More fundamentally, it is important to distinguish between the different types of measures that have been implemented by governments. These measures can be split into two broad categories:

- Measures to directly support aggregate demand, through either tax cuts or increased spending, including on job support programmes; and

- Measures to provide financial assistance to companies, including through loans, guarantees or equity stakes.

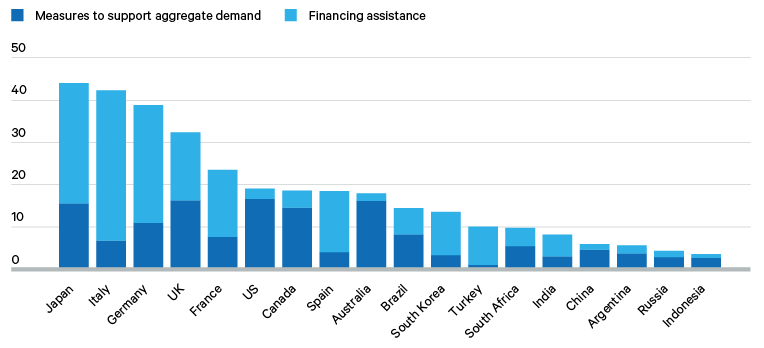

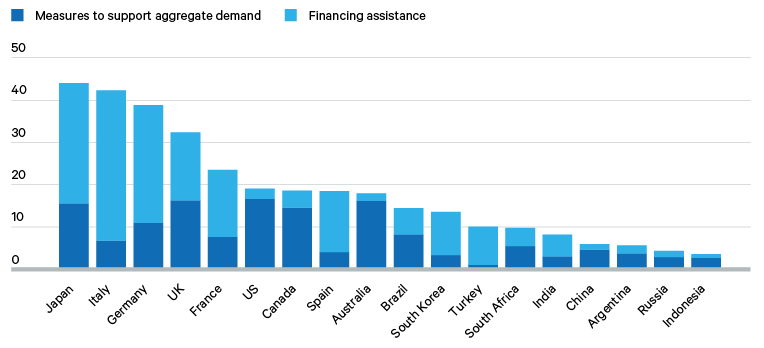

Figure 1 also breaks down the support packages in major economies according to these two categories. One point that stands out is that, while the overall size of support has differed across countries, so too has the balance between the two types of measures.

In some countries, including the US and Canada, measures to support aggregate demand have constituted the largest share of support packages. In others, such as Italy and Germany, there has been greater emphasis on providing financial assistance to companies.

What’s more, measures have been designed and implemented in different ways in different countries. This is particularly true of labour market policies. In Europe, there has been a much greater focus on protecting jobs through government-sponsored furlough or short-working schemes. The details vary, but in general these involve governments subsidizing the wages of workers for a period, thus keeping them on company payrolls and tied to jobs. This has the benefit of preserving job-specific skills among employees and, in so far as it helps keep otherwise viable firms afloat, avoids bankruptcies and deadweight costs. It also maintains a connection between workers and firms so that when demand does return, companies can ramp production back up much more quickly.

In contrast, the US support package has focused less on protecting jobs and more on helping individuals. Unemployment insurance coverage has been expanded, with payments enhanced by $600 a week between April and July 2020, and by $300 a week for three months from December 2020. Stimulus cheques worth $1,200 have also been sent to all households with annual incomes below $75,000, with another round worth $600 sent in December. At the time of writing, a third batch of cheques – perhaps worth up to $1,400 per recipient – is under discussion.

Financial assistance to companies has also come in various forms. Governments have reduced business taxes or delayed deadlines for their payment. There has also been support through equity and debt finance. The former has been on a relatively small scale, generally confined to equity injections by governments into companies deemed ‘strategically important’. Debt finance, in contrast, has played a much larger role. It has included direct and guaranteed lending by governments to private companies. These measures have helped keep afloat firms that have been hit hard by recession but otherwise have a viable post-COVID-19 future.

Yet the understandable push to provide a lifeline in the depths of a crisis means that debt financing has necessarily been a blunt instrument. It is likely that, in some instances, public funds will have been used to prolong the life of unviable firms, or will have inadvertently created ‘zombie’ companies that act as a drag on future investment and growth. Such schemes may have also been a target for fraudsters.

The nature of government-backed loans means that it is impossible to say at the time of their disbursement how much they will ultimately cost the exchequer. If the loans are repaid in full, then the ultimate fiscal costs will be negligible. In contrast, if companies fail to repay the loans, then a fiscal cost will crystallize – though in practice the banks that issue the loans may come under pressure to absorb some of the losses. The light blue bars in Figure 1 therefore represent the upper bound of the anticipated ultimate costs to governments. In practice, the final costs are likely to be much lower.