The COVID-19 crisis could lead to a wider rethink of Europe’s political economy. This paper explores what such a model might look like, and what it would mean for the governance of the European Union.

Research paper

Published 8 June 2020

Updated 26 September 2024

ISBN: 978 1 78413 403 7

The COVID-19 crisis could lead to a wider rethink of Europe’s political economy. This paper explores what such a model might look like, and what it would mean for the governance of the European Union.

If a new political economy were to emerge at national level in some parts of Europe, what would this mean for supranational governance? Countries that are outside the EU will be comparatively freer to tailor the balance between state and market to their own needs – as the UK will be once it ends its transitionary Brexit arrangements. EU member states, on the other hand, will need to reconcile any such shift with the requirements and obligations of their membership.

As discussed, the EU evolved in size and policy orientation against the background of the neoliberal turn and the emergence of ‘hyper-globalization’. Many of the structures of the EU as it is today were designed to limit the capacity of member state governments to intervene in the functioning of the market. In particular, the bias towards ‘negative’ integration had the effect of impeding state intervention at the national level. Yet in many areas it proved difficult to create the corresponding instruments at a European level to achieve social objectives or manage the consequences of interconnected markets. A shifting settlement between the state and the market would therefore raise questions over the sustainability of existing forms of integration and the institutional architecture created to govern them.

Potentially, the EU itself could become the driver of change in Europe’s political economy, championing a renewed focus on solidarity, welfare and the reduction of inequality between and within states. In some areas, such as tax policy, working at the EU level would be more effective, potentially reducing capital flight and regulatory and tax arbitrage. In a Europe in which a broad consensus emerged on changing the balance between state and market, EU institutions might take the lead on reform. This could involve a number of ambitious measures:

Delivering such an ambitious agenda, aspects of which have been extensively debated or considered at EU level in the past, would require wide consensus among member states on implementing substantive economic and legal reform of the EU. It would almost certainly require negotiating changes to the EU treaties, as well as wider reform of the EU’s institutions in order to provide legitimacy and accountability for such a large-scale expansion of the role of the EU – or what is sometimes termed ‘political union’.

However, while some modest measures appear both possible and likely, it seems doubtful that the coronavirus crisis will lead to a decisive political breakthrough, given the uneven impacts of the pandemic and the different starting points of member states, both economically and politically. The recent political quarrels over ‘coronabonds’ exposed the gaps between member states rather than helping bridge them. At the outset of the crisis, the only EU institution to move in a more radical direction from past policies was the ECB, which does not require agreement from member states – though the recent ruling by the German constitutional court on the ECB’s bond-buying programme has now limited its room for manoeuvre.20

It seems doubtful that the coronavirus crisis will lead to a decisive political breakthrough, given the uneven impacts of the pandemic and the different starting points of member states, both economically and politically.

In mid-May, France and Germany proposed an EU recovery fund, which was subsequently turned into a more detailed proposal by the European Commission. Such a fund – totalling €750 billion in grants and loans – would be financed by collective borrowing through the European Commission. This has been interpreted by some analysts as a response to the German constitutional court ruling and even as a kind of ‘Hamiltonian moment’ that may lead to a real fiscal or even political union analogous to the United States.21 But while the recovery fund would undoubtedly be a step forward, it would be a one-off EU instrument, as opposed to a permanent mechanism to address structural imbalances in the EU. It therefore would not constitute a significant step towards ‘completing’ economic and monetary union, nor would it represent a significant change in the EU’s economic governance structure.22

These difficulties may reflect a more fundamental challenge: whether the EU as currently constituted (and encompassing such a diversity of states) is capable of major structural changes. The long-standing practice of treaty-driven integration, in which regular and periodic evolutions in constitutional aspects of the EU have been agreed through new treaties, has effectively come to a halt. As discussed above, it was through treaty change that the EU was able to evolve and reflect wider shifts in the political economy in the 1980s and 1990s. For long periods during the euro crisis, it was widely expected that another treaty change would occur at some stage. However, although minor amendments were made to the treaties, European leaders avoided a major overhaul because this would almost certainly have required multiple referendums across the EU and would therefore have been fraught with political risk (as the experiences of France and the Netherlands over the constitutional treaty in 2005, and of the UK in its 2016 referendum on EU membership, illustrate). As mentioned, the risk is that the EU may now be stuck in a politically unstable status quo without a shared view among member states on how to change it, and therefore be unable to accommodate national shifts in the state–market paradigm. Working around the treaties – the strategy employed during the euro crisis – is a lot harder when the problem lies with what the treaties say instead of what they lack.

Rather than catalysing a transformation of the EU in support of a different economic model, it seems more likely that COVID-19 will lead to an uneven shift in economic policy across different countries. This would bring the political trajectories of some member states into conflict with the existing regulatory framework, and generate greater economic and political divergence within the union. One way to start considering the implications for European integration is to examine how shifts in the three policy areas discussed above might specifically intersect with this EU framework.

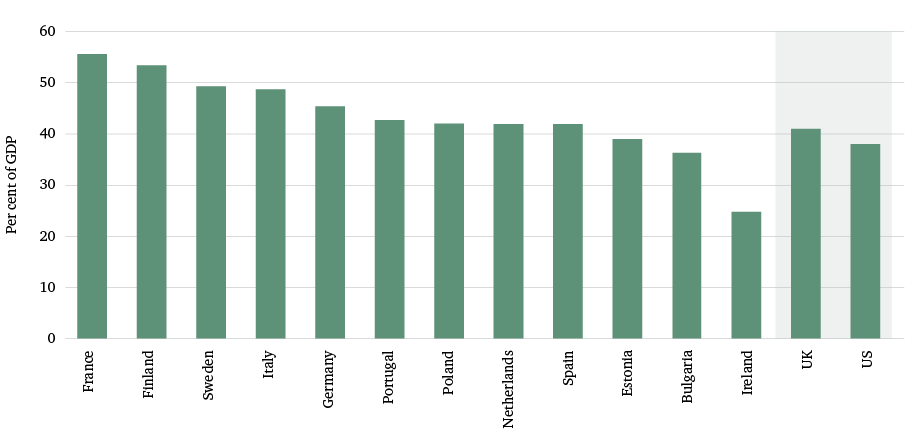

The most obvious clash between the EU system and a shift towards a more interventionist state could be over the fiscal rules, which are particularly relevant for the member states that use the euro. There is no EU rule prohibiting a high level of state spending per se – several European governments, such as France and Finland, were already spending more than 50 per cent of GDP before the current crisis. But for some states, expenditure increases will almost certainly mean continuing to break the fiscal rules, which prohibit eurozone countries from running a budget deficit equivalent to over 3 per cent of GDP or accumulating public debt equivalent to over 60 per cent of GDP. The question is whether the EU will reform these rules or try to enforce them again, the latter of which would require drastic austerity.

Shifting the burden of taxation will also be difficult without EU-wide, or preferably global, cooperation. Attempts to tax wealth or capital gains are famously vulnerable to capital flight. The success of national efforts in this direction will be seriously constrained if they are not followed through uniformly. A similar issue arises around attempts to end tax competition and tax optimization by multinational firms. This topic has created tensions within the EU in the past, as southern members were irked by the practice of some northern members (such as Ireland and the Netherlands) using favourable tax regimes to persuade companies to locate headquarters in their jurisdictions. Meanwhile, despite being able to choose where they pay tax, companies can still sell throughout the single market from their chosen base. In time, there is a risk that these single-market rules will come under pressure as governments attempt to tax multinationals, for instance large technology companies, more aggressively.

Attempts by national governments to build more protective and less precarious labour markets would not immediately conflict with EU rules. Except for rules related to the free movement of workers, labour market policy remains largely a member state competency. This is visible in the wide divergence in labour market institutions and protections between member states. The European Commission has been moving to expand the EU’s role in this area through the Work Programme 2020, intended to create more commonality at a European level on issues such as minimum wages and unemployment insurance. However, significant shifts in how labour markets are governed within member states could conflict with the imperative of keeping markets open to workers from across the EU.

For instance, despite the European Commission’s published guidelines to ensure the movement of critical workers during the pandemic, there have been reports of seasonal workers being sent back to their countries when attempting to cross borders. If restrictions of this kind persist beyond the end of the COVID-19 state of emergency in place in several EU countries, it could heighten tensions among member states and jeopardize the integrity of the principle of free movement. Previous disagreements between western and eastern member states over the ‘posted workers’ directive highlight the political salience of these issues and the difficulty of resolving them.

Some tensions in these policy areas have always been visible in the EU. Many social security and labour market protections require strong social contracts, as they are a form of obligatory collective insurance. This has often led to politicized demands to exclude some groups – usually foreign workers – who have not paid into the relevant scheme for a sustained period or who are seen as somehow less legitimate users of public services. There are also potential questions over unfair competition when some workers are covered by and paying into the insurance system and others are not.

Increasing the hand of the state in the economy potentially clashes with a number of fundamental tenets of the EU, particularly where any measures involve state support for specific companies. EU state aid rules prevent governments from granting national monopolies, and EU competition policy can throw up barriers to attempts to create, or maintain, national ‘champions’ – as the current case of Lufthansa illustrates.23 It can even be a barrier to the creation of European champions, as was demonstrated by the failed merger of the German engineering conglomerate, Siemens, and France’s Alstom in 2019. Even before the COVID-19 crisis, France, Germany, Italy and Poland were demanding that the European Commission show ‘more justified and reasonable flexibility’ in allowing mergers that could forge European champions. Such demands will likely become stronger in the future.

The imperative to increase economic resilience is also likely to be reflected in stronger state controls over ownership of critical industry, and wider definitions of what constitute ‘critical’ sectors. For now, restrictive measures tend to apply to investments originating outside the EU – see, for instance, the German government’s new plans to include healthcare in its more stringent investment screening mechanism. However, further moves to ‘re-shore’ critical production could lead to a decreased openness to intra-EU capital flows. If states started exploring ways to ensure critical national industries were domestically owned or located, rather than owned or based in other EU states, this would likely bring them into conflict with EU competition law. National-interest dynamics similar to those that have played out in the defence-industrial sector could thus apply in new areas. For example, in 2017, France nationalized the STX shipyard to prevent it falling into Italian ownership.24

Attempts to support national industry could also have consequences for the EU’s external trade policy. Some member states might want to use trade policy to protect national champions, for instance by stronger insistence on maintaining tariffs or non-tariff barriers on specific sectors in trade agreements. This would lead not so much to a clash with the EU as to tensions between member states about the future direction of EU trade policy. It would also complicate an area of European cooperation – over trade policy – that has been among the most successful in recent years.