| |

Venezuela

|

Canada (Alberta)

|

Mexico

|

Brazil

|

Nigeria

|

Iraq

|

|

Oil reserves (bn barrels)

|

303.8

|

167.8

|

7.7

|

12.7

|

37.5

|

145.0

|

|

Oil output million b/d

|

0.92

|

5.65

|

1.92

|

2.88

|

2.11

|

4.78

|

|

Independent regulator

|

No

|

AER

|

CNH

|

ANP

|

No

|

No

|

|

National oil company

|

PDVSA

|

No

|

PEMEX

|

Petrobras

|

NNPC

|

No*

|

|

Contractual models

|

Joint ventures,

concessions (natural gas)

|

Concessions

|

Concessions, production-sharing contracts, service contracts

|

Concessions, production-sharing contracts, transfer of rights

|

Joint ventures, concessions, production-sharing contracts, risk-sharing

|

Service contracts

|

|

Fiscal regime

|

Royalties, taxes

|

Royalties, taxes

|

Profit oil, royalties, taxes

|

Profit oil, royalties, taxes

|

Profit oil, royalties, taxes

|

Fees, income tax

|

|

Reference oil (API gravity)

|

Merey

(15.9º)

|

WCS

(20.5º)

|

Maya

(20.5º)

|

22–31 API

|

Bonny Light

(33º)

|

Basrah Light

(30º)

|

Sources: BP (2020), Statistical Review of World Energy; EY (2020), Oil and Gas Tax Guide 2019;

Wiley (2020), ‘OPEC and non OPEC oil sales prices’, Oil and Energy Trends Annual Statistical Review, 21(1): pp. 62–66.

Note: * Iraq does not have a national oil company directly comparable to those in other countries. Instead, there are multiple companies controlled by the Ministry of Oil.

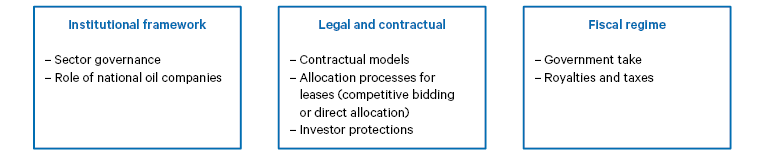

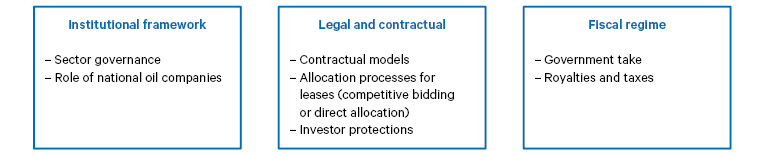

Institutional framework

Brazil’s government reformed its domestic oil industry in 1997 by eliminating the traditional monopoly that the NOC, Petrobras, had over the entire hydrocarbons industry. This decision was part of a larger macroeconomic reform aiming to attract private investment to new offshore areas. Brazil strengthened its institutions by creating the independent National Agency of Petroleum, Natural Gas and Biofuels (ANP) that took over regulation and administration. Policymaking remains under the Ministry of Mines and Energy with the support of the National Energy Policy Council (CNPE) while Petrobras and private investors operate the wells and production.

Legal and contractual arrangements

Brazil initially used concessions awarded through competitive auctions. In 2010, the government created a framework for new areas in the pre-salt layer, introducing production-sharing contracts (PSCs) and initially mandating that Petrobras should have a minimum share of production and act as operator. In addition, for certain pre-salt blocks the government transferred the rights to Petrobras to produce 5 billion barrels of oil in exchange for new company stocks. These arrangements were intended to capture a higher share of revenues and strengthen government control. Since 1999, Brazil has conducted 26 bidding rounds for exploration projects, production fields and pre-salt areas. In 2019, the ANP also implemented the open acreage bids process that continuously offers oil and gas fields that have been returned by investors, without requiring a specific bidding round. Despite successive auctions, Petrobras still controls most oil and gas production. Since 2017, it no longer has an obligation to act as the main operator of projects in pre-salt areas, a change intended to improve conditions for international investors. Despite these changes, two pre-salt auctions in 2019 failed to attract any large international company, possibly due to high entry barriers for investors and the focus of major oil companies on controlling capital spending. Brazil has progressively deregulated other segments like downstream operations and natural gas, with the aim of fostering investments in network infrastructure for domestic fuels and gas consumption.

Brazil’s government reformed its domestic oil industry in 1997 by eliminating the traditional monopoly that the NOC, Petrobras, had over the entire hydrocarbons industry.

Fiscal regime

Traditional concessions are subject to a signature bonus, a flat 10 per cent royalty rate for the government (which can be reduced to 5 per cent) and a special participation tax on profits that uses progressive rates depending on the field’s location, lifetime and production. This scheme is designed to capture additional rents in case of highly profitable findings from large resources and production potential. Pre-salt PSCs are also subject to signature bonuses and a 15 per cent royalty. Investors in PSCs can recover the cost incurred during the development of the project (cost oil), with the remaining profits split between companies and government based on pre-agreed rules (profit oil).

Mexico

Institutional framework

As part of a comprehensive energy reform process that started in 2013, Mexico opened all oil and gas activities to private competition and separated the industry’s governance roles. The National Hydrocarbons Commission (CNH) was restructured to act as an independent oil and gas upstream regulator and to allocate exploration and production contracts. The Secretariat of Energy defines the broad energy policies and Petróleos Mexicanos (PEMEX) remains a state-owned NOC but one operating more autonomously and with more accountability. In addition, the role of the Regulatory Energy Commission (CRE) includes regulating and granting permits for storing, transporting and distributing oil and gas products. The National Centre for Control of Natural Gas (CENAGAS) was created in 2014 to operate the country’s natural gas pipelines, while the state utility Federal Electricity Commission (CFE) manages its own pipeline network. However, the experience since President Andrés Manuel López Obrador took office in 2018 suggests that policies are oriented towards greater state involvement in the oil and gas sector and limiting the autonomy of some of its institutions.

Legal and contractual arrangements

The CNH can use several upstream contracts, including licences, profit-sharing contracts, PSCs and service contracts. PEMEX can also subcontract some of its areas to private partners. These contracts are allocated through a competitive process with multiple criteria, which may include royalties, profit shares and investment commitments, depending on the location of the resources. The government negotiated with PEMEX on which areas the company would keep and which would be offered to private investors, a process known as ‘Round Zero’. Contracts also include fiscal stabilization clauses to protect investors against arbitrary contractual changes. These clauses allow the state to modify fiscal terms only if they also apply to the overall economy. There has been similar deregulation in the midstream segment with several rounds of auctions for infrastructure projects – noticeably in the retail market for gasoline, which has become more flexible and moved towards market pricing. President López Obrador has tried to reverse elements of some of these reforms by halting auctions and strengthening the dominant position of the CFE (more recently, through a proposed reform of the Electricity Law) and PEMEX. But, despite the policy changes, the legal regime created by the reforms remains and existing contracts have, so far, been respected – though again this may change given recent government signals.

Fiscal regime

Fiscal terms include a combination of income taxes, a variable royalty (as a function of oil and/or gas prices), surface taxes and additional royalties or profit-sharing mechanisms that depend on the type of contract and resource field. They also include adjustment mechanisms to increase government payouts as the project becomes more profitable, either using R factors (based on a ratio of cumulative revenues over cumulative costs) or internal rates of return calculations.

Iraq

Institutional framework

Iraq’s government directly manages most operations in the oil and gas industry. The importance of oil in a country with such a large resource endowment and high rent dependence cannot be overstated. Policy, strategic and operating decisions are centralized in the Ministry of Oil. There is no independent regulator or traditional NOC. Instead, the ministry owns several companies controlling different aspects of the oil and gas value chain, including the State Oil Marketing Organization, which controls oil exports. Legal reforms aiming for a new institutional framework and recreating Iraq’s NOC, which was eliminated in 1987, have repeatedly failed due to protracted political disputes.

Legal and contractual arrangements

The Ministry of Oil assigns technical service contracts (TSCs) under which companies operate fields in exchange for a fee per barrel capped to a maximum amount agreed during a bidding process. The ministry has conducted five bidding rounds since 2009, with the last one taking place in 2018. In the semi-autonomous Kurdistan Region, the regional government offers PSCs for oilfields with the idea of also using these contracts for gas projects. Service contracts allow the state to maintain ownership of the oil or gas extracted (in line with constitutional requirements) from well-known fields with large reserves, little geological risks and very low production costs.

Fiscal regime

Under the TSCs, contractors are reimbursed for capital investments and operation costs, plus a rate of return, and the remuneration fee changes according to incremental production (that is, production above pre-contract levels), in which case the price risk is assumed mostly by the government. It has been estimated that the TSCs become too expensive for the government when oil prices fall below $40–$45 per barrel as lower profits limit the ability to reimburse costs. Some of these contracts have been re-negotiated in previous oil crises, introducing an element of uncertainty for development plans. Despite these problems, Iraq was able to build capacity after the 2003 US invasion and, more recently, deal with the threats coming from Islamic State (ISIS).

Nigeria

Institutional framework

The Department of Petroleum Resources is the formal oil and gas regulator, but the Nigerian National Petroleum Corporation (NNPC) acts as a quasi-regulator as it is the primary actor dealing with investors and the main source of revenues for the government. With most of the sector’s decisions motivated by politics and with little independent oversight, there is ample room for opacity, inefficiency and corruption. Institutional reforms to modernize the sector have been proposed for several years but have failed to win political support. Currently, a Petroleum Industry Bill is being discussed in parliament. It proposes the creation of separate regulators for upstream and downstream activities.

Legal and contractual arrangements

International investors have traditionally acted as minority partners in joint ventures with the NNPC, although with effective control over operations and budgets. Most recent activity has focused on offshore fields in response to political violence, sabotage and militant groups in the Niger Delta. These projects use PSCs that forego cash calls to the NNPC (as in traditional joint ventures), reducing financial pressure on the government and risks to investors. The government has ample authority to assign blocks and projects to investors, and there has not been an open bidding round since 2003. Private investors can also participate in refining and downstream products but there are few signs of interest on their part so far.

Fiscal regime

Nigeria uses a combination of royalties, petroleum profit taxes (income tax) and production splits for the PSCs. Royalty rates are indexed to the price of oil and vary according to the type of oil field, with lower rates for deep-water projects. The rate of the petroleum profit tax depends on the type of contract used (production sharing or joint venture). The Petroleum Industry Bill proposes to replace the petroleum profit tax with a lower-rate Nigerian hydrocarbons tax, with corporate income tax collected separately. Analysts view these changes as leading to aggressive reductions in government take, although the final impact is still unclear as companies have expressed concerns about fewer tax-deductible costs.

Alberta, Canada

Institutional framework

Canada has not had a NOC since the privatization of PetroCanada in the early 1990s. Most of the country’s resources and production are concentrated in the province of Alberta, and its heavy crude competes with the most abundant grades in Venezuela. Alberta’s Ministry of Energy defines the province’s oil and gas policies, and it grants the rights to exploit fields. The Alberta Energy Regulator (AER) is under the provincial government’s control. It has broad oversight over oil and gas operations to ensure their compliance with laws, as well as the capacity to review and decide on proposed energy developments.

Legal and contractual arrangements

Alberta provincial government owns over 80 per cent of the province’s mineral rights, which can be transferred through lease contracts in transparent and public auctions. Initial project time frames are limited, but they can be extended indefinitely if projects are profitable.

Fiscal regime

Oil and gas projects are subject to royalties (collected by the provincial government) and income tax (collected by the federal government at the same rate as for non-oil activities). Alberta distinguishes oil sand projects from other oil and gas projects. Oil sands are subject to variable royalties over gross revenues during the pre-payout period, ranging between 1 per cent and 9 per cent based on oil prices. After payout, royalties are charged over net revenues with rates between 25 per cent and 40 per cent, also based on oil prices.

Institutional framework considerations

Governments in Brazil and Mexico were able to introduce reforms and build legal stability from political consensus that required constitutional amendments. In both countries, the need for massive investments to develop the sector, and the interests of other sectors in the economy, led to overarching energy reforms in the hydrocarbons and electricity sectors. These reforms also aimed to develop markets that could provide affordable energy for the entire economy. Brazil and Mexico also separated the operational roles from the administration and regulation of the sector by creating agencies with autonomy from the government. Independent regulators do not supplant the government’s role in policymaking; the case of Mexico shows how policies can change the trajectory of, or even reverse, institutional reforms.

In Brazil and Mexico, the need for massive investments to develop the sector, and the interests of other sectors in the economy, led to overarching energy reforms in the hydrocarbons and electricity sectors.

Nigeria had the opposite experience: stalled reform attempts that lack political consensus, which led to uncertainty and delayed investments. The 2008 Petroleum Investment Bill attempted to overhaul an industry dominated by the NNPC, which effectively serves to distribute rents among multiple stakeholders. However, the bill has suffered several setbacks, and a new version is yet to be approved. While Iraq has managed to increase production after the establishment of the post-2003 state, it still struggles with conflicts around the distribution of resources among regions, institutional competences and authority. The oil and gas industry still relies on an ad hoc structure that, even if it successfully raised output, could create additional risks to investors.

The cases of these five countries demonstrate different NOC models, although there is no clear trend in how these differences impact investor decisions. Mexico and Nigeria have more traditional state-owned NOCs and the government has a greater role in shaping their finances – in Mexico, most recently, with a clear intention of increasing its involvement in oil and gas operations. Brazil seems to have the most autonomous and technically sound NOC in Petrobras, due in part to its partial share listing in Brazil and in the US. The company, however, has still had notorious incidents of corruption. Iraq lacks a traditional NOC and its operating companies act as extensions of the Ministry of Oil. It remains to be seen whether the creation of a NOC could meet the constitutional stipulations enforced by the legal system.

Legal and contractual arrangements

The experiences of the five countries clearly show a trend of granting further flexibility on the type of contracts used for upstream oil and gas activities. Mexico, Nigeria and Brazil allow for different contract models for different types of fields. Following its energy reform, Mexico has used licences mostly for legacy onshore fields and complex deep-water fields, while PSCs are more common in shallow-water fields. Nigeria has traditionally relied on joint ventures with the NNPC, but the financial pressure these placed on the government pushed the country to adopt PSCs for new offshore fields. Conversely, Iraq has mostly relied on TSCs with aggressive fiscal terms and more price risk exposure as its very productive oil fields have resulted in very low costs and high economic rents. Venezuela does not have the same type of fields or resources as Iraq, so this type of contract may not be suitable. Furthermore, Iraq has failed to sign new large oil contracts since 2009, highlighting the need for further reforms in order to continue to attract investors.

The majority of the five countries use open and competitive auctions – the most efficient and transparent mechanism – to allocate oil and gas production rights. Brazil and Alberta have consistently allocated fields to the winners of auctions. Mexico has conducted nine bidding rounds since its 2013 energy reform, although the López Obrador administration halted them soon after taking office in 2018. Iraq has also used competitive bidding to allocate service contracts, with five rounds since 2009. Nigeria is an outlier with most areas directly allocated by the government and no competitive bidding rounds since 2003.

Regarding investor protections, the five countries have used different approaches. Alberta has a strong judicial system and domestic investor protections, and Canada ratified the ICSID convention in 2013. Mexico offers investors a limited international arbitrage option only after the domestic legal system has been exhausted. Brazil has not been a member of the ICSID convention, nor has it ratified bilateral investor treaties incorporating international arbitration. Beyond international arbitration, Mexico offers a fiscal stabilization clause protecting investors from fiscal changes targeted at the oil and gas industry. Some investors in Mexico and Canada’s energy industry could potentially settle investment disputes through mechanisms included in the recent US–Canada–Mexico Agreement, although these have a more limited scope than those in the previous North American Free Trade Agreement. In Iraq, TSCs provide for disputes under the rules of arbitration of the International Chamber of Commerce.

Fiscal regimes

Each country examined has introduced variable fiscal regimes allowing the state to receive a proportionally larger share of profits as they grow. Such progressive tax regimes can, in theory, reduce the risks of future renegotiations – an area in which Venezuela has a poor track record. Progressive taxes can take the form of variable royalty rates as a function of oil and gas prices, as in Mexico, Brazil, Alberta or Nigeria. They also relate to special taxes after extraction reaches specific thresholds indicating highly productive and profitable fields. Fiscal stability clauses, such as those introduced in Mexico that restrict the state’s ability to impose new taxes targeting oil and gas production, and investor protections in the form of international arbitration can also lower investors’ risks.

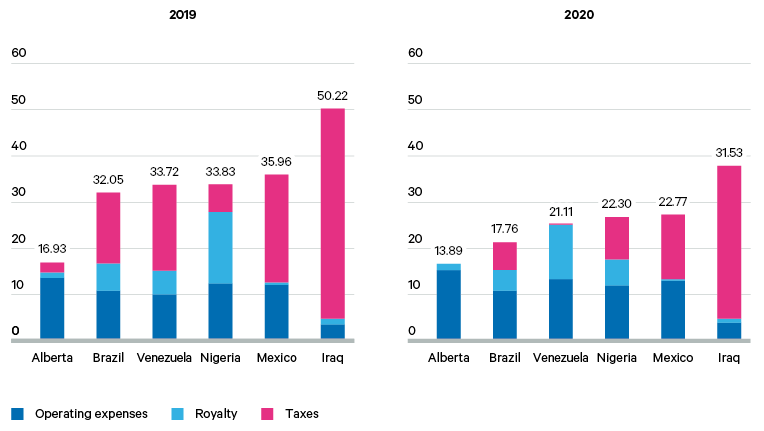

Extraction and transportation costs in Alberta are significantly higher than in the other cases, which explains why contractual and fiscal terms are relatively more flexible there too. Iraq has the lowest oil-production costs, which, along with the fee structure in its service contracts, allows the government to capture a majority of the industry’s profits – although the state also absorbs all the price volatility risk. Without mechanisms such as an oil revenue stabilization fund, this leaves government finances highly exposed to oil price volatility.

Compared to the five countries examined, Venezuela is more reliant on oil royalties. These discourage investments and production, but they can also be more stable and easier to collect than profit-based taxes that can be more volatile to changes in prices. The 2020 fall in oil prices depressed fiscal revenues in all five countries, but profit-based taxes were more sensitive to lower oil prices than royalties. Collectively, their average royalty per oil barrel fell by 29 per cent, while profit-based taxes fell by 69 per cent (Figure 4).