The COVID-19 crisis could lead to a wider rethink of Europe’s political economy. This paper explores what such a model might look like, and what it would mean for the governance of the European Union.

Research paper

Published 8 June 2020

Updated 26 September 2024

ISBN: 978 1 78413 403 7

The COVID-19 crisis could lead to a wider rethink of Europe’s political economy. This paper explores what such a model might look like, and what it would mean for the governance of the European Union.

The exact shape of the post-coronavirus European political economy is impossible to predict. However, it is feasible to identify certain elements that could emerge at a national level, based on some of the clear shortcomings and vulnerabilities that the pandemic has revealed and exacerbated. First and foremost, it is assumed here that the crisis will lead to a larger role for the state in the economy. Following decades in which the governing consensus largely dismissed the effectiveness of state intervention in many areas of life (albeit with the balance struck differently in different parts of Europe), the pandemic and the response to it have highlighted the power of the state in no uncertain terms, notably its central role in providing universal healthcare and essential economic relief.

What was previously regarded by many as politically unnecessary, undesirable or just impossible has been shown to be both essential and deliverable.

The way in which many European governments have used unprecedented fiscal and monetary firepower to put economies into semi-hibernation is likely to change how people think about state capacity. The crisis has revealed the state as the fundamental guarantor of the economy, and has expanded public awareness of the policy options available. What was previously regarded by many as politically unnecessary, undesirable or just impossible has been shown to be both essential and deliverable. Governments have discarded long-standing policy restraints such as concerns for fiscal deficits and public debt sustainability (which, alongside the centrality of market mechanisms, were features of the dominant paradigm). In the future, governments may feel more compelled to solve challenges which they have previously considered beyond them, and to build on the experience of the current economic dislocation to push through significant changes to their political economies. One can envisage potential changes in three areas in particular: (1) fiscal policy and taxation, (2) labour markets and redistribution, and (3) industrial policy.

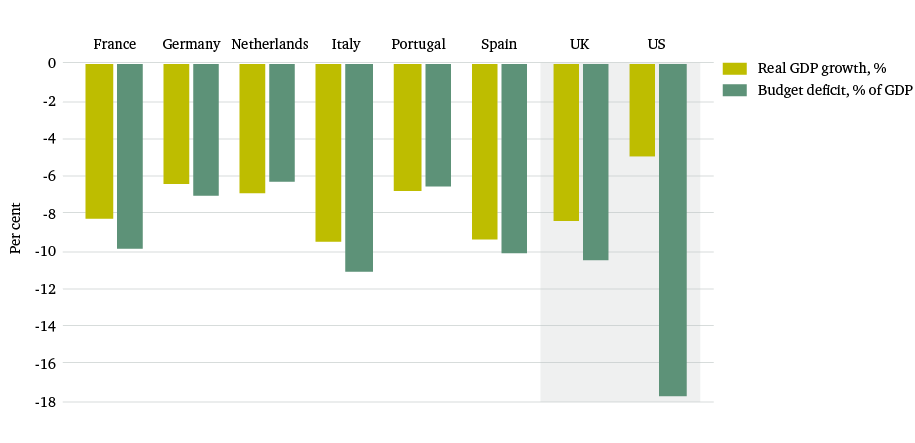

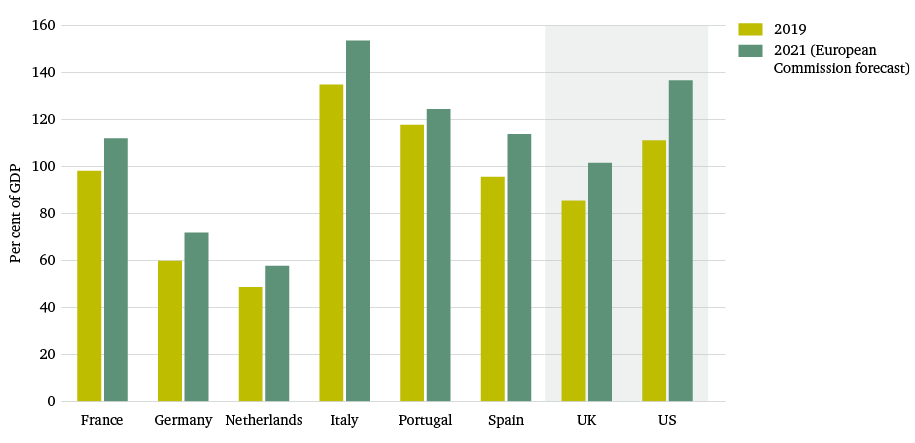

A larger role for the state would almost certainly entail increased government spending. During the coronavirus crisis, European governments have demonstrated an unprecedented willingness to increase spending by, for instance, paying the wages of millions of furloughed workers. In order to enable governments to put large parts of their economies into hibernation, the European Commission has suspended the EU’s fiscal rules, and even the most fiscally conservative member states, such as Austria and the Netherlands, have announced large stimulus packages. Perhaps most strikingly, the German government has rapidly, albeit temporarily, let go of its so-called ‘black zero’ policy of balanced budgets, which in recent years has defined the country’s approach to fiscal policy. The size and effectiveness of the stimulus measures, as well as the speed with which they were designed, approved and implemented, could create popular expectations of continued or more extensive state intervention in the future.

Comparison with the 2008–09 financial crisis is pertinent here. In its aftermath, many European countries primarily used cuts in public expenditure to tackle budget deficits and high public debt levels, which had been caused in part by the fiscal stimulus initially deployed in response to that crisis. But the painful experiences of austerity over the subsequent decade, combined with the political impact of the coronavirus crisis itself, suggest a similar approach is untenable this time. Instead, it seems likely that governments will both raise the overall tax burden and change how it is allocated. States may introduce wealth taxes in an effort to correct the balance between capital and labour and address broader issues of inequality.

Tensions over these issues were already present before the coronavirus crisis, but they are being exacerbated today, particularly as sectors such as tourism and hospitality (with the most precarious forms of employment) have been hit hardest. Meanwhile, more secure, high-wage sectors have had much more opportunity to continue operating in an environment of self-isolation, and have been able to access government support schemes. Correcting the distributive economic effects of the crisis could now become a policy priority, reflecting demands to reform the system that created such unequal vulnerability. Measures could include new or increased taxes on land, property, capital income or capital gains.

Higher corporate taxes would also be an obvious response in light of the massive support that governments have provided to the private sector. When the crisis struck, the lack of financial buffers in the corporate sector necessitated immediate government intervention. Policymakers may now try to regulate companies more robustly to make them more resilient to future shocks and downturns. European governments are likely not just to raise corporate tax rates but also to crack down more firmly and unilaterally on international tax optimization by multinationals – as Belgium, Denmark, France, Italy and Poland have already done in their responses to the coronavirus.15 The political imperative for such measures is clear: citizens are already complaining loudly about governments providing life support to businesses that had previously exploited favourable tax structures to lower their tax bills.

European governments are also likely to move away from a focus on labour market flexibility towards a model that provides greater security for workers. This would be a natural response to the growth of precarious employment over the past decade, including of ‘critical workers’, whose vulnerability has been highlighted by the coronavirus crisis. The long-term social and political effects of a shift in welfare policy away from the limited and conditional model favoured under the neoliberal consensus to one with a broader reach are unclear, but could be substantial. Some governments have already discussed introducing temporary forms of basic income, which in time could be expanded (e.g. to offer more generous benefits) and /or made permanent. Once in place, universal benefits would likely create a change in the public mind-set and become entrenched and politically very difficult to remove.

Finally, European governments can be expected to spend more on healthcare and other selected policy areas. Even before the pandemic, healthcare expenditure was already rising in almost every EU country – a function of the easing of the euro crisis as well as long-term demographic trends and the increasing sophistication of modern medicine. As that process accelerates in the coming years, healthcare will consume an ever higher share of GDP. The same trend could be observed in a range of policy areas that have faced significant budget cuts in the past, including education and social welfare. There may also be a move to renationalize, or ‘remunicipalize’, previously privatized basic service providers in areas such as healthcare.

In contrast, certain other categories of spending may face greater scrutiny as changing political preferences lead to a reassessment of their value. In particular, governments may come under public pressure to reduce conventional defence capacity and reallocate resources towards spending that more visibly improves social and state resilience. Recession will add to the pressure on public finances. Defence budgets – frequently the target of government cost-cutting during economic downturns – will likely be reduced. For example, following the global financial crisis, European defence spending fell by about 11 per cent.16 Defence funding priorities also risk shifting in the post-COVID-19 world. With the UK defence secretary recently declaring ‘lack of resilience’ as the new number one threat,17 it may be harder for governments to justify expenditure dedicated to expensive procurement programmes for conventional capabilities against traditional threats.

European governments may take a new and more activist approach to industrial policy, increasing state control and planning of the economy. The coronavirus crisis could undermine the previously prevailing orthodoxy which favoured smaller states, limited government and free markets. The EU has relaxed rules on state aid to allow governments to support businesses, including through large relief packages for hard-hit industries such as aviation. Member states might push to continue to bypass these rules after the crisis – initially to support the recovery but also for other reasons, such as in pursuit of climate goals. The risk is that this could undermine the single market by distorting the level playing field within the bloc. Some companies may be nationalized or continue to receive significant government support in order to sustain themselves.

Agriculture, for example, which already receives high levels of government support, could become further protected by the state. Governments could also take a more active role in energy provision by combining a new approach to state resilience with the ongoing need to address the climate crisis. Beyond these sectors, European governments or the EU may attempt to protect industries or favour national champions that produce critical supplies, such as in biomedical sciences – perhaps by applying something like the approach of the Common Agricultural Policy to other sectors of the economy.18 A potentially higher degree of caution towards China could lead to greater industrial support in new areas to avoid over-reliance on Chinese companies and technology, and to ward off perceived or real competition from Chinese firms.

Changes in these policy areas will likely manifest themselves in different ways, and to varying degrees, across the EU, for two reasons. First, even within the framework of the EU and the single market, the extent of state activity and welfare provision varies considerably from one country to the next. Countries with more developed welfare states, well-funded healthcare systems and the resources to put their economies in hibernation – such as Germany and Austria – are likely to come out of the crisis with less damage, and may hesitate to make big societal changes. Despite the shared regulatory space of the single market, countries do not start from the same position when it comes to the relationship between state and market.

Countries with more developed welfare states, well-funded healthcare systems and the resources to put their economies in hibernation – such as Germany and Austria – are likely to come out of the crisis with less damage, and may hesitate to make big societal changes.

Second, the pandemic has so far affected different European countries in different ways. At first glance, it seemed likely to be more of a symmetric shock than the eurozone debt crisis or 2015 refugee crisis – as COVID-19 has affected all countries in Europe. But whereas the crisis hit Italy particularly early and hard, other EU member states had extra time to develop their responses, which helped at least some of them (such as Greece) to minimize its impact. Other differences, such as in demographics and economic structure, have also contributed to variations in the spread of the virus and the effectiveness of state response. In other words, the shock also has elements of asymmetry. This means that one should not necessarily expect any shift in the relationship between state and market to occur in a uniform way. The danger is that the crisis may thus lead to further economic divergence within Europe.19