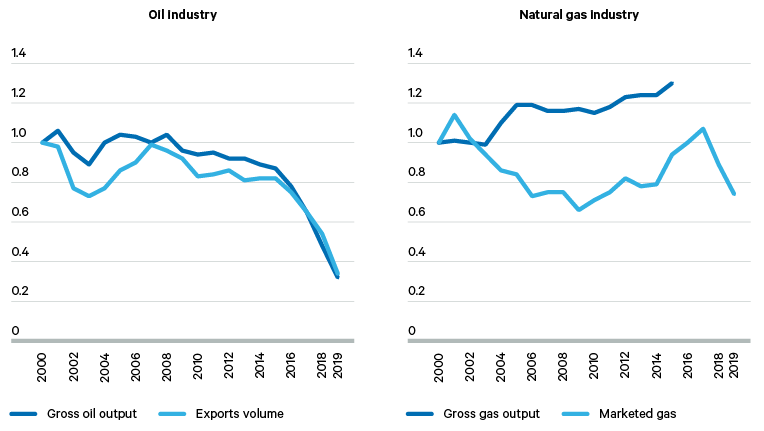

The natural gas industry faces severe constraints stemming from poor infrastructure and low domestic prices that undermine the economics of production. According to the latest available official figures, gross natural gas production grew by 25 per cent between 2000 and 2015 (see Figure 1). But, at the same time, actual supply to the domestic market (at heavily subsidized prices) fell throughout most of this period. There was also a fourfold increase in the volume of natural gas burned (flared) or released into the atmosphere (vented). According to World Bank estimates that use satellite data, Venezuela produced the sixth-largest volume of flared natural gas in 2020 – and the second highest intensity of gas flared per barrel of oil produced.

According to World Bank estimates that use satellite data, Venezuela produced the sixth-largest volume of flared natural gas in 2020.

Venezuela’s official oil reserves exceeded 300 billion barrels at the end of 2019. Most of this consists of extra-heavy oil in the Orinoco Oil Belt, which needs additional infrastructure and specialized refineries to exploit. By one estimate, Venezuela only has 48 billion barrels of recoverable oil resources. The country also has significant natural gas reserves: officially these stood at 6.3 trillion cubic meters at the end of 2019, the eighth largest in the world. But most of these resources are associated gas from oil fields, meaning that they can only be produced along with oil. The remaining non-associated gas reserves – which can be produced independently – come from offshore fields in which PDVSA has virtually no experience.

Several analysts have highlighted various elements in Venezuela’s oil and gas sector that curtail the potential for a recovery of the industry. According to the Fraser Institute’s Global Petroleum Survey, over the last decade, Venezuela has often been the country that ranks lowest for investment opportunities in the oil sector, with significant barriers to investments from overseas. This paper focuses on three basic areas that contribute to these investment barriers: institutional frameworks, legal and contractual arrangements, and fiscal regimes.

Institutional frameworks

- Poor sector governance and concentration of decisions in PDVSA: The 2001 Hydrocarbons Law kept the policymaking and regulation functions under the Ministry of Petroleum. The 1999 Gaseous Hydrocarbons Law created a natural gas regulator, but one with little authority in exploration and production projects. From 2004, the minister of petroleum and the president of PDVSA have often been the same person, and in practice the three governance roles – policymaking, regulation and operation – have been merged. This concentrated most operating decisions across the sector in PDVSA, leading to inefficiency, delays in payments to contractors, overspending, corruption allegations and cash flow management issues as PDVSA handled the sales proceeds for most of the joint ventures in the sector.

- Loss of PDVSA’s autonomy: PDVSA deviated from its core business operations and focused resources and investments on the political objectives of the government and the ruling party, including national debt commitments and foreign energy agreements. Political influence in PDVSA led to a purge of technical staff that the company needed to manage the complex and mature oil fields. New non-commercial subsidiaries frequently participated in the implementation of government social policies, which stretched resources.

Legal and contractual arrangements

- Rigid contractual regime: Investors in oil projects are currently required by law to form joint ventures with PDVSA as the majority shareholder, which increases the state’s fiscal burden to fund investments and the risks it assumes. This requirement contrasts with the different types of oil fields in the country. The Gaseous Hydrocarbons Law allows non-associated natural gas projects to use more traditional licences in which private companies can have full ownership and directly manage operations. But only four of the 19 licences awarded since 1999 reached the commercial production stage.

- Discretionary allocation of production rights: The government has the legal authority to assign oil and gas fields to investors without any competitive process. Almost all existing oil projects were awarded through direct negotiation between the government and international investors. The government awarded most natural gas licences through competitive bidding, but it has not auctioned new areas since 2005.

- Lack of investor protection mechanisms during disputes: The current Hydrocarbons Law forbids international arbitration to resolve investment disputes, which was a key enabler for investors during the 1990s. The government also denounced and left the World Bank International Centre for Settlement of Investment Disputes (ICSID) convention in 2012 and it has removed the investor protection mechanisms from several bilateral investment treaties.

Fiscal regime

- The substantial increase in government proceeds due to rising taxes: The fiscal terms for oil include a 30 per cent royalty, an additional 3.33 per cent extraction tax and a 50 per cent corporate tax. Oil producers must also pay a windfall profits tax based on the difference between the budgeted annual oil price and observed market prices, along with additional tax contributions. There is also a further alternative minimum tax (or ‘shadow tax’) that guarantees that the government will receive at least 50 per cent of the value of the oil extracted – even if investors are losing money. The high amount owed to the government for any project constrains the cash flow available. While non-associated natural gas projects have a much more benign fiscal regime with a lower royalty (20 per cent) and corporate income tax (34 per cent), they have struggled to collect enough revenues due to subsidized gas prices and delays in payments from PDVSA.

- Fiscal distortions and disincentives to invest and produce: A recent study found that Venezuela’s high royalty rates and taxes generated distortions reducing incentives to invest in upstream activities, raise output and explore for new reserves. As a whole, the oil fiscal regime seriously discourages investments in the country.

Venezuela’s policymakers understand that reversing the recent damage to the oil and gas sector requires massive investments and reforms capable of boosting the country’s reputation for contractual reliability. The PDVSA’s Ad Hoc Board (appointed by the National Assembly in 2019) aims to mobilize between $78 billion and $120 billion in capital investments to increase oil output by 2.2–2.5 million b/d within eight years.

Beyond technical and operational plans, there is significant uncertainty on the path to reform. Venezuela is going through a deep political crisis in which Nicolás Maduro still controls the government even if most countries in the continent do not recognize him as the rightful president. Successful reforms can only succeed with a political consensus that brings credibility and stability. While this is still a major impediment, an oil and gas reform agenda must also address the following factors:

- The massive investments needed contrast with Venezuela’s financial difficulties. The country is already in financial default and has few external assets to repay its colossal debts – which last year reached 278 per cent of its GDP. Most available fiscal resources are needed to stem the impact of the severe humanitarian crisis in the country and to support future economic recovery programmes. Further deterioration of fields and physical infrastructure may raise the investments that are required to recover activities across the oil and gas industry.

- Venezuela has an existing base of international investors. Incumbent companies – with a foothold in the country and knowledge of their asset potential and of the current operational risks – focus on reducing costs and optimizing current operations. They may be open to possible expansions under improved fiscal and operational conditions, along with sound economic policies like flexible exchange rates.

- New international investors may require more detailed assessments of risks. New entrants may look for flexible contracts with attractive fiscal terms, the ability to lock in reserves and transparent infrastructure and oil well information. Clear governance rules and provisions for accessing infrastructure would also support the interest of investors. Venezuela’s very negative history of expropriation and weak institutions will augment the need for protection of investors’ rights, including access to international arbitration, fiscal stability clauses and dispute settlement mechanisms. Overall, the oil and gas sector needs strong independent institutions that can administer different geographical areas and negotiate operating conditions, while being flexible regarding contractual terms for the different types of projects and risk profiles.

- Venezuela competes with other oil and gas producers. This is especially true in an energy sector in transition where reaching peak oil demand is a very real possibility and existing suppliers compete for market share. Countries like Brazil, Colombia and Mexico – among others in the region – have already built a legal and institutional framework that attracts FDI in oil and gas projects. The economic impact of COVID-19 has increased calls for governments in the region to improve the fiscal and contractual terms for investors in order to boost economic growth.

- The presence of political allies of Nicolás Maduro could affect the scope of reforms needed. Both civilian and military groups supporting the Maduro government have acquired oil and gas assets in the country but do not necessarily have the required technology or resources to develop some of these fields. They may be concerned about potential losses as their participation in the oil and gas industry was not approved by the National Assembly and they cannot compete with technically sound firms in a competitive process. International political allies of the Maduro regime, such as China and Russia, may also act to protect their oil and gas projects in the country, whether legally or illegally acquired.

Overall, policymakers face a significant challenge aligning the interests of all these groups towards a long-term and sustainable reform process – in reality, the need for political compromise may trump the need for major changes.