The austerity campaign was pursued comprehensively and determinedly, with major constituencies badly affected. For instance, in 2016 state pensions were indexed according to the CBR’s inflation target of 4 per cent, rather than, as is customary, the rate of consumer price inflation in the preceding year – which would have meant an increase in double digits. For those 9 million pensioners who were still working, pension increments were suspended altogether. Yet pensioners did not storm the Kremlin, nor were their complaints as vocal as, for example, they had been a decade previously over benefit reform.

Federal budget transfers to the regions were cut. The value of transfers to the regions in 2015, in constant prices, was only 77 per cent of their equivalent in 2009 – also a recession year. Regional real-terms spending on health and education was reduced, and poorer regions’ bank debt increased. That the regions suffered harsher treatment in 2015 than was the case in 2009 may be explained in part by the existence of sanctions this time around, but the difference is still striking. All the same, no region attempted to secede from the Russian Federation.

There were real-terms cuts in spending on ‘national defence’ – the official Russian designation, which is about 1 per cent of GDP less than the standard Western definition. If the fulfilment of past credit guarantees in 2016 is excluded, there was a clear fall – in both nominal and real-terms – from 2015. In real terms, Western-definition defence spending fell by about 8 per cent year on year. One account, from 2016, of a clash over military spending states that in a discussion of the draft military modernization programme for 2018–25, the defence minister, Sergei Shoigu, ‘yelled’ at the finance minister, Anton Siluanov, accusing him of undermining the modernization of the military and threatening national security. A Kommersant report of the same incident refers rather more euphemistically to ‘raised tones’. At all events, there was no military coup.

Russia’s business community complained about high interest rates, but got nowhere with the central bank. Elvira Nabiullina, the CBR governor since 2013, had Putin’s explicit endorsement; in March 2017 he confirmed his intention to appoint her for a further term of office.

An important legislative restriction on federal public spending came into effect in 2017: under this new ‘budget rule’, tax revenue from oil at prices above $40 per barrel (this threshold rising at 2 per cent a year from 2018) is not available for budget expenditure but is instead paid into the National Welfare Fund (NWF). There was some grumbling, but as at late 2019 the rule has held.

There is one disagreement over the budget rule between the IMF and the Russian government. The government plans to make available some NWF money for domestic infrastructure finance, over and above a minimum level (7 per cent of GDP) of the liquid resources of the NWF; the IMF would prefer that the whole of the NWF be invested in foreign assets, completely sterilizing the inflow of petro-dollars – i.e. excluding this revenue from the domestic flow of money. In June 2019 CBR governor Nabiullina notably also suggested that the threshold of 7 per cent of GDP should be reconsidered.

One bit of intra-elite fighting – albeit only indirectly related to austerity – did become visible with the arrest of the economic development minister, Aleksei Ulyukaev, in November 2016. Ulyukaev had apparently displeased Igor Sechin, the boss of Rosneft, by objecting to Rosneft in effect ‘privatizing’ the smaller state oil company Bashneft. The link to fiscal austerity is that the sale of a controlling stake in Bashneft and of a minority stake in Rosneft was a device to boost the public finances.

All in all, Russia’s austerity campaign was pushed through more easily, as far as outside observers can judge, than such programmes usually are in Western countries.

All in all, Russia’s austerity campaign was pushed through more easily, as far as outside observers can judge, than such programmes usually are in Western countries. The main constituencies ultimately proved biddable and obedient. That is not to say that such passivity has no limits: the subsequent raising of pension ages may have pushed at those limits. It seems reasonable, however, to conjecture that Putin’s own support for financial prudence sent a pretty clear message to the political and business elite. An authoritarian system has advantages when it comes to implementing austerity measures.

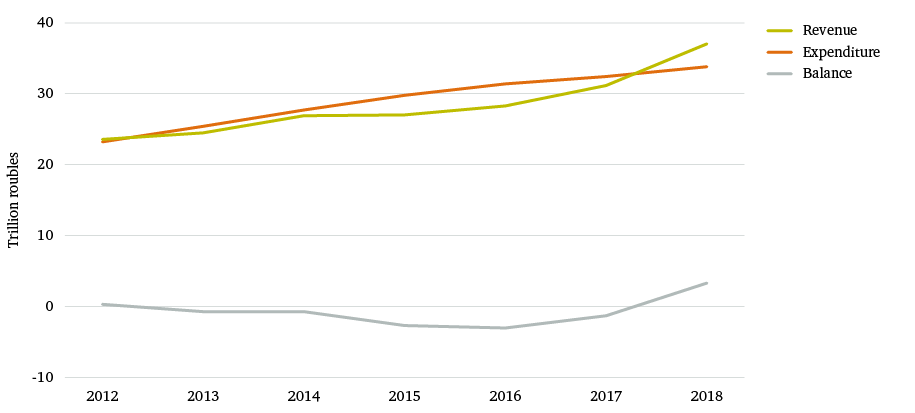

Can the macro-stabilization effort be described as a success? Yes, in so far as inflation has been brought down, public finances are in good order, and there has been a recovery in economic activity – albeit a recovery that leaves the Russian elite and many ordinary Russians dissatisfied.