Technology

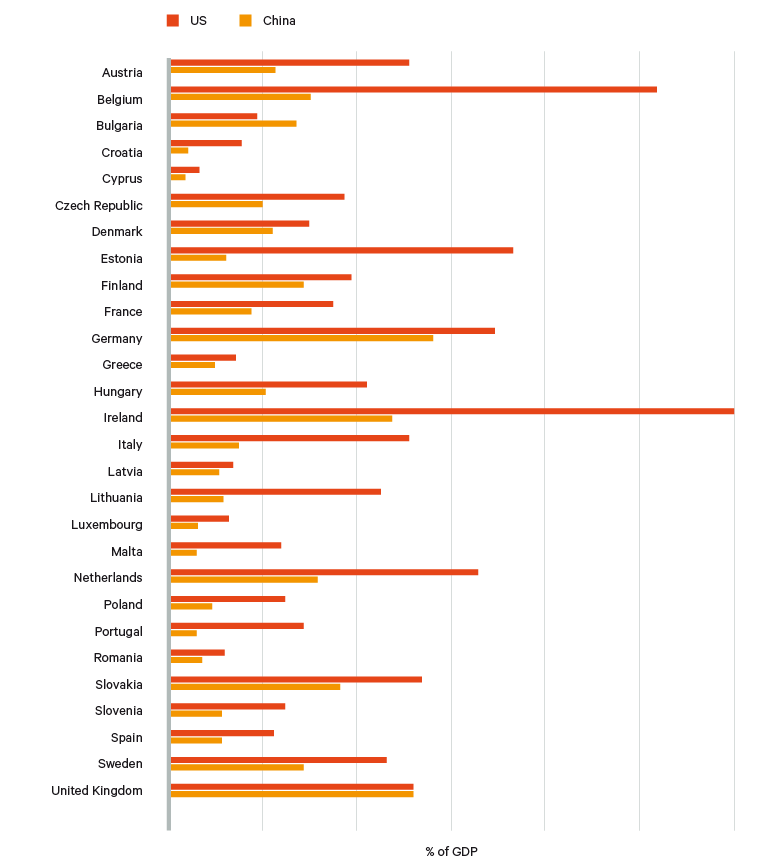

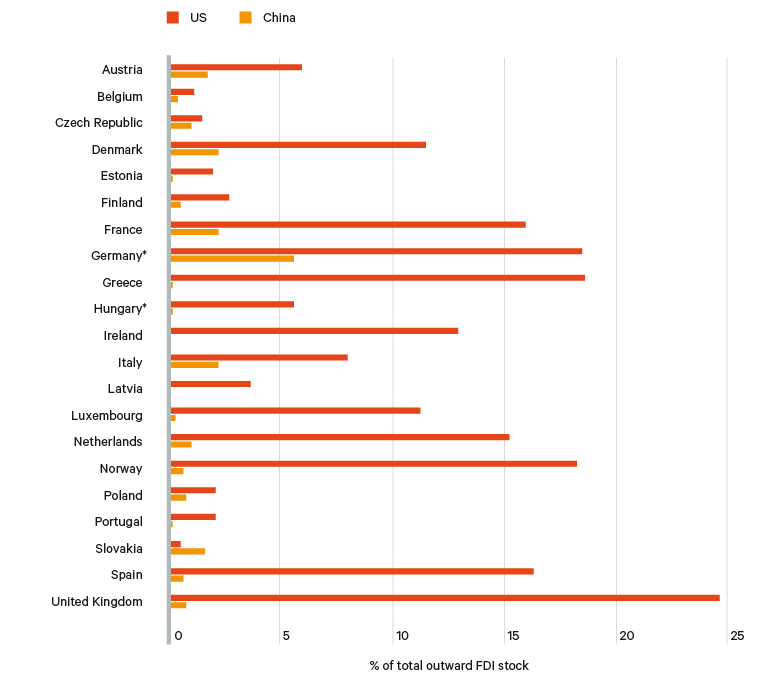

Despite its dependence on imports from China, the European economy is still more reliant on the US. Almost all European countries export significantly more to the US than to China and the economies of Europe and the US are deeply intertwined through extensive investment relations. Western European countries have a long history of deep economic and political integration with the US. Although transatlantic tensions have increased in recent years, and were exacerbated by the Trump administration, the US–EU connection remains close. This stands in sharp contrast with Europe’s relatively new relationship with China, which focuses mainly on trade and for some countries on investment. One of the sectors where this is most visible is in technology.

The European technology market remains dominated by US firms. Large Chinese internet companies have little to no market share, with a few notable exceptions, including the telecoms firm Huawei and the social network TikTok. This is partly due to China playing catch-up but it also reflects fundamentally different views of how the internet should operate. China’s closed, state-controlled model is incompatible with the European vision of an open internet with minimal state interference. Despite transatlantic differences over issues such as the governance of large technology firms, the European vision is significantly further removed from the Chinese authoritarian approach than that of the US.

On the hardware side, the digital economies of Europe and China are more interwoven through global supply chains. For instance, the semiconductor industry is spread throughout the world, with crucial companies based in Europe. However, this is not the case for other technologies, with Europe for instance lagging in artificial intelligence, and the combination of competition and conscious decoupling between the US and China is likely to widen this gap further. In part through diverging standards, there is a chance that the global technology scene will be split between the US and China. If this is the case, it is most likely that Europe will continue to gravitate towards the US.

The elephant in the room

By almost all measures, Germany has a deeper economic relationship with China than any other EU member. The value of German goods exported to the country in 2019 was equal to the combined exports to China of all other EU members, driven by Chinese demand for German capital goods, machinery and cars. This is also a reflection of the size of the German economy and its export dependence. Exports to China were equivalent to 2 per cent of Germany’s GDP and made up 8 per cent of its exports. This was slightly higher than exports to the UK but still below those to the US.

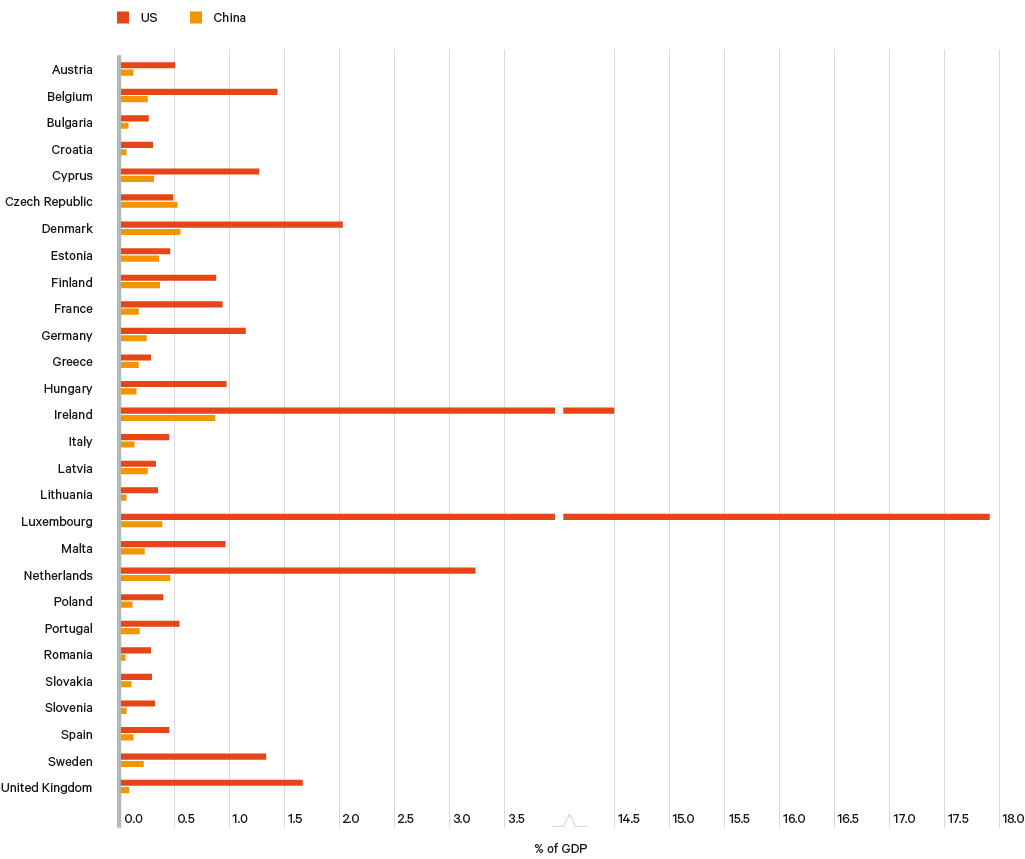

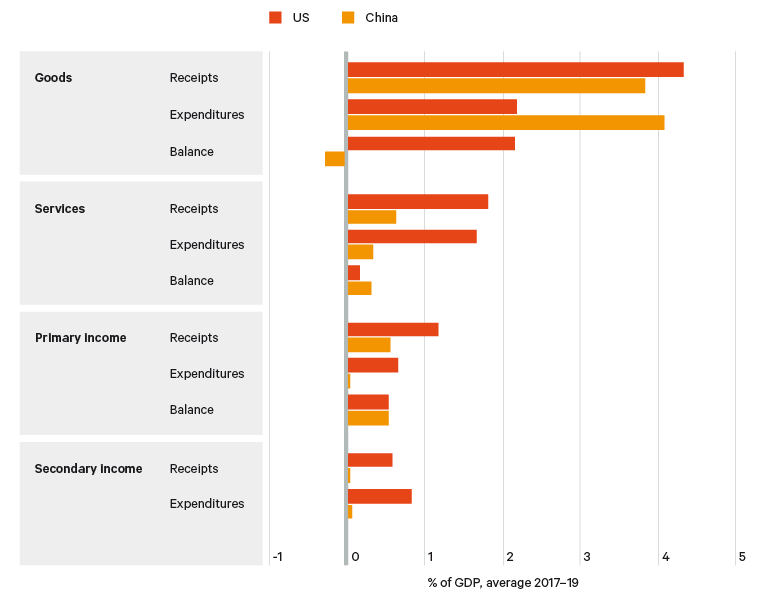

Germany has in recent years run small current-account surpluses with China, resulting from the combination of relatively modest bilateral trade deficits against it and significant income streams arising from investments there. This is also a revealing metric when comparing the economic relations that Germany has with China and with the US as it captures all income flows. As Figure 6 shows, all income flows between Germany and the US, except for goods imports, are significantly larger than those between Germany and China. The German economy remains significantly more integrated with the US economy.

Nevertheless, many large and politically influential German firms are deeply integrated with and exposed to the Chinese economy, influencing the country’s China policy. For instance, China has become the largest market for Volkswagen. This has not meant a significant boost to German exports, though, as the majority of Volkswagen’s sales in China are produced locally. This includes production in the western province of Xinjiang, where the alleged use of forced labour in its supply chain has caused political difficulties for the company. Volkswagen is increasing its exposure to the Chinese market through significant investment in electric mobility production there.