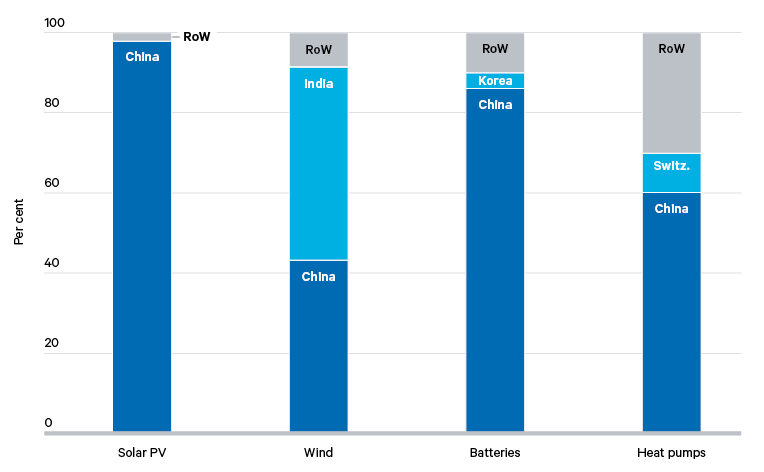

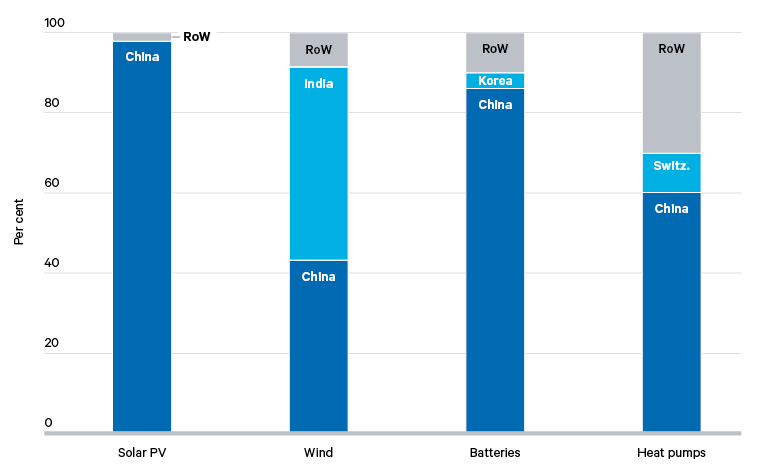

China has firmly established itself as the world’s leading manufacturer of low-carbon technologies. The country’s dominance of these sectors is the result of many factors, including consistent government support, huge economies of scale and intense competition between domestic firms. Today, Chinese low-carbon products are both competitively priced and technologically sophisticated.

During Ursula von der Leyen’s first five-year term (2019–24) as president of the European Commission, the commission made a concerted effort to boost EU manufacturing of low-carbon technology. This drive has continued in von der Leyen’s second term under the banner of a package called the Clean Industrial Deal. The initiative aims to fuse measures to improve economic competitiveness with those to promote decarbonization, and includes plans to support domestic low-carbon technology manufacturing by providing financial guarantees, speeding up the approval of state aid, investing in research and innovation, and boosting demand for EU-made products.

The Clean Industrial Deal builds on progress that is already occurring in some manufacturing sectors. In early 2024, the European Commission judged that the EU was on track to meet 90 per cent of its battery demand through domestic production by 2030 – although the subsequent collapse in late 2024 of Northvolt, a major Swedish battery maker and a symbol of Europe’s green industrial ambition, damaged confidence. Some European companies are also seeking to benefit from Chinese expertise by entering into joint ventures with Chinese firms. For instance, Stellantis, a Dutch-based multinational automotive firm, and CATL, a Chinese battery maker, are collaborating on a lithium iron phosphate (LFP) battery factory in Spain.

Overall, however, there is little chance of the EU becoming self-sufficient in low-carbon technology in the foreseeable future. This was tacitly acknowledged in the EU’s Net Zero Industry Act (NZIA), adopted in 2024, which envisaged the EU producing only 40 per cent of its total demand for low-carbon technologies

by 2030.

As tacitly acknowledged in the Net Zero Industry Act, there is little chance of the EU becoming self-sufficient in low-carbon technology in the foreseeable future.

Moreover, even if this share were to reach 100 per cent, and substantial new capacity to produce intermediary components and process raw inputs were also built, it would not comprehensively reduce the EU’s import dependency for raw materials. The region’s geology condemns it to a heavy reliance on imports of critical minerals, such as lithium for batteries, rare earth elements for wind turbines, and manganese for solar panels. Underlining this limitation, the 2023 European Critical Raw Materials Act set a target for the EU of extracting a mere one-tenth of the bloc’s required supply of critical raw materials from sources within EU borders by the end of the decade.

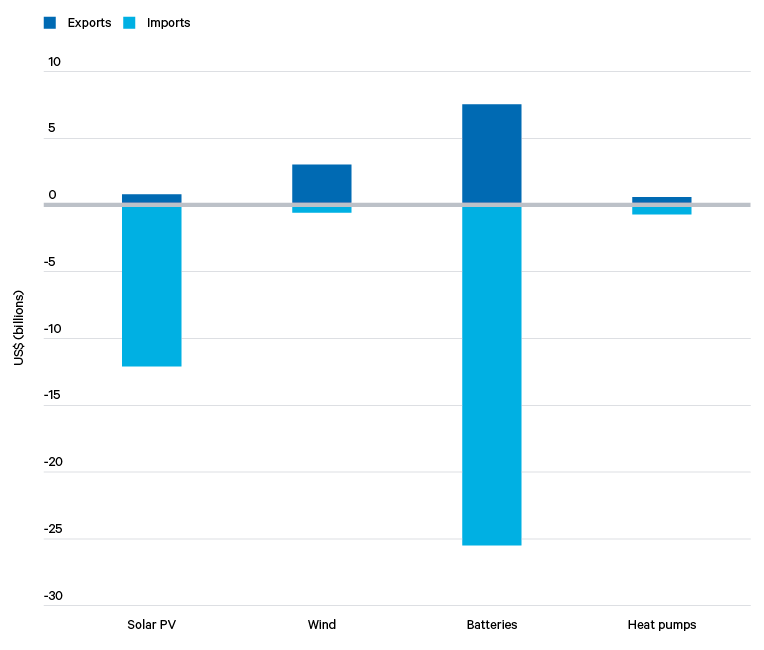

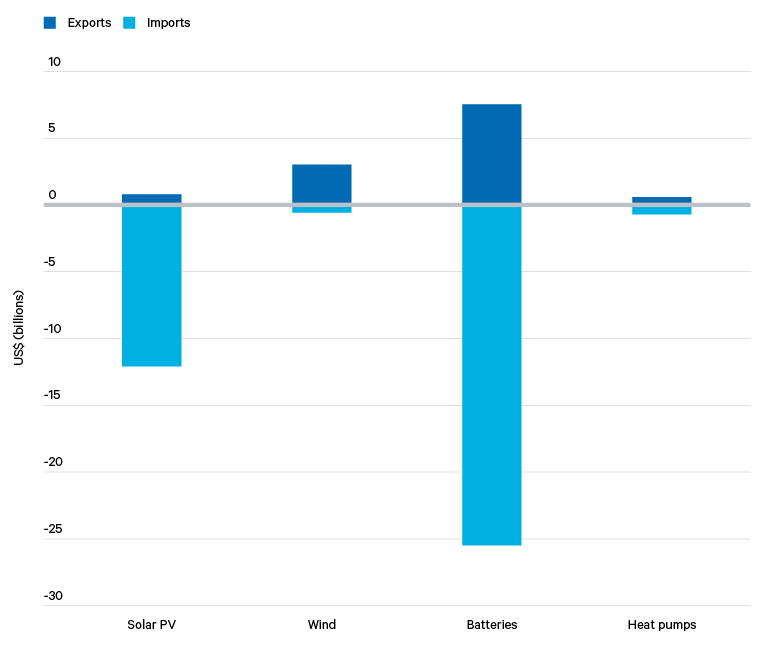

Reserves of these materials are spread across several different countries. Australia, Brazil, Chile, China, the Democratic Republic of the Congo (DRC) and Indonesia all have substantial reserves of different minerals needed for low-carbon technology. China has the largest overall share of known rare earth reserves (40 per cent of the global total), but across the suite of minerals needed for low-carbon technologies it is in refining, rather than natural endowment, that the country is most dominant. In 2024 the country accounted for 78 per cent of the world’s cobalt refining capacity, 91 per cent of refining capacity for rare earth elements used in the production of high-performance magnets, 70 per cent of lithium refining capacity, and 96 per cent of battery-grade graphite refining capacity. A notable exception is nickel refining, in which China, accounting for 31 per cent of global capacity, trails Indonesia (43 per cent).

Beyond security of supply

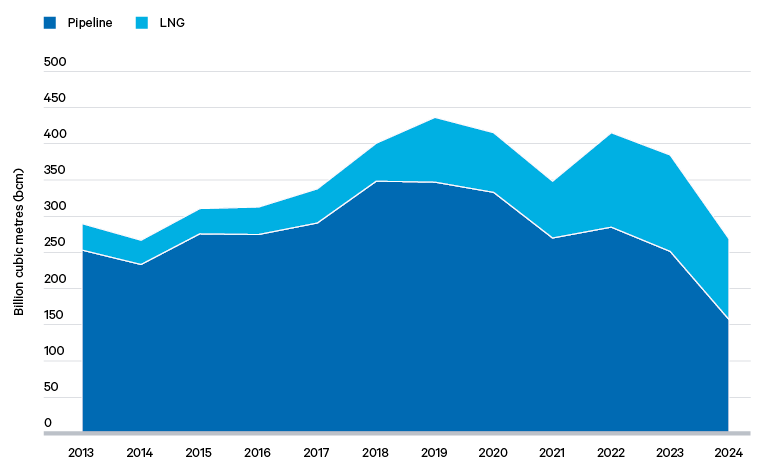

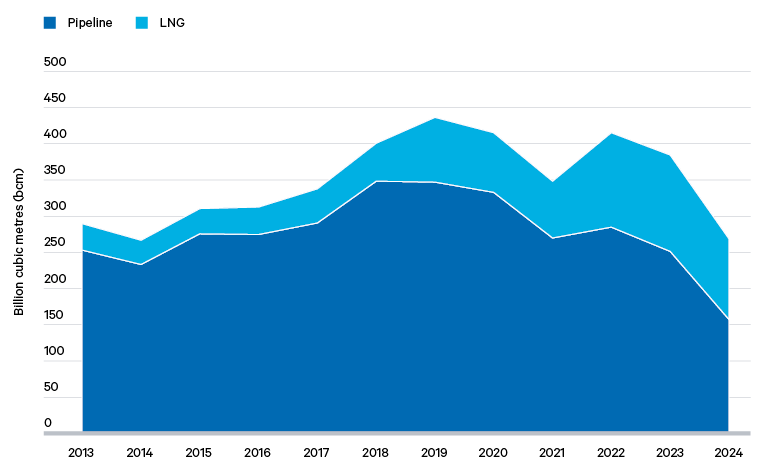

Energy security is commonly associated with security of supply: that is, ensuring a country or region has uninterrupted access to all the energy it needs, at prices it can afford. The importance of this simple imperative became clear in 2022 as pipeline gas flows ceased (or, in some cases, were sharply reduced), and as Europe suffered its worst energy crisis since the 1970s. Yet while the temptation for European policymakers to focus on supply is understandable given the recent trauma of Russia’s weaponization of gas flows, a more expansive understanding of energy security would bring into play additional tools that could improve the EU’s position in the future.

As grids expand and become highly digitized, and as a greater share of energy is consumed in the form of electricity, cybersecurity will become an increasingly vital element of EU energy security.

Rather than being framed principally in terms of supply, energy security should be considered as an equation requiring that supply meets demand. Managing demand is thus as important as securing supply. Insulating homes, making industrial processes more efficient, introducing demand-response technologies into electricity systems – all can contribute to energy security by reducing the total quantity of energy that the EU requires. As EU citizens, businesses and member states demonstrated in the wake of Russia’s full-scale invasion of Ukraine, demand for energy can be reduced if needed. Energy efficiency measures, which enable the same services (e.g. heating, cooking, lighting) to be provided using less energy, have the added benefit of reducing household energy bills. Potentially, this can also help with securing popular and/or political buy-in for the energy transition.

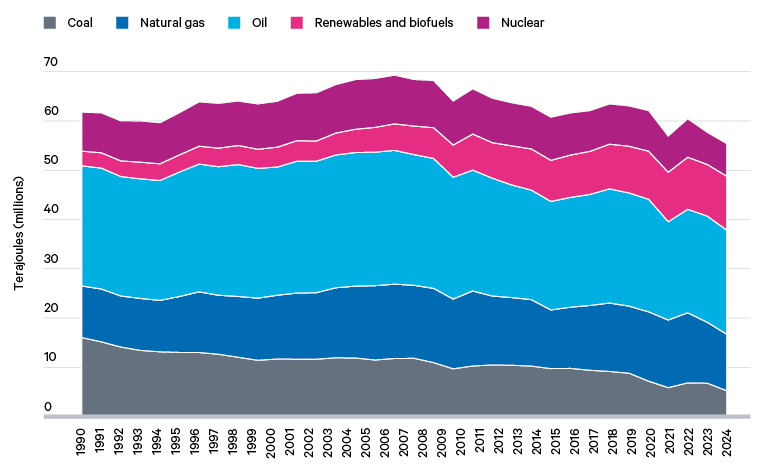

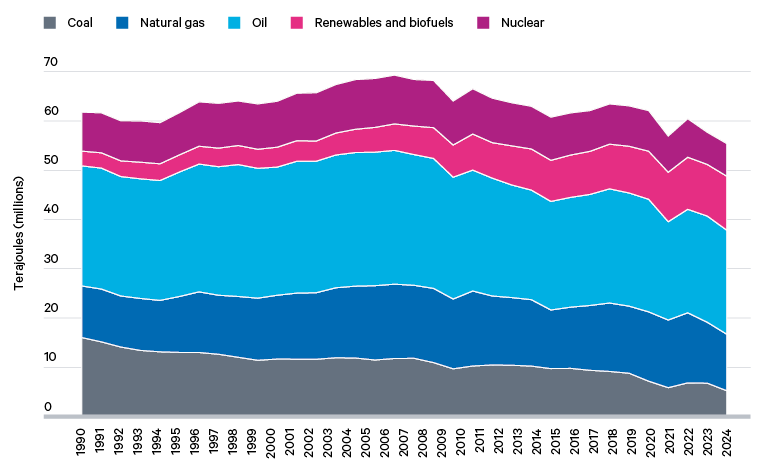

Technology is central to managing the supply–demand equation. The transition to renewables and wider electrification of the economy will increasingly bring into operation systems that integrate sophisticated devices and digital tools. A modest but growing share of the EU’s energy is provided not by the combustion of fossil fuels such as coal and gas, but by technology products that convert renewable, ambient energy into electricity (see Figure 1). These products, which include solar panels and wind turbines, are already contributing to EU energy security by displacing the use of imported fuels. Accelerated deployment of renewables, plus the further electrification of transport and heating, could have a transformative impact in this regard.

However, while this transition stands to reduce EU dependence on foreign fuel suppliers, one consequence would be higher dependence on imported raw materials and technology. As discussed, China is the dominant global supplier of such materials and products, and has demonstrated a willingness to use this leverage, imposing export controls on critical minerals and associated technologies. The transition also introduces a new dimension to managing energy security: because renewable generation relies on inherently variable energy sources such as wind and sunshine, efficient management of supply and demand in the electricity system becomes all the more important. In particular, ensuring sufficient flexibility in electricity networks is critical – for example, through assets such as cross-border interconnections and energy storage. As grids expand and become highly digitized, and as a greater share of energy is consumed in the form of electricity, cybersecurity will also become an increasingly vital element of EU energy security (see also Chapter 3).