A key driver of the surge in inflation across advanced economies – and the associated ‘cost of living crisis’ – has been a huge jump in energy inflation, which is now running at record highs across Europe.

Let’s start with some basic facts. While services inflation is beginning to increase in several advanced economies, most of the increase in headline inflation over the past year has been driven by consumer goods and energy.

In fact, energy alone has been responsible for over half of the increase in Consumer Price Index (CPI) inflation in advanced economies since the fourth quarter of 2020.

How rising energy bills became a political hot potato

However, while energy inflation has increased in every major economy, the increase has been particularly acute in Europe. Energy is now contributing almost 3 percentage points to annual inflation in the eurozone.

And while energy’s contribution to overall inflation is currently lower in the UK (at just over 1.5 percentage points), it will jump in April when the increase in the cap on household utility bills that was announced by the government last week will come into effect.

In contrast, energy is adding (only!) 2 percentage points to headline inflation in the US. More importantly, its contribution is now starting to fall.

So while energy has been a source of higher inflation in every advanced economy, it is now a particular problem for the eurozone and the UK. This explains why the issue of rising household energy bills has suddenly become a political hot potato for European governments.

The reason why it has become more of a European problem has to do with what’s happening in global energy markets. Different grades of oil trade at different prices, but since oil can be shipped to different markets, prices do not tend to differ substantially between regions.

The same is not true of natural gas. While liquified natural gas (LNG) can be shipped, most gas is transported through fixed pipelines. This means that prices can differ considerably between regions depending on local demand and supply conditions.

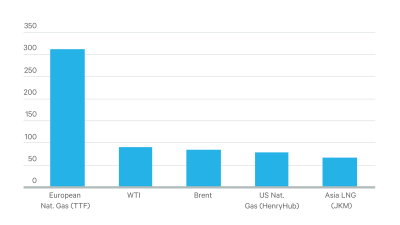

Increases in natural gas prices vary substantially

As Chart 1 shows, while the price of WTI crude (the main US benchmark) and Brent crude (the European benchmark) have both increased by around 70% since the start of last year, increases in natural gas prices have varied substantially.

In Asia and the US, benchmark natural gas prices have increased by 70% and 100% respectively since the start of last year. In Europe, however, they have increased by over 300%.

The reasons are manifold but are mainly to do with supply: stocks are low, and a tendency to source gas on short-term contracts has made it difficult for governments to secure additional supply as demand has surged. In addition, the conflict in Ukraine has threatened European gas supplies and added a considerable premium to market prices. Crucially, natural gas prices tend to be the main determinant of household energy bills.

Chart 1: Increase in Prices of Selected Commodities since 1st January 2021 (%)

The surge in European energy prices has been particularly large.

So what comes next and how should governments and central banks respond? When it comes to inflation, the key point to keep in mind is that it is the rate of change in prices – not the level – that matters.

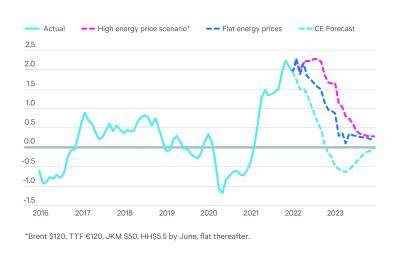

A number of market forecasters expect modest falls in oil and gas prices over the course of this year. But if oil and natural gas prices remain flat at their current elevated level, energy’s contribution to headline inflation will drop back over the course of this year. (See Chart 2.)

And even in a ‘high price’ scenario, in which oil and gas prices increase further, energy’s contribution to overall inflation falls back towards the end of this year.

The key point is that the huge increase in prices in 2021 will gradually drop out of the annual comparison this year, meaning that in the absence of an even larger jump in oil and gas prices in 2022, energy inflation should drop back.

Chart 2: Contribution of Energy to Headline Inflation in Major DMs (%-pts)

Energy inflation will ease even if prices stabilize at current high levels.

Three challenges for policymakers

Inflation shocks caused by energy prices pose three challenges for policymakers. First, there’s not much that monetary policy can do to influence energy prices.

Second, while a rise in energy prices increases inflation in the short term, all other things being equal, the subsequent squeeze on real incomes is disinflationary over the medium term.

Finally, since lower income households spend proportionally more of their income on energy, higher energy prices can have significant distributional consequences.

The squeeze on real incomes – and the disproportionately large hit to lower- and middle-income households – has led to a series of measures by European governments to mitigate the effects of higher energy prices. This has taken different forms.

The UK has announced a rebate on household utility bills; Spain has cut taxes on energy bills and introduced a windfall tax on energy companies; and France has introduced a cap on energy bills until (conveniently) April’s presidential election has passed.

Fiscal measures to cushion the hit to real incomes can be justified if governments believe that the energy shock is temporary, and prices will ultimately drop back. But they can create problems for governments if prices remain elevated.

A permanent increase in energy prices implies a permanent deterioration in the terms of trade of economies that are net energy importers. Someone must ultimately bear this cost.

A stronger case for higher interest rates?

This leaves a difficult choice: should policy support be withdrawn, causing a squeeze on real incomes that hits the poorest hardest, or should it be kept in place indefinitely incurring a permanent fiscal cost and distorting consumer behaviour? More often than not the laws of politics dictate that the can will be kicked down the proverbial road.

Meanwhile, central banks should look through the immediate effects of higher energy prices on inflation and instead focus on the ‘second round’ effects – that is to say the indirect impact they have on activity and inflation further down the line.