Market disruption

The New Producers Group launched the Fostering Resilience in Crisis meeting series in a chaotic context. In March 2020, an oil price war between Russia and Saudi Arabia flooded the market with crude at a time when the COVID-19 pandemic caused demand to collapse. Some fundamentals were already in play: oil markets were oversupplied and stocks were at a historic high when demand plunged. In March, global oil supply outstripped demand by an average of nearly 6 million barrels per day (b/d) in the first quarter of 2020, resulting in an accumulated implied storage build-up of 2 billion barrels in 2020. The situation worsened when airlines grounded their fleets and governments around the world imposed lockdowns and factory closures. These fundamentals precipitated a decline in oil price that reached a negative of -$37/b WTI on 19 April for delivery the following month.

Against this dire backdrop, 58 per cent of the governments and national oil companies (NOCs) that participated in the New Producers Group meeting on 30 March expected the price of Brent to recover above $30/b by the end of 2020. But significantly, half of those surveyed also believed that global peak demand for oil had been reached.

The initial optimism of the emerging producers now appears unwarranted. The second quarter of 2020 witnessed the greatest ever fall in global oil demand, down 16.4 million b/d year-on-year, and the largest reduction in production volumes in world oil history, by 14 million b/d year-on-year. Economic forecasts in March pointed to a global GDP drop of 2.8 per cent for 2020, an estimate that seemed high at the time in contrast to the 1.7 per cent drop that followed the financial crisis of 2008–09. But forecasts in June predicted a much higher 5.2 per cent decline in global GDP for 2020, the most severe economic downturn since the Second World War. In addition, the IMF expects economic recovery to be more gradual than previously forecast.

There remains a great deal of uncertainty around the duration of the crisis with respect to health (globally and locally) and economic impacts (globally, locally and by sector). ‘Black swans’, low probability events that have the power to effect significant disruption, haunt government planners. As Pedro Gomez from the World Economic Forum put it during a New Producers Group meeting in April, ‘we are simply in the dark. And when you are in the dark all the swans are black.’

Impact on emerging producers

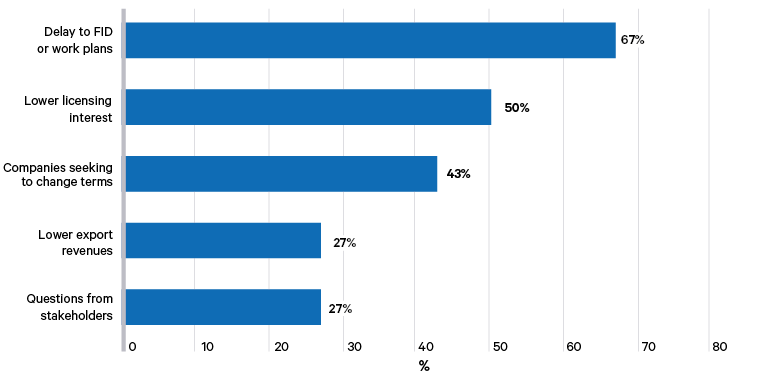

With the fall in demand and reduced availability of finance, the crisis was expected to lead to delays in determining the commerciality of projects, shut-ins of higher cost projects, recourse to force majeure by suppliers and operators, delays to work plans, and contractor and service company bankruptcies. Such impacts were felt as early as March. While established producers were first impacted through the drop in export revenues, according to a New Producers Group survey, emerging producers in the pre-production phase were also affected through delays to final investment decisions (FID) and work plans, reduced interest in petroleum licences, and companies seeking to change agreement terms. Lower sector revenues diminished the budgets of several governments and NOCs and resulted in concerned stakeholders and citizens asking what the impact of the pandemic meant for the future of their country and its petroleum sector.