These debates and trends are seen by some as hiding the true extent and speed of the transition, which is already significantly changing investment patterns. In 2018, 57 per cent of global supply investments in the power sector were in renewable sources. Solar PV and wind, which now account for most renewable energy investments, already produce electricity at a lower cost than fossil fuels in many countries. While the system integration costs of some renewable energy sources may be higher than those of conventional generation, falling storage costs and smarter balancing technologies are likely to mean that it is only a matter of time before these technological advances create an economic rather than an environmental imperative to go renewable. The longer-term investment community is engaging with the concept of declining fossil fuel demand, and many investors view the likelihood of stranded oil and gas assets as credible.

While there is broad agreement among countries and companies that this energy transition is under way, there is less agreement regarding its speed and scale. As with previous energy transitions, once the initial trigger is pulled, other reinforcing factors come into play, changing the relative price and availability of energy sources. These factors range from incremental shifts such as energy efficiency and smarter demand, to more disruptive shifts such as the collapsing cost of renewable energy and battery technology, and faster-than-anticipated EV uptake. Traditional factors are also still an important consideration, with the potential for oil price shocks due to geopolitical upheavals recently returning to the fore.

Government policies have a key role to play and over time will partly determine the quantity and sources of energy that are consumed. The IEA highlights the role of policies and measures in their World Energy Outlook (WEO) analysis, which shows a range of possible global energy consumption by 2040 depending on the extent of government intervention, particularly on climate change (see Figure 1). Under the different scenarios, compared to 2018 levels, fossil fuel consumption varies considerably: current policies lead to a 20 per cent increase; stated policies (where policy goals or targets have been set but the measures to achieve them have not been implemented) result in a 14 per cent increase; while in a scenario in which policies are put in place to meet international agreed climate targets fossil fuel consumption falls by 33 per cent.

Global emissions continue to rise, as the United Nations Environment Programme (UNEP) notes: total greenhouse gas (GHG) emissions grew by 1.5 per cent each year from 2009 to 2018 without land-use change (LUC); and 1.3 per cent each year with LUC, to reach a record high of 51.8 gigatonnes of carbon dioxide equivalent (GtCO2e) in 2018 without LUC emissions and 55.3 GtCO2e in 2018 with LUC. UNEP highlighted that in 2018 there was an increase in the growth of emissions, and that ‘there is no sign of a peak in any of the GHG emissions’. Emissions directly from the energy sector in 2018 grew 1.7 per cent to reach a historic high of 33.1 GtCO2. It was the highest rate of growth since 2013, and 70 per cent higher than the average annual increase since 2010. Coal-fired power plants were the single largest contributor to emissions growth in 2018 with annual total emissions surpassing 10 GtCO2 (up 2.9 per cent year-on-year); non-energy coal use also produced significant emissions of 4.5 GtCO2.

Managing the consequences of climate change is in turn accelerating the need for a rapid move away from the use of fossil fuels. The publication of special reports by the International Panel on Climate Change (IPCC) – Global Warming of 1.5°C in 2018 and Climate Change and Land in 2019 – focused scientific, political and public concern over climate change, prompting calls for more ambitious national climate change mitigation targets. Some countries, such as France and the UK, introduced the target of reaching ‘net-zero’ carbon emissions (hereafter net-zero) by 2050. However, setting targets is only one element of a necessary and complex set of policies and measures that are needed to reduce emissions. International pressure on climate change mitigation plans is anticipated to continue during 2020 ahead of the next Conference of the Parties (COP26) of the United Nations Framework Convention on Climate Change (UNFCCC), expected to be in Glasgow in 2021.

Reducing emissions from the coal sector is therefore fundamental to any global mitigation strategy. It is broadly recognized that this could be achieved by system-wide efficiency improvements, switching to lower-carbon alternatives, renewable electricity generation or the capturing of emissions. More contested is the option of switching from coal to natural gas in power generation, which could rapidly reduce emissions, as gas generates less than half the emissions per kilowatt hour (kWh) of coal. However, without decarbonizing gas and/or using CCS, the use of natural gas is incompatible in the long term with climate targets and therefore risks creating stranded assets or locking-in emissions pathways.

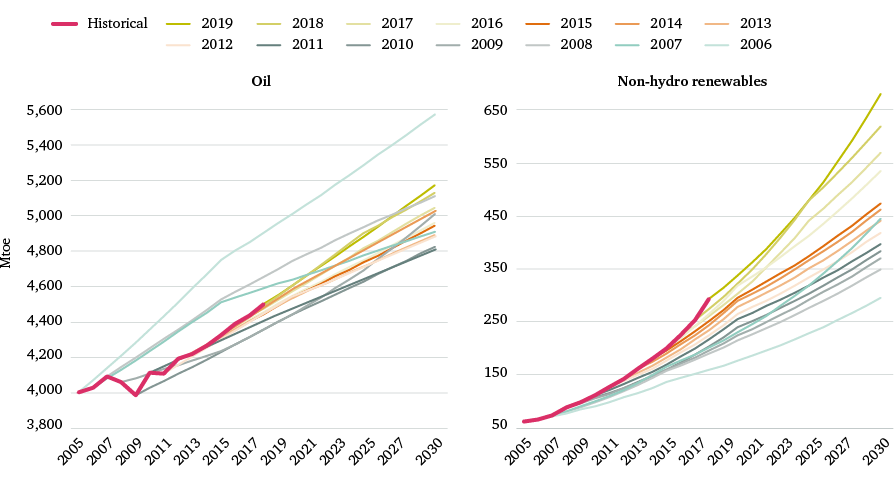

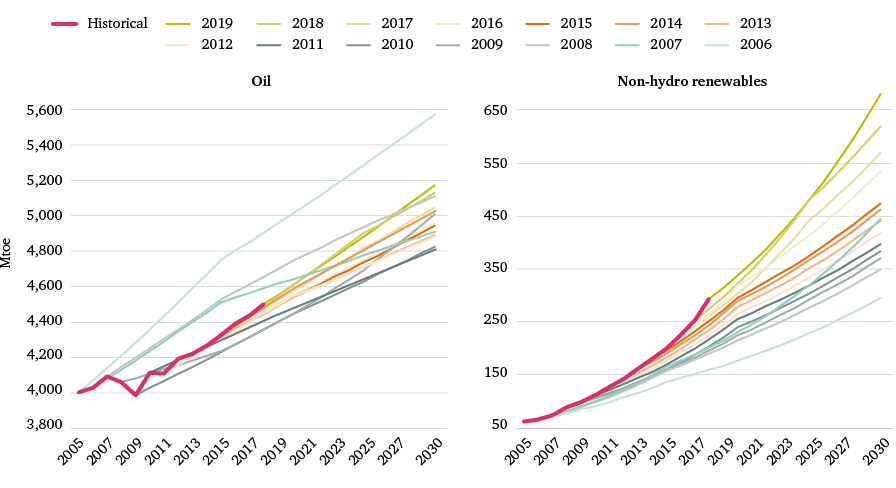

There is increasing debate about when oil and gas demand will peak, yet in many ways this is the wrong question. What matters is what happens after the peak; will there be an extended plateau, a gentle decline or a sudden collapse?

There is increasing debate about when oil and gas demand will peak, yet in many ways this is the wrong question. What matters is what happens after the peak; will there be an extended plateau, a gentle decline or a sudden collapse? Where oil is concerned, it is already clear that OECD demand has peaked, and many believe the ‘rest of the world’ demand will peak before 2030. One of the primary arguments to counter this view (alongside scepticism about the pace of change in transport) is the idea that rising demand for oil as a petrochemical feedstock for plastics and fertilizers, for example, will offset falling demand in other sectors. In its Future of Petrochemicals report, the IEA found that petrochemicals currently account for about 14 per cent of oil demand and 8 per cent of natural gas, but could constitute one-third of oil demand growth to 2030 and half by 2050, as well as rising volumes of natural gas. However, such projections may be overstating demand for plastics (of which 36 per cent is used in packaging) in established and emerging markets, given growing concern over single-use plastics and their impact on the environment, and the development of alternative materials and more circular value chains. The manufacture of plastic, fibres and rubber consumes about 40 per cent of the fossil fuels used within the chemical sector.

While changes in consumption levels are important, especially from a CO2 perspective, the impact of ‘peak demand’ on oil producers is not so much about the immediate effect on sales volumes but the effect on current and future prices. Mainstream scenarios all suggest that falling demand will lead to lower prices over time, although there could still be volatility along the way in the event of a geopolitical upset or if a rapid decline in fossil fuel production leads to a relatively short-term supply crunch, for example, both of which would create a temporary price spike.

There is considerable debate around whether gas can provide a ‘bridge’ to a decarbonized energy system, given its infrastructure needs, price constraints and the lack of clarity over how it would then be phased out. On current trends, there is every possibility that global demand for oil and gas will not grow as anticipated to 2030 and will be significantly below current levels by 2050. Indeed, the long-term goals of the Paris Agreement suggest that oil consumption in 2050 will need to be at least 50 per cent lower than today, and gas demand one-third lower. With rising climate and environmental pressures, the transition is increasingly likely to be driven by real economic and societal shifts.

Norway’s role in the energy transition

As one of the world’s largest exporters of energy and capital, Norway has a significant stake in the energy transition, as well as considerable influence over it. Factors such as the price of oil in a declining global market and the role of gas in a decarbonizing Europe will shape Norway’s energy relations in the coming decades. So, too, will its overseas investments and its policy experience in transitions in transport and industry (including the oil and gas sector). Clear signalling from the major energy nations would reduce at least some of the uncertainties surrounding the energy transition. By defining its energy transition, including the role of its oil and gas exports and investments, Norway could demonstrate real leadership among oil and gas producers, and help to encourage meaningful engagement with the end-point of the energy transition, as well as its start. This could also help to guide an orderly transition in the energy, power and industrial sectors, which are critical given both their importance to the Norwegian economy and their exposure to decarbonization trends.

This research paper explores the opportunities and challenges for Norway, as seen by its international partners. Through a series of interviews with 15 experts, it explores a range of important questions for Norway’s energy future in a European and global context, including:

- the speed and scale of transition globally and in those regions and countries that are heavily dependent on fossil fuels, especially those dependent on Norwegian oil and gas;

- Norway’s position in a potentially declining and increasingly competitive fossil fuel market, and what this means for the competitiveness of its heavy industry;

- the role for existing fossil fuels and energy infrastructure in a decarbonizing world;

- the emergence of climate-related financial risks and their influence on Norway’s decisions regarding future production and the management of its SWF;

- whether power systems become decentralized or retain a core of large-scale, centralized generation and, in turn, the role of interconnectors and Norway’s hydropower; and

- the development of the European Energy Union and Norway’s role within that, including its role in delivering net-zero targets enhancing energy security and developing new industrial strategies.

Chapter 3 brings together some of the key themes that emerge from the interviews, and builds on these, outlining the parameters of the debate and highlighting some of the key questions for Norway and for its European and international partners. The Annex contains 15 expert perspectives, covering these themes in greater detail and from different viewpoints. The paper concludes with a summary of the opportunities and challenges identified, and a series of high-level recommendations for key Norwegian stakeholders.