting initially caused some damage to oil and gas infrastructure, production itself was not dramatically affected except during Jadran’s blockade. The fact that the LNA’s takeovers of the ‘oil crescent’ have involved limited open fighting contrasts sharply with the intense bombardments unleashed by the LNA in Benghazi and Derna, and to a lesser extent currently in Tripoli, in much more violent attempts to defeat opponents.

The fact that the LNA’s takeovers of the ‘oil crescent’ have involved limited open fighting contrasts sharply with the intense bombardments unleashed in Benghazi and Derna

Depriving local populations of the proceeds of oil production drives political and social divisions. In Basra in Iraq, for instance, economic exclusion has entrenched armed networks of profiteers. The inequities of the Iraqi system for distributing oil revenues are stark. Basra is home to 90 per cent of Iraq’s oil production, which account for 95 per cent of the revenues of the central government in Baghdad.127 Yet this wealth has not trickled down to Basra’s residents. The province remains destitute, lacking basic services such as electricity and water. Reflecting economic malaise and political volatility, a vibrant protest movement has defined provincial politics, with citizens vocal in expressing grievances against the local and central governments. Protesters have on several occasions demonstrated against oil companies, blocking key roads and marching in front of their offices in a show of their anger and disillusionment.

The distribution system is sustained by an implicit understanding that local networks (which include armed groups) will be able to extract rents from the system in return for ensuring its continued functioning. A major factor in the looting of Basra’s oil resources has been the role of Iraqi state actors, many of which are either complicit in this activity or unwilling or unable to stop it. The local oil industry either lacks the equipment to measure its losses or deliberately chooses not to employ proper detection mechanisms, due to the tacit agreement with state employees and officials. Lack of capacity, incompetence and deliberate fraud are all potential explanations. For the central government, providing a source of revenue to armed tribes and groups in effect is merely another form of subsidization, and far easier to implement than institutionalization and formal revenue-sharing between the centre and the periphery.128 Moreover, maritime police and border guards are unable to capture smugglers, and are often under orders not to arrest members of the cartels.

The international community has mistakenly equated military control of oil fields with a monopoly over the revenues generated by them. Physical control over these areas is a necessary but insufficient condition for monetizing the oil trade. The complexities of Basra’s smuggling industry illustrate the breadth of actors involved. In Syria, the emphasis on oil as a source of revenue for ISIS prompted the US-led anti-ISIS coalition to conduct a widespread bombing campaign targeting oil and gas infrastructure in 2015. The objective was to reduce ISIS’s revenues, yet the policy also devastated the livelihoods of local populations and removed their principal source of heating oil just as winter was setting in. The incident offers an example of the perils of intervening in a conflict sub-economy where coping mechanisms are inextricably linked with revenue generation for armed actors.

In Syria, elements of the oil supply chain are controlled by actors in conflict with each other. Recognition of the need to monetize those elements under their control has led armed groups to tolerate a degree of cooperation with their rivals. Moreover, where this has not been possible through direct relations, profiteering opportunities for middlemen have arisen. Syria’s oil resources are overwhelmingly located in the country’s northeastern region, with around 85 per cent of extraction taking place between the Euphrates River and the Iraqi border.129 Between roughly 2013 and 2017, the northeast was divided into two areas of control: in the north, the so-called Jazira region was under the control of the Kurdish People’s Protection Units (Yekîneyên Parastina Gel – YPG), the military arm of the Kurdish Democratic Union Party (Partiya Yekîtiya Demokrat – PYD), which in turn is affiliated to the Kurdistan Workers’ Party (Partiya Karkerên Kurdistanê – PKK); meanwhile the southern part, including the city of Raqqa and half of the city of Deir ez-Zor, was under the rule of ISIS. Routes along the Euphrates River were also ISIS-controlled, meaning that most commodities traded with the northeast transited through areas under ISIS rule.130 Yet the country’s only two refineries are in Homs and Baniyas, territory that has remained under regime control. Hence, oil can be extracted from a field controlled by the PYD, transported by tankers operated by members of local tribes, then reach the regime, which will refine it and send some of it back to the eastern region. Other shipments will reach opposition areas, with some ending up in Turkey – thus generating revenues for each of the militias, checkpoints and border crossings (and the groups that control them) along the way.

Oil can be extracted from a field controlled by the PYD, transported by tankers operated by members of local tribes, then reach the regime, which will refine it and send some of it back to the eastern region

In most cases, money earned from these activities in Syria has directly financed the warring armed groups. But it has also had an indirect impact on conflict economy actors, enabling intermediaries to earn hefty commissions and make financial contributions to the regime’s war effort. Among such intermediaries, two regime-affiliated figures have risen to prominence. Baraa Qaterji, a businessman originally from Raqqa who is now established in Aleppo, was identified by the US Office of Foreign Assets Control (OFAC) as a middleman between the regime and ISIS for the trade of oil products. Baraa operates in partnership with his brother, Hussam, who was put under sanctions by the EU in January 2019. The brothers have effectively become beneficiaries of Syria’s internal trade barriers. In recent years, both have employed intense competitive violence to control territory and access to resources. Besides doing business with the YPG and ISIS, they have worked with armed forces from opposition groups, the Assad regime and Iran.

Following the US-led invasion in 2003 and the breakdown of state order in Basra, armed groups vied for control of the area’s territory and resources. In Basra, by 2007, it was estimated that Muqtada al-Sadr’s Mahdi Army (Jaysh al-Mahdi) was stealing around $5 million worth of oil per day – most notably from the Abu Flus port – and selling it on the black market. By 2013, Shia Islamist armed groups and associated political parties were reported to be running 62 floating docks in the province of Basra, with nine armed groups controlling the port and collecting protection fees.131 Whereas in 2003 protection fees used to be around $100 per month, by 2014 the rise in the oil price had pushed them up to around $10,000 per month (to continue or to expand smuggling operations).132 The spike in oil prices from the mid-2000s to 2014 enriched the actors in this system, creating a nouveau riche and leading to market distortions: for instance, residential real estate rents in Basra skyrocketed to over $2,000 per month. As a result, a large proportion of Basrawis – excluded from employment or access to kickbacks in the oil sector – have become part of an underclass, suffering from a lack of electricity, water and jobs (which wasn’t a problem under Saddam). By the 2018 elections, the voter turnout in Basra was calculated at 14.4 per cent – underlining the high levels of political disillusionment in the city.133