The economic shock caused by lockdown measures taken in key economies to contain the spread of COVID-19 was of unprecedented magnitude, but a financial crisis was averted in nearly all countries. This owed much to the significant risk-reduction measures adopted by banks in most countries following the last global financial crisis, and to the prompt reuse and scaling up of large parts of the policy playbook from that period. This included, in particular, balance sheet expansions by major central banks (on a much more massive scale than in 2008–09), the renewal of swap lines between the US Federal Reserve and major central banks (including, as in 2008, a handful of emerging-market central banks), and increases in IMF emergency relief resources and lending limits.

The economic shock caused by lockdown measures taken in key economies to contain the spread of COVID-19 was of unprecedented magnitude, but a financial crisis was averted in nearly all countries.

There were also important policy innovations. The first set came from the Fed, with its decision to extend its quantitative easing (QE) programme of asset purchases to include US investment-grade and ‘fallen angel’ corporate bonds. By compressing spreads on this asset class, this move had enormously positive spillover effects: first for US high-yield bonds, and soon after for emerging-market dollar-denominated bonds and eventually local-currency ones too. Through new ‘repo’ lines, the Fed offered foreign central banks the opportunity to obtain US dollars via repurchase agreements on securities issued by the US Treasury; this tool, though ultimately little used, helped relieve fears of massive liquidations of US Treasuries. Together, the above measures significantly alleviated investor risk aversion and fears of a dollar liquidity shortage. This helped to contain upward pressures on the dollar, and in turn eased global financial conditions.

The second innovation in 2020 was that more than a dozen emerging-market central banks instituted domestic QE programmes of their own. This allowed the large increases in bond issuance from governments in those countries to be absorbed by markets without a large increase in borrowing costs, and hence without causing private sector borrowers to be crowded out. Remarkably, what many might regard as a worrying step towards ‘fiscal dominance’ – in which monetary policy becomes guided not by the inflation outlook but by the needs of fiscal policy, and which could herald a future jump in inflation – did not lead to meaningful currency depreciation.

The third innovation was the provision of liquidity to the poorest countries, in the form of temporary relief on debt service payments via the G20-sponsored DSSI. Under this initiative, 77 low-income countries were eligible for a postponement of debt service obligations falling due between May and December 2020. As of the G20 summit in November 2020, 46 countries had availed themselves of the opportunity to delay repayments to official creditors, accounting for $5.7 billion in relief. However, only one of the eligible countries had also requested debt service deferral from private sector creditors (this was, strictly, part of a broader negotiation rather than a DSSI-specific request). Fiscal monitoring by international organizations indicates that DSSI participant countries are undertaking substantial COVID-19-related spending even as they face major revenue shortfalls.

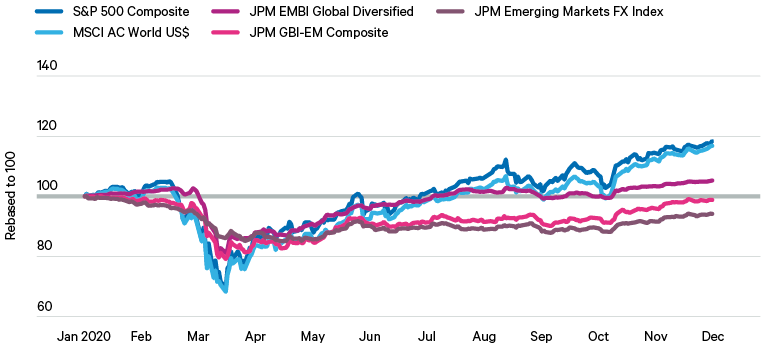

Assessments of this set of policy responses during the first phase of the crisis have been overwhelmingly positive, the consensus being that the measures outlined above have contributed both to a ‘V-shaped’ global recovery in market prices and, to a lesser degree, to the more uneven and incomplete recovery in the real economy.